NFLX: Successfully Resisted the Market Meltdown but is There Any Upside Left?

Source: TradingView

Investment Thesis

TradingKey - Netflix was spared from the recent market drop as entertainment historically has been pretty resilient in tougher economic times. The recent Q1 results demonstrated that the flywheel is working well with high quality content keeping user stickiness, generating cash that is invested in even more content. Also, the company rides the wave of a secular trend – the transition from cable TV to streaming. However, the valuation seem quite high at 50x PE and after the market drop, there seem to be more attractive names in the tech sector.

2025Q1 Results Review

In contrast with the recent doom and gloom across the markets, and the tech sector in particular, Netflix came up with a very solid first quarter, beating the estimates both in terms of EPS and revenue.

- Earnings per share: $6.61 vs. $5.71 expected (25.3% year-over-year growth)

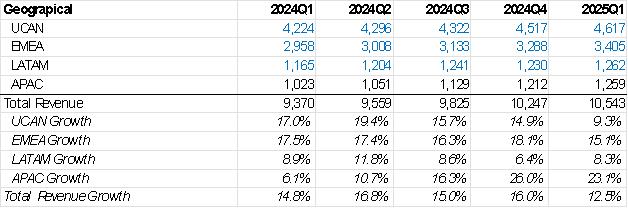

- Revenue: $10.54 billion vs. $10.52 billion expected (12.5% year-over-year growth)

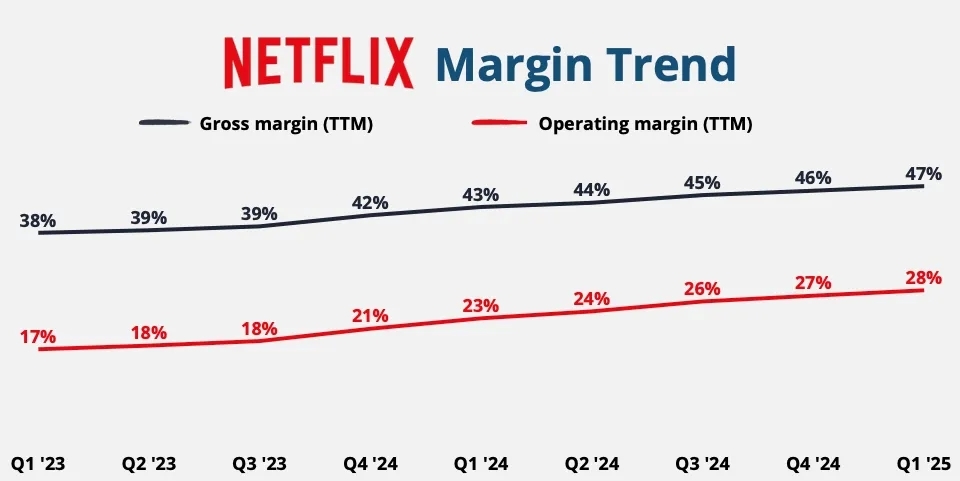

While revenue was relatively within the expectations, the big positive surprise came from the profitability improvement (EPS number). The gross margin for the quarter was 50.1% vs 46.9% a year ago, while the operating margin was 31.7% vs 287.1% in 2024Q1.

The operating cash flow stood at 2.79 billion, 26% higher than 2024Q1.

Starting from this quarter, the company will not be reporting subscription numbers, implying that the main focus will be monetization and profitability rather than user acquisition, which means the margin expansion we saw in Q1 is a proof of a strong management execution.

Source: appeconomyinsights.com

On the business operation side, the company is focusing on two fronts – ad business and improvement of content.

The ad business retains its momentum. It appears that users react positively to the lower priced ad-supported plans and currently the ad revenue has already reached a mid-single percentage of the total revenue, and this percentage will continue to grow.

When it comes to major titles for Q1, Adolescence, which turned into one of the biggest successes in the history of the platform with 124 million views

Top Q1 Shows:

· Adolescence (124M views).

· The Night Agent S2 (50M views).

· Running Point (36M views).

Top Q1 Movies:

· Back in Action (146M views).

· The Life List (67M views).

· Ad Vitam (63M views).

Overall, the flywheel of Netflix remains intact with improved profitability bringing more cash flow, which is then used to invest in quality content.

The “Unofficial” Guidance

Last month, a senior staff of Netflix revealed certain long-term goals for the company and even though this is not an official management guidance, it does show how the management sees the future:

By 2030, Netflix executives want to:

· Bring market cap to $1 trillion from $440 billion currently

· Double revenue—from $39 billion in 2024 to $78 billion. (Roughly +12% CAGR)

· Triple operating income—from $10 billion in 2024 to $30 billion (Roughly +20% CAGR)

· Bring ad revenue to roughly 12% of its total revenue ($9 billion) —up from a mid-single-digit share today. (Roughly +30% CAGR)

For the operating income to triple in the next six years, it must grow at a 20% CAGR, primarily fueled by 12% annual revenue growth and the operating margin expanding to 38%. This is key to Netflix’s plan: modest top-line growth, amplified into stronger bottom-line gains.

Outlook

Source: SEC Filings, TradingKey

Even though we observe a certain slowdown in revenue growth, we do expect the annual top line growth to be maintained at 10%-12% due to several tailwinds:

- Expansion of ad-supported business

- Continuing investment in content, maintaining user stickiness and ability to increase pricing smoothly. Currently Netflix is about to roll out new seasons of its three biggest hits by total hours watched in 2025: Squid Game S3, Stranger Things S5, and Wednesday S2.

- Cord-cutting in UCAN

- Further penetration in Europe, Asia and Latin America

However, the main contributor of the earnings growth will not come from the top-line but from the margin expansion.

The single biggest expense in the P/L statement for Netflix is the content amortization which is part of the cost of revenue. Throughout the years, amortization significantly decreased as a percentage of revenue from 48% in 2018 to 36% in 2025Q1, implying that amortization grows at a slower rate than revenue does. As growth in amortization is related to growth of content, we do expect amortization to remain stable as the growth of content in the balance sheet has been quite flat in the last three years.

Source: SEC Filings, TradingKey

Source: SEC Filings, TradingKey

Another tailwind for margins is the ad business. Historically, the media advertising has been among the highest-margin industries – Comcast (CMCSA), for instance, has a gross margin of over 70% - much higher than the current Netflix margin of 47%

We also expect Netflix to control its future marketing spending, as they already have an established product.

Competition

An important feature of the streaming industry is the competition. Compared with other big tech firms that have a comfortable market share, Netflix still has to compete with several other strong players like YouTube, Prime, Hulu and Disney+ for the viewers’ attention.

Netflix still remains the most profitable of them all. Disney streaming business just turned profitable in 2024 while for Prime we do not have an exact number, but it is not expected to be significant. The much-advanced profitability allows Netflix to invest in more content, which is already a big advantage against its peers.

Source: appeconomyinsights.com

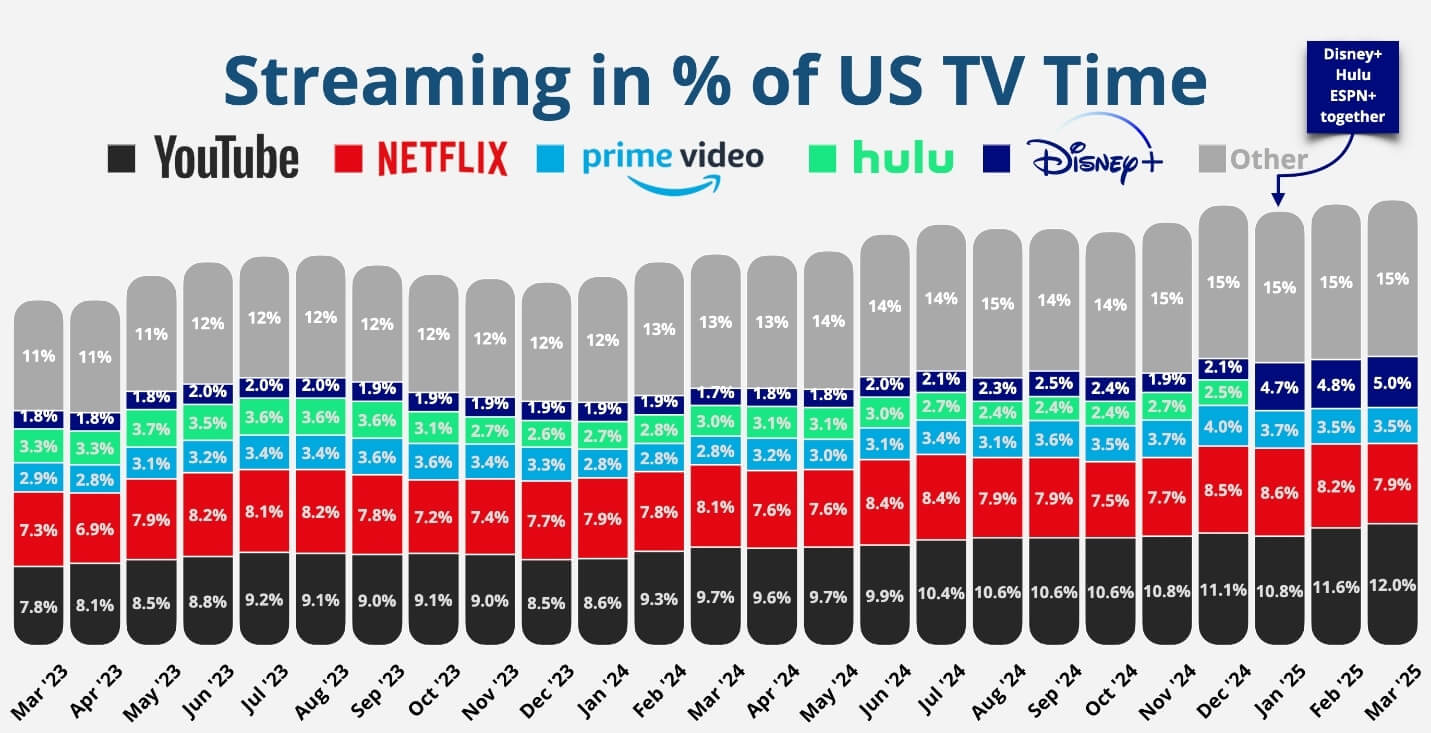

YouTube is leading Netflix when it comes to engagement, and there is a big increase in YouTube share from 7.8% to 12.0%, while Netflix has been rather flat. We believe YouTube video format is not a direct competitor to Netflix, as YouTube is more engaged with vlogs, music videos and short videos while Netflix is primarily movies and TV shows. Thus, we do not consider it as an immediate threat

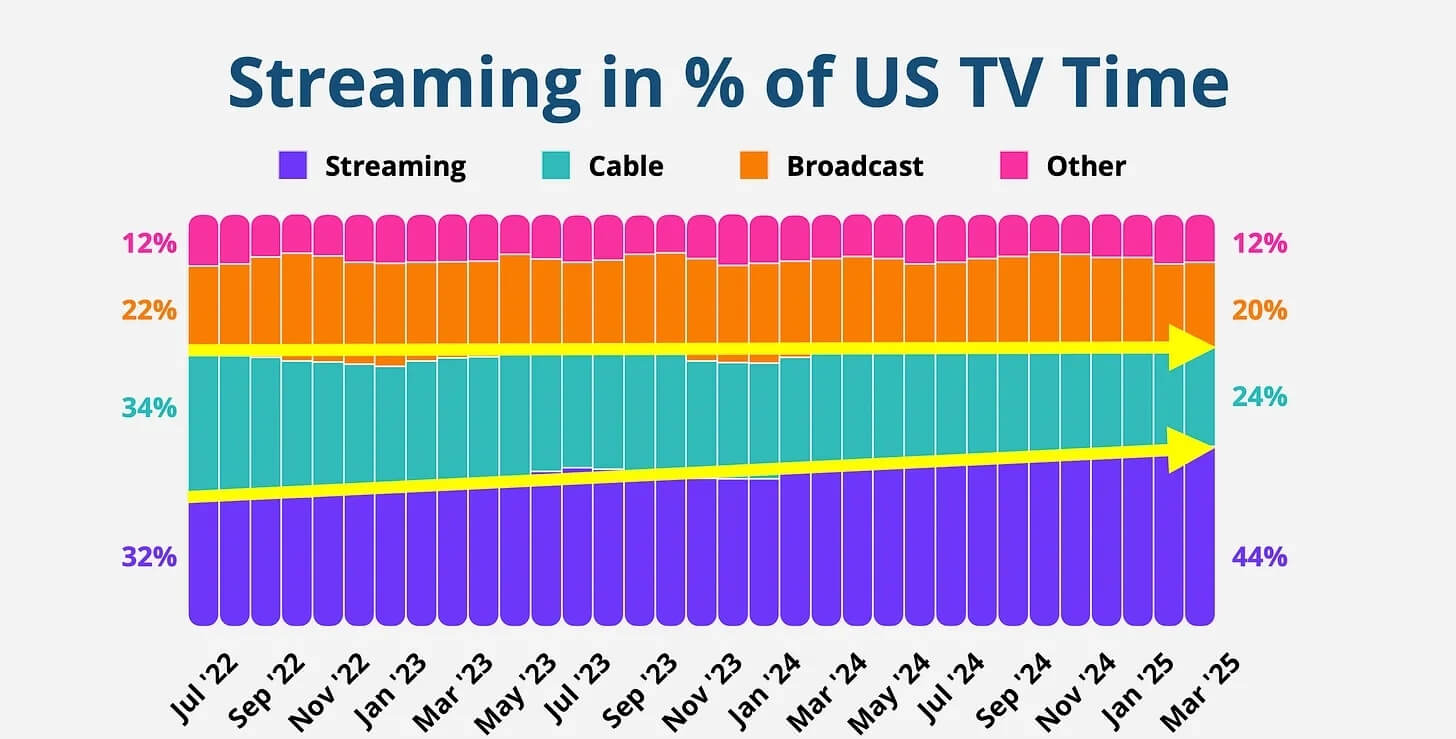

However, the trend of cord cutting (cancelling traditional cable TV in favor of internet streaming) is under way, benefiting all of the streaming players and making the competition between them less intense. According to Nielsen, streaming accounted for 44% of US TV Time in March, up from 39% a year ago and an all-time high. That gain came directly at Cable’s expense, a segment now representing a 24% market share, down from 28% a year ago.

Source: appeconomyinsights.com

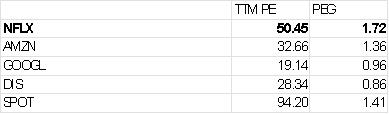

Valuation

It is not a simple task to grasp the valuation of Netflix, as the closest competitors YouTube, Prime and Disney+ are not stand-alone stocks but part of larger companies with other, very different business lines (GOOGL, AMZN and DIS). But if we compare the TTM PE and the PEG ratios with Netflix, we can see they are significantly lower, implying NFLX is already quite generously priced.

A potential suitable peer for comparing is Spotify, the music streaming platform, with a business model almost identical to Netflix (streaming business with growing ad business). SPOT PE stands quite high at 94x but the earnings also grow at a much higher rate as the company is earlier stage compared with NFLX, and after we compare the PEG ratios, it seems that SPOT is more of a bargain.

However, even Spotify cannot be a perfect one-to-one comparison, as the company is in much earlier stage of development than Netflix (higher growth and higher valuation) and also Spotify is engaged in music while Netflix is engaged in TV shows and movies.

Source: SEC Filings, TradingKey

Risks

Competition risk remains the most serious one and there is still a level of uncertainty in ROE on whether a content becomes successful or not.