GOOGL: Q1 Results Were Okay but not Impressive

Source: TradingView

Investment Thesis

TradingKey - We maintain our positive stance on Alphabet after the Q1 earnings. We do expect certain level of macro headwinds to affect the growth within the advertising business and also the increased capex would result in higher level of depreciation, affecting the profitability. Despite the signs of a slowdown in the earnings growth, the valuation still remains quite attractive at just 21 times the forward 2025 earnings – almost at the lowest level within the last ten years. We do expect positive development from the cloud business and from the improved AI capabilities, that can drive the earnings growth in the future.

2025Q1 Results Review

- Earnings per share: $2.81 vs. $2.01 expected (48.8% year-over-year growth)

- Revenue: $90.23 billion vs. $89.12 billion expected (25.3% year-over-year growth)

Google first quarter results were good but cannot be considered impressive with revenue slightly beating the expectations. On the EPS side the surprise seems quite big (80 cents) at first glance, however, this was due to much higher-than-expected gains from a one-off private investment of nearly $9 billion which is not related to the company’s direct operations.

Margins also improved a bit with a 59.7% gross margin vs 58.1% in Q1 last year, and 33.9% operating margin vs 31.6% one year ago.

Other notable business lines were rather in-line or even below the estimates:

YouTube

YouTube ad revenue was slightly below expectations:

YouTube advertising revenue: $8.93 billion versus $8.97 billion (10.3% year-over-year growth).

However, this does not include the revenue YouTube generated from subscription, which was 15% year-over-year.

Cloud

Google Cloud revenue: $12.26 billion versus $12.27 billion (28.1% year-over-year growth)

Cloud margins, however, have been rather flat in the last three quarters, despite this being the fastest growing business within the company:

Source: TradingKey, SEC Filings

Outlook

During the earnings call, the management mentioned a slowdown in business due to the more complex economic environment. We do believe that advertising has a cyclical nature, and we expect a slight slowdown in ad revenue growth to high single digits.

However, we expect the total revenue growth for 2025 to still be in the range of 10% due to ramping up subscription revenue (mainly from YouTube) and the still-growing cloud business.

The revenue growth for cloud continues to be quite high at 28%, but we are yet to see any updates on the supply/infrastructure bottleneck. Further, we are expecting updates from the other two main cloud players, Amazon and Microsoft, to report results, so we can draw a clearer picture on the current state of the cloud industry.

In terms of profitability, Q1 operating margin was record high at almost 34%, however there might be certain headwinds to it in the coming quarters.

With the significant capex ramp-up, we are expecting depreciation to grow at a much higher rate than the revenue. Q1 depreciation increased 31% from $3.4 to $4.4 billion and we do expect this number to increase significantly as the company has already spent a lot on AI infrastructure in the form of data centers and servers.

Also, we expect headwinds from both the slowdown of the economy and the intensified competitive landscape for ad players.

Despite these factors slowing the margin expansion, we do believe we will see slightly higher OPM in 2025 as the company improves its economies of scale, as well as further profitability expansion in cloud.

Valuation

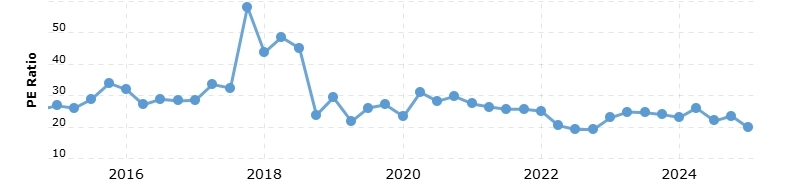

With expected EPS of $7.94 for 2025, GOOGL is traded at 21 times the forward earnings. The trailing twelve moth PE has been also at similar level – 22 times.

Source: macrotrends.net

Both these numbers are almost at the 10-year historical low. A target multiple of 30x may be a bit generous for GOOGL, due to the not-so-high growth rate in earnings, but 25x PE sounds very reasonable, implying $200.00 target price and 20% discount.

A major determinant for Alphabet this year will be the outcome from the legal anti-monopoly cases the company is involved in. During the earnings call, the management did not share any updates on the legal processes, but we guess we have to wait till the middle of the year for more clarity.