[Reuters Analysis] Tariff-driven Wall Street pain sparks investors to weigh more gloomy scenarios

NEW YORK, April 8 (Reuters) - A dramatic U.S. stock slide is fanning fears of even more dire scenarios for the market, as investors weigh the potential for a prolonged global trade war and a much dimmer corporate profit outlook.

Stocks swung wildly on Monday, with the benchmark S&P 500 .SPX down well over 4% at one point, as investors continued to grapple with President Donald Trump's sweeping tariffs that last week drove the biggest weekly drop for the stock market since the onset of the COVID-19 pandemic five years ago.

With so much unclear about where the tariff battle will lead, Wall Street strategists contemplated how much more of a beating stocks could take, including that the S&P 500 could fall by nearly half from its February 19 all-time high. The index ended on Monday at 5,062.25, down more than 17% from that peak.

Matthew Maley, chief market strategist at Miller Tabak, said a decline in the S&P 500 in coming months to 4,300 was "very possible," and a fall to 4,000 or lower was not out of the question. Trade tumult aside, Maley said, markets had been overly optimistic about the near-term profit potential from artificial intelligence and not properly factoring in weakening consumer behavior.

"This is more than tariffs," he said. "This is the process of the market falling back in line with its underlying fundamentals."

The worst-case scenarios from some analysts saw the S&P 500 dropping as much as roughly 50% from its all-time high, which would be akin to the aftermath of the bursting of the dot-com bubble in 2000.

The recent drop has been one of the steepest concentrated selloffs for U.S. stocks, on par with the speed and intensity of drawdowns seen during the COVID-19 swoon in 2020 and the financial crisis slide in 2008, and has put the S&P 500 close to bear market territory.

The S&P 500's combined 10.5% decline last Thursday and Friday was the index's fourth biggest two-day drop since 1950, according to Keith Lerner, co-chief investment officer with Truist Advisory Services. The biggest two-day falls occurred in March 2020, when COVID-19 was hitting; in November 2008, during the financial crisis; and in 1987, for the two-day period that included Wall Street's "Black Monday."

Despite the wild swings on Monday, the S&P 500 ended down just 0.2%. Even so, the Cboe Volatility index .VIX, Wall Street's "fear gauge," registered its highest closing level in five years.

JPMorgan equity strategists on Monday outlined a year-end S&P 500 target of about 4,000 as their "bear case," which included assumptions of no tariff relief and a 2026 earnings view that implied two years of no real profit growth.

Evercore ISI offered a "bear" outcome of 4,500 for the S&P 500 and a "SuperBear" case of 3,100, which would be a drop of nearly 50% from the February high. The SuperBear scenario involves a recession that takes down annual corporate profits by about 15%, as well as disruption in credit markets and difficulty raising the debt ceiling, Evercore strategists said in a note on Sunday.

Michael Purves, CEO of Tallbacken Capital Advisors, said a combination of "some (valuation) contraction, some earnings contraction" could push the index down to 4,000.

"It's not an unrealistic scenario at all," Purves said.

Like Purves, investors pointed to two potential reasons that create the potential for further weakness in stocks: valuations that are moderating from expensive levels and the possibility of more severe cuts to earnings estimates.

The forward price-to-earnings ratio for the S&P 500 fell from 22.4 times expected 12-month earnings in February, to 18.4 as of Friday, which is in line with the index's average P/E ratio of the past 10 years, according to LSEG Datastream.

But the longer-term 40-year average P/E ratio is 15.8 -- still 14% below Friday's level. The P/E ratio sank to as low as 15.3 as recently as 2022, when the Federal Reserve was raising interest rates to bring down spiking inflation.

Current valuations also are based on earnings expectations that many investors say have yet to adequately reflect the likely economic damage from the tariffs.

S&P 500 earnings are still expected to rise 10.4% in 2025, according to an LSEG IBES report on Friday. However, during recessions, earnings fall at an average annual rate of 24%, according to Ned Davis Research.

"If it's a 50% probability of recession, you've got to look at another 20%-25% down in equities from here," Colin Graham, head of multi-asset strategies at Robeco in London, said during trading on Monday.

To be sure, even investors who feared steep fallout for stocks did not think these were the most likely scenarios.

Evercore strategists, for example, on Sunday set a year-end price target of 5,600 for the S&P 500, or a 10% gain from current levels, even as they described more negative potential outcomes.

Markets also could be poised to rally on any news of possible trade relief. Stocks briefly rose on Monday on a report that said Trump was considering a 90-day pause on tariffs, before the White House denied the report, sending the market lower.

"The only thing that's going to help both sentiment and the market's direction is going to be some easing of the entrenched tariff views," said Michael James, managing director of equity trading at Rosenblatt Securities. "We're going to need some form of moderation on those tariff levels to have any potential for meaningful improvement."

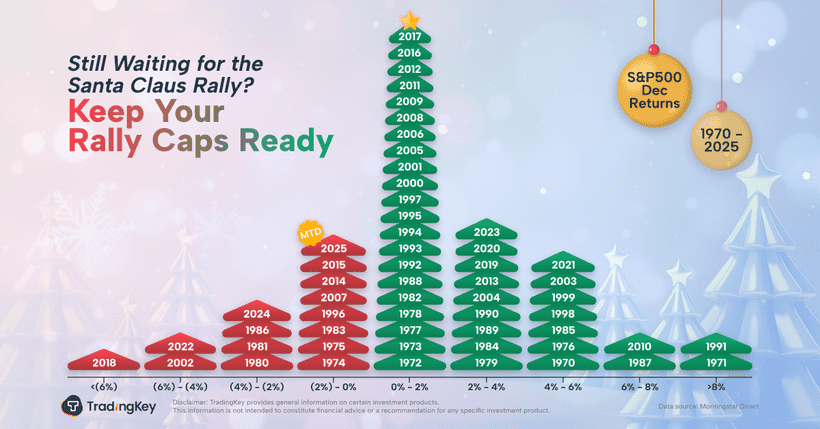

GRAPHIC: Historically big swing