Robinhood's Quiet Resurgence: From Meme Broker to Fintech Platform

- Robinhood flipped from a $541M loss to $1.41B net income in 2024, driven by 58% revenue growth and a 21% reduction in operating expenses.

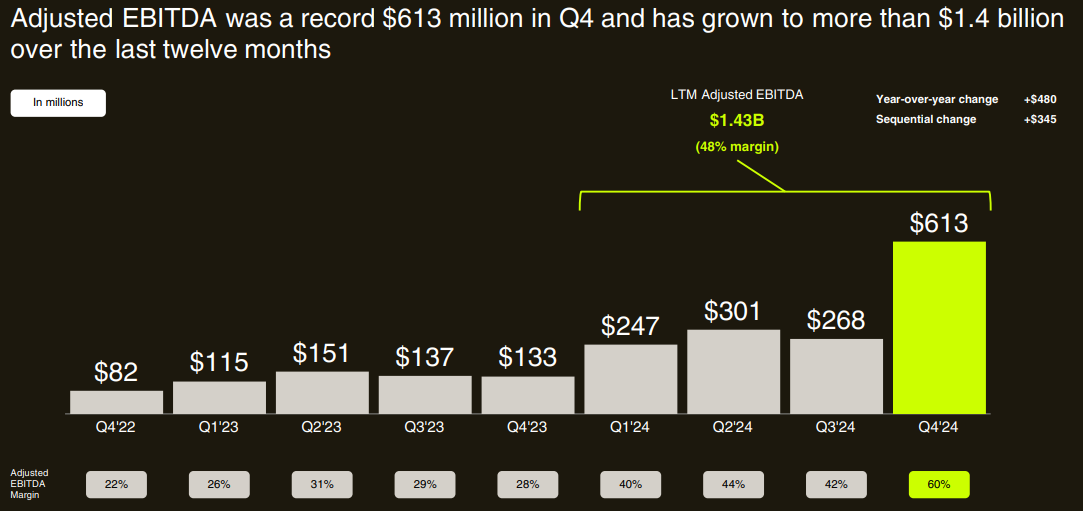

- Adjusted EBITDA rose 167% YoY to $1.43B with a 48% full-year margin, reaching 60% in Q4—outpacing legacy fintech and SaaS firms.

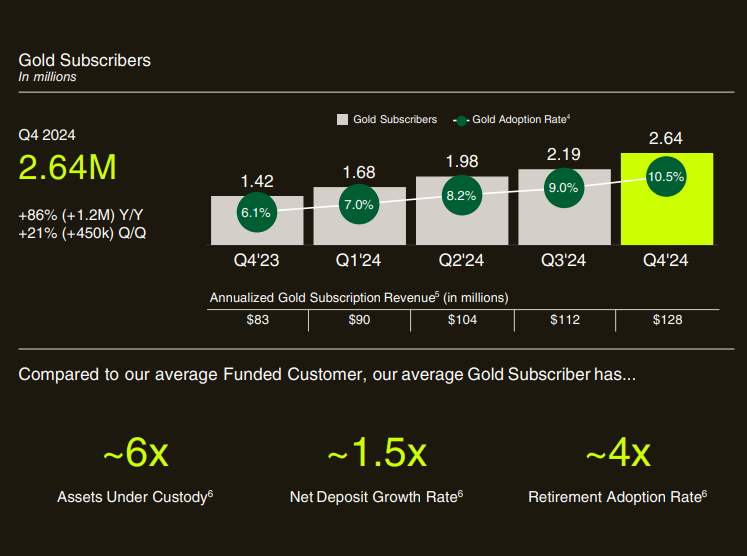

- Funded accounts hit 25.2M (up 88% YoY), with AUC at $193B, driven by higher ARPU ($164) and 2.64M Gold subscribers.

- Robinhood launched futures, index options, IRAs ($13.1B assets), and a Gold Credit Card with 3% cashback—accelerating wallet share and retention.

TradingKey - For years, institutional investors wrote Robinhood (HOOD) off in unqualified terms as a retail trading flash-in-the-pan, a beneficiary of a pandemic-driven speculative mania. No more. The company's 2024 results and recent strategic disclosures show a platform in advanced evolution. With rapidly diversifying revenue stream, growing operating leverage, and substantial thrusts in crypto custody, advisory services, and international expansion, Robinhood is stealth-building one of the most efficient, scalable consumer fintech firms in the business.

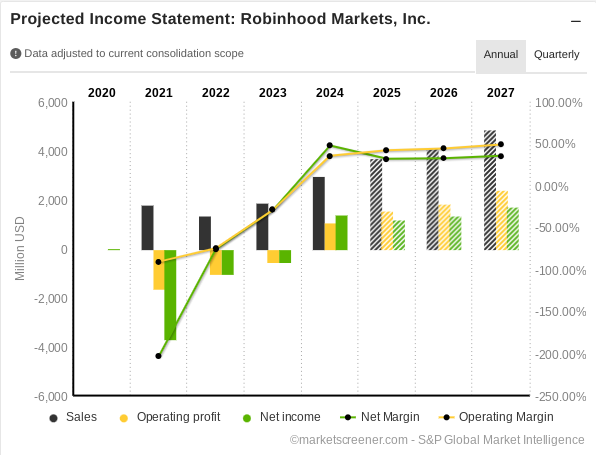

The change at Robinhood is more than skin-deep. Full-year 2024 net income reversed from a loss of a year ago of $541 million to a profit of $1.41 billion, supported by a 58% rise in revenues while operating costs fell by 21%. Adjusted EBITDA jumped a year-over-year 167% to $1.43 billion, with a margin of 48%, keeping pace with or catching up with many legacy SaaS competitors. The company has assets under custody of $193 billion and funded accounts of 25.2 million, up year-over-year by 88%, demonstrating a clear unscoping from transactional revenue-only to more wallet depth penetration and more sustained user economics.

The Street continues not to value Robinhood's upside. There are regulatory risk, crypto exposure, and payment-for-order-flow risk issues lingering, but the firm's future path, into margin lending, advisory custody, index derivatives, and tokenization rails, already looks more like a vertically integrated financial super app. Robinhood, in early 2025, is under 5.5x EV/EBITDA, and under 17x forward EPS. That ain't a meme. That's a misprice.

Source: marketscreener.com

From Trades to Tectonics: The Evolution of Robinhood's Business Model

The strength of Robinhood was always in keeping things simple: commission-free trading from a mobile-first platform. The business model underneath has modified, though. Robinhood's revenue in 2024 was $2.95 billion, of which 56% was transactional revenue and 38% was net interest revenue. Crypto trading, once dismissed as market noise, was $358 million in Q4 alone, more than up more than 700% from last year, and supported by the institutional order flow from Bitstamp pending acquisition approval.

What is most telling, however, is rising monetization per user. Average Revenue Per User (ARPU) grew year-over-year by a two-fold increase to $164, thanks to product stack growth. Robinhood Gold, its subscription product for $5 per month, has 2.64 million members, with the users averaging 6x assets in average balances generating a subscription revenue of $128 million in the run rate annually. This recurring stream provides Robinhood a base of steady, high-margin income overlaid above trading volatility.

The diversification by the firm is not by chance. In addition to equities and options, in 2024 Robinhood launched Robinhood Legend for professional traders, futures, index options, and a waitlisted Gold Credit Card with a cash-back rate of 3%. Robinhood expanded into retirement business with retirement assets growing more than 600% year-over-year, up to a total of $13.1 billion. This is not product expansion, this is vertical integration throughout a investor's lifetime.

Most under-recognized, perhaps, is the firm's growing efficiency in terms of capital. With more than $5 billion in corporately held liquidity, a margin book close to $8 billion, and cash sweep balances of $26 billion, Robinhood is a de facto high-yielding bank in fintech clothing. And doing so through tech margins, not branch economics.

Source: marketdataforecast.com

Standing Out: Robinhood's Uniqueness in a Competitive Fintech Space

Fintech brokerage is a highly competitive industry, with industry stalwarts such as Charles Schwab, Fidelity, and E*TRADE supported by the weight of institutions. Meanwhile, new entrants such as Public, SoFi, and Webull fight for share of niches. However, Robinhood has established a distinctive moat: a mass-market mobile base of highly engaged users, wide product exposure, growing per-user economics, all within a brand identity crafted for the next gen.

Robinhood's price advantage continues to hold up. The platform has the tightest average crypto trading spreads of the major brokerages, as well as margin rates highly competitive with industry stalwarts, besting traditional players by wide margins. The Gold subscription functions as a retention flywheel, combining top-shelf data, IRA match, margin access, and cash back into a high-LTV client relationship.

In contrast to most fintechs grappling with CAC inflation, Robinhood's growth is still predominantly organic. The most recent period captured a whopping $16.1 billion in net deposits and 850,000 sequentially funded account growth, the most in close to three years. This implies product velocity rather than mere spend in advertising is driving user sign-ups as well as more wallet share.

Whereas peers such as PayPal and Block are shifting towards cost discipline due to decreasing growth, Robinhood is doing both: expanding top-line 115% year-over-year while keeping adjusted operating costs basically flat quarter-over-quarter. Even Schwab, with scale, can't keep up with Robinhood's 60% adjusted EBITDA margin in Q4.

Nevertheless, there are risks. The RIA and retirement channels are controlled by Fidelity and Schwab, a marketplace Robinhood is accessing only just recently through the acquisition of TradePMR. The firm's appeal among Millennials and Generation Z, with a median client age of 35, has to be countered by credibility in higher-asset, older demographics.

Engines of Eion: The Financial and Strategic Flywheels of HOOD

Robinhood's strategy in 2025 focuses on three pillars: domination of active traders, penetrating wallet share in Millennials and Gen Z, and creation of a global financial ecosystem. On all these fronts, the firm is laying solid foundations.

Active traders, first. Robinhood Legend's introduction, along with index futures, brings Robinhood into the pool of high-frequency users with substantial notional volumes. Equity volumes in the most recent quarter grew 154% year-over-year, while crypto volumes grew more than 400% to a total of $71 billion. Options contracts were up by a similar margin, 61%. Significantly, these are product segments with structural tailwinds as retail usage of derivatives keeps growing.

Second, share of wallet. Robinhood’s Gold Card, with more than 100,000 users within months of launch, is not merely a credit product. It’s a monetization wedge into payments, rewards, and lending. With cash sweep balances and increasing retirement accounts, Robinhood is deploying a closed-loop system of capital around the user. The economics reflect: net deposits from Gold users increase at 1.5x the rate of average, with 4x the retirement adoption rate.

Third, globalization. Robinhood's first serious forays outside the U.S. are the pending acquisition of Bitstamp and APAC expansion beginning in Singapore. The company has obtained options trading licenses in the U.K. and has plans in three more countries. Bitstamp, with assets under administration of $40 billion, introduces Robinhood to institutional crypto custody, a burgeoning vertical in a period when the proliferation of ETFs as well as staking has made institutional adoption more viable.

On profitability, Robinhood's scaling economics are phenomenal. Its revenue per employee is more than $800,000, as of today, while its incremental EBITDA margin in 2024 was 82%. Adjusted EBITDA margins were as high as 60% in Q4, from 28% a year ago. Such a margin expansion, along with adding more than a1.8 million funded users, implies strong unit economics even before international scaling takes effect.

Source: Q4-Deck

What's It Worth? A Premium Multiple or a Misunderstood Compounder?

The valuation of Robinhood has become a hot topic of contention, and not unfairly. Using traditional metrics, the stock appears to be richly valued relative to peers, but it overlooks the intrinsic optionality and operating leverage that characterize the business today.

With a forward P/E of 22.64 and trailing P/E of 18.71, Robinhood is at a 137% and 80% premium, respectively, to the industry median. PEG (FWD) is at 3.23, more than 200% higher than peer averages, highlighting warning signs that the stock's price might be rich in relation to anticipated near-term earnings growth. The forward Price/Sales ratio of 8.26 and trailing P/S of 10.3 are similarly above the sector median of 2.39 and 2.67, respectively. The numbers indicate investors are factoring in unusually large growth and monetization upside.

The comparison, however, gains nuance in the context. Robinhood's capital-light business, tech-native margins, and vertical integration support a structurally higher return profile compared to traditional brokers. The platform achieved 60% adjusted EBITDA margins in Q4 and 48% for the year, unusually for a business with 25+ million funded accounts and just 1% market penetration of its estimated $600 billion TAM. In contrast with peers dependent upon net interest spread or asset management fee-driven economics, Robinhood monetizes across a broad stack, from derivatives and subscriptions, through cash sweep, crypto, and payment rails.

The firm also trades at 5.4x trailing EV/EBITDA, comfortably lower than the industry median of 10.4x, indicating that even though headline multiples are generally low, underlying cash profitability is still attractively valued. Price/Book of 3.73 is over 270% higher than the industry median, but a reflection of the firm's high-margin, IP intensive business model.

Although the present price implies a growth multiple, the compounding in the platform, especially with advisory, credit, and cryptocurrency custody in infancy, warrants a fair value of between $15 and $20 per share. If, in addition, Bitstamp and TradePMR are successfully integrated, bringing in EBITDA of $80 million to $120 million, Robinhood's PEG ratio can quickly compress, warranting today's multiple.

Source: Q4-Deck

Risk Profile: Macro Volatility, Regulation, and Brand Stretch

Robinhood's regulatory risk is its largest structural hazard. While Payment for Order Flow was not specifically banned in recent SEC plans, a negative decision regarding the transparency of order execution or crypto custody would impact transaction margins. Also, the company's large crypto volumes, close to half of transaction revenue in Q4, subject it to price risk and headline risk.

Second, macroeconomic factors, such as declining interest rates, would squeeze the $296 million in quarterly net revenue from interest, most notably from cash sweep and margin loans. If this were the case, fee-based revenue would be even more crucial.

Third, brand evolution is a risk. Robinhood is attempting to scale upmarket into global markets and advisory services while maintaining its youth-driven brand. Slip-ups in compliance, customer support, or cultural localization might stymie adoption, especially in high-trust verticals such as retirement planning and institutional custody.

Lastly, since dilution is moderate, the company is likely to issue equity to cover payment for Bitstamp and TradePMR employees, leaving some sort of overhang for valuation.

Source: Q4-Deck

Overall Takeaway

Robinhood is no longer a single-dimensional retail brokerage. It's a product-dense, capital-light, rapidly-scaling fintech platform with global, institutional aspirations. Where the market perceives volatility, we perceive optionality. The stock merits a strategic re-rating, and long-term capital should take notice.