GRAB: From Growth Engine to Cash Machine

- Q4 2024 adjusted EBITDA jumped 173% YoY to $146 million, driving $253 million in operating cash flow and confirming platform-wide leverage.

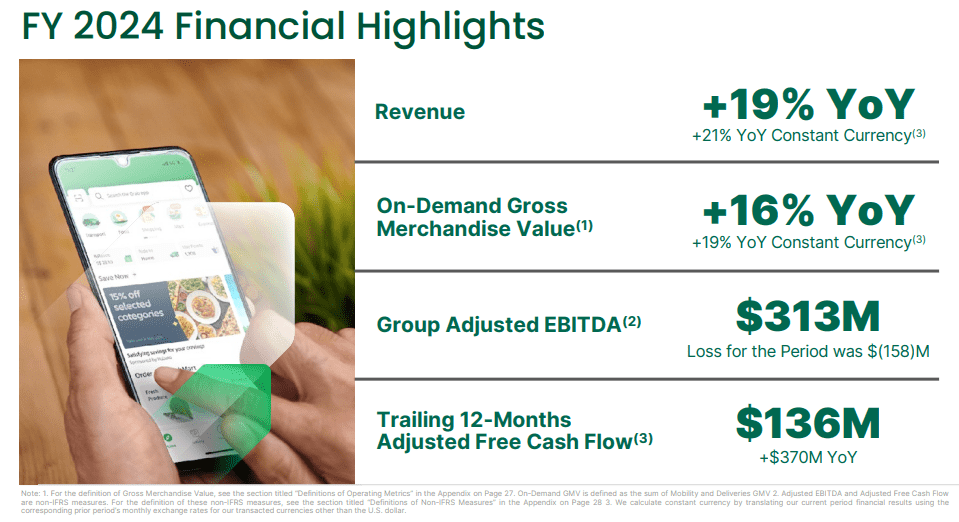

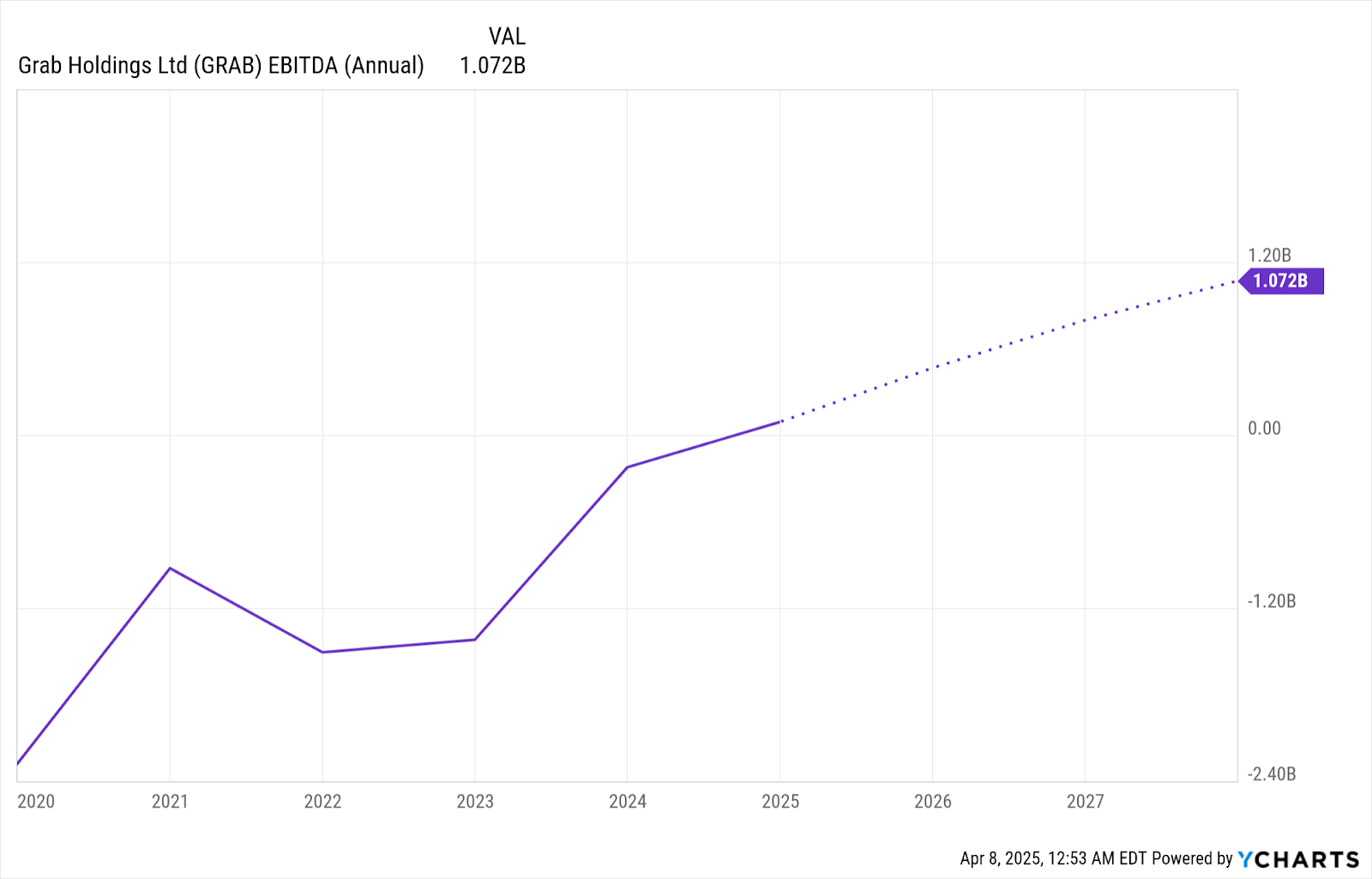

- Full-year 2024 adjusted EBITDA reached $313 million vs. a $22 million loss in 2023; free cash flow flipped to +$136 million from -$234 million.

- Mobility delivered $569 million EBITDA with 8.6% margin on $6.6B GMV (+23% YoY), driven by 26% adoption of Saver tier transport rides.

- Deliveries posted $196 million EBITDA (+140% YoY) on $3.2B Q4 GMV, with 42% of orders now using tiered delivery offerings like Saver and Priority.

TradingKey - Grab (GRAB) starts 2025 with a compelling story of transformation. No longer stuck in the growth-capital story with a heavy baggage of incentives, Grab has now become a company with unit economics proven, platform-wide operable leverage, and a deepening digital financial ecosystem that could match regional banks. The Southeast Asian superapp finished 2024 with its initial full year of positive adjusted EBITDA ($313 million) as well as free cash flow ($136 million) as a result of a dramatic $370 million YoY turn in cash creation. In the face of 19% YoY revenue growth on a constant currency basis, Grab has at last shown itself to be able to scale profitably in a market characterized by logistical density as well as regulation heterogeneity.

This evolution isn't just a financial one, it's structural. Strategic vertical integration of mobility, deliveries, and digital banking has strengthened customer retention as well as monetization per user. At a deeper level, however, Grab's AI investments, from batching algorithms for deliveries to merchant-facing auto-tools, are no longer speculative phenomena, now, they're quantifiable efficiency drivers. By putting hyper-localized product design alongside back-end auto-mation as well as disciplined incentive use, Grab is now a high-margin platform business in form, not a rideshare-adjacent logistics company. Its most recent quarter (Q4 2024) delivered 173% growth in adjusted EBITDA along with $253 million in op cash flow, driven by both topline expansion as well as corporate cost synergies.

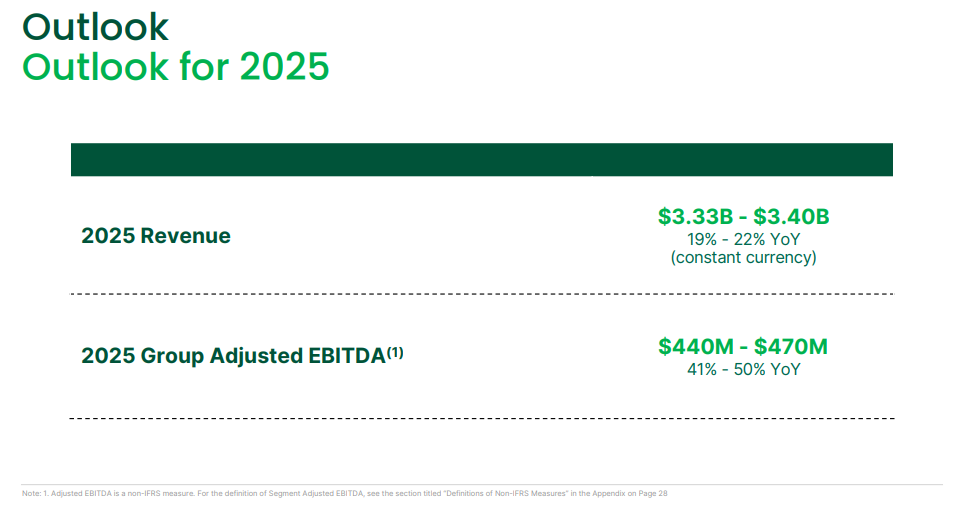

Against a backdrop in which peers such as GoTo and Sea Limited struggled with slowing growth and ecosystem expansion, Grab's consistency, and by extension, restraint, has proven a winning strategy. The $440–$470 million of 2025 adjusted EBITDA guidance and as much as $3.4 billion of revenue guidance speaks to 41%–50% EBITDA growth, indicating continued inflection in earnings power. Macro risks abound, most notably FX volatility in the ASEAN markets, yet the trajectory reflects a lean operator with a defendable ecosystem nearing platform maturity.

Source: FY2024 Deck

A Tri-Segmented Flywheel: From Mobility to Monetized Ecosystem

Grab's business model nowadays has three synergistic engines at its base: Mobility, Deliveries, and Financial Services. Each of them has grown from transaction-based growth into monetization-focused flywheels with cross-selling opportunities as well as built-in network effects.

The Mobility segment remains the market leader in size and profitability. Contributing $569 million in segment EBITDA on its own, it delivered $6.6 billion GMV in 2024 (+23% YoY) with a strong 8.6% adjusted EBITDA margin. Of special note, the deployment of Saver transport rides, representing 26% of Q4 rides, doubled the growth of Standard rides while improving user engagement (transaction frequency 1.5x higher). This tiered pay-as-you-go model grows addressable demand at the same time as preserving unit economics.

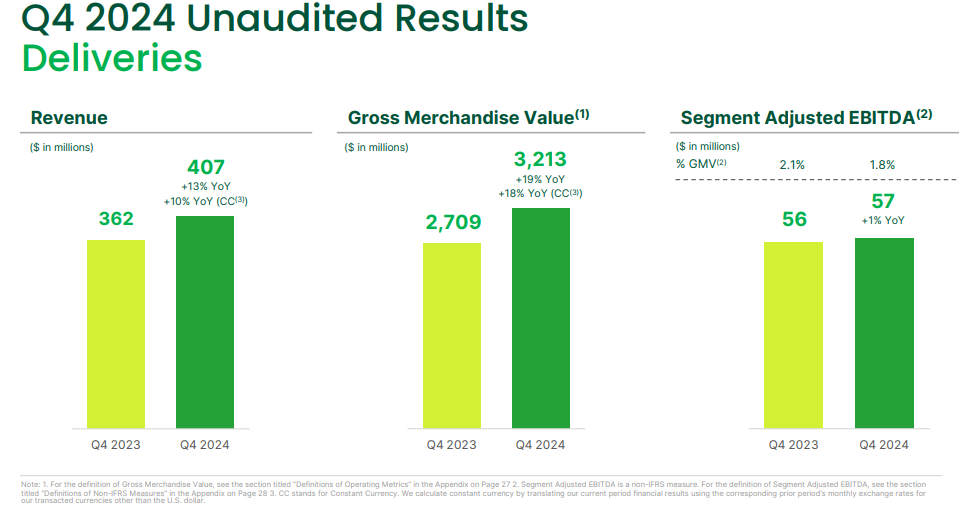

Deliveries, previously a margin-strained business, is also indicating structural efficiency. Q4 GMV was $3.2 billion (+19% YoY) on the back of innovations such as Saver Deliveries and Priority Deliveries, which by quarter accounted for 42% of all transactions. Deliveries' 2024 segment EBITDA was 140% YoY higher at $196 million despite Q4 margin compression to 1.8% as Grab invested in batching algorithms and user acquisition. Notably, the advertising engine attached to Deliveries is taking hold, adding $216 million of annualized revenue as well as enhancing merchant monetization, an often-overlooked margin driver.

Financial Services is transforming from a cash burn hub into a growth pillar of the future. 2024 revenues rose 44% YoY to $253 million, with adjusted EBITDA losses decreasing 38% to $105 million. The overall loan portfolio was $536 million (+64% YoY), as Grab's digital banks (GXS Bank and GXBank) had $1.2 billion in deposits. Delinquency rates remaining at 2%, the lending business shows both risk discipline as well as scale. The segment is likely to breakeven by H2 2026, another structural driver.

Collectively, these segments are a self-reinforcing system: Mobility induces user onboarding, Deliveries increases engagement, and Financial Services deepens monetization with embedded finance. This flywheel framework lowers CAC, raises LTV, and buffers revenue cyclicality by business unit.

Source: FY2024 Deck

Winning the Platform War:Competitive Moats and Strategic Discipline

Grab's defensibility is not merely at scale, however, but in execution. Against its competitors such as GoTo in Indonesia or Foodpanda in the Philippines, Grab has differentiated on product localisation, density of infrastructure, and execution of operations.

While its competitors were deep into price wars, Grab concentrated on supply-demand equilibrium through algorithmic matching as well as on incentivising retention cohorts. It's reflected in Q4: regional corporate expenses fell 13% YoY, and as a percentage of GMV (10.1%), incentives were tightly managed even as GMV growth was 20%. This is compared to GoTo's sustained losses on the back of growth driven by incentives.

AI integration has become a key moat. Platforms such as GrabRideGuide and Merchant Menu Assistant enhance partner economics at scale with nearly zero marginal cost. At a company-wide level, more than 60% of engineers are leveraging AI code assistants to decrease development time and accelerate product iteration. Although Sea Limited's Shopee has also made a turn to AI, its marketplace dynamics are fundamentally different and don't include real-world operations feedback loops for its ride and delivery networks.

The advantage in financial services is Grab's in-built distribution network. 90%+ of customers of GXBank are Grab users, and Superbank Indonesia's 2.8 million customers are 60% drawn from the Grab ecosystem, leading to much lower acquisition costs. This is reflective of strategies observed in China's Ant Group or India's Paytm, only with a Southeast Asian localised moat that's difficult to replicate.

Sequencing is what Grab has excelled at: not launching aggressively, then ramping up vertically after product-market fit and margin visibility are established. This prudent strategy is currently the foundation of its high-confidence 2025 guide, as well as offering a cushion from short-term shocks, whether it is FX fluctuations, regulation changes, or seasonal fluctuations such as Ramadan and Lunar New Year.

Source: FY2024 Deck

Financial Fortitude: From Cost Controller to Cash Compounder

Grab's 2024 numbers show a company that has not just grown, but matured. Full-year revenues came at $2.8 billion (+19% YoY), as adjusted EBITDA reversed a $22 million loss in 2023 at $313 million last year. Such EBITDA was not just window dressing, it equated to $136 million free cash flow, a turn from a $234 million deficit last year. These figures confirm the company's capability to internally compound capital while preserving optionality for strategic investment.

The most lucrative vertical continues to be Mobility with $569 million of segment EBITDA, followed by Deliveries at $196 million, with Financial Services at a loss of $105 million. Regional corporate costs fell from $398 million to $350 million, a sign of continued fixed cost absorption as well as AI back-office efficiencies. Notably, the company realized $852 million of operating cash flow, supported by $1.2 billion of customer deposits as well as disciplined CapEx of $148 million.

Capital deployment is also changing. Grab bought back $37 million worth of shares in Q4 and has returned $226 million since program initiation. This is meaningful for a firm with $5.8 billion of net cash and minimal near-term refi requirements. Even with a historically dilutive comp structure, management expects <1% dilution in 2025, representing a sea change in shareholder affability.

Valuation-wise, Grab is at ~2.9x FY2024 EV/Revenue and ~21x FY2025 EV/EBITDA. It is premium relative to loss-making comparatives such as GoTo, but a steep discount to scaled fintechs or platform comparatives with similar EBITDA profiles and ecosystem depth. Using a back-of-the-envelope 20x EV/EBITDA multiple on Grab's 2025 midpoint EBITDA of $455 million implies a valuation of $9.1 billion. Net cash of ~$6 billion implies a reasonable level for the equity value at ~$3.1 billion, representing ~25% potential upside from here.

Source: Ycharts

Risk Matrix: Currency, Cyclicality, and Fintech Frag

Although fundamentals for Grab are improving, several key risks persist. In the first place, FX volatility in ASEAN markets (i.e., IDR, MYR, and PHP) can materially distort reported performance even if underlying GMV is stable. Management rightfully takes guidance on a constant currency basis, but USD-reporting generates perception gaps during macro shocks (like Trump Tariffs).

Secondly, seasonality persists. Ramadan, as well as Lunar New Year, land in Q1 2025, thus we are expecting a temporary dip in GMV prior to Q2 rebound. This temporal cyclicity, while not structural in nature, could trigger noise in quarter-to-quarter analysis.

Third, Financial Services growth, as remarkable as it is, is necessarily risk-weighted. Delinquencies are minimal (2%), yet a forced advance into MSME lending or lending to the retail market in a possible ASEAN macro slowdown may detract from risk-adjusted returns. Grab has to walk a thin line between growth and credit restraint, particularly as fintech competition becomes increasingly fierce.

Lastly, regulatory risk hangs heavy, most notably regarding digital banking licenses and inducement regimes. Grab's multi-market operations expose the company to diversified frameworks, tightening of which could stymie growth or profitability, most notably in lending and payments.

Source: theguardian.com

Conclusion: Real-time Repricing on a Platform

Grab's 2024 result signals the end of its "growth-at-all-cost" era and the start of a sustainable, margin-rich era. Having multi-segment operating leverage, sticky users, and real AI-driven productivity benefits, Grab is getting repriced by the market, not merely as a delivery or a rides business, but as a platform business with option value built into it. Short-term FX and macro risks remain, yes, but structural story is in place. Investors looking for asymmetric exposure to Southeast Asia's digitization curve would be negligent to discount Grab's new capital prudence and monetization depth.