Nvidia Results Overview and Implications

Overview

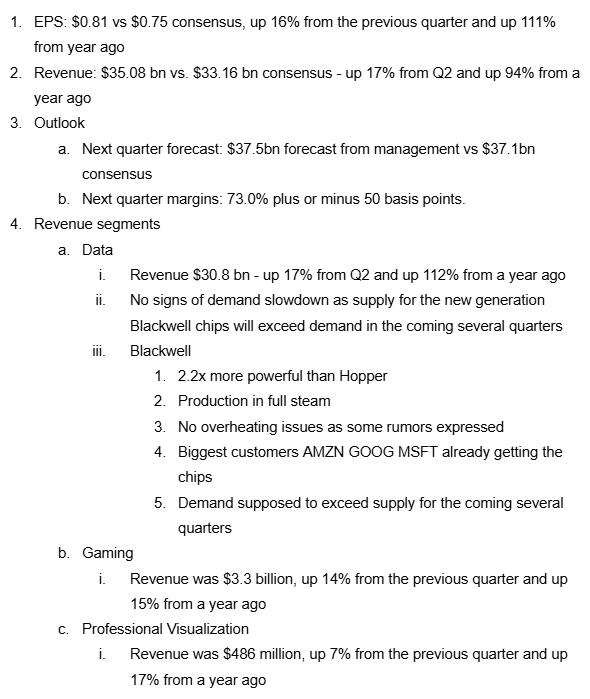

Once again NVDA results beat expectations in terms of revenue and earnings. This also comes with better-than-expected forecasts for Q4. Below are the following details from the previous quarter:

However, the initial reaction of the market was rather tepid. NVDA stock closed just 0.53% higher on the first trading day after the results were announced and dropped 3.22% the following day.

Source: TradingView

What makes investors worried about Nvidia

Not topping expectations of the same magnitude as before

Even though the revenue forecast for January quarter ($37.5bn) came above the FactSet estimate of $37.1bn, some buy-side analysts expected a $39-$40 bn range.

The guidance beat, with just $400mn, was the smallest since April 2023 and recently has always been with $1bn or more.

Supply constraints

"Both Hopper and Blackwell systems have certain supply constraints, and the demand for Blackwell is expected to exceed supply for several quarters in fiscal 2026," Nvidia said in CFO

At first glance, demand exceeding supply sounds like a problem that everyone wants to have, however any potential supply disruptions can actually be harmful for the revenue – therefore the risk is high. This is especially true in situations where a new product has been launched, which is the case with Blackwell.

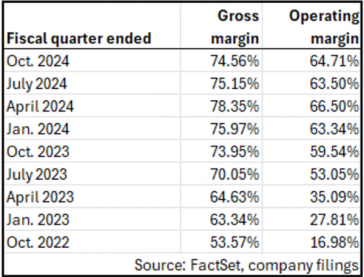

Margins Peaking

Q3 Gross Margins were at 74.6%. This is higher than a year ago 73.95%, but lower on a sequential basis where 2024Q2 was 75.15%. Operating margins are 5pp higher than 2023Q3 and 1pp higher than in 2024Q4, however they still are below the peak in 2024Q1.

The forecast for the coming quarter implies another sequential decrease in gross margin to 73%

This may be a sign of a potential intensification of the competition and price pressure from suppliers. However, the management expects the margin expansion to re-accelerate and reach the rich mid/high 70s due to the premium pricing of Blackwell.

We should bear in mind that among semiconductor companies, NVDA still has the third highest gross margin, after Arm Holdings with 97% and Broadcom with 76.6%.

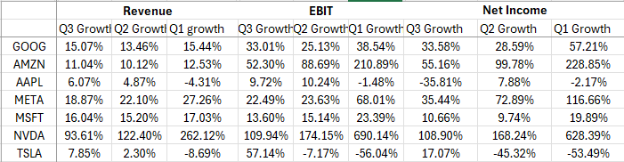

Growth de-accelerating compared with other M7 stocks

If we compare the revenue, operating income and net income growth for the past three quarters we will definitely observe that NVDA posts the largest growth rates, way ahead of any other of the rest of the M7. However, we can also observe that NVDA growth decelerates the fastest from triple digit to around 90%.

Source: TradingKey

Further, we see a deceleration on a sequential basis (Q3 vs Q2), unlike the other M7 companies which are rather stable.

Source: TradingKey

Bull and Bear Case for Nvidia

Bull Case | Bear Case |

Strong brand reputation reflected in 80%+ market share in GPU (main type of CPU that is used for AI) | High AI project failure rates - according to a recent research, over 80% of the AI-related projects fail or not able to deliver the desired result |

High obsolescence rates – In order to stay ahead, companies and especially big tech (which are the biggest customers of NVDA) have to constantly invest in the latest capabilities | Potential loss of China as a market – China brings 12.6% of NVDA revenue. Geopolitical tensions between China, the USA and Taiwan may negatively affect the company |

Expand productive capacity - a lot of the suppliers of NVDA are expanding their capacity so they can benefit from the growing demand | Growing Competition – direct competition from AMD, but also some of the customers also want to develop their own chips (AMZN) |

Investing in smaller AI startups thus trying to maintain the edge | Potential complications with launching and scaling Blackwell GPU |

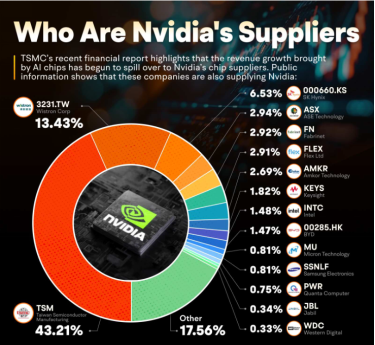

CUDA – programming language that can be used only with NVDA chips – improves stickiness among customers | Higher bargaining power from TSMC may harm gross margins. Currently, nearly half of the supplies come from TSMC, making NVDA increasingly dependent on them |

Source: Moomoo

Assumptions and Valuation

LTM Trailing P/E is at 56x. This is relatively high, no matter how we look at it. However, we should consider that NVDA is in a hyper growth stage. Next quarter they will record ~70% growth, which is a further deceleration, however with the new Blackwell GPUs, the growth will further accelerate, thus I expect growth in the range of 50%-70% for the next fiscal, where 50% is already quite conservative.

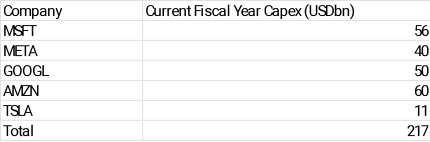

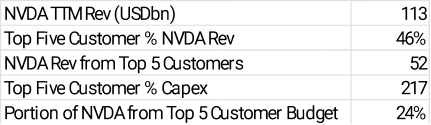

Also, NVDA has five major customers contributing nearly half of the revenue. Currently NVDA has penetrated just 24% of their budget. With the fact that, it’s very important for NVDA customers to constantly improve their computing capabilities and with their capex growing fast, NVDA can further monetize from them.

Source: TradingKey, Company Financials

Why use PEG ratio but not PE ratio

Big tech firms often have very high price-to-earnings ratios but PEG ratio with its embedded growth element can help understand if the valuation is really high or not.

If we see the PEG ratio of NVDA and its peers, we will notice how NVDA has one of the lowest such ratios at 0.64. Its direct competitor AMD is 1.12, twice higher.

Source: Reuters, LSEG

Source: Reuters, LSEG

Also if we see the historical table, the current PEG ratio for NVDA is lower than both the company average (3.74x) and the industry average (1.13x).

If we assign NVDA a PEG ratio 0f 0.80-0.90 (which seems reasonable) we will receive a stock price upside of 25%-40%, with a target price of $175-$200.

.jpg)