ECB March Policy Rate Preview: A 25bp Cut is Almost Certain, But the EU Emergency Summit Takes Centre Stage

On 6 March 2025, the European Central Bank (ECB) will announce its March policy rate decision. The market widely anticipates a 25-basis-point rate cut, lowering the Deposit Facility Rate to 2.5%. We concur with this expectation.

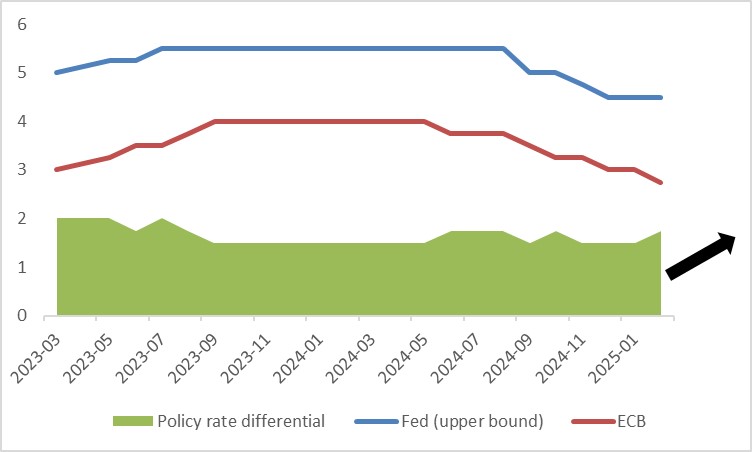

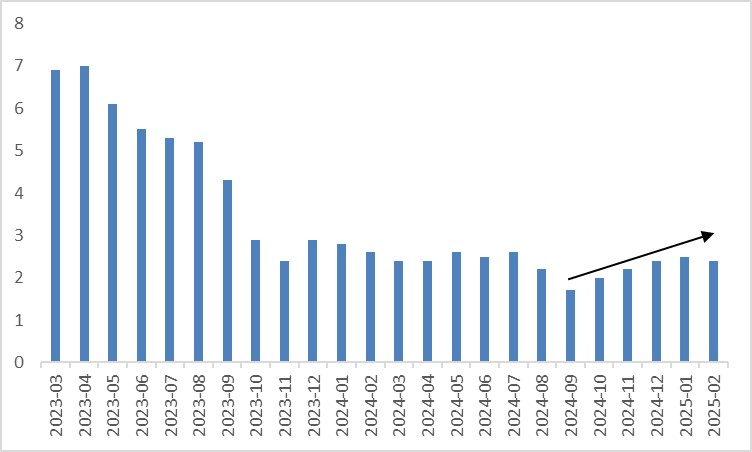

Looking back at 2024, the Eurozone economy appeared weaker than the U.S. economy, prompting the ECB to begin cutting rates earlier than the Federal Reserve (Figure 1). Since the start of this year, policymakers have raised concerns about stagflation risks in the U.S., causing the Fed to adopt a more cautious approach to its rate-cutting path. In contrast, the ECB remains more concerned about the Eurozone’s economic growth than a potential resurgence of inflation (Figure 2). As a result, while the Fed paused rate cuts in January, the ECB continued its easing, widening the policy rate differential between the U.S. and Europe.

Figure 1: Fed vs. ECB policy rate (%)

Source: Refinitiv, Tradingkey.com

Figure 2: Eurozone HICP (%)

Source: Refinitiv, Tradingkey.com

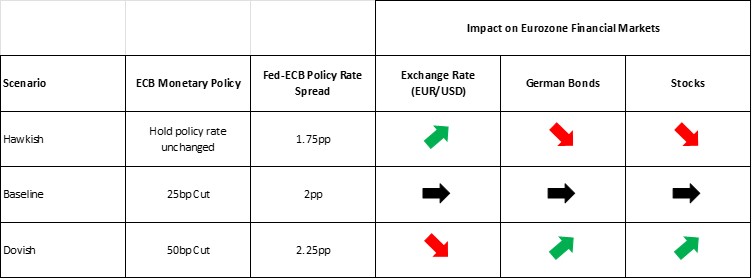

Looking ahead, although the ECB’s primary focus is on economic growth, rising inflation in the Eurozone—potentially fuelled by Trump’s high tariffs—could place the central bank in a dilemma. This necessitates a scenario-based analysis of the ECB’s monetary policy (Figure 3).

- Our baseline scenario predicts a 25-basis-point rate cut, expanding the Fed-ECB policy rate spread to 2 percentage points. Given that this has been already priced into markets, we expect minimal market movement following the rate decision.

- If the ECB adopts a cautious stance and keeps the policy rate unchanged at 2.75%, higher interest rates could boost the euro against the dollar and push up German bond yields. However, this would be negative for European equities.

- Conversely, if the ECB takes a more dovish approach—cutting rates by 50 basis points—market reactions would likely be the opposite.

Figure 3: Scenario-based analysis of the ECB’s monetary policy

Source: Tradingkey.com

Since a 25-basis-point cut is the most probable outcome, the EU emergency summit on the same day, addressing the next steps for Ukraine and European security, will take precedence. Against the backdrop of shifting U.S. policy under the Trump administration and a softening stance from the Ukrainian government, European leaders will convene to discuss how to address the Ukraine situation. Should European leaders lean toward an early resolution of the Russia-Ukraine conflict, it could help lower energy prices, reduce geopolitical risks, and restore confidence in the European economy—all of which would support the euro.

.jpg)