ASML 2025 Q1 Earnings Report Analysis: Robustness, Caution and Uncertainty

ASML's 2025 Q1 financial report has both highlights of stable performance and strong profitability, but also exposes challenges brought by cautious orders and customer purchases. Sales were basically in line with expectations, but orders and machine sales were significantly lower than market expectations, while gross profit margin, net profit, EPS and cash levels exceeded expectations. Although ASML's financial situation remains robust, driven by high-margin EUV systems and strict cost management, macroeconomic uncertainties, especially tariffs, and the cyclical slowdown in semiconductor demand have caused some concerns about near-term growth.

Source: ASML, TradingKey

Interpretation of Financial Indicators

Sales stability: order backlog and the driving force of EUV

Large order backlog: The core driver of ASML's sales is the delivery of signed orders, not new orders in the quarter. Revenue is recognized when the equipment is delivered. In Q1 2025, ASML delivered a large number of high-end EUV equipment, especially orders signed in Q4 2024, such as Intel, TSMC and other customers. These orders were delivered in this quarter, driving sales to 7.74 billion euros, which is basically in line with market expectations.

The company currently has about 7 billion euros in orders on hand, providing a solid guarantee for revenue in the next few quarters. The orders accumulated during the peak period of semiconductor capital expenditure in the past few years are gradually being fulfilled, forming a buffer for sales revenue. Even if new orders are temporarily reduced, delivery orders can still maintain stable revenue.

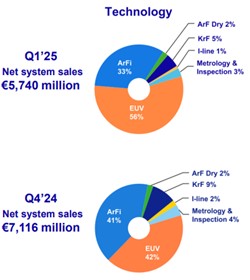

Contribution of high-value EUV equipment: The price of a single EUV equipment is about 30 million euros. The 11 EUV equipment delivered in Q4 2024 contributed nearly 3 billion euros in revenue, greatly supporting sales in that quarter. The delivery of high-end EUV equipment not only increased sales but also led to an increase in overall gross profit margin.

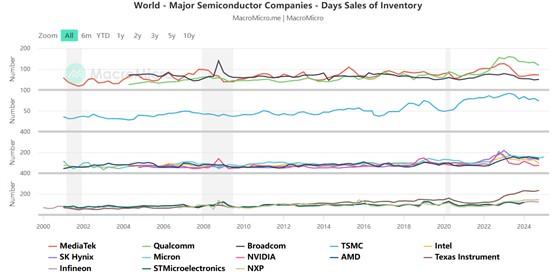

Weak Orders and Shipments: Cyclical and geopolitical challenges

Macroeconomic and geopolitical pressures: Since 2024, the global economic growth has slowed down, China-US trade tensions have intensified, and export restrictions and tariff policies have continued to escalate, leading to cautious capital expenditures by customers. ASML's net bookings in Q1 2025 were only 3.94 billion euros, far below the market expectation of about 4.8 billion euros, a month-on-month decrease of nearly 45%, reflecting a clear wait-and-see attitude of customers.

Semiconductor industry inventory adjustment: Since 2022, the semiconductor industry has experienced a peak in inventory accumulation and entered the destocking stage in 2023-2024. Customers prioritize digesting existing inventory and reducing new equipment purchases, resulting in a significant decline in orders and machine sales. This is a normal manifestation of cyclical adjustments in industry, not a fundamental decline in demand.

Source: MacroMicro, TradingKey

Long order cycle and fluctuating purchasing rhythm: The EUV equipment purchasing cycle is as long as 12-20 months, and there is a significant lag between orders and deliveries. The order peak in Q4 2024 is converted into delivery in Q1 2025, but the pace of new orders has slowed down significantly, reflecting that customers have adjusted their purchasing plans in an uncertain environment.

Differentiation of customer structure and demand: The demand for AI and high-end logic chips has driven some customers to accelerate procurement, while the demand for traditional consumer electronics and memory chips has been weak, resulting in uneven overall order growth. Some customers have adopted a cautious strategy and delayed large-scale investment due to technology upgrades and capital budget constraints.

Profitability and Cash Flow: Highlights

High gross margin drivers:

- High profit margin of EUV equipment: EUV and High-NA EUV equipment have profit margins far exceeding traditional equipment, driving the gross profit margin to 54%, higher than the market expectation of 52%-53%.

- Product portfolio optimization: The company gradually reduces low-profit immersion lithography equipment, increases the proportion of EUV and ArFi equipment shipments, and improves overall profitability.

- Cost and supply chain management: Reduce manufacturing costs and further increase gross profit margins through production efficiency improvement and supply chain optimization.

Source: ASML

High gross margins lead to expanded profit margins, with net profit reaching 2.36 billion euros in Q1 2025 and EPS of 6 euros, both exceeding market expectations. R&D and sales expenses are effectively controlled to avoid profit erosion. Cash reserves fell from 12.7 billion euros in the fourth quarter of 2024 to 9.1 billion euros, but remained robust. The decline mainly reflects 2.7 billion euros in share repurchases and dividend payments, a proposed dividend of 6.40 euros per share in 2024, an increase of 4.9% from 2023.

Tariff Impact

Increased U.S.-China trade tensions and new tariff announcements have created significant uncertainty in the market.

- Direct costs: Tariffs on systems shipped to the U.S. could push up prices, dampening demand from customers such as Intel. Tariffs on parts and tools required for on-site operations in the U.S. could increase maintenance costs, which could be passed on to customers. ASML’s U.S. manufacturing facilities could face import tariffs, further complicating the cost structure.

- Supply chain disruptions: ASML relies on a global supply chain involving key suppliers in the U.S., Europe, and Asia. Tariffs could result in production delays or higher costs, which, if not effectively mitigated, would impact ASML’s gross margins.

- Indirect demand impact: CEO Fouquet noted that tariffs could dampen semiconductor demand in industries such as consumer electronics and automotive by reducing global GDP growth. Retaliatory tariffs from other countries could limit ASML’s growth in non-U.S. markets, particularly in China, where export restrictions have already dampened growth.

Future Outlook

ASML is expected to remain financially stable in 2025, with expected net sales of 30 billion to 35 billion euros and a gross margin of 51-53%. The company's long-term growth prospects remain strong, driven by AI, 5G and advanced logic/memory nodes. Sales are expected to grow to 36 billion to 40 billion euros in 2026, assuming inventory normalization and continued strong demand for AI. Tariffs remain a key variable, but ASML's proactive supply chain management and strong customer relationships should mitigate major disruptions. The company's strong cash reserves and continued R&D investment put it in a good position for the next industry upcycle. Although short-term fluctuations may exist this year, ASML's technological leadership and exposure to long-term growth trends such as AI make it likely to rebound strongly in 2026.