Netflix Q1 2025 Preview: Subscriber Momentum Meets Margin Scrutiny

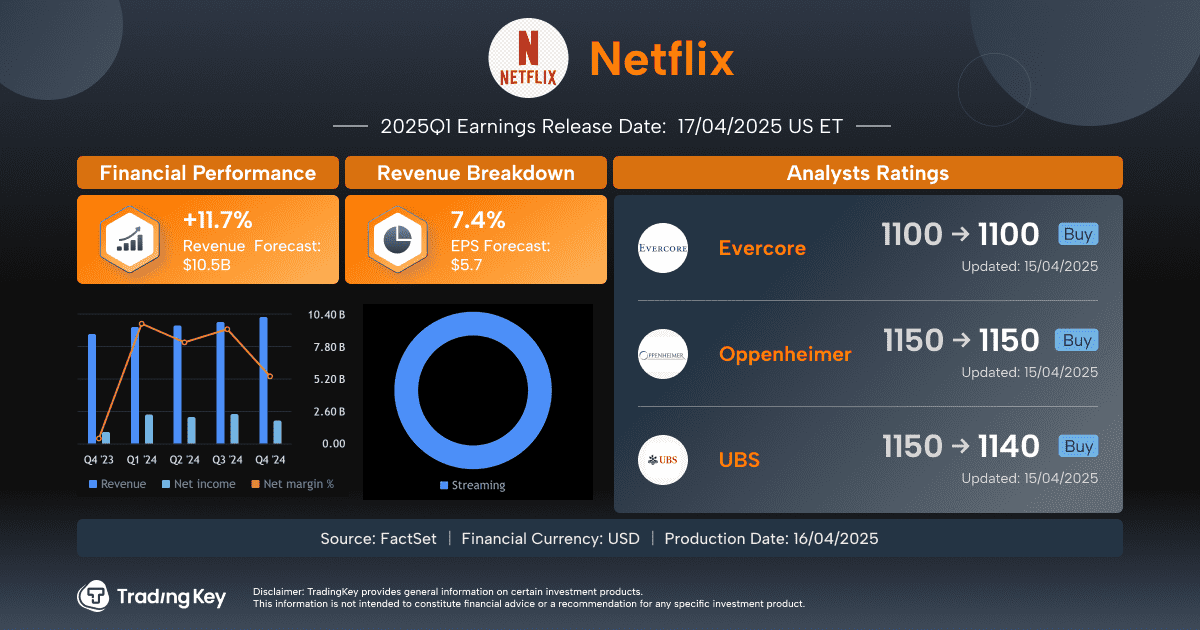

TradingKey - Netflix enters its Q1 2025 earnings report on a wave of guarded optimism. Analysts expect Netflix to post year-over-year growth in Q1, with consensus revenue at 10.5billion (+11.7% YoY) and EPS at 5.67(+7.4%YoY).

Ad-Supported Tier: Growing Pains or Monetization Engine?

One of the more discussed elements of this quarter's report will be the progress of Netflix in building up its ad-supporting tier. Management had earlier revealed that the tier had crossed the 40 million mark globally in monthly active users, though monetization per user remains behind traditional pure-play AVOD destinations like YouTube or Hulu.

This quarter should present more specific data on revenue per user (ARPU) growth, not least in North America where the advertiser base is the largest. Clarifying how the company's shifting content development helps fuel the tier, and in turn, sustained ad interest in its more low-budget series and international hits, will also interest analysts. Expect words on Netflix's new exploration of programmatic ad selling and third-party measurement, both of which should boost advertiser confidence and revenue in the period to come.

Costs, Margins, and Free Cash Flow

With revenue increasing, Netflix is likely to report operating margins of ~24.3%, compared to last year's 21%, as it continues to benefit from scale and improve content investment efficiency. Watch out, however, for any deviation in this trend, as this will come under intense scrutiny. Netflix had earlier given guidance of more than $6 billion in full-year 2025 free cash flow, and this quarter should serve to validate that target in principle, at least in the early stages.

If management indicates content amortization or production slippage is accelerating costs, near-term margin compression might follow. That being said, sentiment remains strong given the platform's pricing power, particularly in established markets like the U.S. and Canada. Net income is likely to come in at approximately $2 billion, paving the way for potentially even more capital return potential in the latter part of the year, potentially in the form of buybacks.

What Investors Should Watch

The stock's performance at Netflix will ride on a couple of elements above and beyond raw numbers: guidance, subscriber composition, and growth by region. In particular, forward-looking comments on the Q2 pipeline and revisions to the full-year forecast could propel price action. Also, look for attention on the company's gaming efforts, which have expanded with beta releases and recent acquisitions.

While still not material to revenue, these initiatives are part of the bigger picture of expanding the company's moats. Lastly, competition is a low-boil issue. Disney+, Max, and Amazon Prime keep pumping money into prestige content, but Netflix's widening edge in scale, data-driven production, and distribution holds firm. For the time being, the story's no longer about keeping up in the streaming wars, but rather how Netflix accelerates its lead.