[IN-DEPTH ANALYSIS] From Investment Banking to Wealth Management: How Morgan Stanley is Shaping the Future of Finance

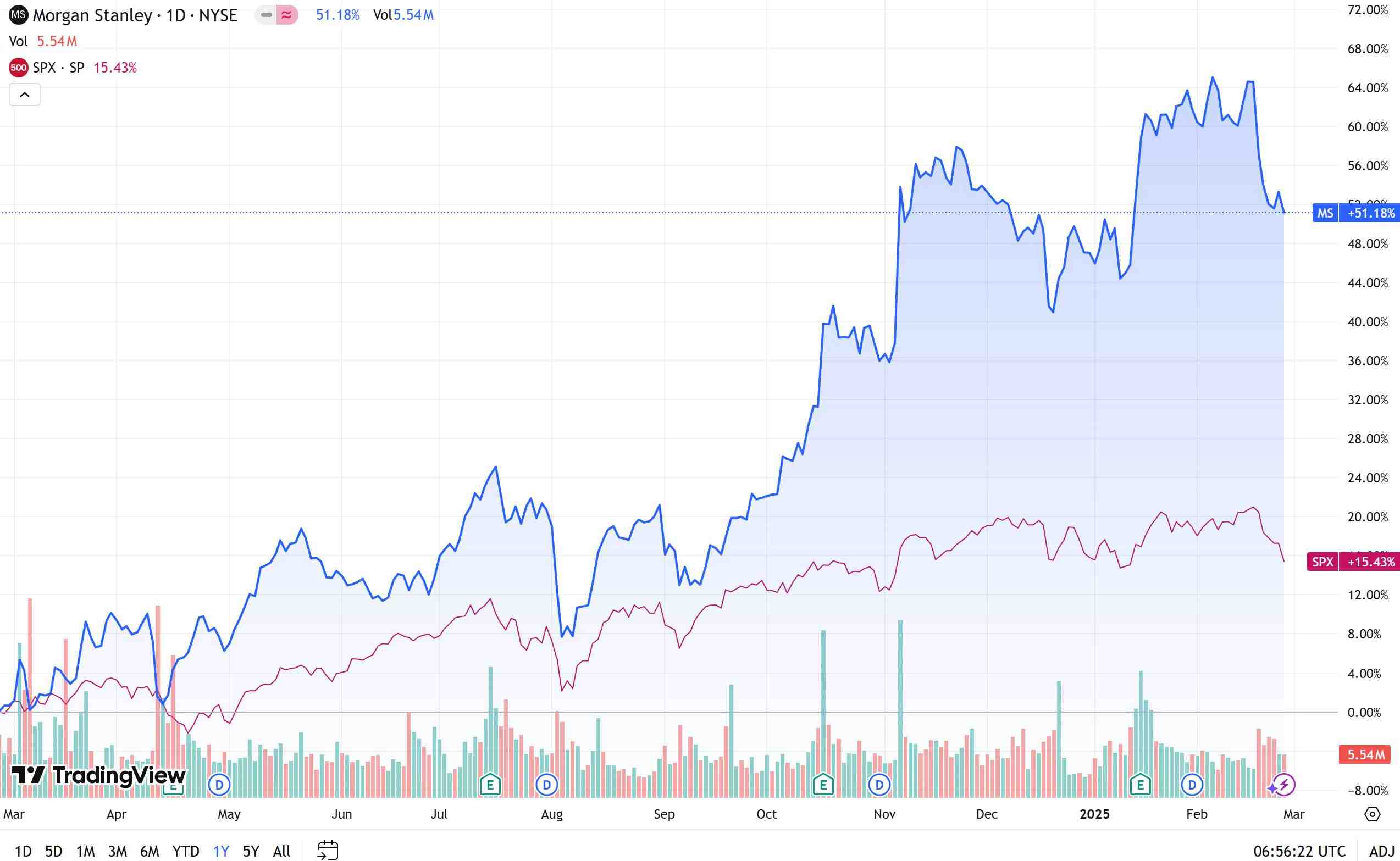

Source: TradingView

Key Takeaways

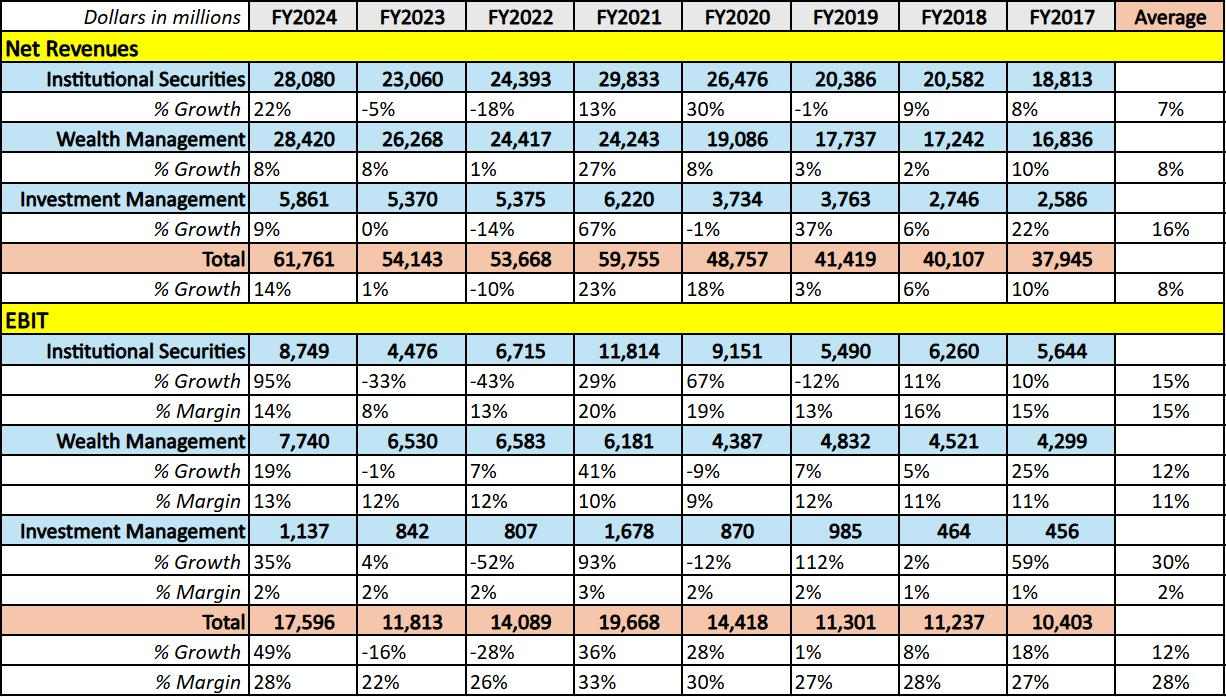

Strong Financial Performance: In 2024, Morgan Stanley posted impressive growth, with net revenue of $61.76 billion and a remarkable 53% growth in EPS. Their EBIT surged by 49%, demonstrating robust profit generation.

Market Position: Morgan Stanley’s Wealth Management division has become its largest revenue source, reaching $1.67 trillion in AUM, a nearly 15% increase. The company dominates high-net-worth and institutional wealth management, with AI technology playing a key role in enhancing service offerings.

Diversified Business Model: Although Institutional Securities remains volatile, its impressive performance in equity and fixed income sales & trading makes it a strong contributor to the company's success. Investment Banking, while smaller, still plays a crucial role in large transactions.

Strategic Transformation: With a shift towards wealth management, Morgan Stanley has proven its ability to remain competitive even as market share in traditional sectors like M&A and investment banking shrinks.

2025 Outlook: While it expects a reasonable target price of $151.85, the company’s high valuation may be influenced by market expectations, with potential risks from geopolitical factors, market volatility, and regulatory changes. This could impact the overall price trajectory.

Company Overview

Morgan Stanley is a leading global financial services company with a strong reputation for delivering innovative solutions across Wealth Management, Institutional Securities, and Investment Management. With offices in 41 countries, more than 90,000 employees, and decades of experience, the company provides a range of services designed to meet the needs of individual investors, businesses, and institutions worldwide. Morgan Stanley excels in managing client assets, with over $1.6 trillion in wealth management assets under management. Morgan Stanley’s strategic investments in technology, including AI, ensure it stays at the forefront of financial services, providing tailored, data-driven insights. A proven leader in the financial market, Morgan Stanley continues to redefine the future of finance with a commitment to excellence and sustainable growth.

Analysis of Morgan Stanley's Main Businesses

In 2024, Morgan Stanley delivered a strong financial performance, with net revenue reaching $61.76 billion, marking a 14% year-on-year increase. The company’s earnings per share (EPS) for the year stood at $8.04, reflecting a remarkable 53% growth, while EBIT rose by 49% to $17.6 billion, resulting in an EBIT margin of 28%. This strong performance highlights the company’s solid profit growth. At the close of 2024, total assets reached $1.215 trillion, up 2%, and total deposits grew by 7% to $376 billion. Notably, the company achieved significant profit growth while keeping non-interest expenses relatively stable, with only a 5% increase compared to the previous year. This underscores Morgan Stanley’s success in managing operational efficiency and driving asset accumulation.

Morgan Stanley's key businesses are divided into three major segments: Institutional Securities, Wealth Management, and Investment Management.

1. Institutional Securities

The Institutional Securities division is one of Morgan Stanley’s core businesses, primarily providing investment banking services and sales & trading services of equity and fixed income. The division’s clientele mainly consists of large corporations, government entities, hedge funds, and other financial institutions.

In 2024, the Institutional Securities division delivered an impressive performance, becoming a key driver of Morgan Stanley’s profit growth. The division’s revenue grew by 22% year-on-year, reaching $28.08 billion, while pre-tax profits surged by 95%, reaching $8.75 billion. Several factors contributed to the growth in 2024: the post-pandemic economic recovery reignited capital market activity, especially in equity and fixed-income trading. Strong demand for underwriting services significantly supported the division's performance. Additionally, the recovery in advisory services reflected growing market confidence in corporate activity and capital raising.

However, based on the revenue trends of the Institutional Securities division in recent years, it is clear that revenue performance is highly influenced by market cycles, resulting in significant volatility in growth. For example, revenue grew sharply by 30% in 2020 but declined by 18% and 5% in 2022 and 2023, respectively, while in 2024, it increased by 22% again. This indicates that market fluctuations and economic cycles have a significant impact on the division's revenue.

2. Wealth Management

Morgan Stanley’s Wealth Management division focuses on providing a comprehensive range of wealth management services to high-net-worth individuals and families, including investment advice, financial planning, tax optimization, and retirement planning. Through its extensive expertise and tailored services, Morgan Stanley helps clients grow and protect their wealth. The division’s clients mainly include affluent individuals, family offices, and charitable organizations.

Wealth Management has been a key growth driver for Morgan Stanley, especially in 2024. Following the acquisitions of E*TRADE and Eaton Vance, net revenue grew by 8%, reaching $28.42 billion, driven by strong demand from high-net-worth clients and institutional investors due to the global market recovery. EBIT rose by 19%, reaching $7.74 billion, with a new high 13% EBIT margin for the past few years, reflecting the growing profitability. Non-interest expenses grew by only 5% compared to previous double-digit growth, highlighting operating leverage.

Unlike Institutional Securities, Wealth Management has experienced steady revenue growth in recent years with relatively smaller fluctuations, demonstrating its unique stability. In fact, its revenue has surpassed that of Institutional Securities over the past two years. While Wealth Management has yet to exceed Institutional Securities in terms of margin, it is now very close, highlighting the strategic shift by management towards a Wealth Management-oriented business, moving away from an Investment Banking-driven model.

3. Investment Management

The Investment Management division primarily provides asset management services for institutional investors and high-net-worth clients and it has a high-level synergy with Wealth Management division. The synergy lies in the seamless integration of personalized wealth planning and efficient fund allocation. Wealth Management designs tailored financial plans, directing funds into investment strategies aligned with clients' long-term goals. Investment Management, in turn, ensures these funds are deployed into optimal investment products, including equities, bonds, private equity, and ESG assets. This collaboration maximizes the efficiency of fund flows, aligning wealth management with investment strategies to achieve both short-term returns and long-term capital growth, while enabling swift portfolio adjustments in response to market changes.

Although the division accounts for a relatively small share of Morgan Stanley’s overall revenue—less than 10%—it remains a crucial part of the company. In 2024, the Investment Management division performed significantly better than in previous years, with net revenue growing by 9% to $5.86 billion, showing strong momentum. Pre-tax profits surged, with EBIT increasing by 35% to $1.14 billion, though the EBIT margin was only 2%, lower than other divisions but still within historical averages.

Source: TradingKey, Morgan Stanley

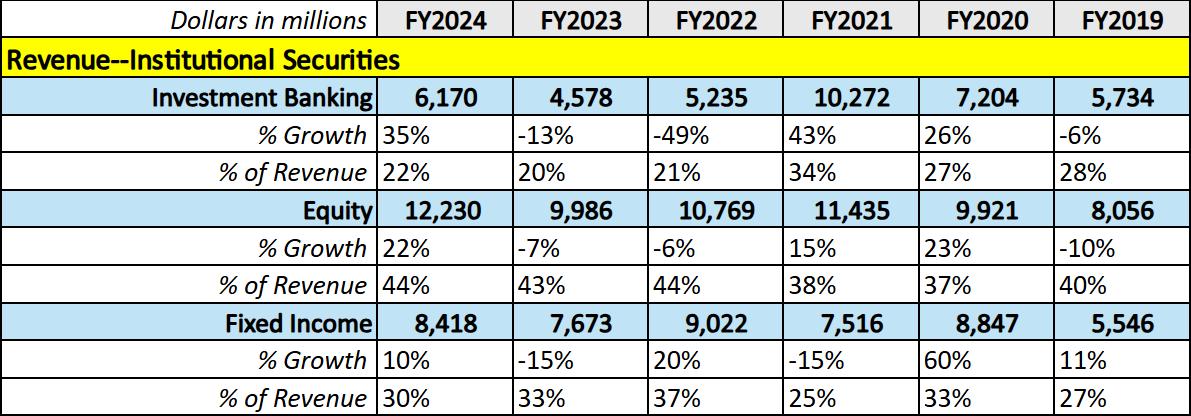

The Volatile Catalyst for Morgan Stanley—Institutional Securities

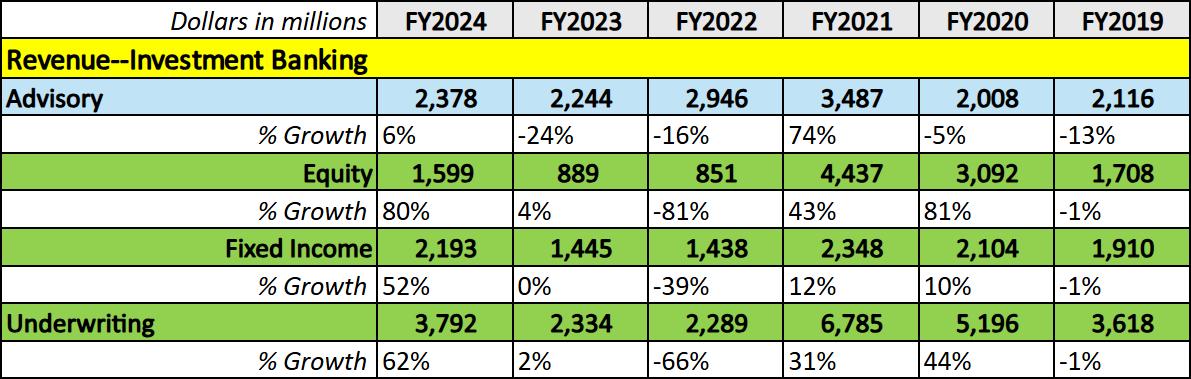

We have previously mentioned that the revenue of the Institutional Securities division experienced significant volatility. As shown in the chart below, we can clearly observe large fluctuations in revenue growth across its sub-divisions, including Investment Banking, Equity, and Fixed Income over the past few years. Additionally, we can see that the share of revenue from Investment Banking has been shrinking, while the revenue share from Sales & Trading of Equity and Sales & Trading of Fixed Income has been steadily increasing, maintaining stability in the past two years.

Source: TradingKey, Morgan Stanley

Investment Banking

Although the revenue from Investment Banking has been steadily decreasing as a proportion of Morgan Stanley's total revenue, the company’s significant role in the global Investment Banking sector remains undeniable.

In 2024, Advisory generated $2.38 billion in revenue, accounting for 39% of total investment banking revenue, with a modest 6% growth. On the other hand, Underwriting (including both equity and fixed income) accounted for $3.79 billion, representing 61% of investment banking revenue, and experienced a strong 62% growth in 2024, recovering from previous years of volatility.

Source: TradingKey, Morgan Stanley

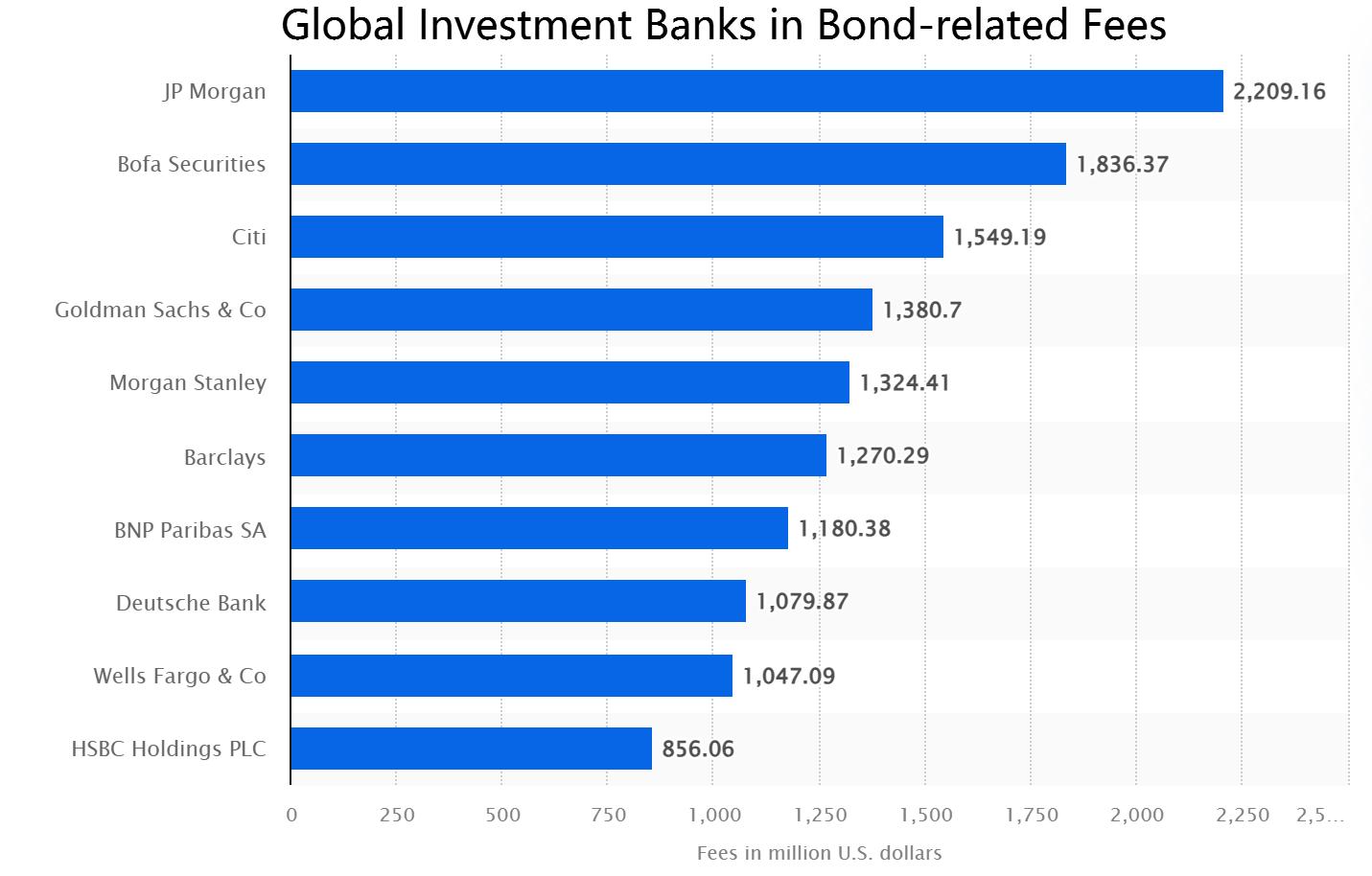

- Advisory Service

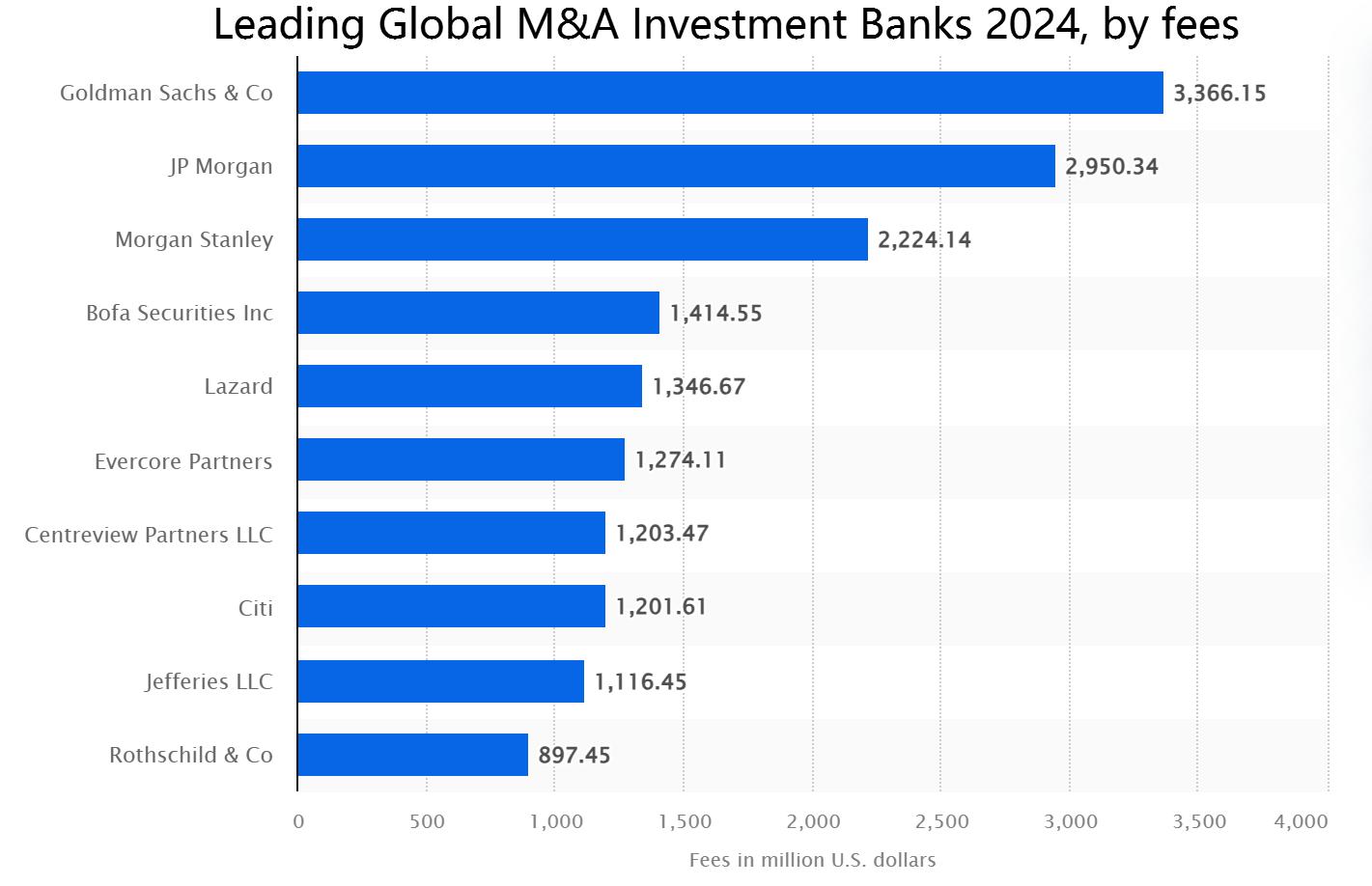

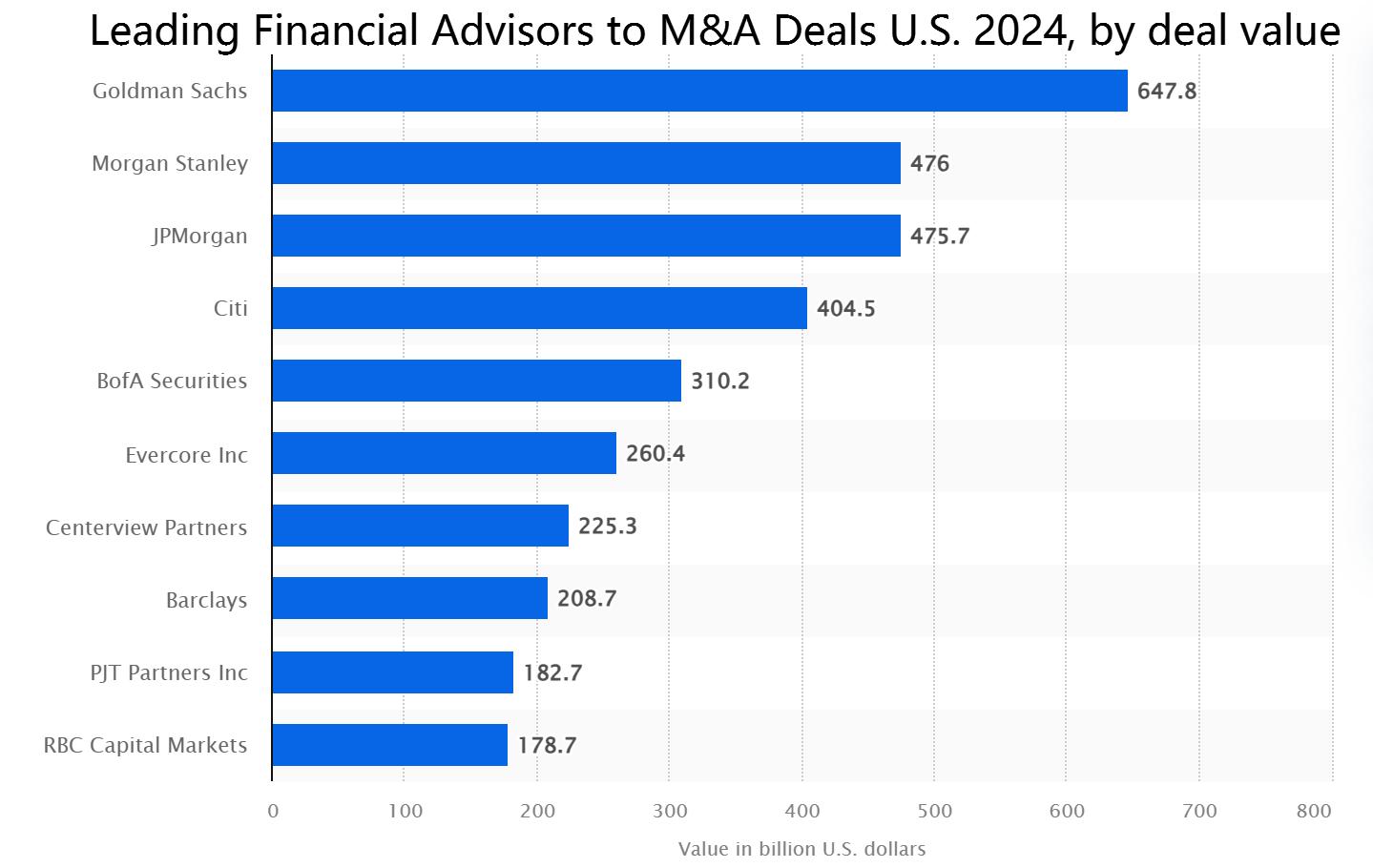

Morgan Stanley holds a strong position in the M&A (Mergers and Acquisitions) advisory business, ranking third in global M&A investment banks by fees in 2024 with $2.22 billion. In terms of deal value, Morgan Stanley is also a leading financial advisor in the U.S. for M&A deals in 2024, securing a spot in the top two with $476 billion in deal value. This indicates Morgan Stanley's significant influence and reputation in facilitating large, high-value transactions across various industries.

According to current SEP expectations, the Federal Reserve is likely to implement two rate cuts in 2025. If this expectation holds, borrowing costs will decrease, which will encourage mergers and acquisitions activity. Lower interest rates will reduce financing costs, especially for leveraged buyouts (LBOs), as businesses can acquire targets at a lower cost.

Additionally, if Trump successfully implements tax cuts and deregulation policies, it could stimulate M&A activity. Lowering corporate tax rates would increase company profits and cash reserves, providing more funds for acquisitions. Additionally, deregulation could remove barriers to mergers and acquisitions, making cross-industry deals easier for companies. However, if Trump's trade policies intensify, particularly the trade tensions with China, global M&A could be affected, as companies may delay or reassess cross-border transactions due to the uncertainty surrounding trade policies.

|

|

Source: Statista

- Underwriting Service

Morgan Stanley’s underwriting services are a critical component of its investment banking division, offering comprehensive solutions for both equity and debt capital markets. As an underwriter, Morgan Stanley assists companies in raising capital by issuing stocks, bonds, or other financial instruments to the public or institutional investors.

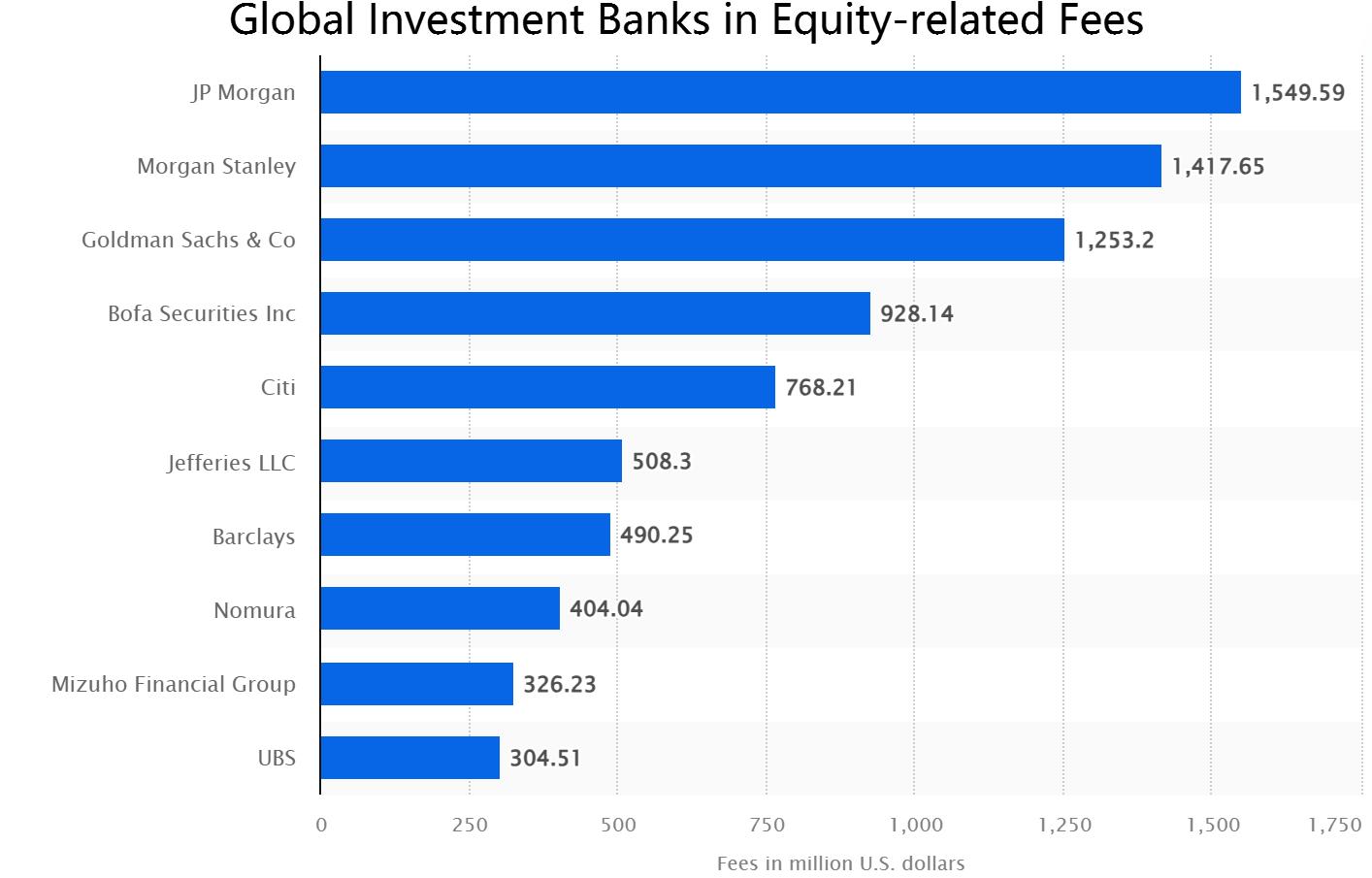

Morgan Stanley continues to solidify its leading position in the global fixed income and equity underwriting markets in 2024, ranking among the top players in the industry. Looking ahead to 2025, interest rate cuts could stimulate underwriting activity, as lower financing costs will encourage capital raising. Additionally, Trump's tax cuts and deregulation policies are expected to boost corporate profitability and capital demand, further driving the underwriting market.

|

|

Source: Statista

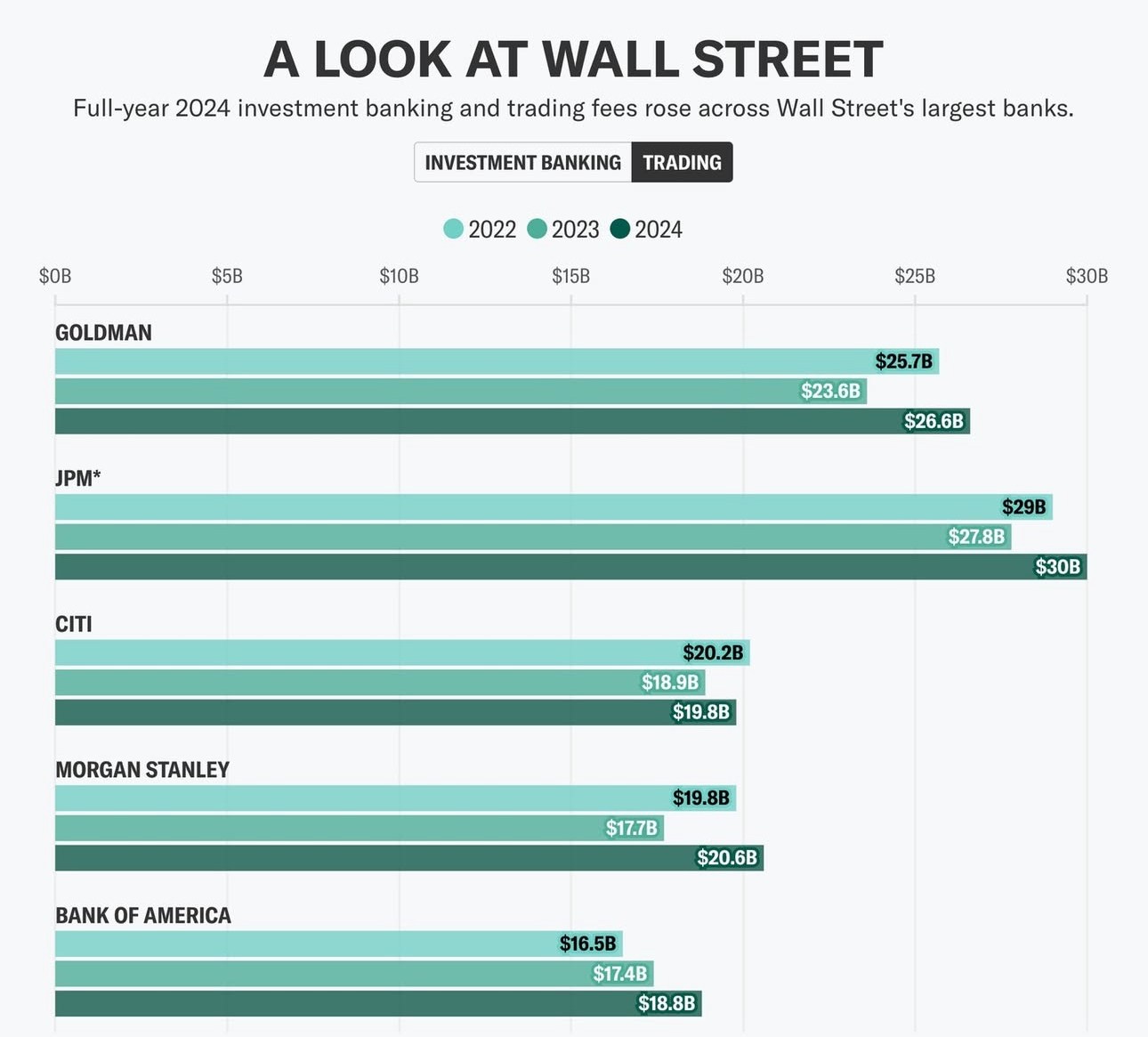

Sales & Trading in Equity and Fixed Income

In 2024, Morgan Stanley's Sales & Trading revenue reached $20.6 billion, showing an increase from $19.8 billion in 2023, further solidifying its leadership position on Wall Street.

In Equity Sales & Trading, Morgan Stanley offers services including equity trading, equity derivatives trading, market-making, etc. The company provides clients with stock investment strategy advice, portfolio management, and liquidity support during market volatility. In Fixed Income Sales & Trading, Morgan Stanley focuses on trading various debt instruments, including government bonds, corporate bonds, mortgage-backed securities (MBS), asset-backed securities (ABS), and other debt products. To hedge interest rates and credit risks and enhance returns, derivatives such as interest rate swaps, credit default swaps (CDS), and bond futures are widely utilized.

In the first few months of 2025, we have already witnessed significant volatility in the capital markets, and this volatility is expected to continue increasing due to fiscal and monetary policies, particularly the uncertainties surrounding Trump’s policies. This volatility presents greater opportunities for Sales & Trading, as it is the source of Morgan Stanley's revenue in both equity and fixed income sectors. The ability to go long or short in such an environment provides Morgan Stanley with ample chances to capitalize on market movements.

Source: Yahoo Finance

The Stable Catalyst for Morgan Stanley—Wealth Management

Wealth Management provides stable fee and commission income, unlike Institutional Securities, which are more reliant on transaction activity. This stability serves as Morgan Stanley's higher margin of safety.

As of December 31, 2024, the Wealth Management Division became Morgan Stanley's largest revenue source, with $1.67 trillion in Assets Under Management (AUM), up nearly 15% from $1.46 trillion in 2023. The division added $123 billion in fee-based flows and $252 billion in net new assets, showcasing its ability to attract and retain clients.

Morgan Stanley’s strategic transformation has strengthened its competitive edge in Wealth Management. According to Barron's 2024 list of top 250 private wealth management firms, Morgan Stanley teams occupy 6 of the top 10 spots, with the No.1 team managing over $49 billion in AUM. This highlights that even if Morgan Stanley loses market share in areas like M&A and investment banking, its wealth management business remains a key source of its brand strength.

By 2025, Morgan Stanley Wealth Management is poised for growth, driven by a rising global HNW population, particularly in Asia-Pacific and emerging markets, increased asset prices, and favorable interest rates. However, challenges such as market uncertainties, geopolitical risks, and interest rate fluctuations could impact performance and operational costs.

Financial & Valuation

Morgan Stanley has demonstrated steady performance over the past three years, with a market cap of $211.36 billion and a 3-year revenue CAGR of 0.96%. While its EPS 3-year CAGR has been negative at -0.33%, the company has maintained a relatively high net income margin of 21.77%, indicating strong operational efficiency.

From a valuation perspective, Morgan Stanley’s forward P/E of 16.15 and P/B of 2.42 suggest it is moderately overpriced compared to peers, with a robust return on equity of 13.22% and a solid return on assets of 3.24%. The high dividend payout ratio of 45.54% highlights its commitment to returning value to shareholders, although the dividend growth has been more moderate at 21.84% compared to some competitors.

Source: TradingKey, SEC Fillings, Seeking Alpha

Source: TradingKey, SEC Fillings, Seeking Alpha

Conclusion

With Morgan Stanley’s industry position, solid financial base, and business transformation, it provides a strong investment opportunity for long-term investors. Given the current market, which places the company at a forward P/E of 16.15 and the average expected EPS of $9.41 over the next three years, a reasonable target price would be $151.85. However, it is important to note that I believe Morgan Stanley's high valuation currently reflects the market's pricing of most potential catalysts in the future. Therefore, if any negative factors impact Morgan Stanley, the current optimistic valuation may see some correction.