PLTR: Buying Now is Like Trying to Catch a Falling Knife

Key Points

- The data industry consists of many companies and various sub-segments, Palantir occupies the application layer in the whole value chain

- Despite their strong business execution and product strengths, investing in Palantir right now comes with big risks

- Palantir valuation is too far ahead of the company’s performance

- Certain aspects of Palantir financials need special attention – interest income and asset composition

- Competition may come from both established tech players as well as niche-market startups

Palantir, the Company

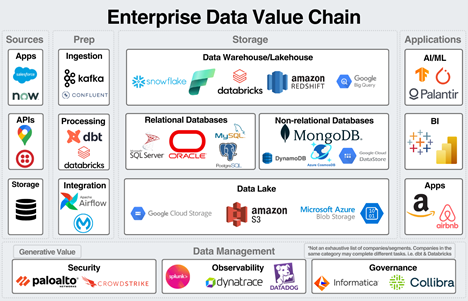

Brief Overview of the Data Value Chain

The data Industry is among the most complex and dynamic industries, with thousands of players, ranging from niche start-ups to trillion-dollar tech giants, each trying to fit into different sections across the data value chain.

Source: Generative Value

The main segments of the data industry include:

Sources: Sources of data can be many types – enterprise apps, Excel sheets, databases, web pages and APIs

Preparation: Where data from the sources is imported into a data platform. There, the data is integrated into an appropriate storage format

Storage: Many companies focus on this area. Data can be stored in data lakes (for raw, unorganized data), databases (where data is organized) and data warehouses (storage of cleaned and processed data). There are also data lakehouses, a mixture of data lakes and data warehouses.

Applications: The section where data is used to derive all kinds of business-related decisions.

Data management: Any kind of activities related to maintaining data – such as data monitoring, cybersecurity and governance.

The biggest tech companies like Amazon, Microsoft, Alphabet and Oracle have a presence in each of these areas. On the other hand, there are also smaller players focusing on specific niches across the map – Snowflake and Databricks (Data Warehouse/Lakehouse), Palo Alto and CrowdStrike (Cybersecurity), Tableau (Business Intelligence Apps) and Data Dog (Data Management).

Where does Palantir stand?

Palantir is different from the above-mentioned companies, as it is entirely focused on the application side with a strong focus on AI and Machine Learning. The strengths of the company can be summarized in the following:

First, Palantir can integrate and analyze data from all kinds of data sources, providing certain flexibility for the clients.

Second, Palantir tools are very powerful, providing solutions to problems other companies do not have the capability to address (so far).

Third, as a company that derives more than half of its revenue from government agencies, Palantir places a great emphasis on data security. This makes it a reliable partner for commercial clients, as they do not need to worry about data breach risks.

Palantir products can identify patterns in data that no other software can detect. They can also identify potential business problems before they occur and provide corresponding solutions.

In simple terms, Palantir is a hybrid of an enterprise software firm (like SAP) and a business consulting firm (like McKinsey), but with much superior capabilities.

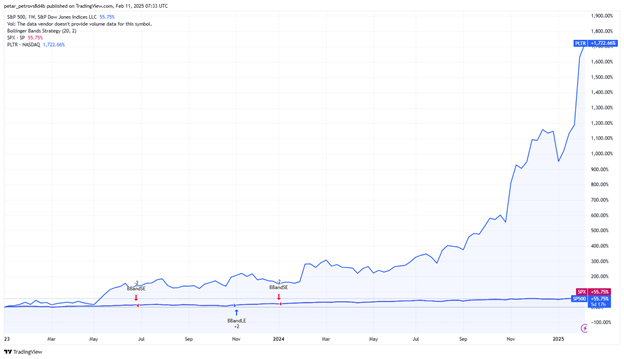

Palantir, the Stock

Source: TradingView

Palantir stock rally is something that we do not see often. Starting from early 2023 (the time when AI started to gain market traction) up until now, PLTR investment return has been above 1,700%. In simple terms, if someone invested $50,000 in the stock two years ago, they would be a millionaire right now.

However, history tells us that such stock rallies are rarely sustainable. Assets experiencing this enormous level of appreciation always face correction at some point, implying that investing in Palantir right now is quite risky. The factors explained below underline why risks for PLTR are quite significant.

Exorbitant Valuation

The stock is traded at 600x TTM Price-to-Earnings ratio – a multiple way above anything we can see on the market. To put more context into how high this valuation is, we can give Cisco as an example. Cisco, the symbol of the dot-com bubble in the early 2000s was traded at around 200x the earnings just before the bubble burst.

Palantir is among the twenty largest tech firms globally with roughly $270 billion of market capitalization, along with companies that are much more established with a much larger scale of operation and much more solid track record of profitability.

It is true that business-wise, Palantir is performing remarkably well with a CAGR of revenue in the past years of approximately 30% and the management is guiding growth in 2025 to be similar.

Source: TradingKey, SEC Fillings

However, a 30% growth rate is still not enough to justify this valuation, especially when the management is guiding for just an incremental expansion of the adjusted operating margin – 42% in 2025E vs 39% in 2024A, implying earnings will grow only slightly faster than revenue will.

With this stretched multiple, it appears that investors are already envisioning Palantir to be a household name in the tech world with the same scale as Microsoft, Salesforce, Oracle and SAP. The possibility of this happening is real but the path to reaching this status will definitely not be short and not always be smooth and straightforward. Every big tech stock has experienced price corrections and business downturns at least once in their lifetimes, making the correction of PLTR stock inevitable.

Warning Signs in the Financial Statements

On top of the high valuation problem, some aspects of the company’s financials can also cause concern.

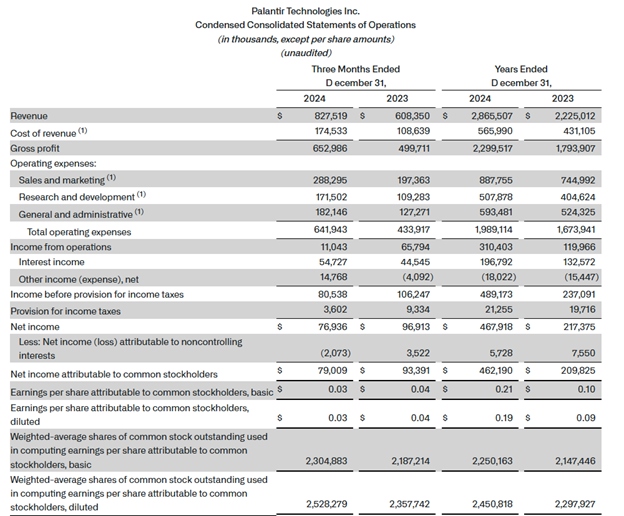

Palantir has been profitable in the last two years, demonstrating that the company can financially sustain itself in the future. However, a very significant amount of the net profit actually comes not from their main business operations, but from interest income earned on the 5 billion dollars of cash and short-term investments they hold.

There is nothing wrong with a company using its cash reserves and earning interest from it, but it is somewhat ironic that a high-growth, high-prospect software firm relies on interest income instead of reinvesting the cash for further business expansion.

Source: SEC Filings

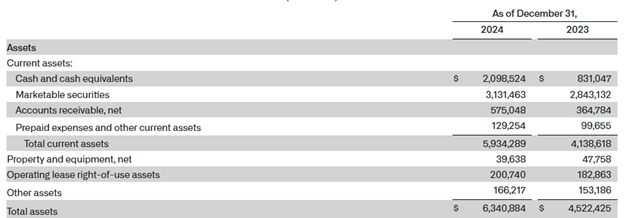

Additionally, if we look into Palantir's balance sheet, we can see that the assets consist primarily of cash and investments. The company does not have any intangible assets (such as copyrights or patents), implying its economic moat may not be as strong.

Source: SEC Filings

Competition

Competition still poses significant uncertainty for Palantir. As mentioned before, the data landscape is highly fragmented, with numerous big and small players. In the tech industry, building a long-term competitive advantage is more difficult compared to other sectors like banking or consumer goods because technology develops exponentially fast and firms are forced to constantly innovate to stay relevant.

Competition can arise from various directions, including big AI scalers and fast-growing startups.

Tech giants such as Meta, Alphabet, Microsoft and Amazon pose a real threat. These companies already operate within the data industry and they also have access to first-hand data from their main businesses—social media, cloud and e-commerce. If these giants introduce products that directly compete with Palantir, it would be a substantial challenge for the latter. This is especially true when comparing the financial resources of Palantir to those of the big tech companies. In 2024, Palantir spent just over half a billion dollars on R&D and capex, a negligible amount compared to the hundreds of billions spent annually by the MAG7 on developing new technologies and products.

Additionally, threats can emerge from small players currently unknown to the public. These competitors don't necessarily have to be from the United States; they could come from countries like China. For instance, no one anticipated DeepSeek's recent market disruption.