Tesla's Valuation Dilemma: Why It's Time to Reconsider TSLA

Key takeaways:

- Tesla's stock valuation soars on the wings of future growth narratives, particularly in autonomous driving, despite current earnings not fully justifying this premium.

- The company's profitability, as indicated by gross profit margins, is on a decreasing trend, largely due to increased competition and a shift to more mass-market vehicles.

- Tesla's ambitious robotaxi service faces significant technological and regulatory challenges that could impede the realization of this key future growth driver.

- Given the high P/E ratio and the speculative nature of Tesla's growth targets, we deem the stock overvalued. Therefore, we recommend a strong sell for the near term, with a calculated target price range of $368 to $391.

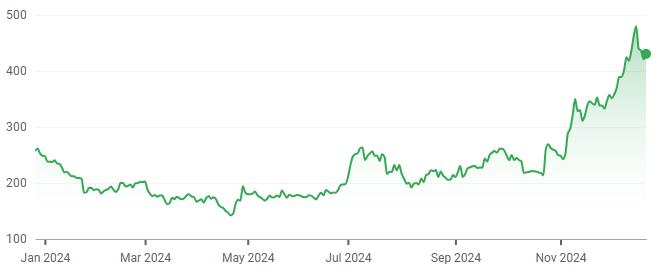

Share Price Overview

Source: Google Finance

Overvaluation of Tesla

Tesla's valuation is driven largely by future growth narratives, particularly its advancements in autonomous vehicles and robotaxi services. While these innovations are exciting, they remain speculative and far from realizing their potential. As of now, Tesla’s stock trades at a P/E ratio of 25.5, a significant premium compared to traditional automakers such as Ford (P/E 11.1), GM (P/E 5.4), and Toyota (P/E 8.3). Even if Tesla achieves its most optimistic growth targets—producing 20 million vehicles annually by 2030—its valuation remains inflated, primarily driven by investor speculation rather than concrete financial metrics.

Margin Erosion and Intensifying Competition

Tesla's automotive business, which forms the core of its operations, has seen declining margins in recent years. The gross profit margin dropped from 26.54% in 2021 to 17.05% in 2023 and further declined to 15.27% in 2024. This ongoing erosion of profitability can be attributed to several factors:

· Rising Competition: Tesla is increasingly facing competition not only from traditional automakers like Ford, GM, and Toyota, but also from Chinese EV manufacturers such as BYD. In the U.S., Tesla’s market share fell from 60.3% in 2022 to 48.2% in Q3 2024, and the competition in China—Tesla’s largest international market—has intensified, leading to pressure on both volume and pricing.

· Product Mix Shifts: Tesla is pivoting from a luxury EV provider to a mass-market producer, with models like the Model 3 and Model Y. While this strategy boosts sales volume, it compresses margins due to the need for competitive pricing.

The Robotaxi Dream: Technological and Regulatory Hurdles

Tesla's vision for autonomous vehicles, particularly its ambitious robotaxi service, is a cornerstone of the company’s future growth narrative. However, this vision is riddled with challenges:

· Technological Limitations: Tesla’s Full Self-Driving (FSD) software, while promising, is far from achieving full autonomy. The company has repeatedly missed deadlines for its self-driving technology, and its vision-only approach remains controversial among experts. Real-world performance is still insufficient to support the lofty stock price.

· Regulatory Barriers: Even if Tesla successfully develops autonomous vehicles, the regulatory framework in the U.S., particularly for urban areas, will be slow to approve their widespread use. Moreover, liability concerns will loom large if Tesla faces a significant safety incident.

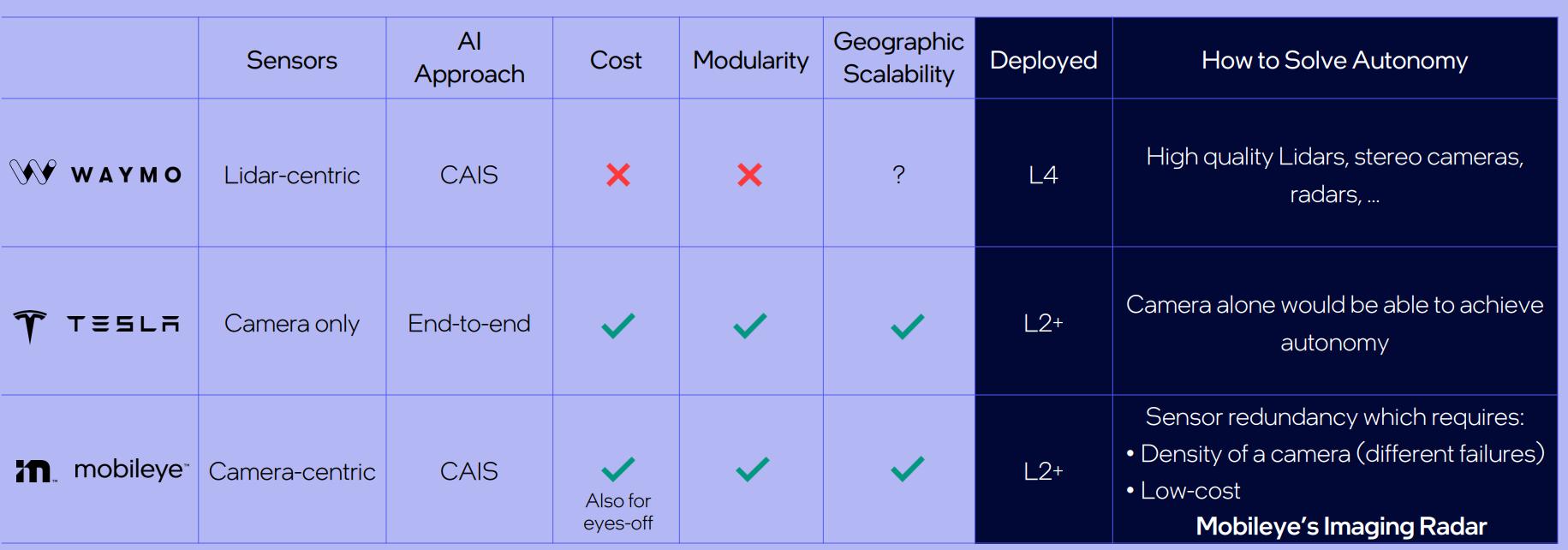

· Increased Competition: Tesla faces stiff competition from players like Waymo, Cruise, and Mobileye. The exit of GM from the robotaxi market through its Cruise division highlights the inherent difficulty of scaling such a service profitably. As competitors like Waymo adopt a more cautious approach, Tesla’s push for rapid expansion could be a costly misstep.

Approaches to Solve Autonomy

Source: Mobileye

Deteriorating Competitive Advantage

Tesla’s once-dominant position in the EV market is eroding due to increasing competition and pricing pressures:

· Competitive Pricing: The global EV market is maturing, and Tesla has been forced to cut prices to stay competitive. Its average sales price (ASP) fell from $51,155 in 2022 to $43,409 in 2023, and it continues to decline in 2024. While these price cuts may drive sales volume, they further compress margins and strain Tesla’s profitability.

· Market Saturation: While the International Energy Agency (IEA) projects strong growth in the global EV market, Tesla’s market share is increasingly vulnerable. New entrants are improving quality, offering competitive prices, and innovating faster than Tesla can keep up.

· Energy Storage Business: Tesla’s energy business is a positive but minor contributor compared to its automotive division. While growth is expected, the size of this segment remains small, and it is unlikely to significantly impact Tesla’s valuation in the short term.

Strong Sell Recommendation

Tesla's stock has surged due to optimism surrounding autonomous vehicles and political developments, but the company's growth trajectory faces substantial risks. Margin compression, intensifying competition, and technological limitations—particularly in autonomous driving—make Tesla’s valuation increasingly unsustainable. Given Tesla’s high P/E ratio and the speculative nature of its future growth, the stock is overvalued. The company’s dominance in the EV market remains, but its growth prospects are overly optimistic, making it a Strong Sell in the near to medium term.

Utilizing a forward P/E ratio of 160-170 times the forward EPS of 2.3, we arrive at a target price range for Tesla of $368 to $391, indicating a potential valuation based on expected earnings per share.

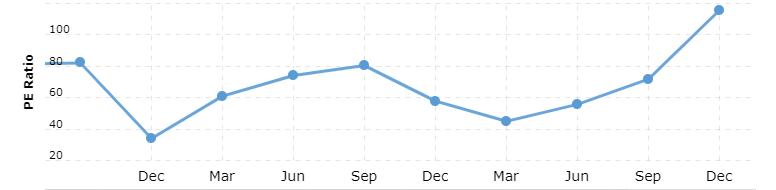

Tesla TTM P/E Ratio

Source: Macrotrends