Tesla Q1 2025 Earning Report Review: Autonomous Driving and Robotics Lead Future Growth

TradingKey - Tesla's Q1 2025 earnings results revealed short-term financial pressure, with core data lower than market expectations, and both revenue and profitability facing challenges. Against the backdrop of sales and profit pressure, Musk remains confident in Tesla's future. He emphasized that Tesla is undergoing a transition period, and the company is in the process of transforming from a traditional automaker to a technology-driven integrated ecosystem. Autonomous driving technology and humanoid robots are the core drivers of Tesla's future growth. This is the key driver for Tesla's future growth.

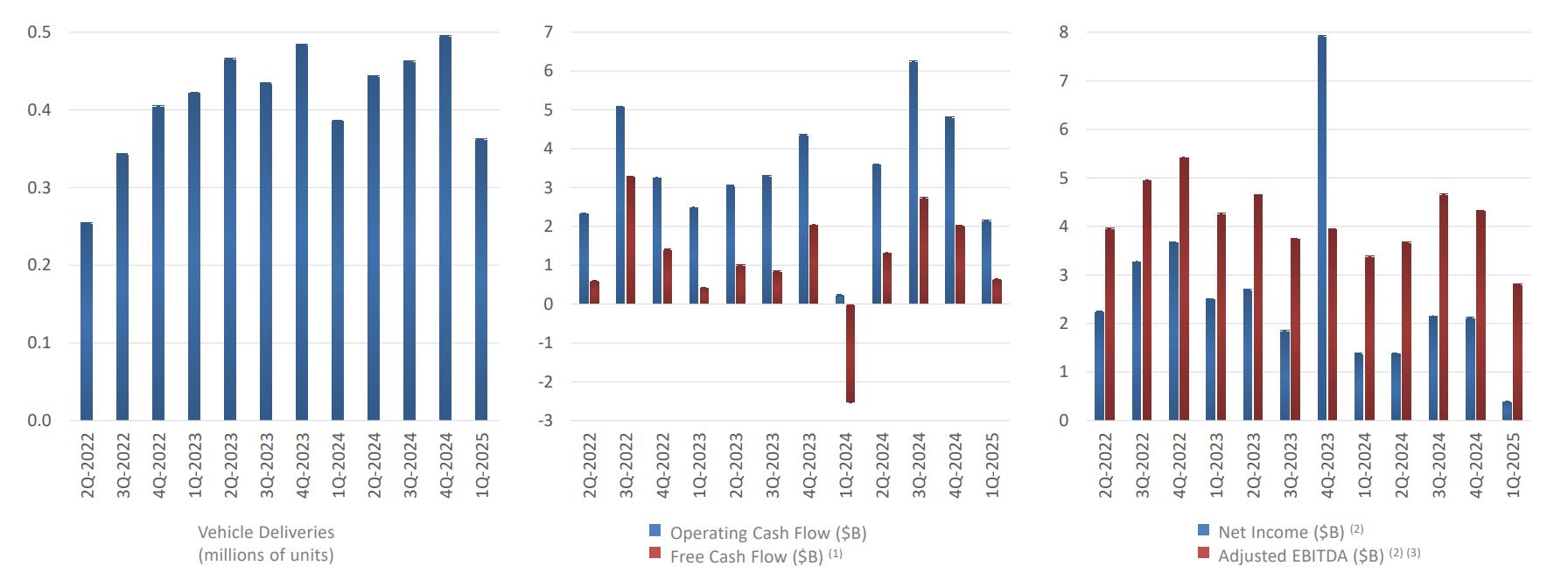

Core Financial Data

· Revenue: $19.335 billion, down about 9% year-on-year, lower than the market expectation of $21.35 billion, showing some revenue pressure.

· Vehicle deliveries: about 337,000 vehicles, down 13% year-on-year, the lowest in the past three years, mainly affected by the Model Y production line upgrade and the macroeconomic environment.

· Gross margin: 16.3%, down from 17.4% in the same period last year, reflecting the pressure of rising costs and price adjustments.

· Free cash flow: $664 million, up year-on-year, but down month-on-month, still positive.

· Net Income: $409 million, down 71% year-on-year, mainly dragged down by the decline in deliveries and increased R&D investment.

Source: Tesla

Although the financial performance in Q1 was not satisfactory, Q1 is usually the off-season for the automotive industry, and the short-term impact of the Model Y production line upgrade has further exacerbated the decline in deliveries. These factors indicate that the current financial data may not fully reflect Tesla's true potential. Tesla's strategic focus is on long-term technological innovation and business diversification, rather than short-term sales and profit performance.

Business Segment Analysis

Source: Tesla, TradingKey

· Automotive: Revenue fell 20% year-on-year, which was the main factor dragging down overall performance. The gross profit margin of the automotive business also declined, but it was still higher than market expectations.

Source: Tesla

· Energy: Revenue increased 67% year-on-year, with a particularly strong performance. Strong demand for Megapack drove the energy storage business’s gross margin to a record high, while Powerwall 3 continued to receive high market acceptance despite supply constraints.

Source: Tesla

· Services and other: Revenue increased 15% year-on-year, but low margins in used car and insurance businesses put pressure on overall profitability.

Judging from the performance of sectors, Tesla's energy business is rapidly emerging as a new growth engine, especially in the context of global energy transformation, hedging the risk of decline in the automotive business.

Tariffs & Supply Chain Risks

Tesla has been actively responding to tariff and supply chain risks, reducing costs and circumventing trade barriers through localized production. Currently, Tesla's North American vehicle localization rate exceeds 85%, and the local rate of Shanghai vehicles exceeds 95%. The localization level of the Berlin plant is also increasing.

This regionalized production model significantly reduces the impact of trade barriers, enabling Tesla to remain competitive in a complex geopolitical environment. In addition, Tesla's vertical integration is unparalleled in the automotive industry, and the company controls the core links of the industrial chain from lithium refining to battery production. Its lithium refinery built in Texas is one of the world's largest non-Chinese lithium refining facilities, ensuring the cost advantage of battery production. Musk emphasized that Tesla's battery cost per kilowatt-hour is the lowest in the industry, which provides a solid foundation for the company in price wars and supply chain fluctuations.

However, tariff issues remain a major challenge for Tesla. The United States' imposition of tariffs on Chinese-made LFP batteries has directly affected Tesla's energy storage business. To address this issue, Tesla is building an LFP battery factory in the United States and actively looking for non-Chinese suppliers, but its supply capacity is still limited in the short term. In addition, the complexity of the global trade environment also puts pressure on Tesla's capital expenditure. For example, high tariffs on imported production equipment increase expansion costs. Nevertheless, Tesla expects capital expenditures to exceed $10 billion in 2025, reflecting its firm commitment to long-term growth. By continuously optimizing the supply chain and investing in localized production, Tesla has taken a favorable position in global competition.

Autonomous Driving: Robotaxi leads the travel revolution

Tesla's autonomous driving strategy is a core pillar of its future growth, and Elon Musk sees it as the key to reshaping the transportation industry. Tesla's Robotaxi plan is to launch a fully driverless service in Austin in June 2025 and plans to expand to other cities in the United States by the end of the year. This plan is based on Tesla's purely visual autonomous driving solution, relying on self-developed AI chips and algorithms, and abandoning expensive sensors and high-precision maps. This technical path not only reduces costs, but also gives the system strong versatility, enabling it to adapt to diverse driving environments. In the Chinese market, where data is relatively scarce, Tesla's FSD system has performed well, proving the universality and scalability of its AI-driven solution.

In contrast, competitors such as Waymo rely on high-cost sensor kits, which limit production scale and commercialization speed. Musk pointed out that Tesla's Robotaxi cost may be only a quarter of Waymo's or even less, which gives it a significant advantage in the competition in the future travel market.

Source: Tesla

By providing driverless mobility services, Tesla is expected to create a highly profitable subscription revenue stream that will revolutionize car ownership and mobility. Musk has likened non-autonomous vehicles to outdated flip phones and believes that Tesla's innovation will revolutionize the transportation industry, similar to how Apple's smartphones revolutionized the communications industry.

Robotics: The future potential of Optimus

The humanoid robot Optimus is one of Tesla's most forward-looking projects. It is expected that by the end of 2025, thousands of Optimus will be deployed in Tesla factories to optimize production processes, and Tesla plans to achieve an annual production of one million units within five years. Optimus' vision is not limited to factory automation. Its long-term goal is to enter a wide range of fields such as home services and medical care and become Tesla's new growth engine. However, the development of Optimus faces supply chain challenges, especially its actuators rely on rare earth permanent magnets, and China's export controls on rare earth magnets have increased uncertainty. Tesla is actively negotiating export licenses with the Chinese government and exploring alternative suppliers to ensure the stability of the supply chain.

Although the Optimus project is still in its early stages, its potential economic value cannot be underestimated. If successfully mass-produced, Optimus will not only significantly improve Tesla's manufacturing efficiency but may also open up a whole new robot market.

Global Expansion: Opportunities and Challenges in Indian Market

Tesla's global expansion strategy aims to tap into the growth potential of emerging markets, but the high tariff barriers in the Indian market have become a major obstacle. India imposes tariffs of up to 70% on imported cars, plus a 30% luxury tax, making Tesla's vehicles much more expensive than local competitors. The company is actively negotiating with the Indian government to seek tariff reductions to enter this market with great potential. To further reduce costs, Tesla plans to build a localized factory in India. Successful entry into the Indian market will open up growth space in South Asia for Tesla and further consolidate its global leadership.

Valuation Story of Long-Term Growth

Tesla's current market value relies heavily on its future growth story rather than short-term financial performance. The financial data for Q1 2025 reflects the reality of declining deliveries and pressured profitability, which makes the current high valuation difficult to support under traditional financial indicators. However, Tesla's valuation logic is not based on the profitability of the traditional automotive business, but on its disruptive potential in autonomous driving, robotics and energy. If successful, the Robotaxi plan will significantly increase Tesla's revenue scale through high-profit subscription revenue streams, and its market potential may be comparable to the world's largest travel platform. Similarly, the mass production of Optimus may open up a whole new robotics market, whose economic value may exceed Tesla's existing automotive business.

From an investment perspective, Tesla's appeal lies in its technological leadership and ecosystem synergies, but it also comes with high risks. Autonomous driving and robotics still need to overcome technical, regulatory and supply chain challenges, and global expansion also faces geopolitical and policy uncertainties. For long-term investors, Tesla's innovation capabilities and Musk's vision provide unique investment opportunities. If Robotaxi and Optimus can be commercialized within the expected time, Tesla's market value may be further supported or even significantly increased. On the contrary, if technology development or market acceptance is not as good as expected, the valuation may face the risk of correction. Therefore, investing in Tesla requires confidence in technological innovation and long-term growth, while being prepared for short-term fluctuations.