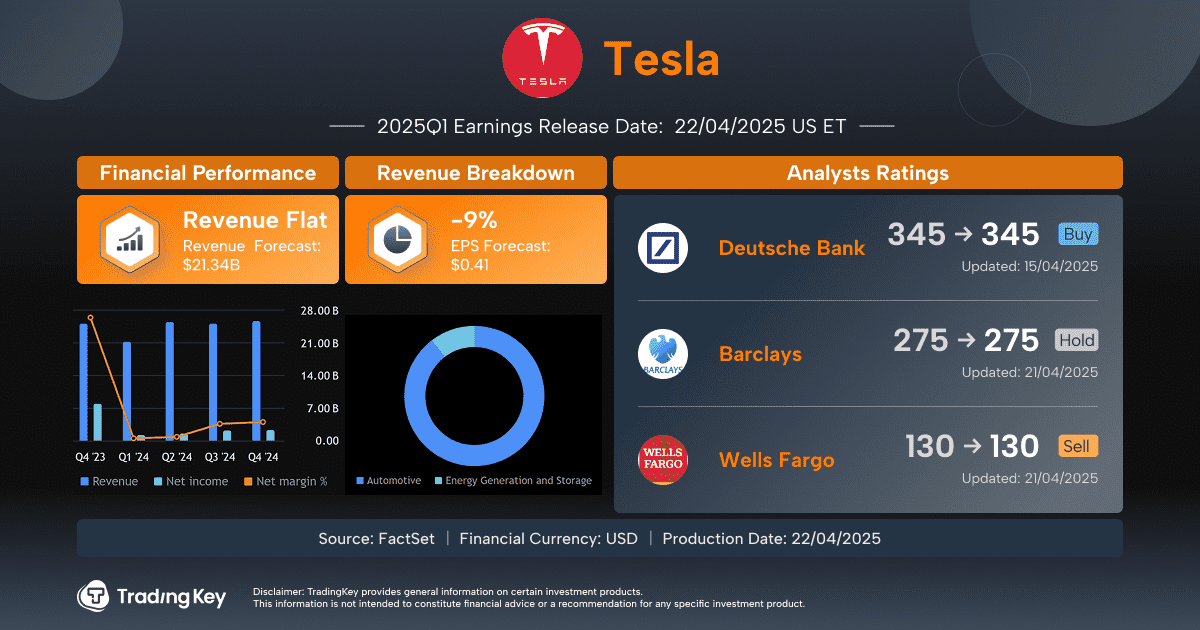

Tesla's 2025 Q1 Earning Report Preview: A Critical Moment of Hope and Challenge

TradingKey - Tesla's 2025 Q1 financial report will be released on April 22. As a leader in the global electric vehicle industry, its performance has attracted much attention from the market. Investors and analysts are full of expectations for it, but it is also accompanied by many doubts. After years of rapid growth, Tesla is currently facing a series of challenges, including short-term fluctuations caused by capacity adjustments, increasingly fierce global market competition, the squeeze in profitability from rising costs, and the uncertainty of the macroeconomic environment. These factors work together to make Tesla's Q1 performance the focus of market attention and provide an important observation window for the company's future strategic direction.

Delivery and Production: Below expectations, worst quarter in three years

In Q1 2025, Tesla's global car deliveries were 336,681, far below analysts' expectations of 377,000, down 13% from the same period last year; car production was 362,615, down 16% year-on-year. This is Tesla's worst quarterly performance in three years.

Source: S&P Global

The decline in production and delivery is mainly due to the adjustment of the Model Y production line. As Tesla's main sales model, the conversion and upgrade of its production lines in Texas, Fremont, Shanghai and Berlin Super Factory has resulted in weeks of capacity loss. Although this large-scale production line adjustment affects production in the short term, it is a strategic pain to improve production efficiency and reduce costs in the long run. Tesla said that the Model Y production line has now accelerated its recovery.

Also, the global macroeconomic environment has tightened, and consumers are less willing to buy cars, especially in the US market. Inflationary pressure and rising interest rates have suppressed bulk consumption, and the overall growth of the electric vehicle market has slowed down.

In addition, Tesla's delivery decline also reflects the natural fluctuations of the product life cycle. Model 3 and Model Y have been updated many times since 2017. They are currently in the product maturity stage. Without the stimulation of new models, sales are difficult to grow rapidly.

To summarize, although the delivery and production performance in Q1 2025 was not good, it was more the result of structural adjustments and external environmental influences, rather than a signal of demand collapse.

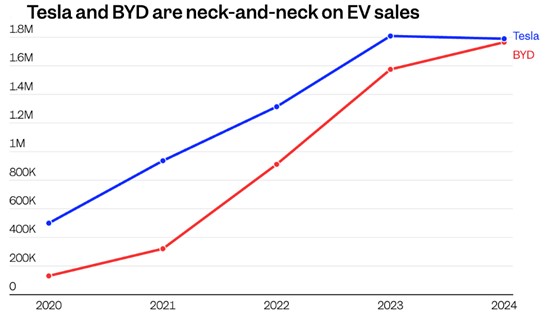

Competitive Pressure: BYD is rising rapidly, and overseas markets are under pressure

Chinese electric car giant BYD is rapidly eroding Tesla's market share, with an overseas sales target of 800,000 vehicles in 2025, doubling from 2024. BYD's global sales in 2024 will be about 1.765 million vehicles, almost catching up with Tesla's 1.789 million vehicles, and BYD's operating profit margin is close to Tesla's 6.2%.

Source: cnBeta

BYD's average selling price is much lower than Tesla's, about $15,000 to $20,000, which meets the needs of a wider range of consumer groups. At the same time, BYD has a layout in both hybrid and pure electric vehicles, with a richer product line to adapt to different market segments. With the advantages of vertically integrated supply chain, low-cost battery technology and diversified models, it is rapidly occupying overseas markets, especially Europe, Southeast Asia and Latin America. It poses a substantial challenge to Tesla. The increasingly fierce competition in overseas markets has compressed Tesla's growth space.

In addition, Tesla's supply chain and production costs are still high, especially its reliance on imported batteries and key raw materials, and its cost structure is relatively fragile. BYD further reduces costs by producing batteries and materials on its own. Therefore, Tesla must accelerate the pace of launching new models and cost control, while strengthening brand and technical barriers to stay ahead in the fierce global competition.

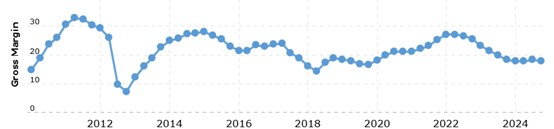

Profitability: Gross margin is under pressure, cost control becomes the key

Analysts generally expect Tesla's automotive gross profit margin in Q1 2025 to drop from 13.6% in the previous quarter to around 12.8%, a multi-year low. This reflects the dual impact of price pressure and rising costs.

Source: Macrotrends

In order to cope with the competition, Tesla had to adjust prices in some markets, especially in China and Europe, where price wars squeezed profit margins. The prices of key battery materials such as lithium, nickel, and cobalt fluctuated sharply, directly pushing up production costs. The suspension of production and reduced efficiency caused by the upgrade of the Model Y production line increased unit costs in the short term. The market expects Q1 EPS to decline to about $0.42.

Although Tesla actively promotes cost-cutting measures, such as optimizing the supply chain, improving automation levels, and developing more efficient battery technology, it is difficult to completely offset the above pressures in the short term.

Product Strategy: Model Y Lite version delayed, difficult to boost sales quickly

Originally planned to launch the cheaper and smaller Model Y "Juniper" version in Q1 2025, it will open up a larger market space by reducing costs and prices. It is expected to reduce costs by about 20% compared to the current model, with an annual production target of 250,000 vehicles, but mass production may be delayed until early 2026. In addition, the simplified version of Model 3 and other potential new models have not yet clearly defined the launch schedule, and the pace of product line updates has slowed down, which may cause consumers to turn to competitors. This means that Tesla lacks strong support for new models in the first half of 2025, and the pressure on sales growth remains heavy.

Brand Impact: Musk's role has sparked controversy

Recently, Tesla's brand has been negatively impacted by CEO Elon Musk's political activities and remarks, and industry forecast that about 5% of consumer demand may be permanently lost. In the future, whether Musk can adjust his strategy, focus on company operations and improve public relations will directly affect Tesla's market performance and investor confidence.

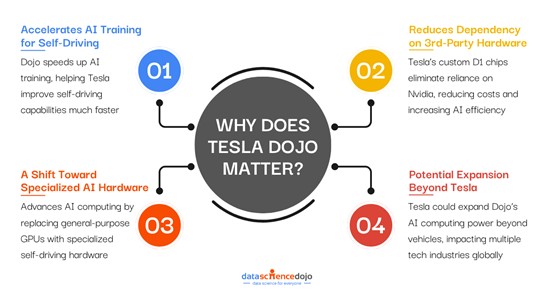

FSD & Dojo: AI-driven blueprint for future autonomous driving

Tesla continues to increase its investment in FSD. The Dojo supercomputer, as the core of AI training, supports large-scale neural network model training and improves the performance and safety of autonomous driving algorithms. Although FSD has not yet achieved full autonomous driving, the upgrade of Dojo and the continuous optimization of AI models are seen as key supports for the future commercialization of autonomous driving.

Source: Data Science Dojo

The Dojo 2 chip is expected to enter mass production and application by the end of 2025, marking a major upgrade of Tesla's AI training hardware. This second-generation chip and its system are expected to compete with Nvidia's upcoming B200 chip in performance. This progress will further promote Tesla's realization of higher levels of autonomous driving capabilities and shorten the distance from assisted driving to truly fully autonomous driving.

Robotics: Optimus still in early stages, unlikely to contribute revenue in the short term

Tesla's humanoid robot Optimus currently has limited production, with only about 5,000 units expected in 2025, and it will take 3-5 years before large-scale commercial production. Considering that factory automation has already adopted a large number of efficient equipment such as robotic arms, Optimus's market positioning and profit model still need time to be verified, and it is difficult to make a substantial contribution to the financial report in the short term.

Tariff Impact: Rising costs

The United States imposed a 25% tariff on imported electric vehicles, increasing production costs. Although Musk publicly opposed the tariff policy, the Trump administration has a tough attitude. Tariffs may suppress Tesla's sales in the short term, but they may also squeeze some competitors and form certain market barriers.

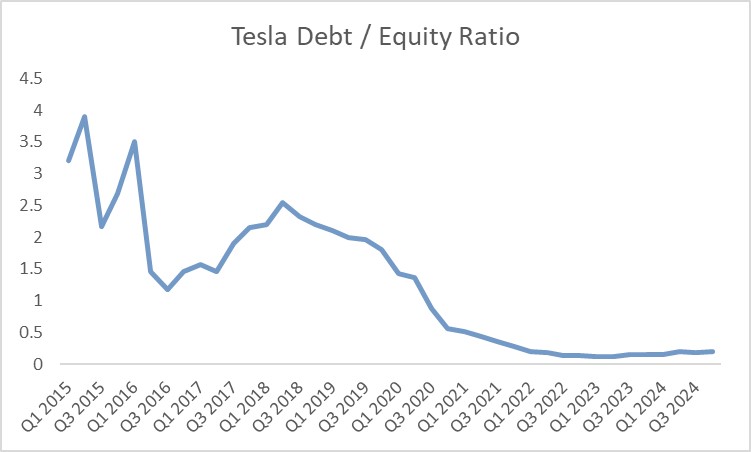

Tesla's debt-to-equity ratio at the end of 2024 was approximately 0.19, which is generally lower than the industry average, indicating that its financial leverage is low, and its debt pressure is small. More importantly, Tesla's cash-to-debt ratio is as high as 2.68, indicating that the company has sufficient liquidity to cope with short-term debt and sudden economic risks. Therefore, in the face of the 25% increase in costs and global economic uncertainty caused by the 25% auto tariff, Tesla can use its robust financial structure as a buffer to reduce financial pressure and maintain flexibility in operations and strategic adjustments.

Source: Company Financials, TradingKey

Energy Storage: Growth engine with huge potential

Tesla's energy business currently accounts for about 10% of the company's total revenue, but it is expected that the installed capacity of energy storage will double in 2025, and the proportion of revenue is expected to increase to more than 15%, and the profit margin is expected to increase to 30%. The energy storage business not only supports the stability of the power grid and the development of renewable energy but also provides green electricity for Tesla's AI data center, forming a synergistic effect. As global energy transformation accelerates, the energy storage market has huge space.

Overall Outlook: Challenges are severe, but long-term potential remains

Tesla's Q1 2025 earnings report will reflect that it is in a critical period of slowing growth and structural adjustment. Car sales and production are declining, profitability is under pressure, product updates are delayed, brand image is damaged, and the rise of competitors, especially BYD, brings huge pressure.

However, Tesla still has a leading autonomous driving AI platform, strong growth potential in energy storage business, and a relatively healthy financial structure. Whether Musk can effectively integrate multiple businesses such as automobiles, autonomous driving, robots, and energy storage, and tell a good growth story, will determine investor confidence and the company's future direction.

At present, the market's expectations for Tesla are pessimistic, and the stock price has been adjusted significantly. If there are any positive signals in the financial report, such as improved cost control, new product progress, and accelerated growth in energy storage business, it may trigger a certain rebound. Overall, Tesla has not yet fallen into a long-term downward trend, but it must meet and overcome severe challenges to maintain its leading position in the industry.