[IN-DEPTH ANALYSIS] Tesla's 2025 tariff impact and valuation outlook

Key Takeaways

· Tariff impact: Trump's tariff policy has led to rising costs for electric vehicles and energy storage, intensified market competition, and declining demand in China and the United States.

· Supply chain risks: The company is heavily dependent on China's rare earths and batteries and needs to accelerate local production and diversify its supply chain to meet challenges.

· Valuation impact: Based on our assumptions, if there is no price increase, profits will likely to fall by 20%-25%, and the target share price is about $100; price increases can alleviate the impact, and the target share price is $215.

TradingKey - Trump's policy of imposing a 125% tariff on China and a 10% tariff on other countries has mainly affected Tesla's two core businesses, electric vehicles and energy storage. Electric vehicles and energy storage will contribute 79% and 10% of total revenue respectively in 2024, and are also the most sensitive to tariffs due to their high dependence on the global supply chain. Although other businesses such as solar energy, autonomous driving, AI, and robotics are also affected to a certain extent, the impact is relatively minor because they contribute less to revenue or are still in the early stages of development.

Electric vehicle business: Dual pressure from supply chain and market

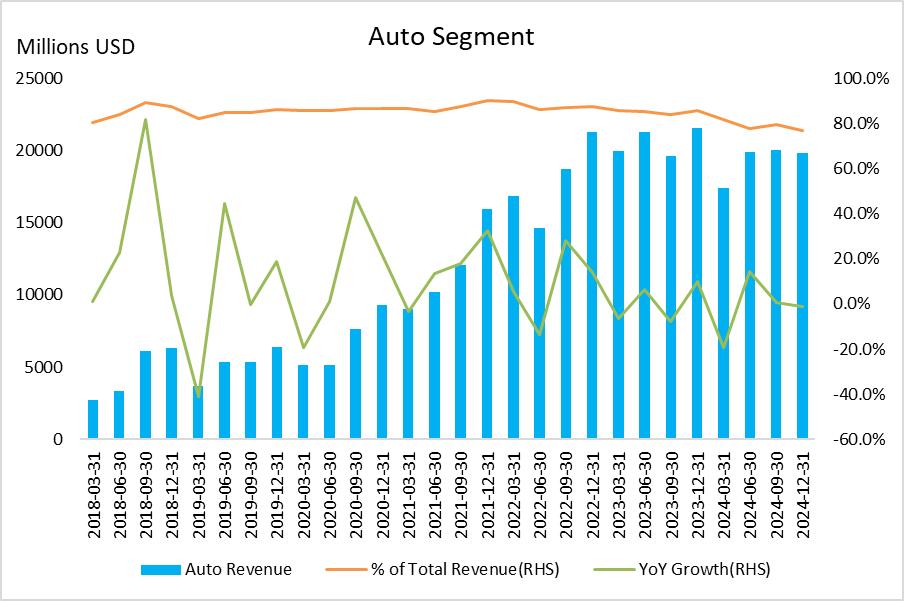

Electric vehicles are the core of Tesla. In 2024, 1,789,226 vehicles were delivered worldwide, with automotive revenue of $77.07 billion, accounting for 79% of total revenue. In the first quarter of 2025, 336,681 vehicles were delivered, a year-on-year decrease of 13%. The impact of Trump's tariffs on it is mainly reflected in rising costs and changes in the market competition landscape.

Source: Company Financials, TradingKey

1. US Market: Trade-off Between Localization Advantages and Component Costs

In 2024, Tesla delivered about 630,000 vehicles in the United States. These vehicles are all produced by the Fremont plant and the Austin plant, including Model Y, Model 3, Model S, Model X and Cybertruck. The sales distribution in 2024 is roughly as follows: Model Y has 370,000 vehicles (60%), Model 3 has 190,000 vehicles (31%), Model S/X has 32,000 vehicles (5%), and Cybertruck has 39,000 vehicles (6%).

From May 2025, Trump imposed a 25% tariff on auto parts, and Chinese goods were subject to a 125% tariff. Since Tesla's entire vehicle is produced in the United States, its entire vehicle is not directly affected by tariffs, but about 30% of its parts are imported from countries such as Mexico. In 2024, Tesla's average revenue per vehicle is about $43,100, with a gross profit margin of 18%, and the average cost per vehicle is approximately $35,342 (43,100 × (1 - 18%)). Of this, approximately 30% of imported parts (approximately $100,603) are subject to a 25% tariff, which will increase the cost of each vehicle by approximately $2,650, bringing the total cost to $37,993.

If increase prices:

To offset rising costs, Tesla may raise prices for its main models. For example, the price of the Model Y long-range all-wheel drive version can be increased from $48,990 to $50,000, and the Model 3 rear-wheel drive version can be increased from $38,990 to $40,000, with an average increase of about 2.6%. Taking into account the $7,500 federal tax credit, the effective price of the Model Y will increase from $41,490 to $42,500, and the Model 3 will increase from $31,490 to $32,500. Bloomberg analysis shows that Tesla's average price elasticity in the US market is about -3.4, that is, a 1% price increase leads to a 3.4% decrease in demand. This high elasticity reflects that the electric vehicle market is more sensitive to prices, especially mid-range models. It is expected that a 2.6% increase will lead to a decrease in demand of about 8.8%.

2025 Assumptions: Assuming that the US sales in 2025 were originally 630,000 units, a decrease of 8.8% to 580,000 units, and assuming that the growth of Cybertruck squeezed out the market share of some other models:

· Model Y (60% → 58%, 337,440 units): price increase to $50,000.

· Model 3 (31% → 30%, 173,280 units): price increase to $40,000.

· Model S/X (5%, 29,000 units): average price of about $100,000 (Model S $94,990, X $99,990, including options).

· Cybertruck (6% increase to 7%, 40,600 units): average price of about $85,000 (basic version $79,990, fully equipped $99,990).

Taking into account the impact of tax reductions, the ASP of 2025 vehicles is $45,350, and U.S. sales will drop from 630,000 to 580,000, with revenue increasing by approximately $900 million.

If not increase prices:

The global delivery volume forecast for 2025 is 1.8 million vehicles, and the US delivery volume forecast is 600,000 vehicles. The total cost will increase by about $1.6 billion (600,000 × $2,650). Even if there is no price increase, tariffs will significantly increase the cost of living for American consumers in the short term. The first to be affected is car consumption, and consumers will reduce or postpone the purchase of new cars. In the first quarter of 2025, the sales volume of electric vehicles in the United States has dropped by 10% year-on-year, indicating that consumers are more willing to postpone car purchases. If we conservatively assume that sales will drop by 8.8% in 2025, the revenue loss will be about $2.28 billion (600,000 × 8.8% × $43,100).

If the price is not adjusted, the gross profit margin in the US market will drop from 18% to about 12% (43,100 - 37,993) ÷ 43,100), which will significantly compress profits. The high prices of Model S/X and Cybertruck buffer some of the cost pressure, but Model Y and Model 3 account for a large proportion of sales (90%) and are highly price sensitive. The overall decline in gross profit margin still poses a significant challenge to Tesla's finances.

Tesla's global automotive business gross profit margin will be affected by the US market. The global delivery forecast for 2025 is 1.8 million vehicles. There is no tariff impact on non-US markets, maintaining an 18% gross profit margin and a per-vehicle gross profit of $7,758. If the US market does not increase prices, the gross profit margin will drop to 12%, with a per-vehicle gross profit of $5,107. The global total gross profit dropped from $14.2 billion to $12.4 billion, with an overall gross profit margin of about 15%. The $2 billion loss in gross profit may limit Tesla's investment in fully autonomous driving technology, low-cost vehicle development, or factory expansion.

Source: TradingKey

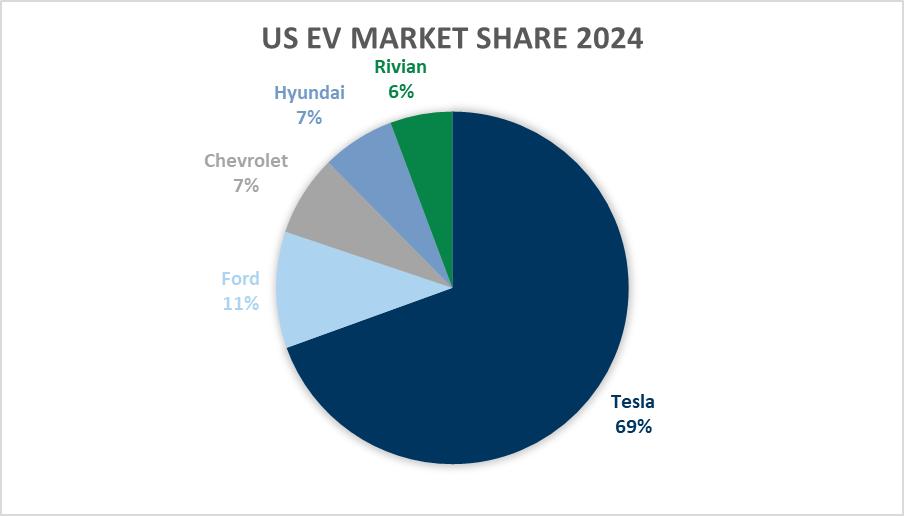

Nevertheless, competitors such as Ford Mustang Mach-E and Chevrolet Equinox EV are subject to a 25% tariff because they are imported from Mexico, which increases costs by about $2,000-3,000. Based on the CIF price of $33,600-43,995, the USMCA-compliant parts are tax-free. Therefore, compared with Tesla, which is mostly produced in the United States, it is at a disadvantage. Tesla's localization advantage may further expand its market share to more than 50%. However, if Tesla does not raise prices, profit compression will weaken its capital investment capacity and affect its long-term competitiveness.

Source: Yahoo Finance, TradingKey

2. China market: retaliatory tariffs and intensified competition

The Shanghai factory is Tesla's global production center. In 2024, Tesla's Shanghai Super Factory delivered more than 916,000 vehicles, of which 660,000 were delivered in mainland China, accounting for 72% of the Shanghai factory's deliveries and 36.7% of Tesla's global deliveries. The remaining approximately 260,000 vehicles were exported to Europe, Australia, Southeast Asia, South America and other places, accounting for approximately 28% of the Shanghai factory's deliveries, supporting Tesla's global supply chain.

Since the Shanghai factory mainly produces locally, the US's 125% tariff on Chinese goods does not directly affect local sales, but China imposed a 125% tariff on US goods from April 10, 2025, impacting the US exports of Model S and Model X to China, about 50,000 vehicles in 2024. Model S and Model X are high-end models produced by Tesla from the Fremont factory in the United States and exported to China, which are different from the Model 3 and Model Y produced in the Shanghai factory. Based on an average selling price of $100,000, the industry estimates that its production cost is approximately $70,000, with a gross profit of $30,000 per vehicle. China's 125% tariff increases taxes and fees by $87,500 per vehicle (70,000 × 125%). If Tesla partially passes on the tariff (assuming 50%), the price will increase from $100,000 to $150,000, a 50% increase. Based on the price elasticity of high-end models of about -1.5, demand will fall by 75% (50% × 1.5), and sales will fall from 50,000 to 12,500. Revenue will fall from $500 million to $187.5 million (12,500 × 150,000), a loss of approximately $312.5 million; gross profit will fall from $150 million to $37.5 million (12,500 × 3,000), a loss of $112.5 million. This impact is limited to imported high-end models, and the Model 3 and Model Y produced by the Shanghai factory are not directly affected due to localized production.

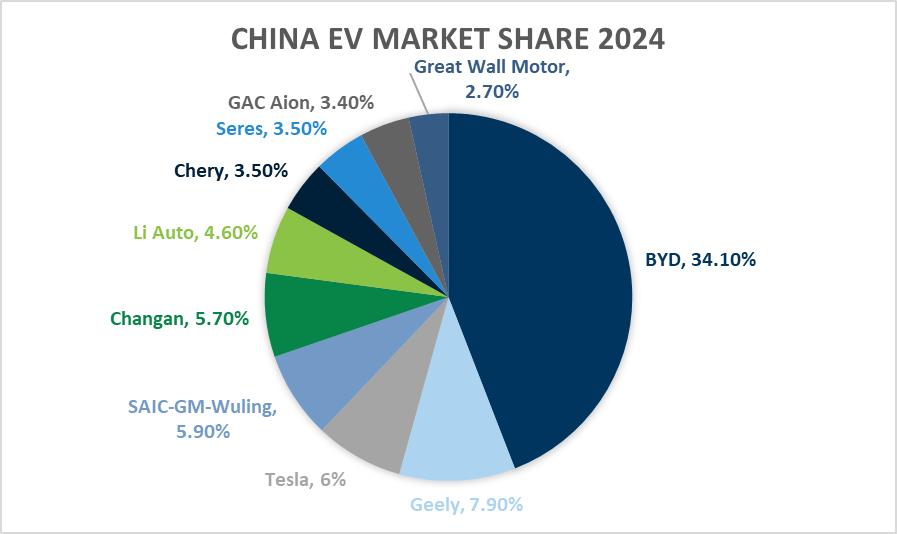

More importantly, the greater challenge in the Chinese market lies in intensified competition and potential changes in consumer sentiment. BYD is expected to surpass Tesla to become the global leader in pure electric vehicles in 2025. Its sales in 2024 have reached 4.27 million, including 1.77 million pure electric vehicles, close to Tesla's global delivery of 1.79 million. In China, BYD delivered 416,388 vehicles in the first quarter of 2025, a year-on-year increase of 39%. In contrast, Tesla's delivery volume in China during the same period was 172,754 vehicles, a year-on-year decrease of 21.8%, showing signs of fatigue. Tesla's market share in China has dropped from 7.8% in 2023 to 6% in 2024. Local brands continue to occupy space with low prices (such as BYD Seagull's starting price of $19,267 compared to Model 3's $32,661) and technological advantages.

Source: CPCA, TradingKey

Although the localization rate of parts in the Shanghai factory exceeds 90%, the escalation of the China-US trade war may trigger consumers' boycott of American brands. Tesla CEO Elon Musk's interactions with the US government have caused some controversy on Chinese social media, and some consumers have begun to question its American brand positioning. In March 2025, the customer flow of Tesla stores in Shanghai fell by about 15% year-on-year, indicating fluctuations in consumer confidence. At the same time, Tesla is highly dependent on the Chinese market and consolidates its market position through localized production in the Shanghai factory. However, trade frictions may amplify consumers' sensitivity to the dual identity of brands. Tesla's price disadvantage is amplified in the context of the trade war, and consumers may prefer local brands due to economic pressure. If trade frictions continue, the damage to foreign trade companies may weaken the purchasing power of middle-class consumers and indirectly suppress Tesla's demand. If this trend continues, Tesla's sales in China may fall by 5%-10% from 660,000 vehicles in 2024 to 630,000 to 590,000 vehicles. Based on the average revenue of $43,068 per vehicle, this decline will result in a revenue loss of $1.3 billion to $3 billion.

3. Supply Chain Risk: Rare Earth and Batteries

Electric vehicle batteries account for about 40% of the cost of a Tesla vehicle, about $14,000. Tesla's global supply chain relies on Chinese rare earths, and China controls 90% of the world's rare earth supply, as well as suppliers such as CATL. In 2025, the Shanghai factory is expected to deliver 927,000 vehicles, using CATL LFP batteries, with a localization rate of over 90%, but it still requires Chinese rare earth raw materials. Of the battery cost, raw materials account for about 60% ($8,500), and rare earth-related accounts for 30% ($2,550). If China restricts rare earth exports to the United States due to the trade war, global rare earth prices may rise by 50%, and the cost of non-Shanghai factories (873,000 vehicles) will increase by $1,275 per vehicle, and expenditures will increase by $1.1 billion. Because China prioritizes local supply, the Shanghai factory may see a slight increase in rare earth prices by 10% ($255 per vehicle), an increase in expenditure by $240 million, and global total expenditure of approximately $1.34 billion. If the rare earth backlog leads to a 10% domestic price drop (-$255 per vehicle), Shanghai will save $240 million, and the global expenditure increase will be reduced to $860 million.

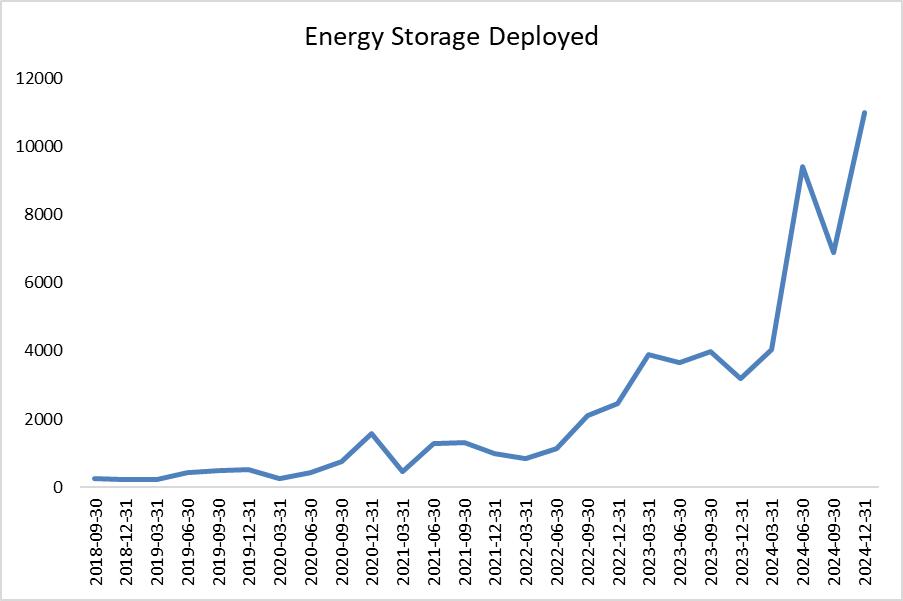

Energy storage business: supply chain dependence and transformation pressure

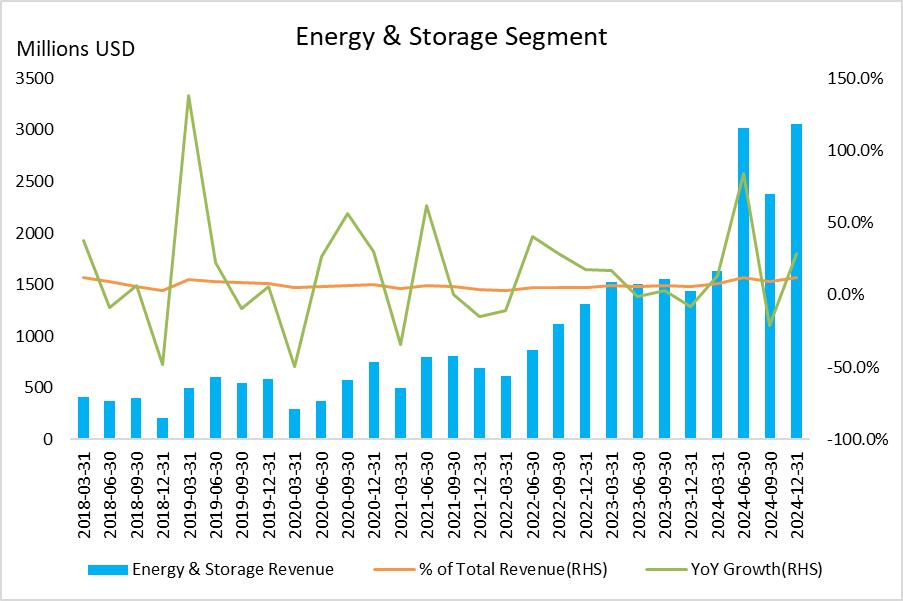

Energy storage is Tesla's fastest growing business, with 31.4 GWh deployed in 2024 and revenue of $10 billion, a year-on-year increase of 67%, accounting for 10% of total revenue. 10.4 GWh was deployed in the first quarter of 2025, showing continued momentum. Tesla's energy storage products are highly dependent on the Chinese battery supply chain, especially CATL's lithium iron phosphate (LFP) batteries, but the Shanghai Megafactory does not directly export to the United States, and the battery procurement of the Lathrop Megafactory in the United States is diversified, so the direct impact of the 125% tariff on China is limited. CATL's plan to build a factory in the United States may bring about cost changes, and Tesla needs to adjust its supply chain to maintain profits and competitiveness.

Source: Company Financials, TradingKey

Source: Company Financials, TradingKey

1. Cost surge and profit compression

Tesla's energy storage products Megapack and Powerwall mainly use LFP batteries from CATL, which is one of its core suppliers. Shanghai Megafactory will produce 40 GWh in 2025, with the first batch sold to Australia and then to China and the Asia-Pacific market. The cost of each GWh battery is about $110 million, with revenue of $149 million/GWh and a gross profit margin of about 26%. The Shanghai factory uses all local CATL batteries, with a total cost of $4.4 billion and a gross profit of $1.56 billion, with stable profits and no external interference.

The Lathrop Megafactory in the United States will have a production capacity of 40 GWh in 2024 and supply the US market. Some of its batteries come from CATL, but they are not imported directly from China but produced in other regions through CATL's overseas factories or partners. Due to factors such as transportation, the cost of these overseas batteries has slightly increased to about $130 million/GWh, with revenue of $250 million/GWh. The global deployment in 2025 is expected to be 60 GWh, with a gross profit of about $3.96 billion, showing the current stability of the supply chain.

2. Export strategy and stability of Shanghai factory

The Shanghai Megafactory will produce 40 GWh in 2025, with the first batch sold to Australia (1-2 GWh), and will subsequently mainly supply China (about 10 GWh) and the Asia-Pacific market (about 29 GWh, such as Europe, Australia, and New Zealand). There is no plan to sell directly to the United States. All of its 40 GWh uses local CATL batteries, with stable costs and gross profits, totaling $1.56 billion. Even if the Asia-Pacific market faces a 10% ordinary tariff and costs rise to $121 million/GWh, the gross profit will still reach $1.12 billion, with limited profit fluctuations. The Shanghai factory focuses on the Asia-Pacific market, avoiding the complexity of the US market and maintaining the stability of the supply chain and profitability. Even if CATL builds a factory in the United States and adjusts its capacity allocation, the local supply priority of the Shanghai factory is not expected to be affected.

3. Competitiveness and potential pressure in the US market

The United States is the largest market for Tesla's energy storage revenue, contributing $5 billion in 2024, accounting for more than 50% of total revenue. The revenue per GWh is about $250 million US dollars. Tesla has two major energy storage factories in the United States: Lathrop Megafactory (capacity of 40 GWh in 2024) and Nevada Gigafactory (10 GWh energy storage), which jointly supply the US market. The newly planned Texas factory is expected to have difficulty reaching 20 GWh capacity before 2026. Some of Lathrop's batteries come from CATL, but they are not imported directly from China, but supplied through CATL's overseas factories or partners. For example, CATL has production bases in Germany and Hungary-the German factory has been put into production (14 GWh), and the Hungarian factory is expected to be operational by the end of 2025 (100 GWh). In addition, the batteries in Malaysia may be manufactured by local partners rather than CATL directly setting up factories. The cost of batteries from these overseas sources is slightly higher than the $110 million US dollars/GWh in China due to factors such as transportation, reaching about $130 million/GWh.

CATL plans to build a factory in Michigan, USA, with an investment of $2 billion, and put it into production in 2026. Since the labor and land costs in the United States are 30%-50% higher than those in China, the cost of battery production may rise from 110 million/GWh to $140 million-165 million/GWh. If Tesla purchases from CATL's US factory, the gross profit will drop to $85 million/GWh, and the specific impact depends on the purchase volume. At the same time, the cost of batteries produced by CATL's overseas factories or in Malaysia and other places is expected to remain at 130 million/GWh. If the United States restricts these supply chains due to geopolitics in the future, Tesla can turn to South Korea's LG Chem (cost $150 million/GWh) or produce 4680 batteries on its own, but profits will still be under pressure. Global deployment of 60 GWh If CATL's costs in the United States rise, the overall gross profit may drop from $3.96 billion to $3.3 billion, a compression of 10%-15%. But in the long run, its US production capacity will support Tesla's localization, reduce its dependence on China's supply chain, and reduce geopolitical risks. To cope with this transition period, Tesla needs to accelerate the construction of its Texas factory and ensure supply chain diversification to maintain the growth momentum of its energy storage business.

Other businesses: limited impact

Although electric vehicles and energy storage are the first to be affected, other businesses are also affected by tariffs, but the impact is relatively small, mainly due to low revenue contribution or development stage limitations.

1. Solar Energy

Revenue in 2024 will account for less than 2%. Solar panels rely on Chinese silicon wafers (80% of the global supply), and the 125% tariff increases the cost per watt from $0.2 to $0.45, and the cost of 5GW deployment increases by $125 million. However, the business is small, and the overall impact is only 0.6% of total profits.

2. Autonomous Driving & AI

Revenue is not disclosed separately, but it relies on Chinese chips and sensors. The 125% tariff increases the hardware cost of each vehicle by $750 and $750 million for 1 million vehicles. Since FSD has not yet been monetized on a large scale, the impact is mainly reflected in R&D costs rather than revenue.

3. Robotics

The Optimus project will be put into trial production by the end of 2025, with an estimated production of 1,000 units. The cost of each unit will increase by $12,500 due to tariffs on Chinese parts, totaling $12.5 million. There will be no revenue in the early stage, and the impact will be limited to the R&D budget.

4. Charging network and insurance

The charging network will have revenue of $1 billion in 2024, and the 125% tariff will increase the cost of 5,000 new charging piles by $50 million; insurance revenue will be $500 million, which will be indirectly affected by the price increase of electric vehicles. The two account for a low proportion of revenue (1% and 0.5%), and the impact is weak.

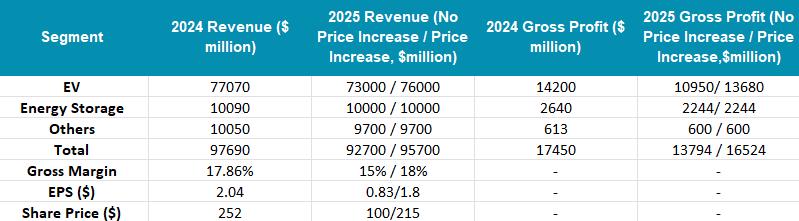

Comprehensive Financial Impact

Source: TradingKey

Valuation

The current P/E ratio is 123, reflecting the market's high growth expectations for Tesla as a concept stock in 2024, and is particularly optimistic about its potential in the fields of autonomous driving and energy storage. In the scenario of no price increase in 2025, total revenue is $92.7 billion, gross profit is $13.8 billion, and gross profit margin is 15%. Due to rising tariff costs and intensified competition in the Chinese market, EPS is expected to be $0.83, and the P/E ratio will remain around 120 (it is more reasonable to maintain a P/E ratio of 120, because Tesla's valuation is more based on long-term technological prospects rather than short-term gross profit margin fluctuations, and it maintains a premium for concept stocks), and the target stock price is $100. In the price increase scenario, total revenue is $95.7 billion, gross profit is $16.5 billion, gross profit margin is 18% (close to the 2024 level), EPS is $1.8, P/E remains at 120, and the target stock price is $215.

Conclusion

Trump's 125% tariff on China and 10% tariff on other countries mainly impact Tesla's electric vehicle and energy storage businesses. Electric vehicles are the first to be affected due to their high revenue share and the complexity of the global supply chain, facing the dual pressures of rising costs and market competition; energy storage, as a growth engine, will be impacted due to the blow to its dependence on Chinese batteries. Although other businesses are affected, the impact is limited due to their small scale or immaturity. Tesla needs to respond through localized production and market adjustments, otherwise its profits may shrink by 20%-25% in 2025, and the growth of its core business will face severe challenges. In the short term, the stock price has some room to fall, but in the long term, technological advantages will still provide support for Tesla's long-term growth.