US Tariffs: Will This Be a Disaster?

By Jason Tang

Executive Summary

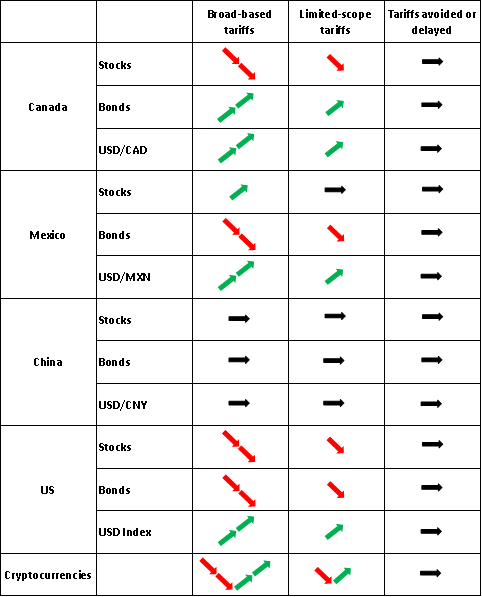

We categorize the additional US tariffs into three potential scenarios: 1) Broad-based tariffs; 2) Limited-scope tariffs; and 3) Tariffs avoided or delayed. The table below summarizes the expected impacts on the financial markets of Canada, Mexico, China, the US and cryptocurrencies under each scenario.

Note 1: This table is based on a comparison with the baselines.

Note 2: Stock and bond returns are measured in local currencies.

Note 3:

1. Tariff Turmoil

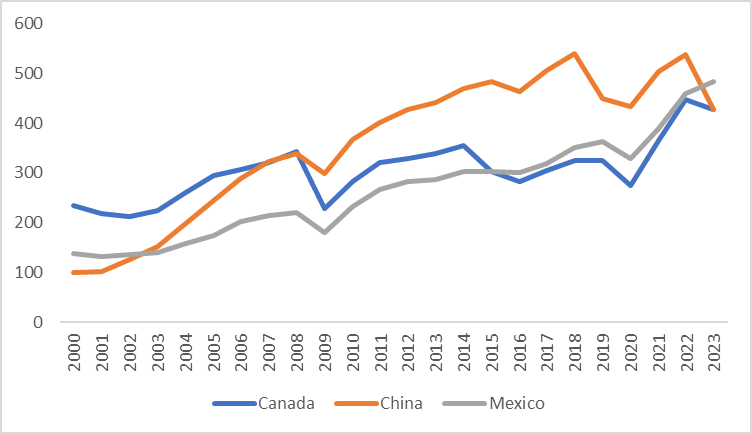

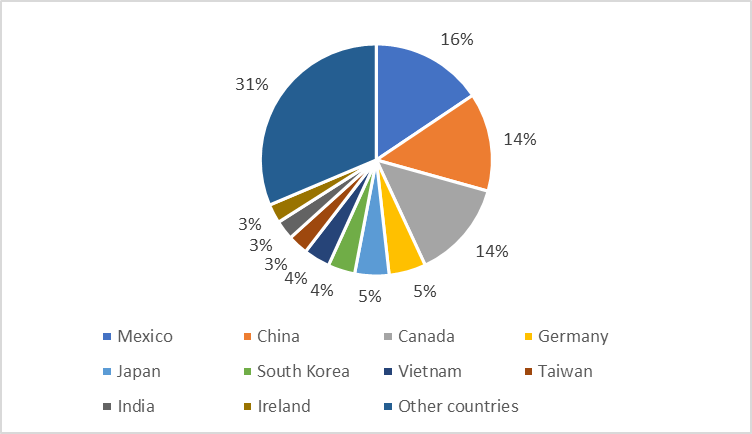

Mexico, Canada and China are the three largest sources of US imports, collectively accounting for 43% of total imports (Figures 1.1 and 1.2). In response to concerns over illegal immigration, fentanyl and trade fairness, on 1 February 2025, newly inaugurated US President Donald Trump announced an additional 25% tariff on imports from Canada and Mexico—including a 10% tariff specifically on Canadian energy imports—and an additional 10% tariff on goods from China.

In retaliation, the three affected countries planned to implement the following countermeasures:

· Canada announced a 25% tariff on US imports worth 155 billion CAD.

· Mexico expressed willingness to negotiate border issues with the US but left open the possibility of imposing higher tariffs on American goods.

· China declared a 15% tariff on US coal and liquefied natural gas (LNG) starting 10 February, along with a 10% tariff on crude oil, agricultural machinery, large-engine vehicles and pickup trucks—though it signalled room for negotiation.

However, just two days later, the Trump administration postponed the tariffs on Canada and Mexico for one month and initiated talks with China.

While we believe a broad-based tariff scenario—where the full 25% tariffs on Canada and Mexico will be enacted after the one-month delay—is unlikely, this article serves as a risk warning. Our analysis focuses on the worst-case scenario (i.e., broad-based tariff scenario): the potential impact on the macroeconomy and financial markets of Canada, Mexico, China, the US and cryptocurrencies.

Figure 1.1: US goods imports (USD Billion)

Source: BEA, Tradingkey.com

Figure 1.2: US goods imports by countries (% of total)

Source: BEA, Tradingkey.com

2. Impact on Canada

2.1 Canada Macro

The new US tariffs will primarily impact the Canadian economy through foreign trade.

· Oil Sector: As the world’s fourth-largest oil producer, Canada exports 80% of its oil production, with the US as its largest buyer. A 10% tariff on oil imports could dampen Canadian energy export volumes, potentially slowing Canada’s economic growth.

· Other Goods: The 25% tariff on non-energy goods is likely to reduce US demand for Canadian exports. However, given Canada’s ability to re-route shipments through third countries, the actual impact may be less severe than market expectations.

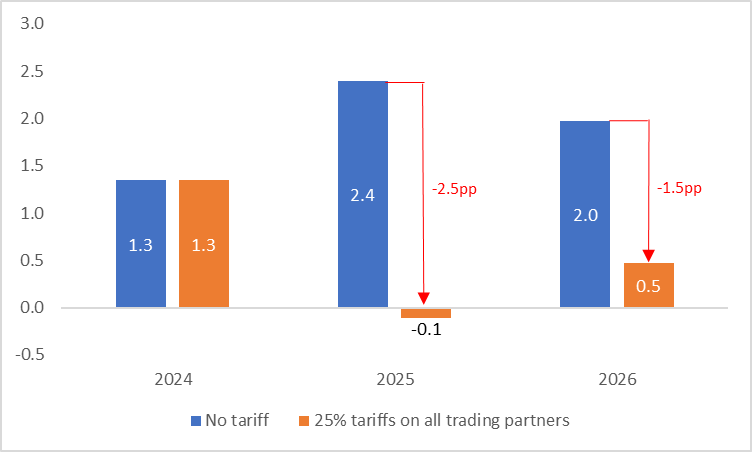

According to a Bank of Canada (BoC) analysis, if the US imposes a blanket 25% tariff on all trading partners, Canada’s GDP will decline by 2.5 percentage points in 2025 and 1.5 percentage points in 2026. Based on the IMF’s October 2024 projections, this would adjust Canada’s economic growth in 2025 and 2026 to -0.1% and 0.5%, respectively (Figure 2.1). However, the BoC’s forecast represents a worst-case scenario and we consider a broad-based tariff escalation across all trading partners to be unlikely, at least in the short term.

Like other central banks, the BoC prioritizes inflation, economic growth and employment. Canada’s retaliatory tariffs on US goods will contribute to higher domestic inflation, but with US imports comprising less than 15% of Canada’s CPI basket, the inflationary impact should be limited. If trade tensions escalate into a full-blown trade war, the BoC is expected to focus on mitigating risks to growth and employment—making more aggressive interest rate cuts a likely policy response.

Figure 2.1: Canada's GDP declines if the US imposes a 25% tariff on all trading partners (%)

Source: IMF, Tradingkey.com

2.2 Canada Stocks

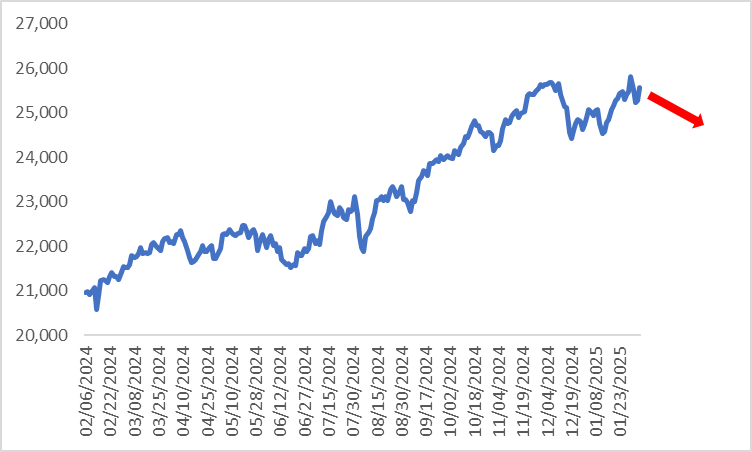

In general, the additional tariffs imposed by the US tend to harm the Canadian stock market (Figure 2.2). In terms of sectors, higher tariffs can reduce the competitiveness of Canadian energy companies in exporting to the US, thereby potentially affecting their revenue and stock prices. The North American automotive industry is highly integrated, meaning that higher tariffs could increase the production costs for Canadian automakers, which is bearish for their stock prices. Similarly, the stock prices of other manufacturing sectors besides automobiles could also be negatively affected. The indirect effects of higher tariffs, such as changes in market sentiment and investor confidence, might further depress the returns of Canadian stocks.

Figure 2.2: S&P/TSX Composite

Source: Refinitiv, Tradingkey.com

2.3 Canada Bonds

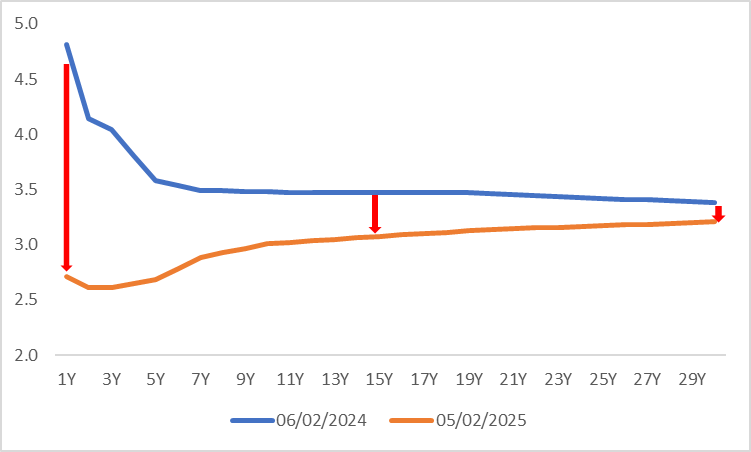

Combined with the 25bp rate cut on 29 January this year, the BoC policy rate has fallen by 200bp in this round of the rate cut cycle. If Trump's new tariff policy is implemented, the central bank's rate cuts will be greater than currently anticipated. This is likely to cause the Canadian government bond yield curve to continue shifting downward (Figure 2.3). Short-end (front-end) government bond yields are expected to decline more than long-end (back-end) as the short-end is more influenced by the policy rate. Therefore, we believe that short-duration bonds have more investment value.

Figure 2.3: Canadian government bond yield curve (%)

Source: Refinitiv, Tradingkey.com

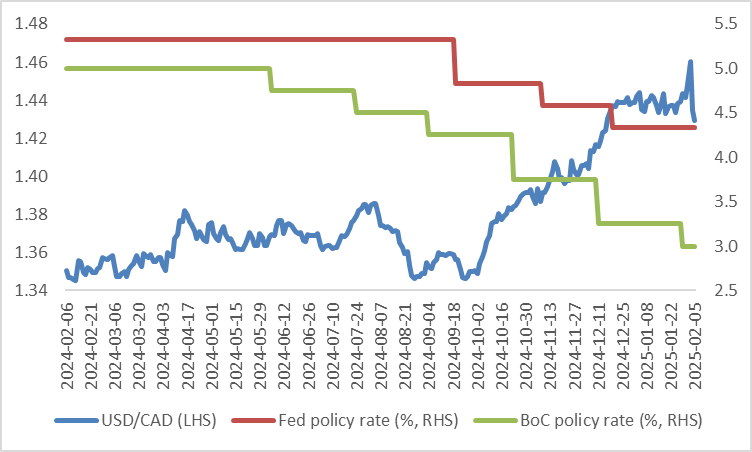

2.4 USD/CAD

The decline in exports to the US will impact the Canadian economy and contribute to the depreciation of the Canadian dollar. The BoC's interest rate cuts continue widening the interest rate differential between the US and Canada, particularly as the Fed has slowed down its rate cuts. This is likely to put additional downward pressure on the Canadian dollar. Moreover, higher US tariffs may suppress imports and reduce the US trade deficit, supporting the US dollar. As a result, the Canadian dollar is expected to weaken further against the US dollar (Figure 2.4).

Figure 2.4: USD/CAD vs. Fed and BoC policy rates

Source: Refinitiv, Tradingkey.com

3. Impact on Mexico

3.1 Mexico Macro

If Trump imposes an additional 25% tariff on Mexico in one month, Mexico's economic outlook will worsen. Export-dependent industries—such as automobiles, auto parts, computers, trucks, wires, medical equipment and mobile phones—are likely to be hit the hardest.

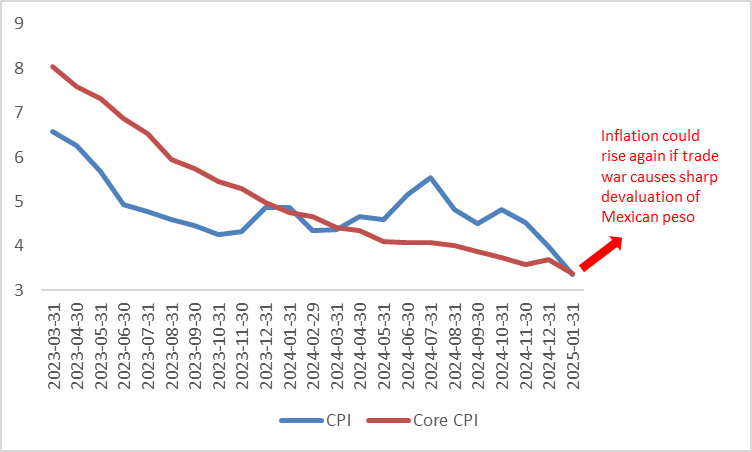

Regarding inflation, the trade war will exert significant pressure on the Mexican peso. While weak economic growth moderates inflation on the demand side, currency depreciation will have an inflationary effect. The latter is expected to outweigh the former, leading to a net rise in inflation (Figure 3.1).

Higher inflation will slow the pace of interest rate cuts by the Bank of Mexico, further weighing on economic growth. Additionally, the sluggish economy is likely to impede fiscal consolidation efforts, deepening Mexico’s fiscal challenges.

Figure 3.1: Mexico inflation (%)

Source: Refinitiv, Tradingkey.com

3.2 Mexico Stocks

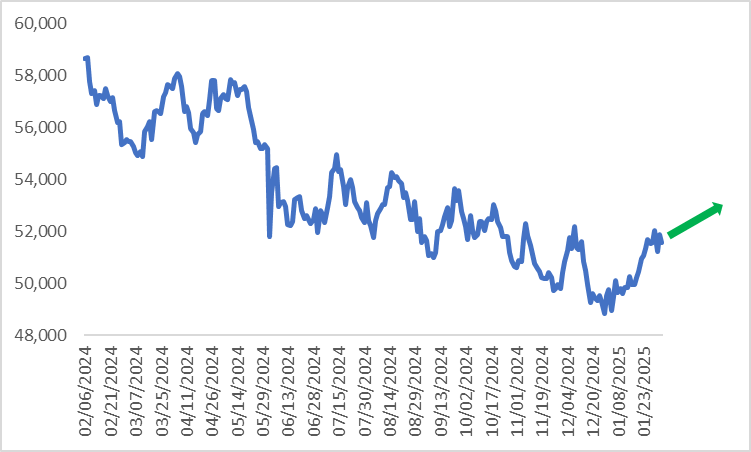

Many economists argue that higher US tariffs will hinder Mexico's economic growth and pressure the Mexican stock market. However, we hold a different view. We expect the depreciation of the Mexican peso to offset much of the negative impact of higher tariffs.

Approximately 50% of the companies listed on Mexbol generate revenue in US dollars, including export earnings from mining companies and income from US operations of consumer brands. Combined with the low valuation, this strengthens our bullish outlook for Mexican stocks (Figure 3.2). We suggest investors pay attention to companies with a high proportion of US dollar revenues. Since a depreciation of the Mexican peso would dilute profits for foreign investors, non-Mexican investors can use currency-hedging instruments to invest in Mexican equities.

Figure 3.2: S&P/BMV IPC

Source: Refinitiv, Tradingkey.com

3.3 Mexico Bonds

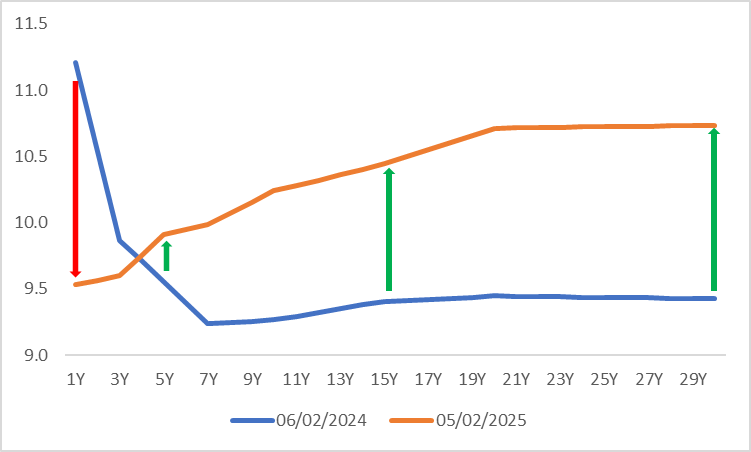

As discussed earlier, the trade war is expected to drive up inflation in Mexico, prompting the Bank of Mexico to slow the pace of interest rate cuts. This will likely result in an overall upward shift in the Mexican government bond yield curve.

Historically, during the negotiations leading up to the trade war in 2016, the Mexican yield curve not only moved higher but also became steeper. If the proposed higher tariffs are implemented this time, we anticipate a similar trend—where long-term yields rise more than short-term yields (Figure 3.3). This is because longer-duration bonds are influenced not only by policy rates but also by broader macroeconomic conditions. Given that the trade war will likely weaken Mexico’s economic growth and push up yields, we advise investors to avoid Mexican government bonds.

Figure 3.3: Mexico government bond yield curve (%)

Source: Refinitiv, Tradingkey.com

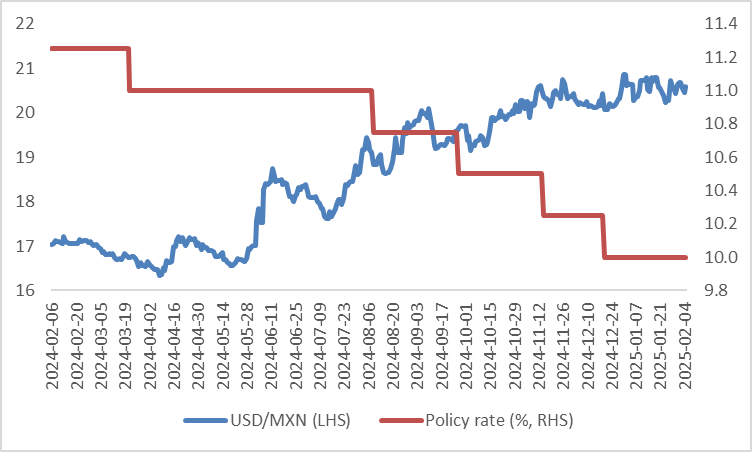

3.4 USD/MXN

Among stocks, bonds and currencies, the foreign exchange market is likely to bear the most brunt of the tariff impact. If the US imposes a 25% tariff in one month, market forces alone could drive the Mexican peso down by 25% without government intervention, effectively making the currency a buffer against the trade war.

However, a sharp currency depreciation would fuel inflation. While the Mexican government is unlikely to intervene directly in the exchange rate, the Bank of Mexico may slow the pace of interest rate cuts to prevent inflation expectations from escalating further. This monetary policy would help curb excessive peso depreciation (Figure 3.4). As a result, we expect that if higher tariffs are implemented, the Mexican peso will weaken by approximately 15% against the US dollar.

Figure 3.4: USD/MXN vs. Bank of Mexico policy rate

Source: Refinitiv, Tradingkey.com

4. Impact on China

China’s export destinations are highly diversified and its reliance on the US is relatively lower. In terms of the overall economy, China’s total international trades make up only 37% of GDP, compared to 70% in Canada and Mexico. This shows that China’s economy is less dependent on foreign trade, meaning the current 10% additional tariff has a limited impact on China’s GDP.

As China’s macroeconomic strength is largely driven by domestic factors rather than the US demand, the impact of US trade protectionism on China’s stock, bond and foreign exchange markets is minimal.

5. Impact on US

Only considering the higher tariffs imposed by the US, along with countermeasures from its trading partners, are expected to drive up inflation and slow economic growth in the US. These actions could negatively affect the US stock market while pushing up US Treasury yields and strengthening the USD index.

However, when considering Trump’s overall policy, there are both positive and negative effects on the macro economy. On the positive side, Trump's tax cuts and initiatives to encourage the return of manufacturing may provide a boost to US economic growth. On the negative side, higher tariffs and strict immigration policies could exacerbate inflation, delaying the Fed's path to interest rate cuts.

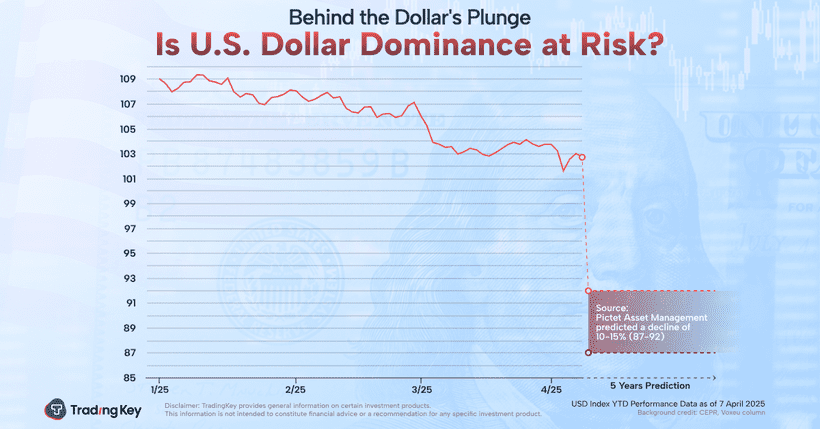

Taking into account the combined effects of US economic fundamentals, fiscal and monetary policies and Trump’s trade policies, we anticipate that US stocks will rise, while US Treasury yields and the US dollar will experience an initial increase before eventually declining. For further details, please refer to “2025 Outlook: Robust Growth and Enhanced Stock Returns, published on 23 January 2025”.

6. Impact on Cryptocurrencies

Due to the US tariff threats to Canada, Mexico and China, while the tariff issue itself is unrelated to the cryptocurrency market, the crypto market often acts as a barometer for global financial sentiment. As a result, it is typically the first to react when investor sentiment shifts from risk-on to risk-off. This was evident when Bitcoin and other altcoins sharply dropped following the tariff news, only for Bitcoin to regain lost ground after the tariff hike was postponed.

Recently, the legislative process around cryptocurrency regulation in the US has accelerated significantly. Discussions have become more focused on the strategic reserve and the role of stablecoins in Bitcoin’s future. Crypto Tsar David Sacks highlighted the goal of “creating a golden age of digital assets” at a White House press conference. Per Trump’s earlier executive order, the Presidential Digital Assets Working Group is assessing the feasibility of Bitcoin reserves. Meanwhile, the SEC has set up a new cryptocurrency task force aimed at providing a clearer regulatory framework for crypto assets.

Fifteen states in the US have introduced legislative proposals for establishing Bitcoin strategic reserves. While federal legislation on Bitcoin reserves faces greater challenges, state-level reserves are easier to implement, which could drive up Bitcoin demand. Grayscale’s application for a Litecoin spot ETF is also moving through the SEC approval process and is expected to receive approval in the current regulatory-friendly environment.

Despite these positive regulatory factors, liquidity remains insufficient. The Fed’s policy stance has lowered market expectations for interest rate cuts this year, with rates remaining high. The next rate cut is expected in the middle of this year, which is likely to limit investors’ risk appetite. As a result, there is not enough capital entering the market to support Bitcoin prices above $100,000. We expect Bitcoin’s price to fluctuate between $80,000 and $100,000 in the first half of the year.