[IN-DEPTH ANALYSIS] Eurozone: Is It Still a Good Time to Short the EUR/USD?

Executive Summary

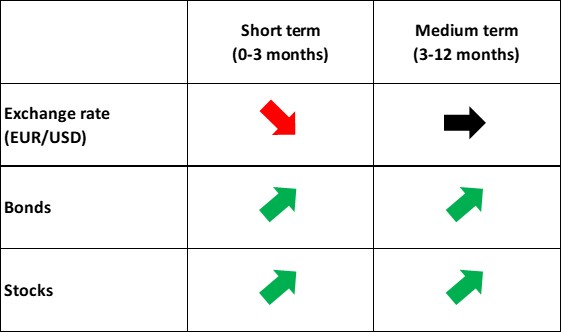

Under the combined influence of potential tariffs, growth disparities between Europe and the US and interest rate differentials, we anticipate a weakening of the euro against the dollar in the short term (0-3 months). In the medium term (3-12 months), we expect the decline of the USD Index to lead to a stabilization period for the EUR/USD. When investing in the foreign exchange market, investors should also closely monitor two uncertainties: the end of the Russia-Ukraine war and the German election.

1. Macroeconomics

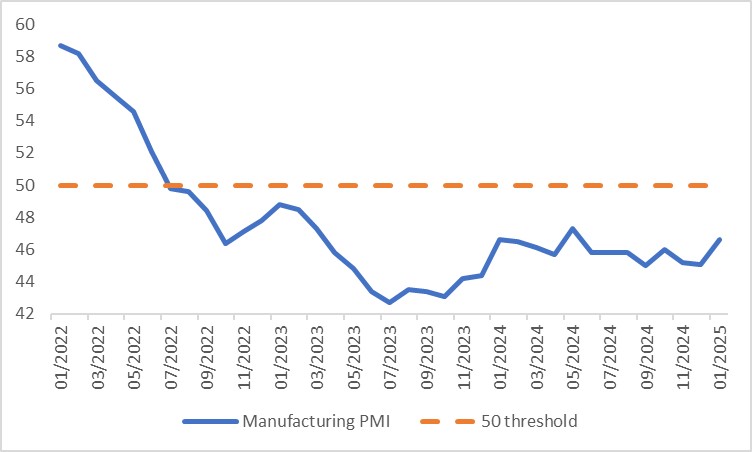

One word to describe the Eurozone's economic performance in 2024 would be "slowdown". This is mainly due to the drag from manufacturing and exports. More specifically, the manufacturing PMI has been below the 50 threshold, indicating contraction, for an extended period (Figure 1.1). From the beginning of last year until August (the latest data), the industrial production index has shown negative year-on-year growth for seven consecutive months. Additionally, goods exports in 2024 were lower than in 2023.

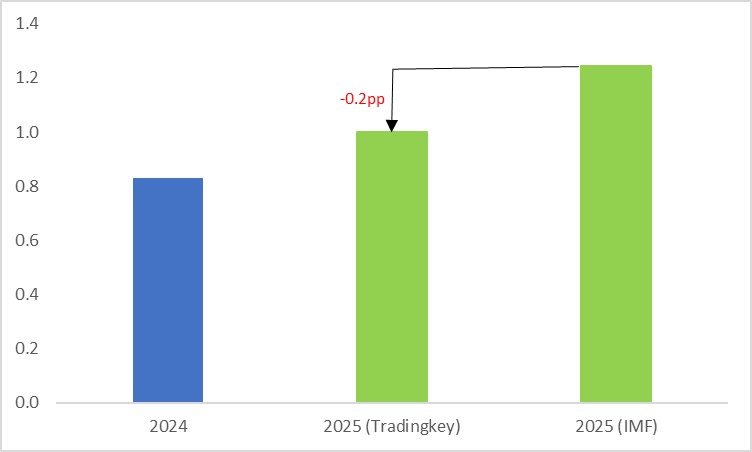

Looking ahead, the Eurozone's economy will be driven by both positive and negative factors. On the positive side, wage growth has shown resilience. With inflation decreasing at a faster rate, real wages continue to grow positively, which is expected to drive up household consumption. On the negative side, investment and manufacturing are unlikely to recover under the influence of political uncertainty. Furthermore, Trump's potential higher tariffs could deteriorate the global trade environment, adversely affecting Eurozone exports. With these opposing forces at play, the Eurozone is expected to experience a weak recovery. We forecast a GDP growth of merely 1% for 2025, below the IMF's prediction of 1.2% (Figure 1.2).

As the largest economy in the Eurozone, Germany mirrors the region's economic landscape. After experiencing economic weakness in the first half of 2024, signs of recovery began to emerge in the second half. However, the recovery is expected to be slow due to: 1) A softening labour market leading to lacklustre wage growth, which curbs consumption; 2) Ongoing political uncertainty challenging fiscal spending.

In France, while rising real wages are pushing economic recovery, political and fiscal uncertainties have started to impact economic activities. Notably, the INSEE consumer confidence index has seen several months of consecutive month-on-month declines. Therefore, similar to Germany, France is expected to undergo a weak recovery this year.

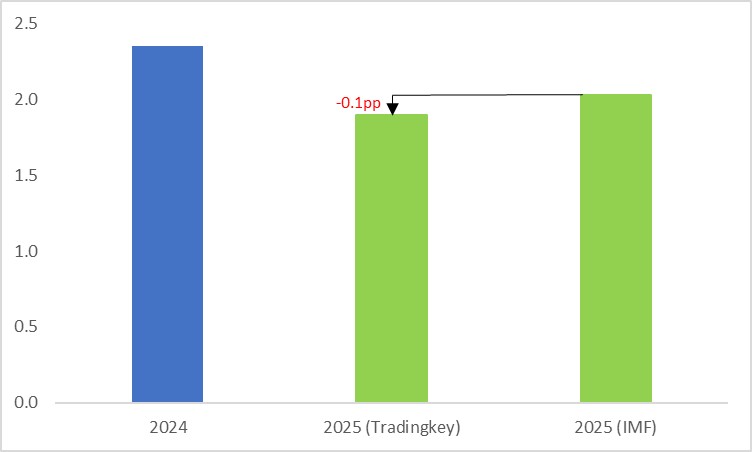

Inflation has gradually decreased from its peak at the end of 2022 due to tight financial conditions and economic weakness. We forecast that the average inflation rate in the Eurozone this year will fall to 1.9%, slightly below the IMF's prediction of 2% (Figure 1.3). The combination of weak recovery and low inflation will provide the European Central Bank (ECB) with ample room for rate cuts. We anticipate that the ECB will cut rates 4-6 times this year, each by 25 basis points.

Figure 1.1: Eurozone Manufacturing PMI

Source: Refinitiv, Tradingkey.com

Figure 1.2: 2025 GDP growth forecast, Tradingkey vs. IMF (%)

Source: IMF, Tradingkey.com

Figure 1.3: 2025 CPI growth forecast, Tradingkey vs. IMF (%)

Source: IMF, Tradingkey.com

2. Exchange Rate (EUR/USD)

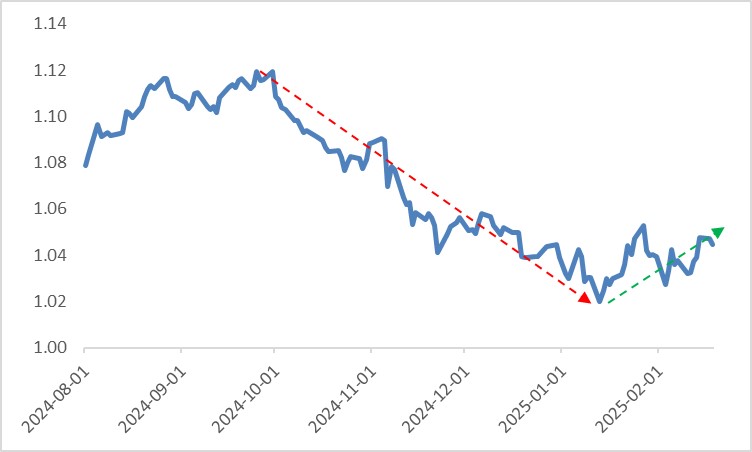

Since September 2024, the euro has significantly weakened against the dollar. The EUR/USD hit bottom in mid-January of this year and began a mild recovery, driven by both internal and external factors (Figure 2.1). Internally, there are signs of economic improvement in the Eurozone. Externally, the "Trump Trade" has cooled down as inflation fears under Trump's policies did not materialize as expected, leading to a weaker USD Index.

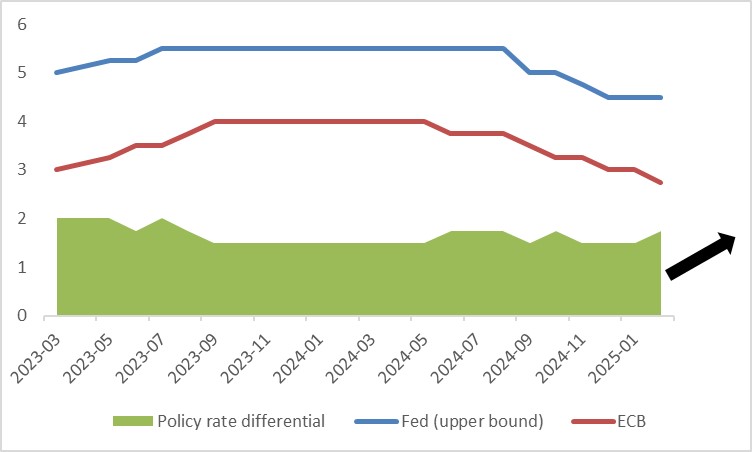

However, looking forward, in the short term (0-3 months), we believe the euro will remain under pressure for three reasons. First, despite Trump using tariffs as a negotiation weapon and his policies being often erratic, based on his first term, we expect tariffs to be a trend during this tenure, suppressing Eurozone exports and thus lowering the euro's exchange rate. Second, as mentioned earlier, the Eurozone might face a weak recovery in 2025 compared to the resilient US economy, which will push the EUR/USD down. Lastly, the ECB's more dovish stance compared to the Fed will also lead to a weaker euro due to interest rate differentials (Figure 2.2).

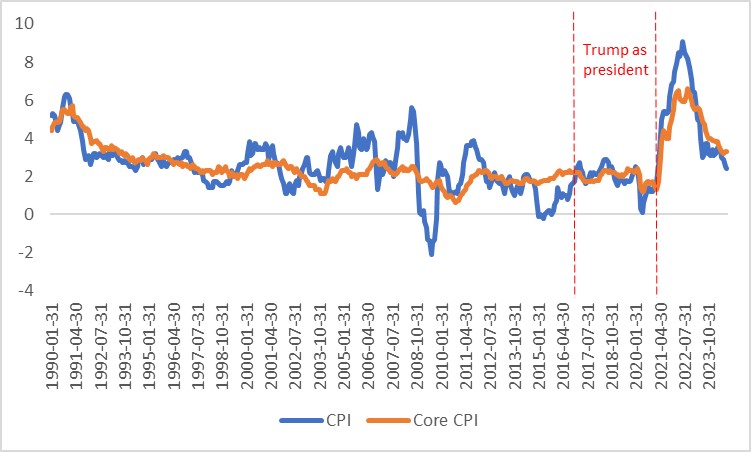

In the medium term (3-12 months), similar to Trump's first term, we think his energy policies might offset his high tariff policies, resulting in inflation lower than current expectations (Figure 2.3). The Fed might shift from hawkish to dovish, with more rate cuts than the market currently anticipates, leading to a stabilization period for the EUR/USD.

Two uncertainties to note are: 1) If the Russia-Ukraine war ends under pressure or persuasion by the Trump administration, it could boost the euro significantly. This is because the end of the Russia-Ukraine war would help lower energy prices, reduce geopolitical risks and restore confidence in the European economy, all of which would be beneficial for the euro. 2) The German election on 23 February might strengthen the euro if fiscal hawks gain a decisive majority and implement more fiscal stimulus alongside structural reforms while maintaining debt sustainability.

Figure 2.1: EUR/USD

Source: Refinitiv, Tradingkey.com

Figure 2.2: ECB vs. Fed policy rate (%)

Source: Refinitiv, Tradingkey.com

Figure 2.3: US inflation (%), CPI did not increase significantly during the Trump 1.0 period

Source: Refinitiv, Tradingkey.com

3. Bonds

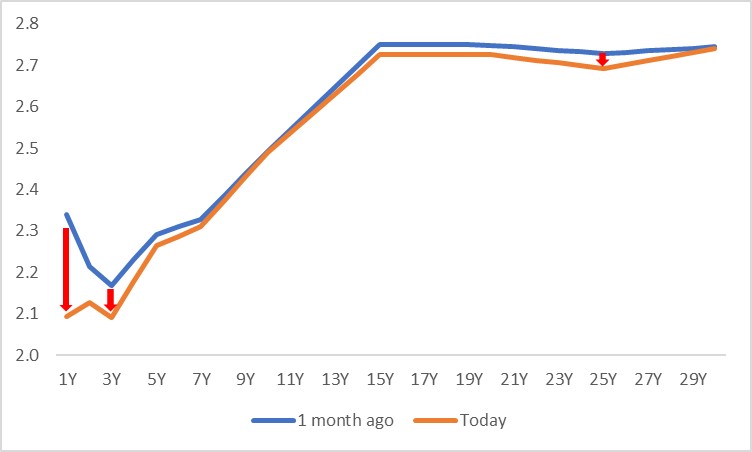

Since January, the German 10-year government bond yield has generally decreased, influenced by factors like German economic softness and declining domestic inflation, but primarily driven by the ECB's aggressive rate cuts. Looking forward, under the ECB's continued monetary easing, the German yield curve is expected to shift downwards. In terms of duration, the main driver of this downward shift will be lower policy rates, affecting short-term yields more and leading to a steeper yield curve (Figure 3.1).

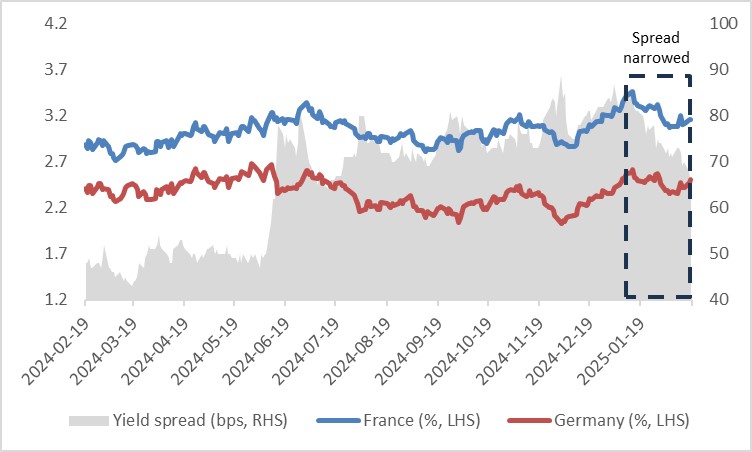

French and Spanish bond yields are expected to follow German yields downward. Since the beginning of January, the spread between French and German yields has narrowed, primarily due to a phase of political stability in France following a failed no-confidence vote (Figure 3.2). However, looking ahead, France's political risk is higher than Germany's, suggesting the spread might widen again.

German yields have traditionally shown a high correlation with the euro. While it is unclear which asset drives the other, a decline in yields might contribute to short-term euro weakness.

Figure 3.1: German government bond yield curve (%)

Source: Refinitiv, Tradingkey.com

Figure 3.2: Frech-German yield spread

Source: Refinitiv, Tradingkey.com

4. Stocks

We analyse Eurozone stock markets through valuation models. In 2024, wage growth exceeded expectations. Higher wages are a double-edged sword; they increase corporate costs but also boost consumer spending, which benefits corporate revenue. Thus, the impact on the numerator in valuation models is limited. Continued rate cuts by the ECB will be positive for the denominator. Overall, we are bullish on Eurozone stocks in the short to medium term (Figure 4).

Figure 4: Eurostoxx 50

Source: Refinitiv, Tradingkey.com

.jpg)