Exchange Rate Outlook: Time to Go Short the EUR/JPY Pair

Executive summary

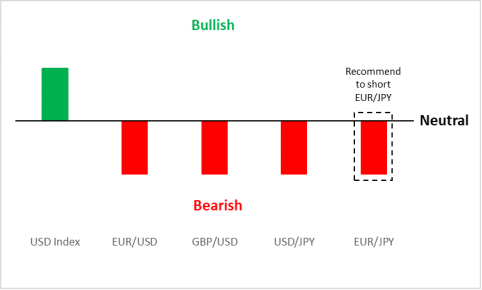

Short-term (<3 months) view

Source: Tradingkey.com

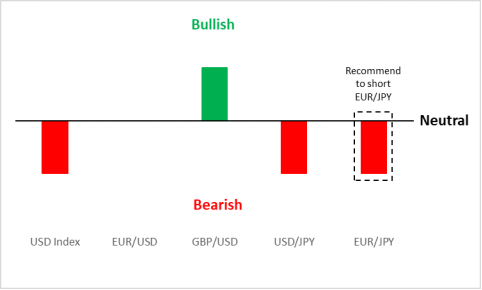

Medium-term (3-12 months) view

Source: Tradingkey.com

1. USD Index

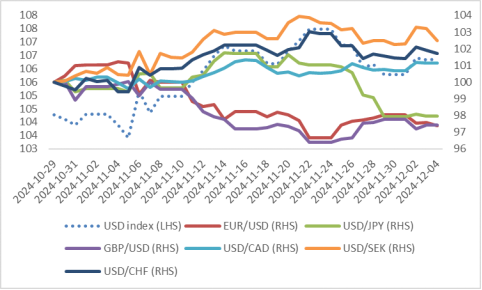

On October 29, we released a report titled The Impact of the US Election on Major Asset Classes, which identified Trump as the frontrunner in the upcoming general election in early November. Based on our baseline scenario, we adopted a bullish outlook on the USD Index. Since the report's publication, the dollar has appreciated by 2.4%. Among the index components, all currencies have depreciated except the Japanese yen (Figure 1.1).

Figure 1.1: USD Index and components

Source: Refinitiv, Tradingkey.com

Note: Component currencies are rebased on 29/10/2024 = 100

Following Trump's election, market sentiment has shifted, with investors increasingly concerned that his policies could spur re-inflation. Although the Fed is expected to cut interest rates by 25bp at the upcoming Federal Open Market Committee (FOMC) meeting in December, the trajectory of rate cuts in 2025 may be slower than previously anticipated. Meanwhile, the recent CPI rebounded slightly from 2.6% in October to 2.7% in November, further exacerbating the uncertainty of the Fed's monetary policy. Moreover, Trump's tariff policies and his criticisms of the independent currency settlement system proposed by BRICS nations have further heightened market uncertainties. The potential appointment of Scott Bessent, a known advocate of a strong dollar, as US Treasury Secretary has reinforced expectations of dollar strength. These factors combined are likely to sustain upward potential on the dollar in the short term.

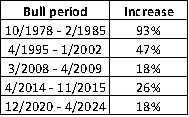

Is the Short-Term Upward Trend of the USD Index Sustainable? To address this question, it is essential to examine the historical upward cycles of the dollar. Since the collapse of the Bretton Woods system and the creation of the USD Index, the dollar has experienced five notable upward cycles (Figures 1.2 and 1.3). While some economists view the dollar's movement post-2008 as one prolonged upward cycle, for analytical clarity, we consider the rises beginning in 2008, 2014, and 2020 as independent cycles. Historical medium- and long-term cycles are as follows:

- October 1978 – February 1985: Following two oil crises, the Federal Reserve implemented tight monetary policies to combat high inflation, driving a sustained dollar rally.

- April 1995 – January 2002: The rise of the Internet era spurred robust US economic growth, attracting significant foreign capital inflows.

- March 2008 – April 2009: During the Global Financial Crisis, the dollar’s safe-haven status was underscored as investors sold risky assets and sought low-risk investments like US Treasury bonds.

- April 2014 – November 2015: Diverging monetary policies between the US and Europe defined this period. The Fed began tapering its QE program, while the ECB significantly expanded its balance sheet. The widening interest rate gap supported dollar appreciation.

- December 2020 – April 2024: In the wake of the pandemic, US inflation surged, prompting the Fed to raise its policy rates from 0.25% to 5.5%. Higher rates attracted global capital inflows, strengthening the dollar.

Historically, the dollar's medium- and long-term upward trends required at least one of the following conditions: 1) Elevated inflation levels; 2) A Fed interest rate hike cycle; 3) Diverging monetary policies in directions between the US and Europe; 4) Exceptional strength in the US economy; 5) A global economic crisis. At present, the US does not meet any of these conditions. In the medium term, as the effects of the "Trump Trade" dissipate and the influence of the rate-cut cycle grows, the USD Index is likely to shift into a downward trend. In short, while the dollar’s short-term strength may persist, historical patterns suggest that without structural tailwinds, it is unlikely to be sustainable in the medium to long term.

Figure 1.2: US dollar upward cycles

Source: Refinitiv, Tradingkey.com

Figure 1.3: Increase in the USD index during upward cycles

Source: Refinitiv, Tradingkey.com

2. EUR/USD

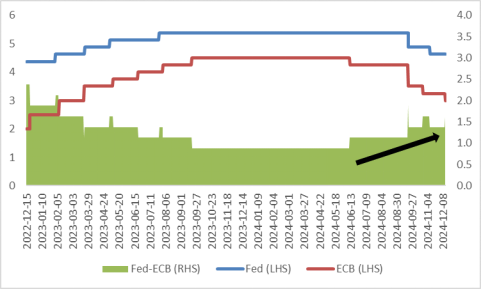

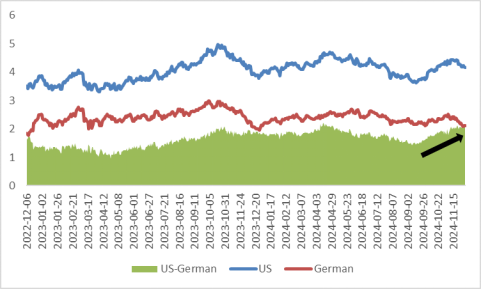

After the US election, the euro has underperformed against other major currencies. Looking ahead, we expect the EUR/USD to continue declining in the short term, influenced by a combination of internal and external factors. On the internal front, monetary policy divergence plays a significant role. The eurozone remains focused on addressing weak economic growth, while the US is more concerned with managing re-inflation pressures. Consequently, following the European Central Bank’s (ECB) further interest rate cut of 25bp on 12 December, we expect the central bank to continue adopting a more aggressive interest rate cut strategy than the Fed, which may further widen the interest rate differential between the US and Europe (see Figures 2.1 and 2.2). Additionally, fiscal policy uncertainties in the eurozone—such as the collapse of Germany's ruling coalition and the risk of a "shutdown" in the French government—may constrain fiscal spending. In contrast to the US, these tighter fiscal conditions may dampen the eurozone's economic recovery momentum. This combination of monetary and fiscal policies suggests that the euro is likely to face continued pressure against the dollar in the short term.

On the external front, the largest challenge may stem from Trump’s tariff policies. Beyond the direct impact of potential tariff hikes on European exports to the US, increased US tariffs on China could also indirectly affect the European economy. As China redirects its lost export activity to other markets, European manufacturers may encounter heightened competition. Furthermore, even though the specifics and scale of US tariff measures remain uncertain, this uncertainty has already weighed on European economic activity, exerting additional downward pressure on the euro.

Figure 2.1: Fed vs. ECB policy rates (%)

Source: Refinitiv, Tradingkey.com

Figure 2.2: US vs. German 10Y government bond yields (%)

Source: Refinitiv, Tradingkey.com

A well-known adage suggests, “A fortress is most vulnerable to threats from inside.” In the medium to long term, the euro’s primary challenge lies not in external factors but in internal structural imbalances within the eurozone. These imbalances, rooted in economic disparities among member states, are a significant factor contributing to the euro’s medium- and long-term vulnerabilities. Since the eurozone’s inception, member states have broadly divided into two distinct economic groups. The first group, led by Germany, consists of industrial and export-driven economies. These countries maintain trade surpluses, as their domestic production outpaces consumption. The second group includes economies such as Spain, Portugal, and Greece, which rely more heavily on imports, leading to persistent trade deficits. These deficits are typically financed through increased government borrowing, contributing to elevated debt levels and economic strain.

Three key factors underpin these structural imbalances.

- ECB monetary policy framework: The ECB, as the institutional successor to the Deutsche Bundesbank, has historically favoured monetary policies aligned with the German economic model. The long-term average inflation rate in Germany is relatively lower than other euro countries, resulting in the long-term policy interest rates being lower than they should be. While this benefits surplus economies like Germany, it inadvertently exacerbates imbalances by providing overly accommodative financing conditions for deficit economies, encouraging unsustainable debt accumulation.

- Debt accumulation in peripheral economies: The lower borrowing costs stemming from the ECB’s policies have led to increased sovereign debt levels in deficit economies. The European sovereign debt crisis (2010–2015) starkly highlighted the vulnerabilities of these economies under the existing monetary framework, where low-cost financing masked underlying structural weaknesses.

- Global manufacturing shifts: The rise of manufacturing powerhouses in emerging markets, particularly China, has fundamentally reshaped global trade dynamics. China’s dominance in manufacturing and its export-driven growth strategy have heightened competition, consolidating Europe’s manufacturing activities within Germany and a few other advanced economies. This has further weakened industrial capacities in southern European countries, deepening regional disparities within the eurozone.

Looking forward, without substantial political and structural reforms to address these imbalances, the eurozone is unlikely to obtain a medium- and long-term appreciation of the euro. While the EUR/USD may remain stable in the medium term due to anticipated dollar weakness, the euro is projected to depreciate against other major currencies.

3. GBP/USD

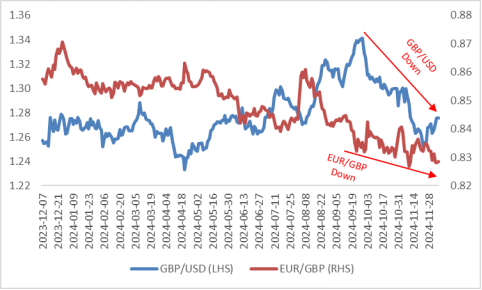

Since October, the British pound has maintained a balanced position between the dollar and the euro, weakening against the dollar while strengthening against the euro (Figure 3.1). As outlined earlier, our short-term outlook anticipates continued dollar strength alongside euro weakness. As current trends are expected to persist, the pound is likely to continue depreciating against the dollar and appreciating against the euro over the next few months.

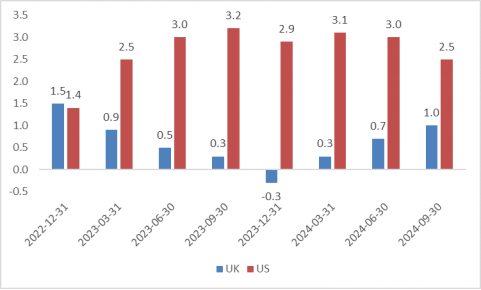

- Against the dollar: On the growth front, the UK economy has shown less resilience compared to the US (Figure 3.2). On the fiscal front, the UK government lacks a tax-cut policy plan comparable to the Trump administration's measures. Both could exert slight downward pressure on the GBP/USD.

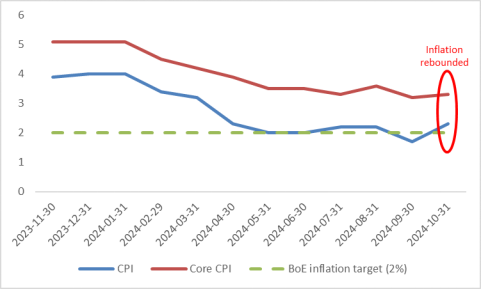

- Against the euro: The UK has been less exposed to political risks, economic stagnation, and the threat of US tariffs compared to the eurozone. Moreover, while the UK economic surprise index has fallen to a low, unexpected development—such as a rebound in average wage growth in Q3 as well as higher-than-expected CPI and core CPI in October—may prompt the Bank of England (BoE) to adopt a more hawkish stance (Figure 3.3). This could support the pound, leading to a slight decline in the EUR/GBP.

Figure 3.1: GBP/USD vs. EUR/GBP

Source: Refinitiv, Tradingkey.com

Figure 3.2: UK vs US GDP growth (y-o-y, %)

Source: Refinitiv, Tradingkey.com

Figure 3.3: UK CPI and core CPI (%)

Source: Refinitiv, Tradingkey.com

4. USD/JPY

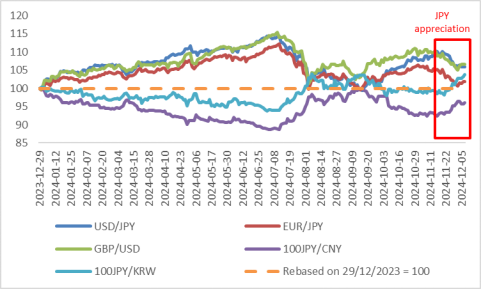

Since mid-November, the Japanese yen has appreciated against all major global currencies (Figure 4.1). The apparent driver appears to be the external fiscal policy signals from key US officials, including US Treasury candidate Bessent and Commerce Secretary Lutnick, who have expressed support for cutting federal spending. This stance indicates a potential limitation on fiscal expansion, which has led to a sharp decline in the spread between US and Japanese government bond yields, resulting in a depreciation of the USD/JPY.

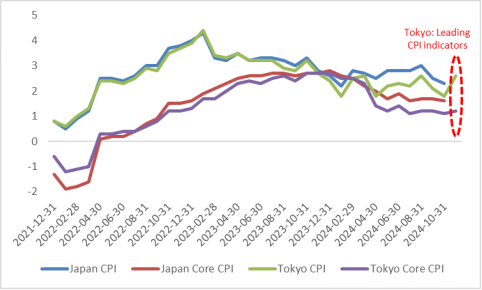

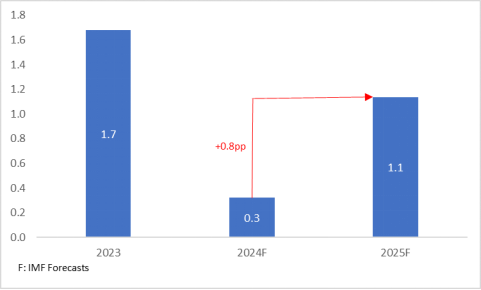

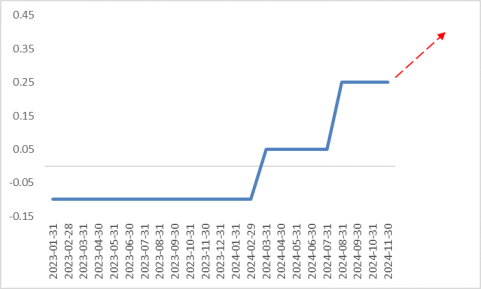

However, we believe the yen's recent appreciation is primarily driven by internal factors rather than external ones. Inflation dynamics indicate a mixed but strengthening trend. While October's CPI and core CPI showed signs of moderation, leading inflation indicators, such as Tokyo's CPI, surged from 1.8% in October to 2.6% in November (Figure 4.2). Basic wage growth in October was 2.6% year-on-year, the highest level since November 1992. Furthermore, at the end of November, Prime Minister Ishiba Shigeru and the Japan Small and Medium-sized Manufacturing Union advocated for substantial wage increases during the 2025 Shuntō, which could further fuel inflationary pressures. Economic growth also presents a positive backdrop. According to IMF projections, Japan's real GDP growth is expected to accelerate by 0.8 percentage points, reaching 1.1% in 2025, driven by a recovery in private consumption and increased corporate investment (Figure 4.3). Given the combination of rising inflation and stronger growth prospects, we anticipate the Bank of Japan (BoJ) will raise interest rates once in December this year and twice in the coming year, further supporting the yen (Figure 4.4).

Looking ahead, in the short term, these factors are likely to continue driving the yen's exchange rate higher. Even in the medium term, the Bank of Japan's (BoJ) monetary policy stance, which contrasts significantly with that of other major central banks, reinforces our bullish outlook on the yen. As highlighted earlier, we remain bearish on the euro in both the short and medium term. Consequently, we strongly recommend taking a short position in the EUR/JPY pair to capitalize on this divergence.

Figure 4.1: JPY exchange rates

Source: Refinitiv, Tradingkey.com

Figure 4.2: Japan and Tokyo inflation (%)

Source: Refinitiv, Tradingkey.com

Figure 4.3: IMF forecast for Japan's real GDP (%)

Source: Refinitiv, Tradingkey.com

Figure 4.4: BoJ policy rate (%)

Source: Refinitiv, Tradingkey.com