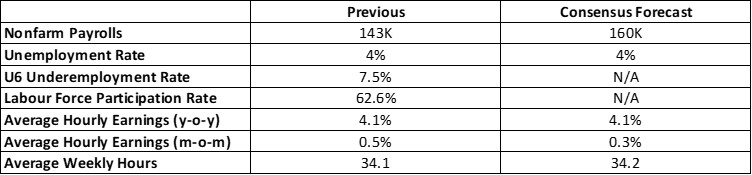

U.S. February Nonfarm Payroll Preview: The Turning Point in the Labour Market Has Arrived

On 7 March 2025, the United States will release its February Nonfarm Payroll (NFP) data. The market consensus currently anticipates a payroll increase of 160,000 jobs. However, we believe the actual figure will fall short of this expectation and also undershoot the prior month’s reading of 143,000 (Figure 1).

Figure 1: U.S. labour market forecasts

Source: Refinitiv, Tradingkey.com

Breaking it down by sector, government employment is expected to experience a sharper slowdown in February compared to private-sector job growth. This is largely due to the federal hiring freeze that began in January as well as the layoffs of federal workers starting in March, which likely suppressed hiring activity in February.

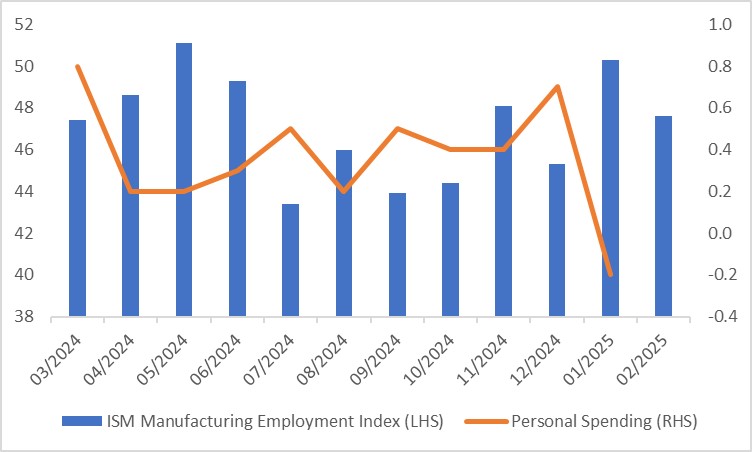

While private-sector employment has not been directly impacted to the same extent as the government sector, its slowdown is still notable, though less severe. Recent high-frequency data consistently point to weakening private-sector job growth. For instance, the ISM Manufacturing Employment Index dropped from 50.3 in January to 47.6 in February, signalling softness in the private-sector labour market. Additionally, Personal Spending has shifted from positive to negative territory, reflecting growing consumer concerns about the economic outlook (Figure 2).

Figure 2: U.S. Manufacturing employment index and personal spending

Source: Refinitiv, Tradingkey.com

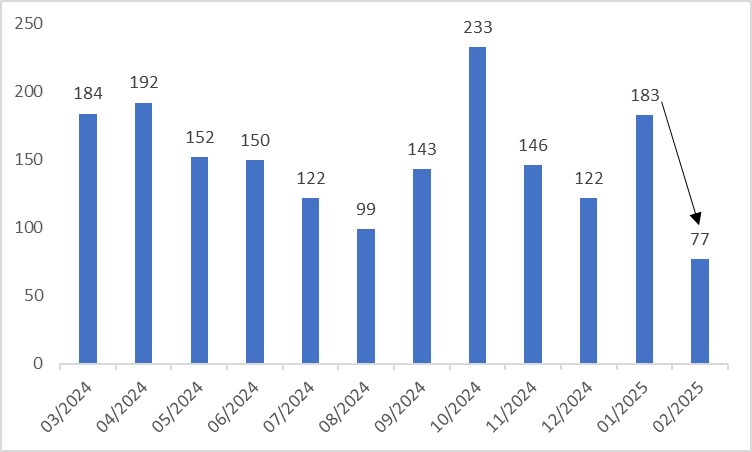

As a leading indicator for NFP, the ADP Employment Report showed a steep decline, falling from 183,000 jobs in January to just 77,000 in February—also well below the market’s expectation of 140,000 (Figure 3). Although ADP and NFP data differ in source and scope, such a significant drop in ADP figures is undeniably a bearish signal. Compounding this, the Atlanta Fed recently revised its GDPNow estimate for Q1 2025 real GDP growth downward from 3.9% to -2.8%, underscoring worsening expectations for the U.S. economy, domestic demand, and labour market strength.

Figure 3: U.S. ADP Employment Change (000)

Source: Refinitiv, Tradingkey.com

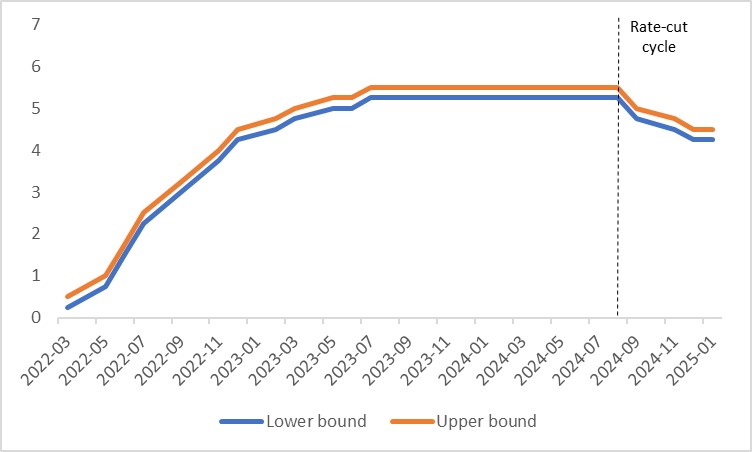

Given the anticipated ongoing weakness in the labour market, we project that the Federal Reserve may implement 4–5 additional rate cuts before the end of this year—exceeding the market’s current consensus of 3 cuts (Figure 4).

Figure 4: Fed policy rate (%)

Source: Refinitiv, Tradingkey.com

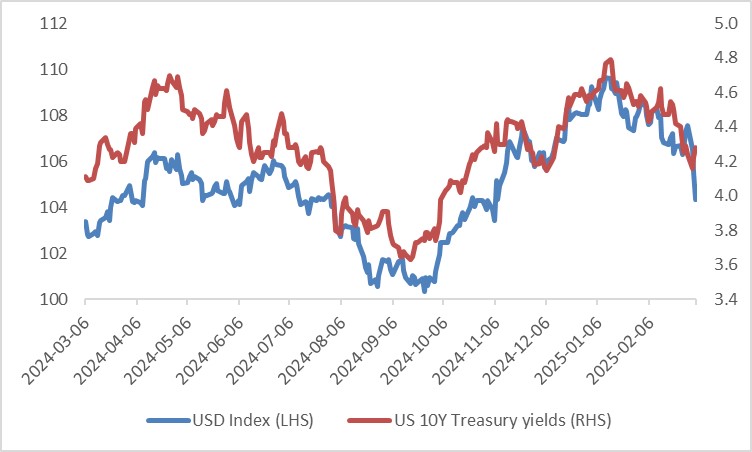

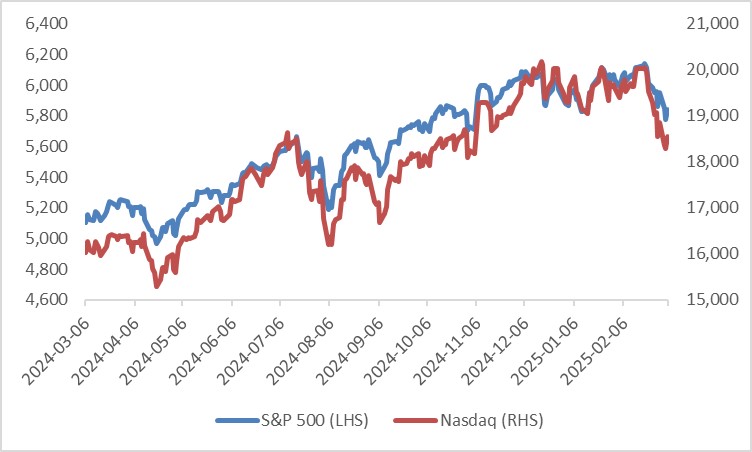

Should our forecast for February’s NFP data prove accurate, we expect the post-release market reaction to include a decline in the USD Index, Treasury yields, and U.S. equities (Figures 5 and 6).

Figure 5: USD Index and US 10-year Treasury yields

Source: Refinitiv, Tradingkey.com

Figure 6: U.S. Stocks

Source: Refinitiv, Tradingkey.com