US January PCE Preview: If the pace of Core PCE growth slows, could it trigger the Fed to resume interest rate cuts?

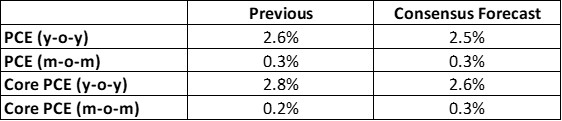

On 28 February 2025, the US will release the Personal Consumption Expenditures (PCE) data for January. Market consensus forecasts suggest that the year-over-year growth rates for Headline PCE and Core PCE will reach 2.5% and 2.6%, respectively, both lower than December 2024 figures of 2.6% and 2.8% (Figure 1). However, we anticipate that Core PCE will rise by 2.7%, positioning it between the prior month’s value and the market’s consensus estimate.

Figure 1: Headline and Core PCE consensus forecast (%)

Source: Refinitiv, Tradingkey.com

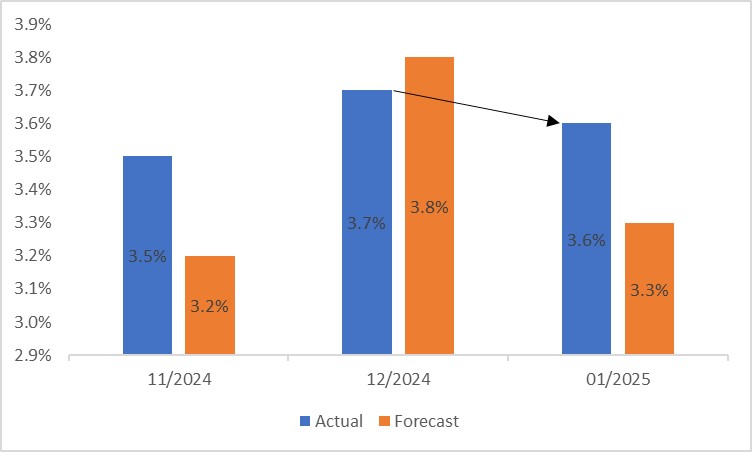

To forecast PCE effectively, we can analyse two key indicators: the Producer Price Index (PPI) and the Consumer Price Index (CPI). The PPI reflects price changes at the producer level, which are often passed on to consumers, thereby influencing PCE. January’s Core PPI recorded a year-over-year increase of 3.6%, a slowdown from December 2024, driven primarily by weakness in subcategories such as healthcare and financial services (Figure 2). If this decline in PPI translates promptly to PCE, it suggests that January’s Core PCE is unlikely to exceed its prior value.

Figure 2: Core PPI (%)

Source: Refinitiv, Tradingkey.com

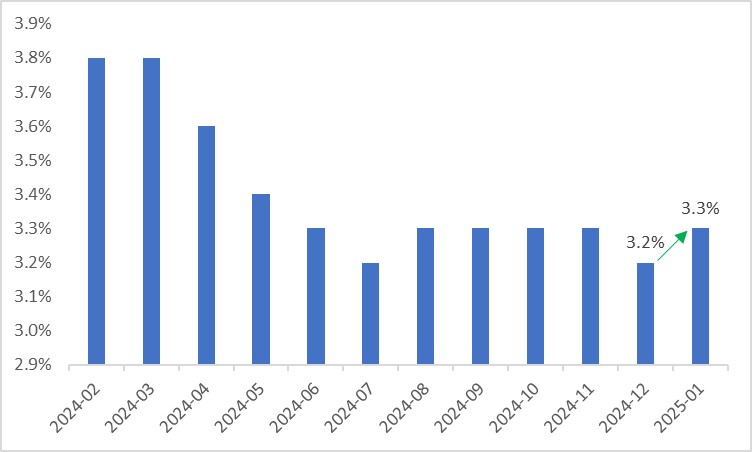

Although CPI and PCE differ in their statistical methodologies, historically, they have exhibited a strong positive correlation. January’s Core CPI rose to 3.3%, surpassing both expectations and the prior month’s readings of 3.1% and 3.2% (Figure 3). This uptick in CPI suggests that Core PCE is unlikely to drop significantly below its previous level.

Figure 3: Core CPI (%)

Source: Refinitiv, Tradingkey.com

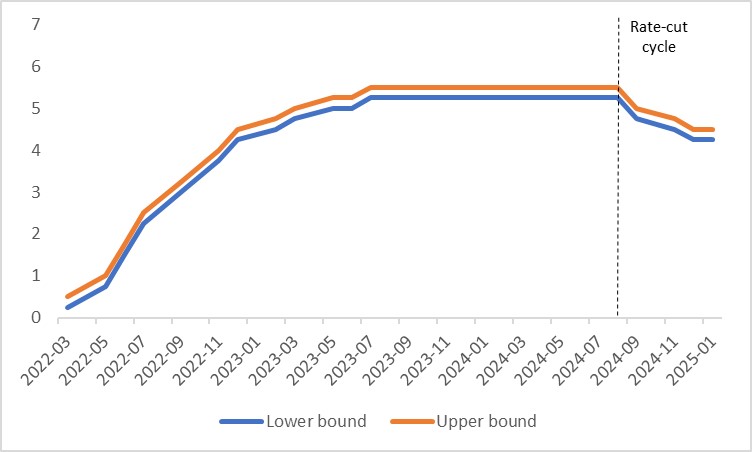

Balancing these factors, we project that January’s Core PCE will experience a slight decline from December 2024’s 2.8%, settling at 2.7%. Core PCE is one of the most critical indicators for the Fed’s monetary policy decisions. Looking ahead, if it continues to decline, this could prompt the Fed to resume interest rate cuts (Figure 4).

Figure 4: Fed policy rate (%)

Source: Refinitiv, Tradingkey.com