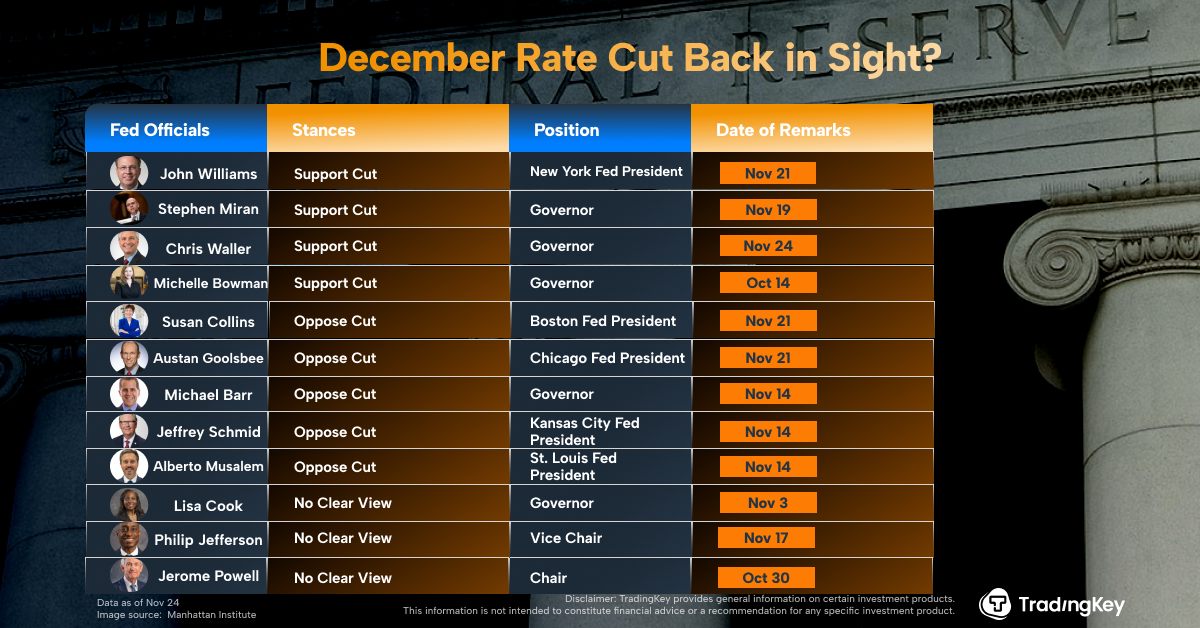

Fed Interest Rate Decision Commentary: Rate Cuts Imminent, Shifting to an “Easing Trade”

TradingKey - On 20 March 2025, the Federal Reserve announced its March interest rate decision. Consistent with broad market expectations, the Fed maintained its policy rate unchanged at 4.25%-4.5%. Regarding balance sheet reduction, starting in April, the monthly cap on maturing U.S. Treasury securities not reinvested will decrease from $25 billion to $5 billion, signalling a slower pace of shrinking its balance sheet.

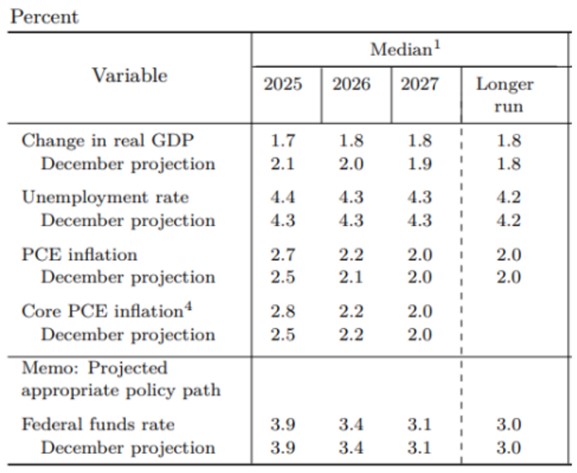

Compared to December last year, the Fed downgraded its U.S. economic growth outlook while raising its inflation forecasts (Figure 1):

· The March projection lowered 2025 real GDP growth by 0.4 percentage points to 1.7%;

· The unemployment rate was slightly adjusted upward by 0.1 percentage points to 4.4%;

· Headline PCE and Core PCE inflation forecasts were revised up from 2.5% in December to 2.7% and 2.8%, respectively.

Figure 1: Fed forecasts

Source: Fed, Tradingkey.com

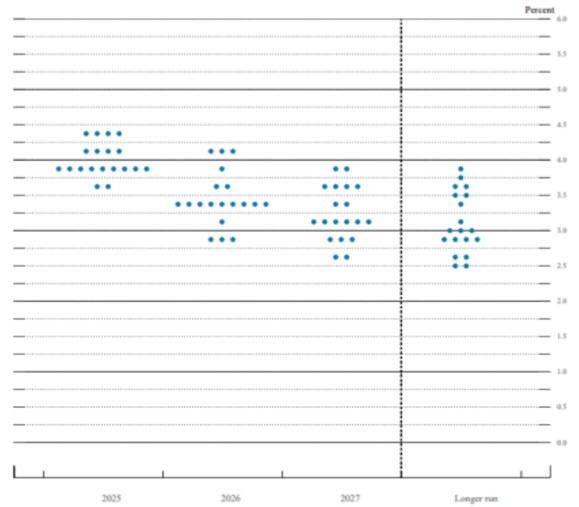

Given the softening economic outlook and rising inflation, the Fed’s resumption of a rate-cutting cycle is now a certainty. The dot plot indicates two rate cuts by year-end, bringing the policy rate to 3.75%-4% (Figure 2).

Figure 2: Fed dot plot

Source: Fed, Tradingkey.com

During the meeting, Chair Powell emphasized that the U.S. economy remains resilient and inflation expectations are still anchored, suggesting the Fed does not need to trigger a recession to tame inflation, as it did in the 1970s. This statement partially alleviated investor concerns about stagflation.

We align with Powell’s view that stagflation is unlikely. On the growth front, while consumer confidence and spending willingness have weakened, both manufacturing and services PMIs remain above the 50 expansion threshold. Looking ahead, Trump’s domestic tax cuts are expected to bolster economic activity. These factors suggest that while the U.S. economy is slowing, a technical recession is improbable. On inflation, although Trump’s tariff measures are pushing up U.S. CPI, his potential energy policies could offset some of the tariff-driven inflationary pressure, keeping medium- to long-term inflation below current expectations.

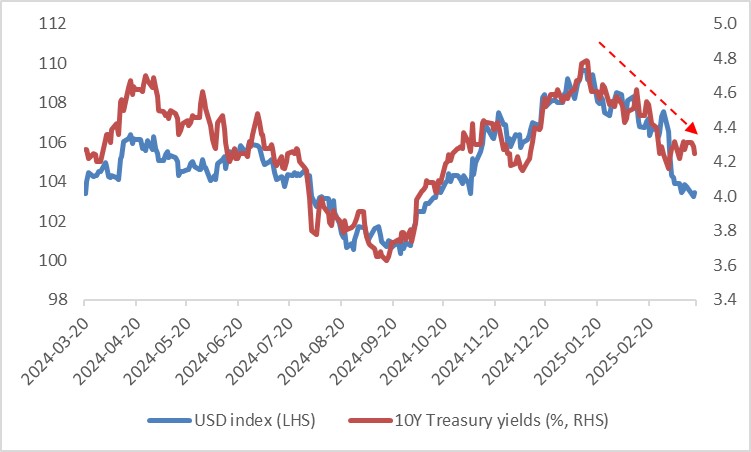

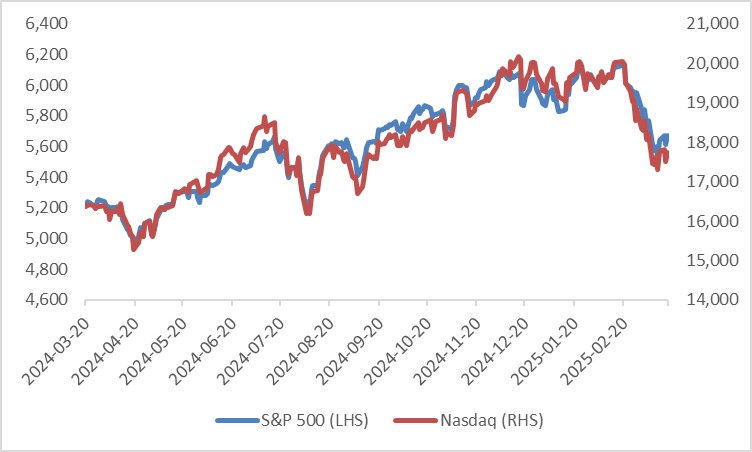

With inflation unlikely to surge significantly, we believe the Fed has both the willingness and capacity to implement more substantial rate cuts. We project 3-4 rate cuts by year-end, exceeding the two cuts indicated in the March dot plot. For investors, this points to a shift toward an “easing trade”—a weaker dollar index, declining Treasury yields and rising U.S. equities (Figures 3 and 4).

Figure 3: USD index and U.S. Treasury yields

Source: Refinitiv, Tradingkey.com

Figure 4: U.S. stocks

Source: Refinitiv, Tradingkey.com