ECB March Policy Rate Commentary: Reshaping Expectations for Rate Cuts

On 6 March 2025, the European Central Bank (ECB) announced its policy rate decision. In line with widespread market expectations, the ECB lowered rates by 25 basis points, reducing the deposit facility rate, main refinancing operations rate and marginal lending facility rate to 2.5%, 2.65% and 2.9%, respectively (Figure 1). Additionally, the ECB has ceased reinvesting the principal from maturing assets under the APP and PEPP portfolios, marking the end of quantitative easing (QE) in the Eurozone.

Figure 1: ECB policy rate

Source: Refinitiv, Tradingkey.com

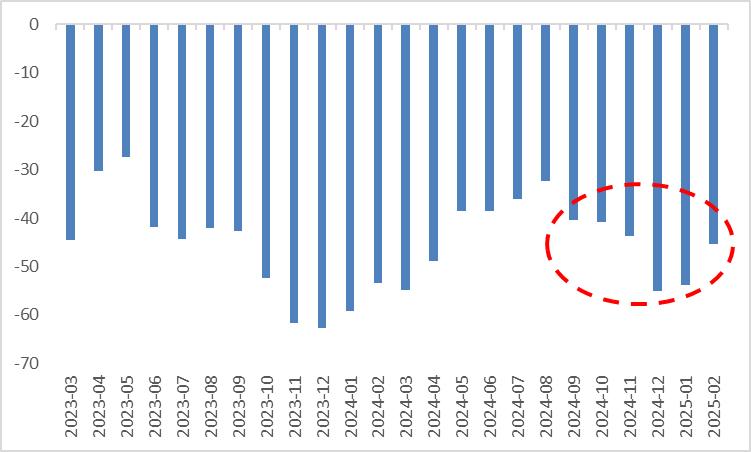

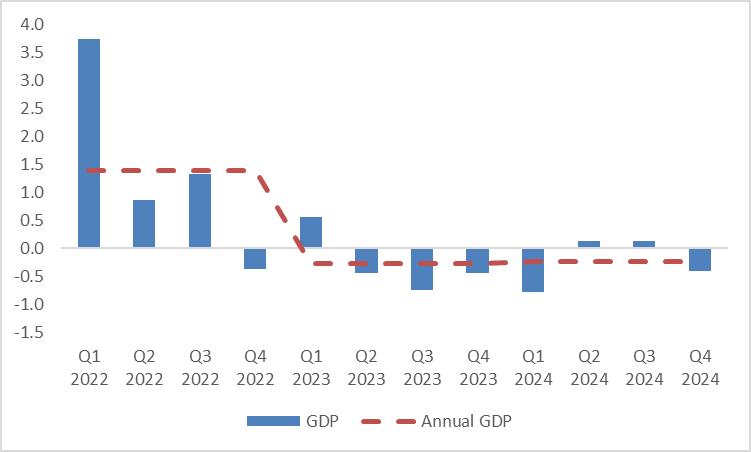

This rate cut is primarily driven by the dual pressures of economic growth and inflation. On the growth front, since the fourth quarter of last year, the Eurozone ZEW Economic Sentiment Index has remained at low levels (Figure 2). Although the services PMI continues to hover above the 50 expansion-contraction threshold, it has been declining for several consecutive months. Germany, the Eurozone’s largest economy, has been plagued by persistent weakness in manufacturing and exports, resulting in two consecutive years of negative economic growth (Figure 3). These indicators collectively suggest that the Eurozone’s economic recovery remains sluggish.

Figure 2: Eurozone ZEW Economic Sentiment Index

Source: Refinitiv, Tradingkey.com

Figure 3: German real GDP growth (%)

Source: Refinitiv, Tradingkey.com

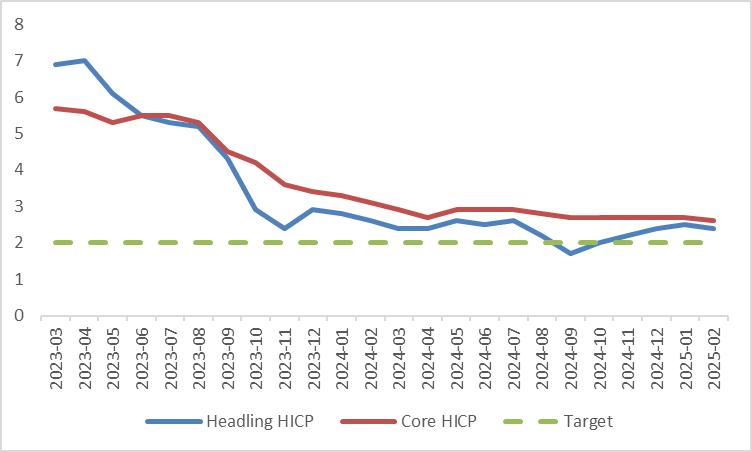

Regarding inflation, while the Harmonized Index of Consumer Prices (HICP) still exceeds the ECB’s 2% target, its downward trajectory remains intact (Figure 4). Against a backdrop of persistent economic weakness and declining inflation, the ECB’s decision to cut rates by 25 basis points in March appears reasonable.

Figure 4: Eurozone inflation (%)

Source: Refinitiv, Tradingkey.com

Notably, due to heightened uncertainty surrounding Trump’s tariff policies and the risk of renewed energy price surges, the ECB revised its forecasts for this year, lowering real GDP growth from 1.4% to 1.2% while raising inflation from 2.1% to 2.3%. This reflects the central bank’s dilemma in determining the future path of rate cuts. We believe that the ECB’s rate-cutting momentum over the next few quarters will likely be weaker than currently anticipated.

Compared to monetary policy, fiscal policy in the Eurozone deserves greater attention. The abrupt shift in Trump’s stance on the Russia-Ukraine conflict has accelerated the formulation and implementation of a “rearming Europe” plan. Increased defence spending is expected to bolster European economic growth. Furthermore, Germany’s “whatever it takes” fiscal stimulus plan, aimed at overcoming economic challenges, is likely to benefit both its domestic economy and the broader regional outlook.

Taking into account the interplay of monetary and fiscal policies as well as the economic and inflation outlook, we project that the decline in the EUR/USD and the yields of German, French and Spanish government bonds will be moderated. Nevertheless, the overall downward trend is expected to persist.