The Ultimate 2025 Investment Guide: 15 Stocks to Buy for Investors in the New Year

Introduction

For investors, 2024 has been an eventful year. It started out with worries over the direction of interest rates from the Federal Reserve (Fed) given ongoing fears over an impending recession in the US. As it turned out, the recession that was supposed to be a “near certainty” never materialised.

Instead, growth in the jobs market continued to be robust, the US economy hummed along and inflation continued to fall. That was a perfect recipe for the Fed – who only cut rates for the first time in September – and particularly investors, who have seen the benchmark S&P 500 Index hit multiple highs this year.

So far in 2024 (as of late November), the index is up 25.9% and on course for a strong year. What has that been driven by? While the economic backdrop described above has certainly helped, the first three quarters of the year came down to two words (or letters): Artificial Intelligence (AI).

The continued meteoric rise of Nvidia Corporation (NASDAQ: NVDA) and other AI-related Big Tech giants drove market returns and gave rise to the term the “Magnificent Seven” given how much these tech companies contributed to the overall market’s gains. Of course, the election of Donald Trump to a second term as President of the US has seen the market gain further on optimism surrounding deregulation and potential new opportunities for growth.

In this environment of geopolitical uncertainty but rapid innovation in the US economy, where do the opportunities lie for investors?

Our list and methodology

Luckily for investors, we’ve compiled a diverse list of 15 best stocks they should be looking to buy heading into 2025.

At the fundamental level, they’re all quality businesses with leading positions in their respective niche. From hot growth stocks that are leading the way in AI to dividend growers that can provide reliable income in any economic environment, this list offers something for everyone.

While all stocks on this list have long-term potential for investors, there are also others that offer more short-term upside given the idiosyncratic dynamics – both at the macroeconomic level but also at the company level. Regardless, investors can use this list as a foundation for building a more diversified and resilient portfolio while also trying to take advantage of short-term movements in markets over the next 12-18 months.

1. Nvidia (NASDAQ: NVDA)

Nvidia Corporation (NASDAQ: NVDA) has been the stock market story of 2024 given its utter dominance of the crucial semiconductors required to power the Artificial Intelligence (AI) revolution. Nvidia’s Graphics Processing Unit (GPU) chips, originally used for advanced gaming, have turned out to be adept at running complex AI algorithms.

With 80% market share of the cutting-edge, powerful, and efficient chips required to run AI, Nvidia is in an enviable position at the forefront of advancements in AI. Its latest Q3 FY2025 results highlight just how dominant the company is in the space, with revenue of US$35.1 billion which was an astounding 94% year-on-year rise.

Its AI-focused data centre division is the crown jewel of the company and it accounted for US$30.8 billion of the company’s overall revenue in its most recent quarter. In the same quarter in 2021, Nvidia’s data centre revenue was just US$2.9 billion.

Clearly, investor expectations are high but its next-gen Blackwell chip, which is in high demand, is set to continue driving growth for the company in the quarters ahead. With a stock price that has nearly more than tripled just in 2024 alone, the “law of large numbers” could start to take hold as its revenue growth rate slows.

Despite that, its grip on the AI chips space means it’s sure to continue to be one of the hottest growth stocks to invest in in 2025.

2. BlackRock (NYSE: BLK)

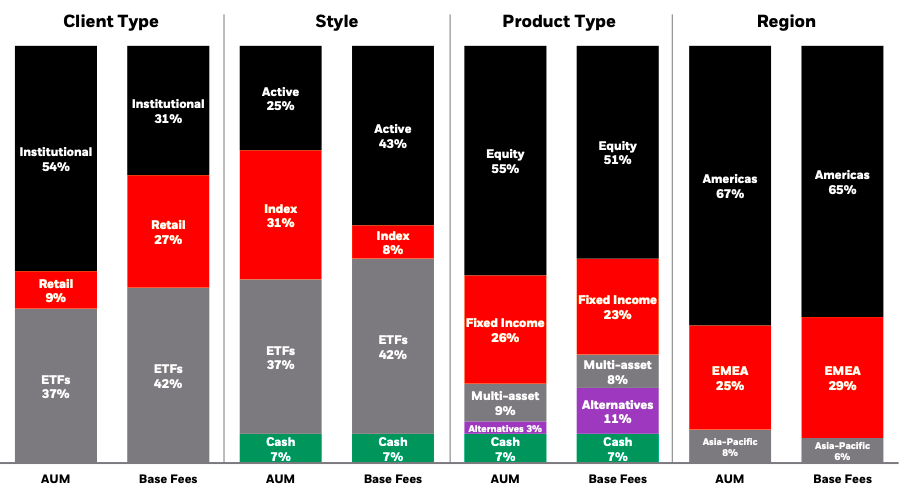

BlackRock Inc (NYSE: BLK) is one of the world’s largest asset managers and has a whopping US$11.5 trillion in assets under management (AUM). Founded in 1988, BlackRock is a relatively young newcomer to the financial services arena but its savvy deal-making has allowed it to prosper and grow into a true investment behemoth.

One of its key acquisitions was a US$13.5 billion purchase of Barclays Global Investors (BGI) in 2009 and, with it, BGI’s iShares unit. Of course, iShares is now one of the world’s leading providers of exchange-traded funds (ETFs) and a giant in its own right.

During its latest quarter, BlackRock reported revenue of US$5.2 billion, up 15% year-on-year. Of course, like any investment manager, BlackRock makes recurring income by taking a small percentage of fees based off its total AUM. Therefore, the more money it manages, the more potential it has to make profits. At that earnings call, BlackRock’s Chairman and CEO, Larry Fink, said that he “expects momentum to further build to year’s end and into 2025”.

BlackRock: Diversified across clients, styles, products and regions

Source: BlackRock’s Q3 2024 earnings presentation

BlackRock recently closed on a landmark US$12.5 billion deal for Global Infrastructure Partners which has added another US$116 billion to its AUM and will make it a larger player in the private markets space. It also was one of the first asset managers that looked into launching a Bitcoin ETF, which it has successfully done when the iShares Bitcoin Trust ETF (NASDAQ: IBIT) listed on the NASDAQ in January of this year.

With the investment giant looking to acquire smaller firms in niche areas of private markets (like private credit), its steady growth seems sure to continue over the longer term.

3. Home Depot (NYSE: HD)

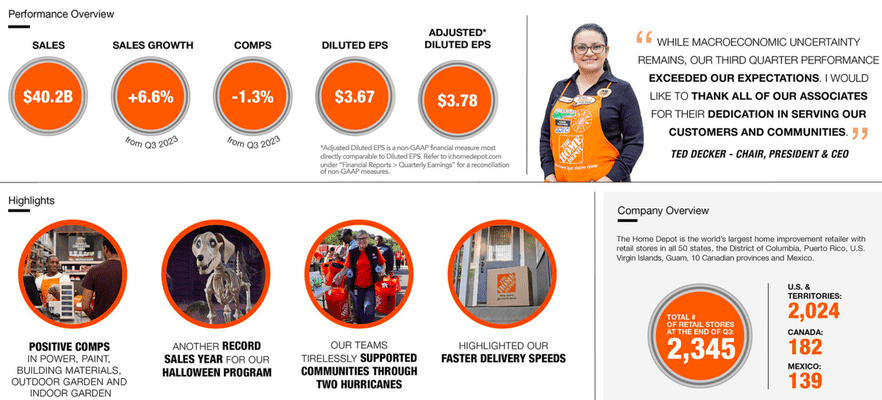

Home Depot Inc (NYSE: HD) is one of the world’s largest home improvement retailers with over 2,300 big box-style stores across North America. As the “go-to” hardware store for professional contractors and home improvement specialists, it was founded in 1979 in Atlanta, Georgia.

Its business has been able to grow consistently over the past four-and-a-half decades as it has become efficient at allocating capital via share buybacks and by growing its dividend. In fact, over the past 10 years, Home Depot has been able to increase its dividend per share (DPS) at a compound annual growth rate (CAGR) of an impressive 17%.

However, its last dividend hike slowed to just over 7% as high mortgage rates in the US – due to higher interest rates – are weighing on its business model of relying on home remodels and people moving homes. As a result, Home Depot’s sales rose 6.6% year-on-year to US$40.2 billion in its latest quarter but comparable sales fell 1.3% year-on-year.

Home Depot’s Q3 2024: Steady performance with pockets of growth

Source: Home Depot Q3 2024 investor presentation

The company did raise its full-year guidance on that earnings release, which provided investors with some optimism that perhaps we are seeing the bottoming out of home demand, with interest rates set to continue to come down.

Overall, nearly half of the housing stock in the US is over 40 years old, meaning the long-term tailwinds continue to be there for retailers like Home Depot. As an underappreciated growth stock of sorts, when mortgage rates do eventually start to come down faster – and people start moving homes again – then Home Depot’s share price could take off.

4. Constellation Energy (NASDAQ: CEG)

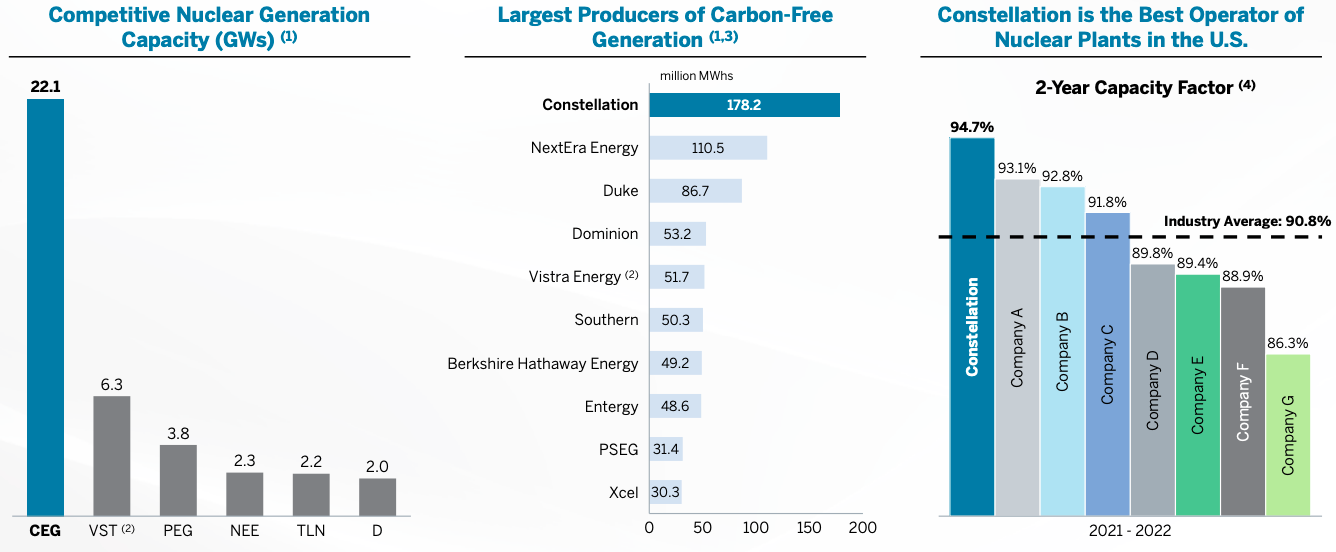

Constellation Energy Corp (NASDAQ: CEG) is the leading nuclear energy provider in the US and is actually the country’s largest carbon-free energy producer. It has around 32 gigawatts (GW) of generation capacity, with just over 22 GW of it being pure nuclear.

Constellation Energy: Nuclear powerhouse operator in the US

Source: Constellation Energy investor presentation, September 2024

As a leading generator of clean power in the US, Constellation Energy is also striking up partnerships with large users of power. Inevitably, it’s also being used to power the insatiable energy demands of Artificial Intelligence and the Large Language Models (LLMs) that are being built off the back of AI.

In late 2023, Constellation struck a 20-year power purchase agreement (PPA) with tech giant Microsoft Corporation (NASDAQ: MSFT) to supply it with clean power. Part of this agreement saw Constellation restart operations at its Three Mile Island unit, with Microsoft set to buy all the electricity generated from the plant.

The company is also benefitting from the nuclear production tax credit (PTC) which will be in effect through to the end of 2032. With both sides of the political aisle in the US seeing the merits of nuclear power, Constellation Energy is set to continue powering ahead and will be one of the hottest AI “power-related” growth stocks to watch out for in 2025.

One concern for investors right now could be its year-to-date price rise in 2024, with Constellation shares up over 115%, but if power demand for AI continues apace and the shift to nuclear is ongoing then Constellation will be certainly one of the biggest beneficiaries over the long term.

5. Shopify (NYSE: SHOP)

Shopify Inc (NYSE: SHOP) is the company that powers the world of e-commerce for small and medium businesses (SMBs). When we think about online shopping and everything that goes into it – the digital storefront, payments, and inventory management – Shopify’s software empowers entrepreneurs to do it all themselves at minimal cost.

Headquartered in Canada, Shopify has lowered the barriers to entry considerably and allowed virtually anyone with a great idea or product to start up an e-commerce business. The company’s stock has been a resounding long-term compounder and the stock is up over 3,600% since first listing shares in May 2015.

In its latest quarter (Q3 2024), Shopify posted 26% year-on-year revenue growth to US$2.2 billion and also achieved a 19% free cash flow margin. For the company, it marked the sixth consecutive quarter of above-25% revenue growth and highlighted just how impressive Shopify’s business model is when it’s scaled up.

Shopify exited its logistics business in early 2023 as it realised just how capital intensive a sizeable logistics business really was. That decision has paid off as it focuses on its core software platform and payments platforms, such as Shop Pay and Shopify Payments with the latter being a payments gateway that allows merchants to accept payments without the need to go through a third-party payments processor.

In Q3 2024, Shopify Payments saw gross payment value (GPV) of US$43 billion, which was up 31% year-on-year and made up 62% of gross merchandise value (GMV) that passed through the Shopify platform. With the increased transition towards e-commerce and the demand for more boutique offerings, Shopify is sure to continue being a growth stock to watch in 2025.

6. NextEra Energy (NYSE: NEE)

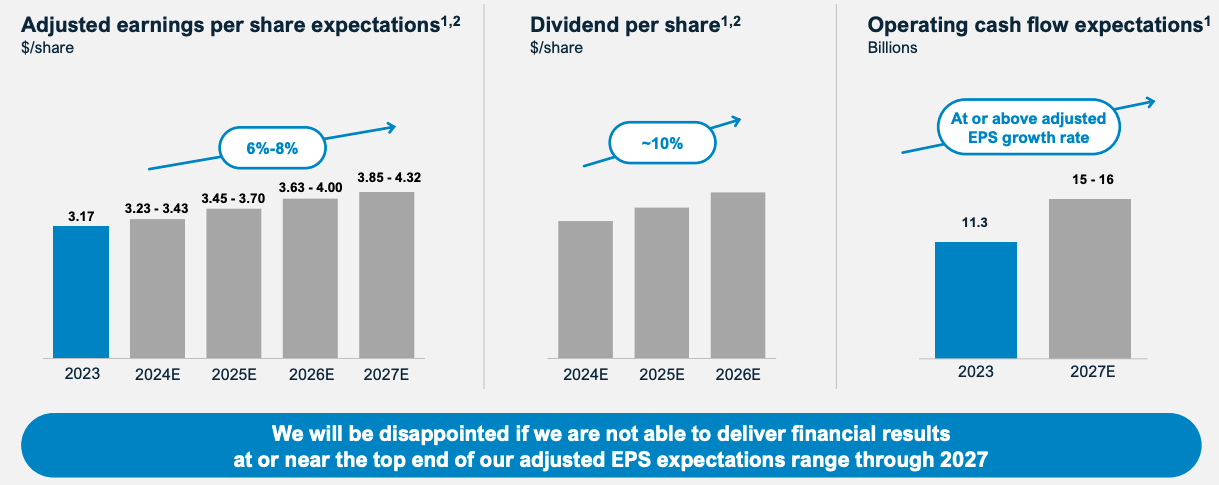

NextEra Energy Inc (NYSE: NEE) is the world’s largest producer of wind and solar power as well as the owner of the largest electric utility in the US – Florida Power & Light (FPL). Indeed, FPL is the company’s cash cow in that it’s a reliable producer of profits being situated in one of the fastest-growing states in the US (Florida). The nature of the utility market in Florida means FPL can provide predictable returns on capital invested.

NextEra’s other business is NextEra Energy Resources (NEER). This arm has 36 GW of renewable energy capacity already in operation and a 24 GW backlog of clean energy projects being developed. NEER partners with large commercial and industrial firms to hammer our long-term contracted investments for the provision of renewable energy.

NEER is actually the number one originator for US power and commercial & industrial customers and has a 20% market share in renewables and storage origination. This extraordinary network has allowed NEER to continue to build out its pipeline of renewable energy projects.

As a whole, NextEra Energy is backed by a strong balance sheet, with over 50% of its sizeable capital expenditure being met by its operating cash flow. This predictability in its business model has allowed NextEra Energy to provide stable guidance on both its adjusted earnings per share (EPS) and dividend growth over longer timeframes.

NextEra Energy: Reliable business and dividend growth

Source: NextEra Energy investor presentation, November 2024

For example, the company foresee around 6% to 8% growth in adjusted EPS through 2027 while it expects to grow its dividend per share at roughly 10% through 2026. That’s pretty much in line with its long-term averages on both fronts. The company has grown its dividend at a CAGR of around 10% since 2006 and NextEra became a Dividend Aristocrat – companies that have grown their dividend for 25 years or more – in 2022.

7. Tesla Inc (NASDAQ: TSLA)

Tesla Inc (NASDAQ: TSLA) is now synonymous with the electric vehicle (EV) revolution that’s taking the world by storm. Led by the charismatic – and often controversial – founder and CEO Elon Musk, Tesla has positioned itself as the leader in the premium EV space over the past decade.

Tesla’s business continues to perform admirably, even amid an ongoing price war in China’s EV market. Indeed, in the latest quarter (Q3 2024) Tesla reported its largest quarterly profit in over a year as it posted net income of US$2.2 billion, which was up 18% year-on-year.

The company also has exciting initiatives such as its Cybercab which will be fully autonomous and Musk predicts the company could be producing close to 2 million Cybercabs per year eventually. Both gross margin and operating margin improved in its latest period.

Musk has also been a big advocate of President-elect Trump and was recently appointed the head of the Department of Government Efficiency (DOGE). This close relationship with the incoming administration is being seen as a positive by the stock market and Tesla shares are up close to 45% since Trump was elected on 5 November.

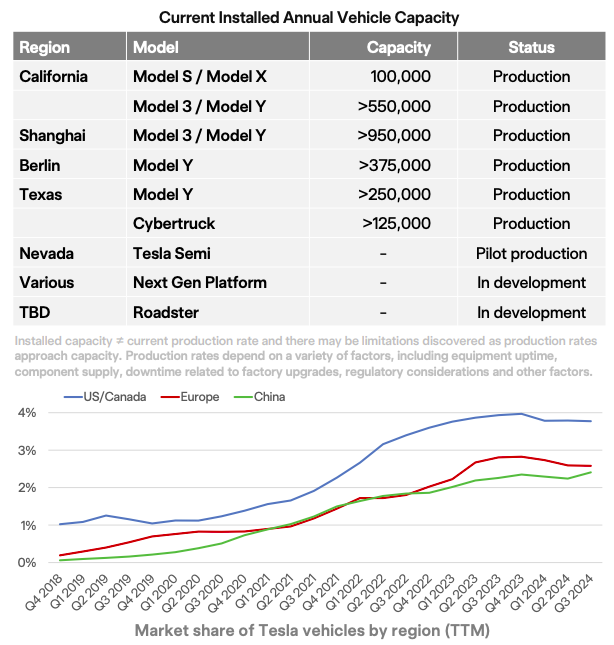

Tesla: Multiple manufacturing locations and room to grow market share

Source: Tesla Q3 2024 earnings presentation

On the business side, Tesla still boasts an enviable brand, manufacturing prowess and robust balance sheet. The company had US$33.7 billion in cash on hand at the end of Q3 2024 and this liquidity will surely prove to be an advantage as the company looks to build out its presence in the still-growing EV market globally.

Tesla still has a market share of only between 2% and 4% in its core markets, giving the company massive runway to expand its revenue worldwide. For investors who want exposure to a unique mix of both hardware and software growth globally, Tesla could be just the growth stock to provide that in 2025.

8. Meta Platforms Inc (NASDAQ: META)

Meta Platforms Inc (NASDAQ: META) is one of the biggest social media companies in the world, given its ownership of Facebook and Instagram. It also owns other key communications platforms like WhatsApp. More recently, the company has bet big on generative Artificial Intelligence (AI).

Meta is riding high on strong revenue growth and AI-driven innovation, but its aggressive spending on next-gen projects is dividing investor opinion. The tech giant reported an impressive 19% year-on-year revenue increase in Q3 FY2024, fuelled by its robust advertising business and AI-enhanced user engagement.

However, concerns over the rising costs for Reality Labs and metaverse initiatives have loomed large. Meta’s AI advancements are reshaping its platforms, driving an 8% boost in Facebook usage and a 6% increase on Instagram. These gains, combined with improved ad targeting, have solidified Meta’s core advertising business, which grew 19% in its latest quarter.

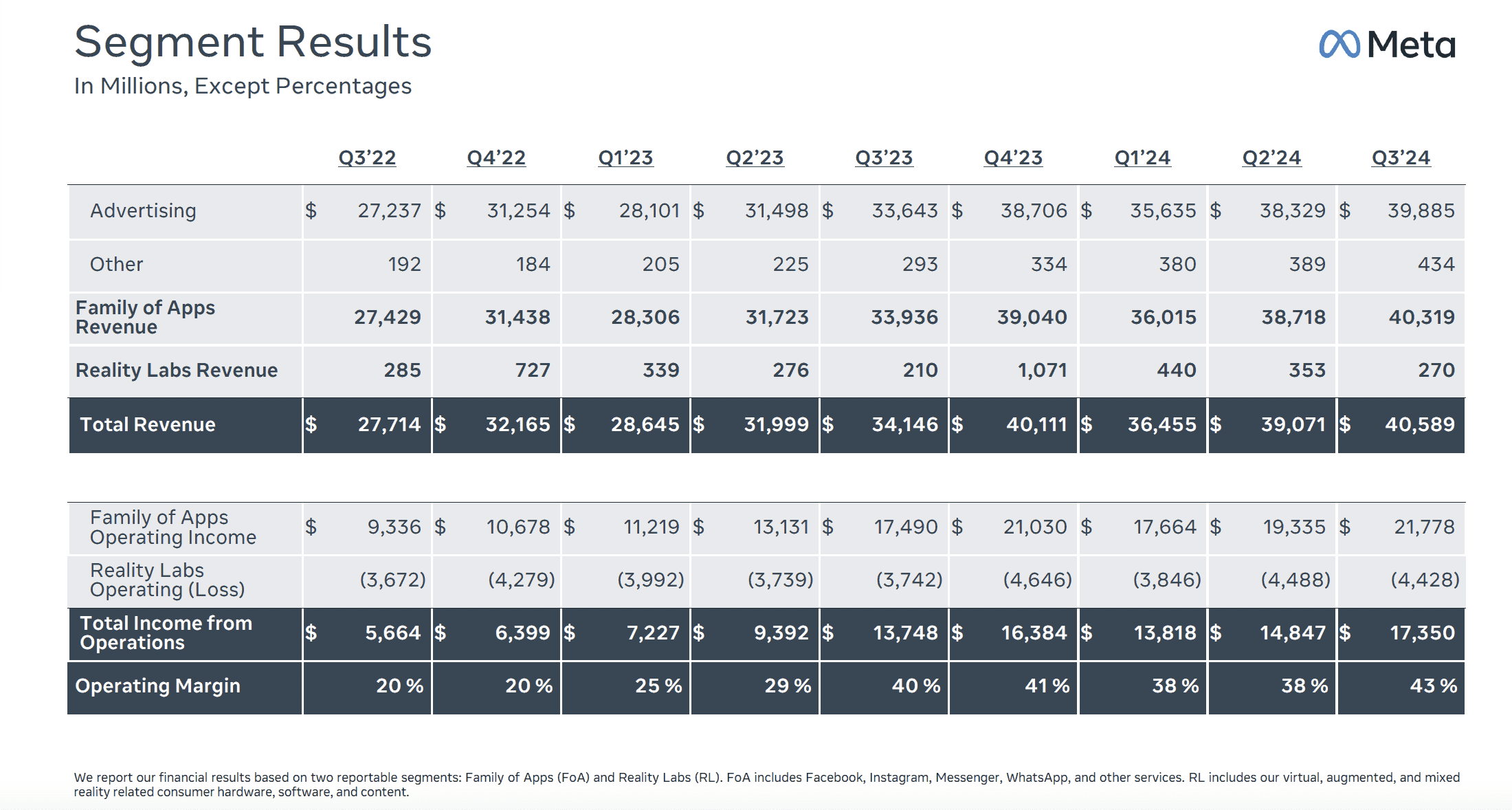

Meta’s Reality Labs: Division continues to bleed red ink

Source: Meta’s Q3 2024 earnings presentation

However, Meta’s bold vision for the future comes at a cost. Its Reality Labs division posted a $4.4 billion loss in Q3 FY2024, as investments in augmented reality (AR), virtual reality (VR), and the metaverse weigh heavily on its bottom line. Investors are waiting to see if the heavy investments being made today will pay off for Meta’s shareholders over the long term.

These initiatives could unlock massive long-term value, but they remain a gamble for now. For investors, Meta offers a tantalising mix of reliable cash flow and high-risk/high-reward potential. If investors believe in the transformative power of AI and are comfortable with volatility, this growth stock deserves a spot on your radar.

9. Broadcom Inc (NASDAQ: AVGO)

Broadcom Inc (NASDAQ: AVGO) is a linchpin of the modern tech ecosystem, making it a standout growth stock for 2025. With its dominant position in semiconductors, the company supplies critical components for data centres, AI hardware, and mobile devices – key drivers of the digital economy.

Broadcom has been riding the wave of surging demand for AI infrastructure, which has propelled its revenue and earnings to new highs. But Broadcom isn’t just about semiconductors. The US$69 billion acquisition of VMware, a cloud computing firm, has enhanced Broadcom’s software offerings, creating a hardware-software synergy that positions it as a leader in end-to-end technology solutions.

The numbers certainly back up the story. Broadcom’s Q3 FY2024 results were stellar, with revenue jumping 47% year-on-year and free cash flow hitting US$4.8 billion, representing 37% of revenue. The integration of VMware has already proven accretive, with infrastructure software revenue soaring to US$5.8 billion at an impressive 90% gross margin.

For investors, Broadcom offers a rare combination of growth and stability. Its consistent dividend increases, robust cash flow, and operational efficiency highlight its commitment to shareholder returns. As AI adoption accelerates and broadens out across the economy, Broadcom is positioned to capture significant market share. For investors, that makes it a compelling buy for both short- and long-term investors in 2025.

10. Costco (NASDAQ: COST)

Costco Wholesale Corporation (NASDAQ: COST) is more than just a retailer – it is a powerhouse of long-term growth, built on a foundation of unmatched value and loyal customers. Over the years, Costco has proven its ability to adapt, innovate, and thrive, making it a standout choice for investors looking to hold a stock for the next five years or more.

A key driver of Costco’s success is its steady financial growth. In the last decade, the company has consistently increased its revenue and net income, driven by a strategic focus on its membership model that generates recurring income. Costco’s focus on bulk goods and competitive pricing resonates with value-conscious shoppers, particularly during economic uncertainty and periods of higher inflation. With renewal rates exceeding 90%, Costco generates a reliable income stream that fuels both expansion and shareholder returns.

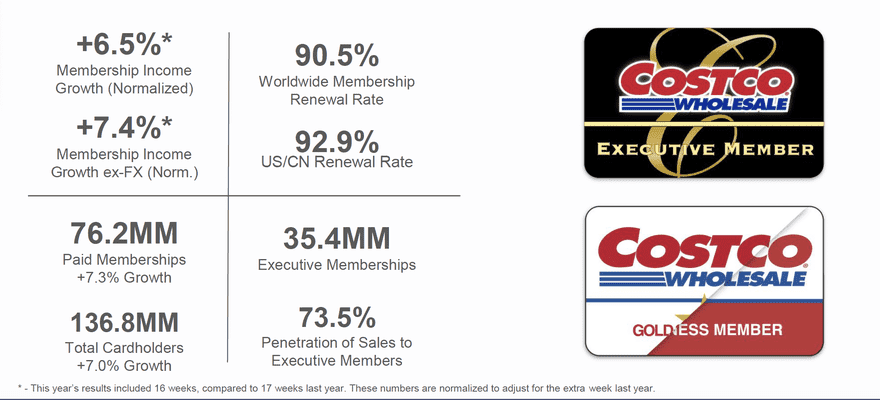

Costco: Renewal rates highlight the loyalty of its customers

Source: Costco Q4 FY2024 earnings highlights

Costco’s growth strategy is equally compelling. The company is aggressively expanding its global footprint, with plans to open dozens of new warehouses annually, including in emerging markets. Its loyalty from customers is unmatched and that gave Costco the confidence to raise its membership fee in the US & Canada (as of 1 September 2024) for the first time since 2017.

Meanwhile, Costco isn’t sitting still. The company is bolstering its e-commerce presence, ensuring it remains competitive in the digital era while maintaining its hallmark efficiency. Investors who buy Costco stock today are not just buying into a retailer; they are buying into a business built to endure.

11. CrowdStrike (NASDAQ: CRWD)

CrowdStrike Holdings Inc (NASDAQ: CRWD) stands out as a cloud-centric leader in the high-stakes battlefield of cybersecurity. The company’s Falcon platform, powered by cutting-edge AI, delivers real-time threat detection and response – exactly what today’s enterprises and governments need to stay ahead of increasingly sophisticated cyberattacks from both criminals and other sovereign states.

CrowdStrike’s strength lies in its innovative technology and its ability to keep customers hooked. With an enviable customer retention rate and a steadily growing client base, the company has cemented itself as a dominant force in the cybersecurity space.

But CrowdStrike isn’t resting on its laurels. The company is expanding its reach by targeting small-to-medium businesses (SMBs), a market ripe for disruption and in dire need of a higher level of cybersecurity protection. Aside from that, CrowdStrike’s subscription-based revenue model offers predictable cash flow and high gross margins, enabling the company to consistently reinvest in R&D. This keeps it ahead of emerging threats while solidifying its position as a go-to solution for cybersecurity. The company’s stock has been a massive long-term compounder, easily outperforming the S&P 500 Index’s 90% rise over the past five years.

CrowdStrike: Flying high on strong structural tailwinds

Source: SeekingAlpha

As organisations across the globe ramp up cybersecurity budgets, CrowdStrike is well-positioned to capture a significant slice of the pie. For investors looking to ride the wave of AI-driven innovation and the ever-growing demand for robust digital defenses, CrowdStrike is a stock to buy—and hold for the long haul.

12. PDD Holdings (NASDAQ: PDD)

PDD Holdings Inc (NASDAQ: PDD), the parent company of e-commerce giants Pinduoduo and Temu, is a standout US-listed Chinese stock with immense growth potential. Combining innovative strategies like gamified social commerce with aggressive international expansion, PDD has redefined online retail for both price-sensitive consumers in China and global markets.

Pinduoduo’s unique model has resonated with budget-conscious Chinese shoppers, driving robust growth in its domestic market. Meanwhile, Temu’s rapid expansion into over 70 countries, including the US and Europe, is reshaping global e-commerce with its value-driven offerings. This dual-market approach provides PDD with a rare blend of stability and growth.

Despite challenges like regulatory scrutiny and intensifying competition, PDD’s strategic investments in logistics and technology have solidified its position as an e-commerce leader. With China's economy showing signs of stabilisation and consumer spending perhaps slowly recovering, PDD is primed to ride the wave of rising e-commerce penetration.

For investors, PDD stands out as a compelling opportunity to tap into China’s growing digital economy while gaining exposure to its global ambitions. With its innovative edge and strong execution, PDD is a top pick for 2025, offering diversification and long-term growth in the ever-evolving e-commerce landscape.

13. Microsoft Corporation (NASDAQ: MSFT)

Microsoft Corporation (NASDAQ: MSFT) continues to shine as one of the most compelling growth stories in 2025, thanks to its leadership in artificial intelligence (AI) and cloud computing. The tech giant reported stellar Q1 FY2025 results, with Azure revenue soaring 34% year-over-year in constant currency. This robust growth highlights Microsoft’s ability to maintain its momentum in an increasingly competitive cloud market and marks it out as one of the leaders in cloud computing.

AI is playing a transformative role in Microsoft’s success, adding a 12-percentage-point boost to Azure’s growth. By integrating generative AI into flagship offerings like Office 365 Copilot, Dynamics 365, and GitHub Copilot, Microsoft is setting the “gold standard” for enterprise innovation and AI use cases. To support this, the company is ramping up capital expenditure in the second half of FY2025, ensuring its AI infrastructure keeps pace with surging demand from clients.

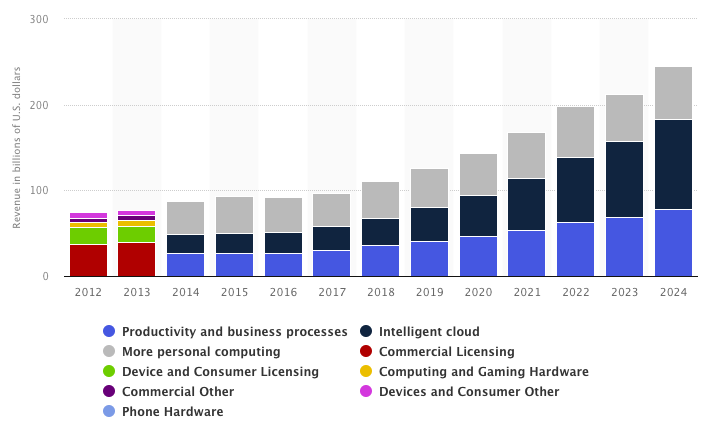

Microsoft: Intelligent Cloud soars to take largest share of company’s revenue over the past 12 years

Source: Statista

Microsoft’s resilience goes beyond AI. Diversified revenue streams, including gaming through Xbox, LinkedIn’s professional services, and enterprise solutions, offer a cushion against market headwinds. The company’s commitment to sustainability – with ambitious renewable energy projects and carbon-negative goals – further underscores its forward-looking strategy.

Backed by consistent revenue growth, a fortress-like balance sheet, and cutting-edge innovation, Microsoft is well-positioned to dominate the AI revolution. For long-term investors looking to ride the wave of digital transformation, this tech titan remains a must-watch growth stock in 2025.

14. Palantir Technologies (NYSE: PLTR)

Palantir Technologies Inc (NYSE: PLTR) is riding the twin waves of booming AI adoption and increased global defense spending, making it a compelling growth stock for investors in 2025. Known for its advanced data analytics platforms, Gotham and Foundry, Palantir supports government and enterprise clients in solving complex challenges with actionable insights.

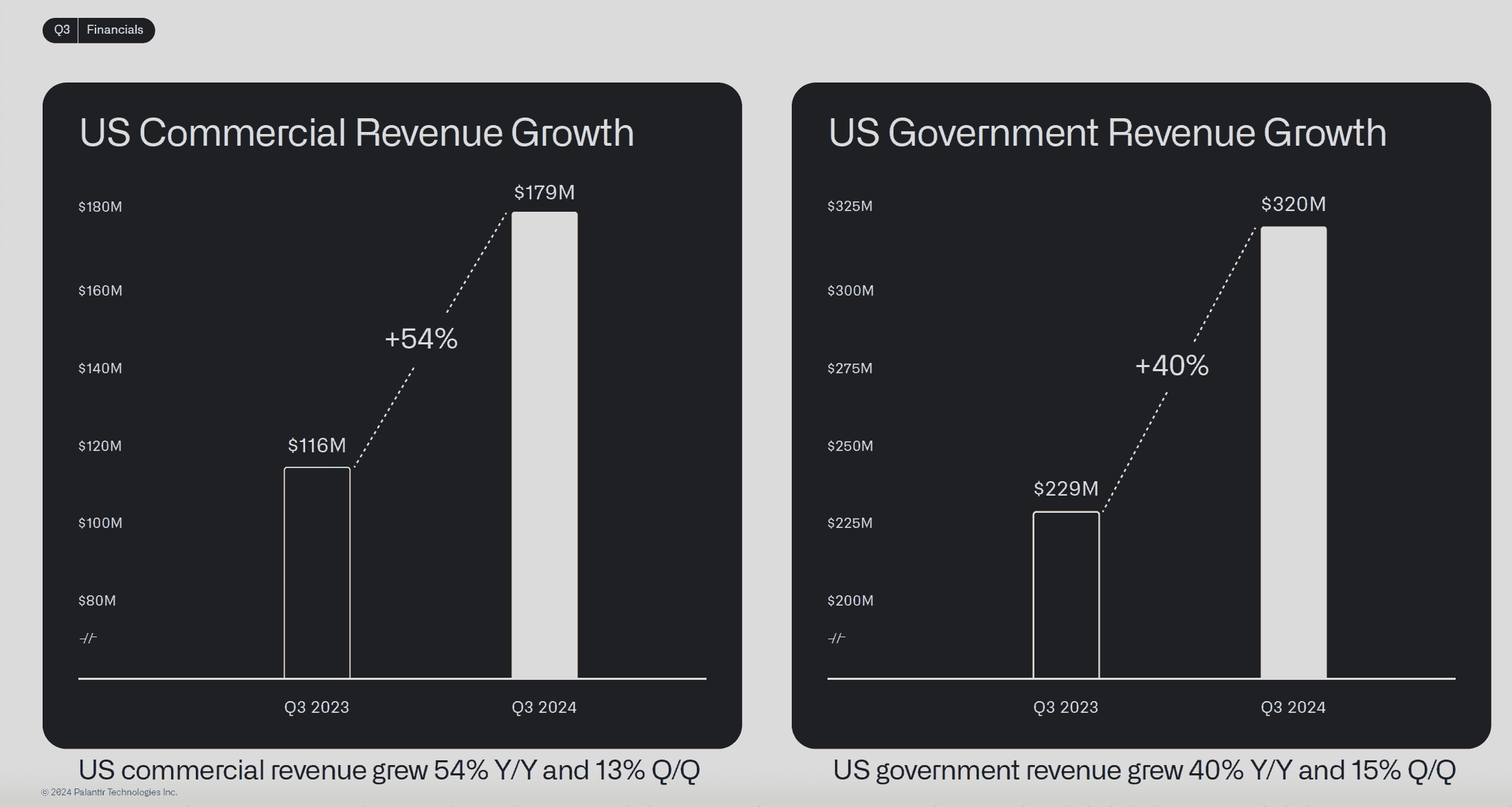

The company’s Artificial Intelligence Platform (AIP) has become a key growth driver, enabling organisations to seamlessly integrate AI capabilities into their operations. Palantir’s expertise in predictive analytics and decision-making tools continues to attract enterprise clients, with US commercial revenue growing 54% year-on-year. Defence spending remains a core pillar of Palantir’s success, with US government revenue soaring 40% in the latest quarter.

Palantir: Boasting both commercial and government revenue growth

Source: Palantir’s Q3 2024 business update

As geopolitical tensions drive higher defense budgets globally, Palantir is well-positioned to secure lucrative contracts. Key wins, like TITAN and Maven, highlight the trust placed in its technology. The company’s financial health is equally impressive, achieving profitability for eight consecutive quarters and generating $1 billion in free cash flow.

While its premium valuation reflects high expectations, Palantir’s strong AI momentum and robust government partnerships suggest significant upside. For investors seeking exposure to AI and defense, Palantir offers a unique blend of innovation and reliability, positioning itself as a key player in the AI-driven future.

15. Starbucks (NASDAQ: SBUX)

Starbucks Corporation (NASDAQ: SBUX) had built itself up as the default coffee option for many people given its ubiquitous presence in both the US and globally. However, it has recently lost its way with its outlets becoming unwelcoming and its beverages menu boasting more sugary drinks than caffeine ones.

Starbucks is, therefore, betting big on a return to its roots to tackle declining sales and shifting consumer trends. Under the leadership of its new CEO, Brian Niccol – best known for his impressive turnaround of fast-casual Mexican restaurant chain Chipotle – Starbucks has unveiled an ambitious plan to revitalise its iconic brand. While the coffee giant faces near-term challenges, Niccol’s back-to-basics strategy could make Starbucks an intriguing short-term play for investors willing to watch the turnaround unfold in 2025 and beyond.

Dubbed the “Back to Starbucks” plan, Niccol’s approach focuses on creating a welcoming “third place” experience by redesigning stores, simplifying menus, and enhancing operational flow. Innovations like no extra charge for non-dairy milk and improved mobile ordering aim to draw customers back while supporting baristas with better staffing strategies should strengthen the overall experience.

While these changes are bold, they are not without risk. Scaling back promotions and re-establishing Starbucks as a premium brand may take time to resonate with customers. However, Niccol’s proven track record of transforming struggling businesses gives investors reason for optimism.

For those interested in pursuing a business that could get back to its former glory days, Starbucks offers an opportunity to buy into a potential turnaround story. If Niccol’s plan succeeds, Starbucks could regain its competitive edge and drive significant shareholder value in the process.

Heading into 2025: What investors should remember

As we step into 2025, the global market landscape presents a compelling mix of opportunities and uncertainties. Major indices like the NASDAQ Composite and S&P 500 Index are hovering near their all-time highs, reflecting Wall Street’s optimism amid an incoming second Trump presidency and robust growth in the US economy.

The return of Donald Trump to the White House has fuelled excitement over potential pro-business policies, such as tax cuts and deregulation, which could create tailwinds for key sectors. However, this enthusiasm is tempered by the cautious recognition of potential volatility from his administration, such as shifts in trade policies, sizeable tariffs, fiscal deficits, and regulatory frameworks that could create new challenges.

Sectors like industrials, financials, and energy stand to gain from a friendlier regulatory environment, while areas like renewable energy and technology may face short-term uncertainties stemming from trade tensions and evolving global alliances. However, as always, the market’s worries over the impact of political policies rarely turn out to be as terrible in reality. Amid these developments, the stock market continues to offer opportunities for both growth and stability.

Diversification also takes on new importance, particularly with US-listed Chinese stocks offering access to China’s domestic recovery and growth potential, even amid geopolitical tensions. Whether seeking short-term gains or long-term resilience, a diversified portfolio aligned with strong fundamentals and global trends is key. By staying adaptable, investors can navigate the upcoming year and position themselves to make money across the landscape, all the way from growth stocks through to dependable dividend stocks.

Related Articles

$660B Capex Bill Triggers $900B Wipeout: Why Apple Shares Outperform Amazon and Google Despite AI Lag

Based on financial disclosures, the combined 2026 capital expenditure forecasts for Meta, Amazon, Google, and Microsoft are projected to reach $660 billion. This figure is not only significantly higher than the $410 billion forecast for 2025 and $245 billion for 2024, but even surpasses the GDP of I

Amazon Stock Predictions for 2026 to 2030: Will They Exceed Expectations and Achieve Major Long-Term Goals?

TradingKey - As we head into 2026, many investors are questioning where Amazon (AMZN) fits into the technology world.

A Crash After a Surge: Why Silver Lost 40% in a Week?

TradingKey - Spot silver (XAGUSD) prices continue to decline. Silver plunged 20% on Thursday, breaking below $71 per ounce, with the sell-off intensifying on Friday as prices fell further below $64. Compared to the all-time high set on January 29, silver prices have retraced more than 40%, wiping out nearly all gains accumulated over the previous month.

Is Bitcoin’s Four-Year Cycle Dead in 2026?

Is the Bitcoin 4-year cycle dead? After 2025 broke historical records with a red post-halving year, institutional analysts explore if the Bitcoin price has decoupled from the halving countdown. Analyze the impact of spot ETFs, global liquidity, and the roadmap to the 2028 halving in this 2026 market