US Stock Sector Analysis: Forecasting Q4 Sector Growth Using Machine Learning

In the ever-evolving landscape of financial markets, investors must stay ahead of market trends to make informed decisions. Whether managing a portfolio or strategizing investments, understanding which sectors are poised for growth or decline can provide a competitive advantage. Traditional forecasting methods often fall short in capturing the complex interdependencies between sectors and the fluid nature of market dynamics. This is where machine learning, specifically Long Short-Term Memory (LSTM) models, comes into play. LSTM models, a type of recurrent neural network (RNN), excel at analyzing historical data to predict future trends by identifying patterns and long-term dependencies in sequential data.

The logic behind this model is that, in an industrial value chain, a sector is often influenced by the industries upstream and downstream from it. For example, changes may begin in the upstream sector and gradually pass down to downstream sectors. By analyzing how different industries impact each other, we can uncover the relationships and the sequence of changes.

How Does the Model Work?

1. Gathering Historical Data and Scaling the Data

All stocks listed in US exchange with 34-year historical quarterly revenue growth are gathered and segmented based on their LSEG TRBC Industry Group. Revenue can offer early signals of changes or trends across different industries. By analyzing revenue patterns, we can anticipate shifts in market demand, customer preferences, or economic conditions.

2. Creating Sequences

The model doesn’t just look at one data point at a time—it looks at sequences of data. It analyzes the last 4 quarters of growth for a sector to predict the next quarter’s performance. This helps the model understand trends over time.

3. Training the Model

The LSTM model is trained using historical data. During this process, it learns to recognize patterns and relationships between past data and future outcomes. Think of it as teaching the model to connect the dots between what happened in the past and what’s likely to happen next within all sectors.

5. Making Predictions

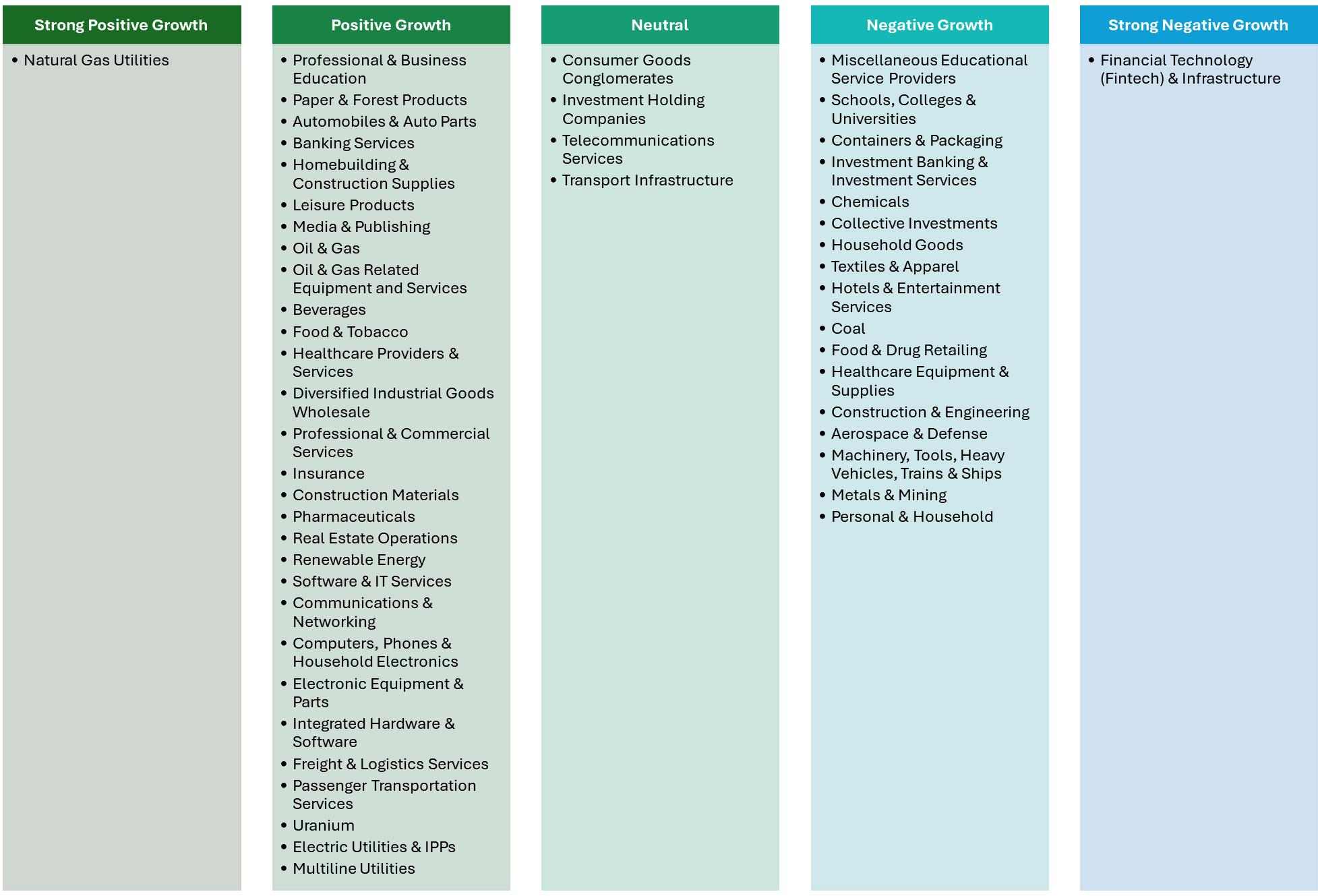

Once the model is trained, it can analyze the latest data and predict how each sector will perform in the next quarter. The predictions are categorized into five levels:

• Strong Negative Growth

• Negative Growth

• Neutral

• Positive Growth

• Strong Positive Growth

By examining how growth in one sector influences others, the model provides a more comprehensive and accurate forecast of economic dynamics. Investors can use these predictions to adjust portfolio allocations, increasing exposure to sectors expected to grow while reducing holdings in those forecast to decline.

Prediction Result for Q4 Revenue Growth

Source: Tradingkey.com

Deep Dive: Fundamentals of Key Growing Sectors

While the LSTM model provides quantitative predictions, understanding the underlying drivers of sector growth is essential for informed decision-making. Below, we explore the fundamentals of sectors expected to perform well in Q4 2024.

Natural Gas Utilities

Prediction: Strong positive revenue growth in Q4 2024.

Key Drivers:

Increased Demand:

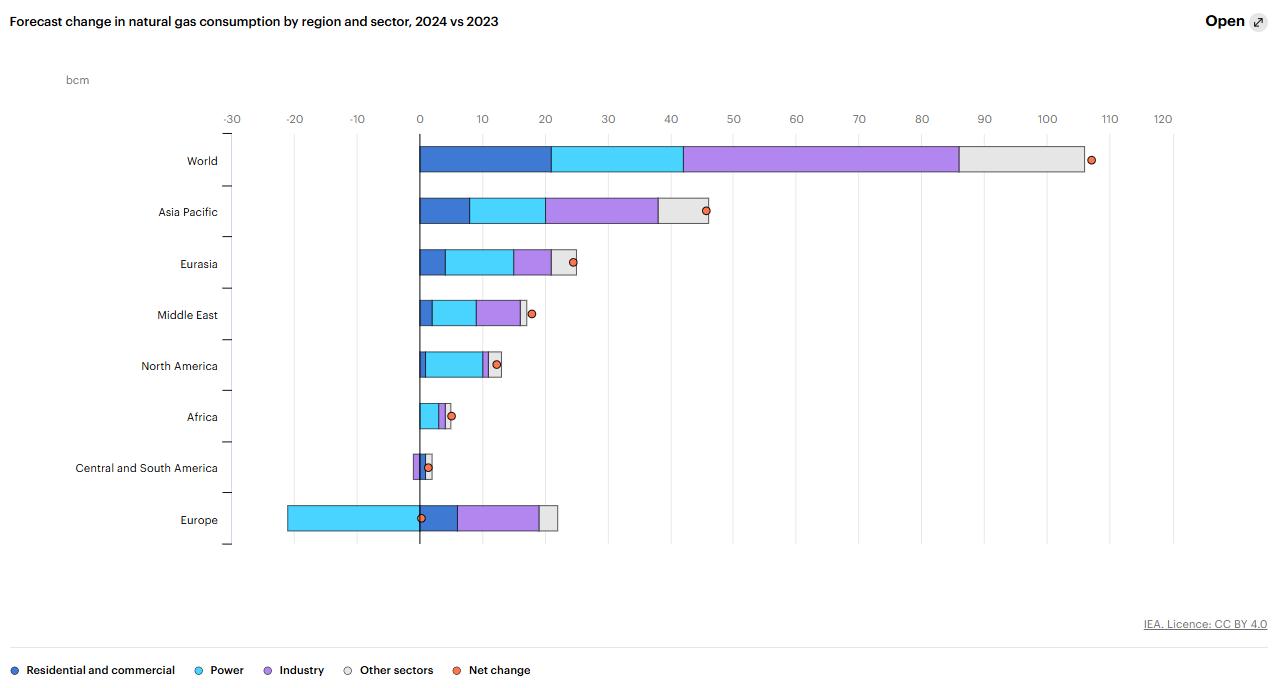

• According to the International Energy Agency (IEA), the global natural gas market is recovering from supply disruptions in 2022-2023. Demand is projected to reach record levels in 2024-2025, driven by:

○ Asia-Pacific Growth: Rapid economic expansion in the region is expected to account for nearly 45% of incremental demand.

○ Industrial Recovery: European industrial gas demand is rebounding, while Asia’s industrial applications continue to drive consumption.

○ Winter Heating Needs: Colder-than-average temperatures forecast for Q4 2024 are expected to boost heating demand, tightening inventories and creating upward price pressure.

• Increased LNG exports from the U.S., driven by European demand for alternative energy sources.

Source: IEA

Tight Supply:

• Demand growth is anticipated to outpace supply, leading to market tightness. This imbalance could result in higher natural gas prices, benefiting producers and utilities.

Source: EIA, Tradingkey.com

Representative Companies:

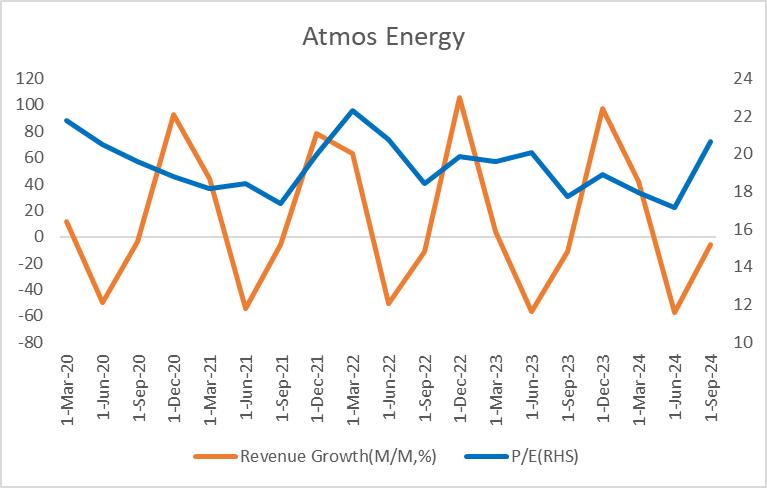

Atmos Energy Corporation: A leading natural gas distribution and pipeline company, It is well-positioned to benefit from seasonal demand cycles, with revenue typically peaking in Q4.

Source: Reuters, Tradingkey.com

Technology Sector

The technology sector continues to be a major growth driver in the U.S. economy, with numerous subsectors benefiting from macroeconomic tailwinds, innovation, and AI adoption.

Subsectors Expected to Grow:

1. Software & IT Services:

• Growth is fueled by cloud computing, enterprise software, and cybersecurity. The global cloud computing market is projected to grow at a 14.1% Compound Annual Growth Rate (CAGR) from 2023 to 2030, reaching $1.5 trillion by 2030 according to Research and Markets.

• Key Players: Microsoft (Azure), Salesforce, ServiceNow, and CrowdStrike.

2. Communications & Networking:

• Demand is driven by 5G infrastructure deployment, IoT, and edge computing. The 5G infrastructure market is forecast to grow at a 49.8% CAGR, reaching $131 billion by 2030 by Maximize Market Research.

• Key Players: Cisco.

3. Computers, Phones & Household Electronics:

• Despite macroeconomic challenges, consumer demand for smartphones remains resilient. Global smartphone shipments grew 3.6% year-over-year in Q3 2024 the fifth consecutive quarter of shipment growth according to International Data Corporation.

• Key Players: Apple.

4. Electronic Equipment & Parts:

• Demand for sensors, batteries, and other components is rising due to applications in automotive, renewable energy, and consumer electronics. The flexible electronics market is expected to grow at a 9.72% CAGR through 2032 from SNS insider report.

• Key Players: Zebra Technologies.

5. Integrated Hardware & Software:

• Companies offering seamless integration of hardware and software are benefiting from vertical integration strategies.

• Key Players: Mobileye.

Subsectors with Weak Growth:

1. Office Equipment: Declining demand for traditional office hardware due to remote work trends.

2. Semiconductors & Semiconductor Equipment: While long-term growth prospects remain strong, cyclical subsegments like memory chips may experience weaker demand in Q4 2024.

AI as a Key Growth Driver for Technology

The integration of artificial intelligence is transforming the technology sector, creating opportunities across multiple phases of growth. In the technology sector, we can also apply industry rotation to invest along the upstream and downstream of the industrial chain. Using the AI stocks roadmap defined by Goldman Sachs to illustrate the predictive results of our model is most appropriate. According to Goldman Sachs Research, the AI-driven growth cycle can be divided into four phases. We can see that we are moving from Phase 2 to Phase 3 now.

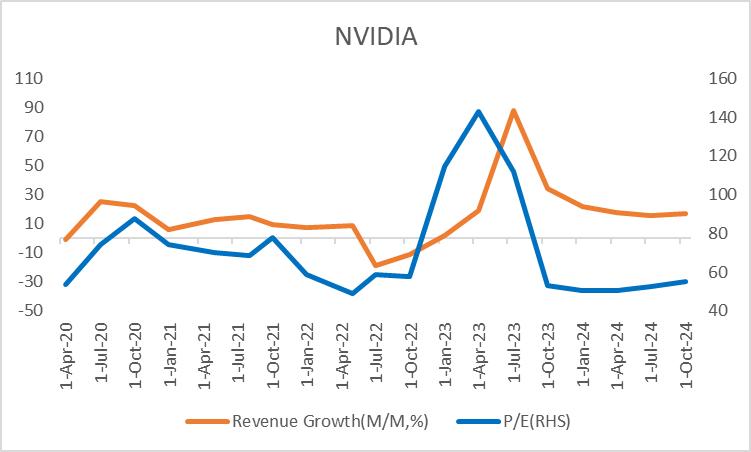

Phase 1: Specialized AI Hardware

Nvidia dominates this phase, with over 80% market share in AI GPUs and partnerships with major tech giants. NVIDIA’s revenue growth started to drop from 2023.

Source: Reuters, Tradingkey.com

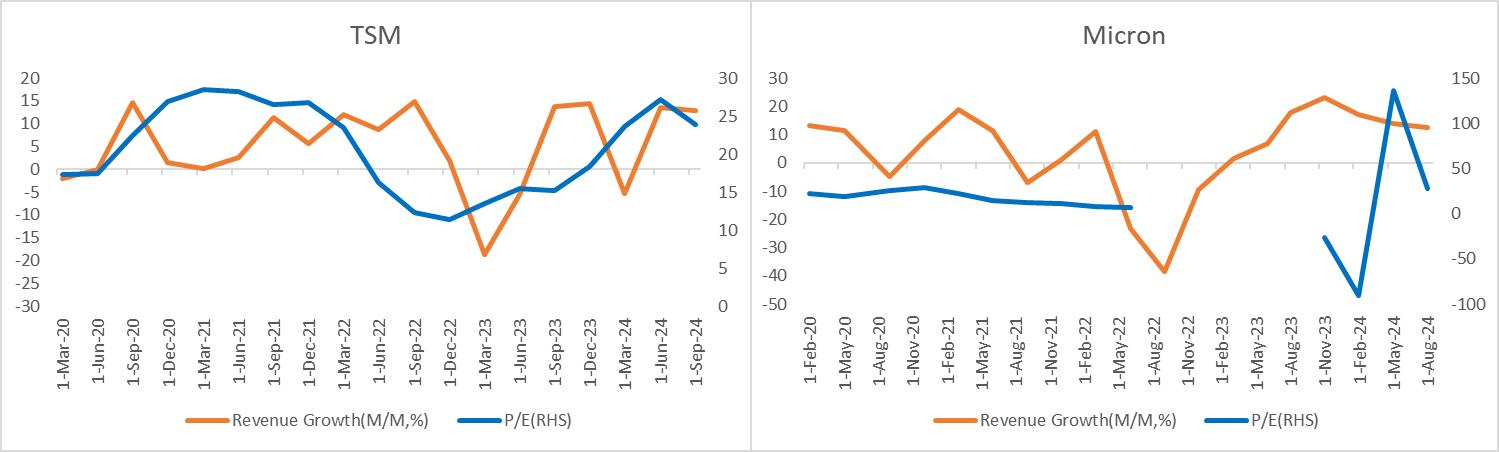

Phase 2: AI Infrastructure

Companies building AI infrastructure, including semiconductors, data centers, and cloud services, are well-positioned to benefit. For example, semiconductor companies include:

• Designers: ARM, now a part of NVIDIA, designing the architecture for microprocessors, GPUs, and system-on-chips (SoCs).

• Memory Producers: Micron specializes in the production of memory products, including DRAM, NAND, and NOR flash memory.

• Equipment Manufacturers: Applied Materials supplies equipment used for the production of semiconductor (silicon) wafers.

• Foundries: TSMC is the world’s largest semiconductor foundry.

Source: Reuters, Tradingkey.com

Phase 3: AI-Driven Sales

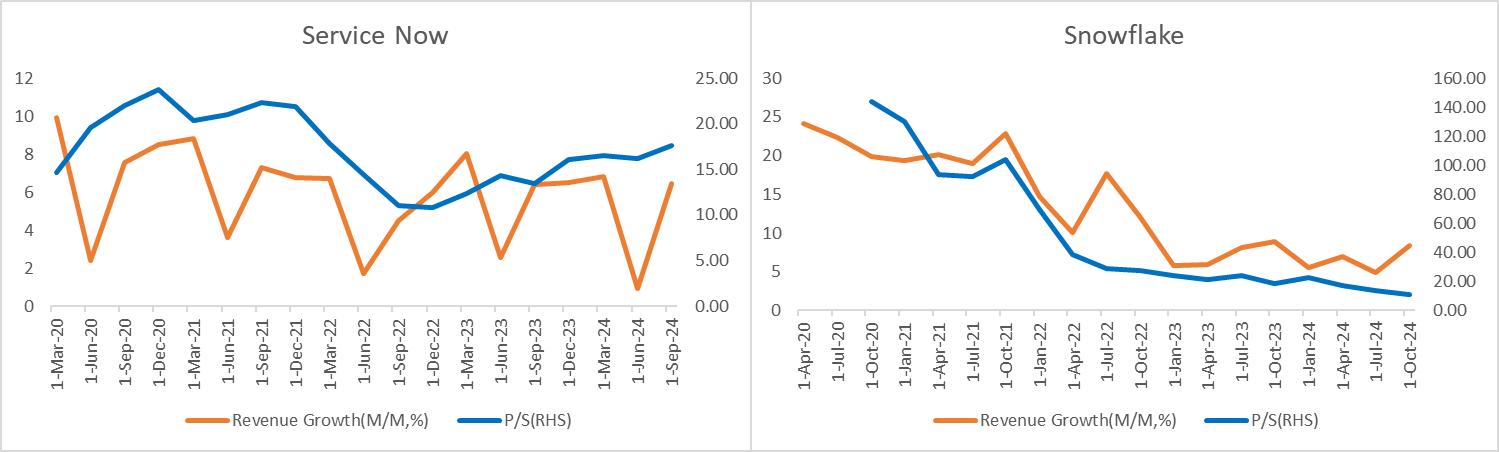

Companies that successfully integrate AI into their product offerings to boost revenue are the primary focus of this phase. At this stage, businesses capable of leveraging AI to drive sales are expected to see significant benefits. Among these, software and IT services companies may hold the greatest advantage.

Software-as-a-Service (SaaS) stands out as the most lucrative segment within the AI value chain due to its recurring subscription model, high profit margins, and scalability. By incorporating AI into their platforms, SaaS providers can offer advanced features to customers, enhance revenue per user, and expand their reach into global markets with minimal operational overhead. This positions SaaS as a critical driver of innovation and long-term profitability in the AI ecosystem.

However, over the past two years, the SaaS industry has experienced a decline. This downturn can be attributed to several factors, including rising interest rates, which have a significant impact on SaaS companies due to their sensitivity to financing costs. Additionally, the pandemic-driven surge in digital transformation and remote work led to heightened valuations for SaaS firms, as their growth accelerated during that period. Post-pandemic, these companies are hard to maintain the same level of growth, contributing to the recent slowdown.

With interest rates now declining, signs of recovery are emerging. For instance, Snowflake reported a 29% year-over-year revenue growth in Q3, with AI playing a significant role in driving this expansion. The company emphasized that AI adoption is growing rapidly on its platform. While part of this growth is directly tied to AI-related advancements, a broader rebound in IT spending is also contributing. As macroeconomic conditions stabilize, businesses are increasingly reinvesting in cloud infrastructure and analytics platforms.

Representative Companies:

ServiceNow: leader in digital workflow solutions, empowers businesses with Now Assist for AI, leveraging generative AI to automate complex workflows, enhance decision-making, and deliver seamless, personalized service experiences at scale.

Snowflake: Increasing demand for its core data storage products as well as healthy interest in its new and forthcoming an AI and interoperability tools.

Source: Reuters, Tradingkey.com

Phase 4: AI-Driven Productivity

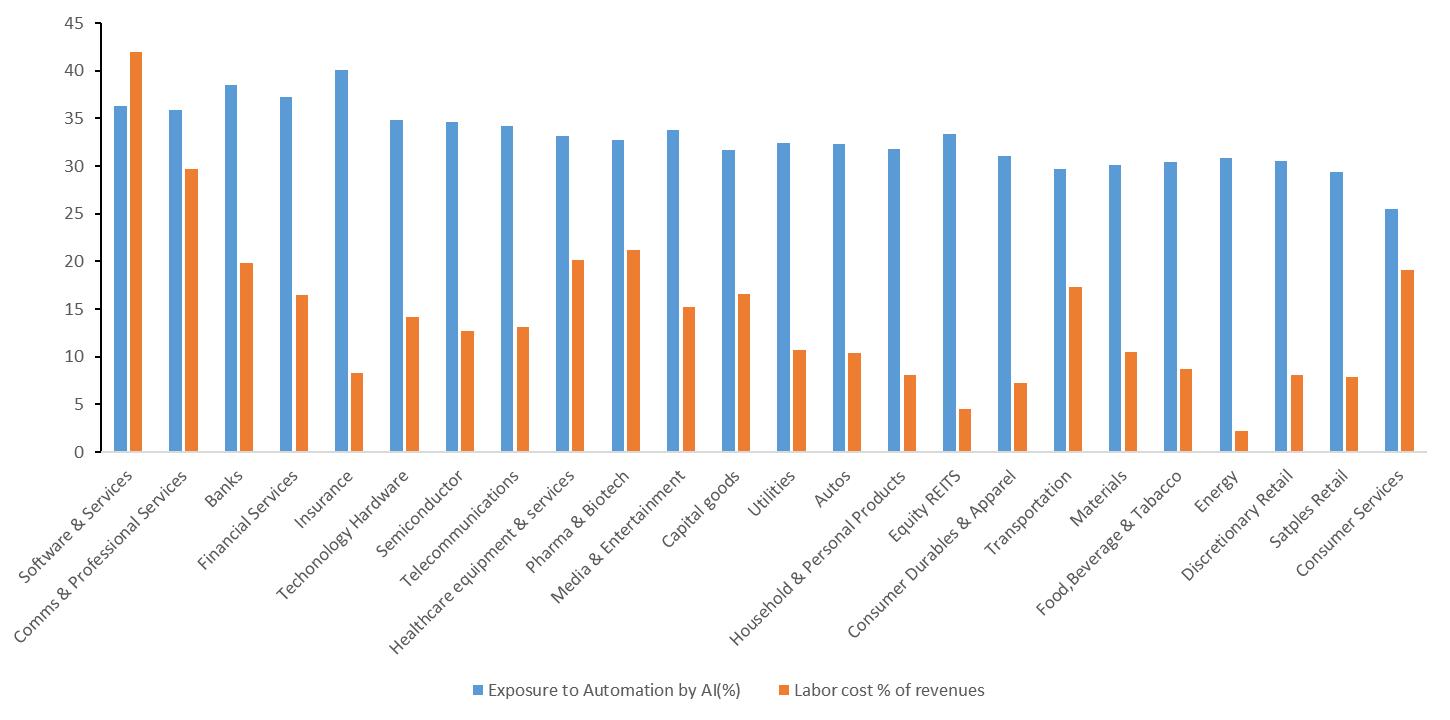

In this final phase, AI adoption is expected to drive productivity gains across industries. Industries with high labor costs can benefit more from AI employment.

Source: Goldman Sachs, Tradingkey.com

Conclusion: Opportunities and Risks

This report outlines an industry rotation model built using LSTM to predict revenue growth in the fourth quarter, with a focus on analyzing the fundamentals of the natural gas utilities and technology sectors.

Key takeaways include:

• Natural Gas Utilities: Rising demand, supply constraints, and global consumption trends make this sector a strong investment candidate.

• Technology Sector: Growth opportunities exist in AI-driven subsectors like cloud computing and software, though caution is advised in cyclical areas such as semiconductors.

The model is subject to macroeconomic or government-related risks, including factors such as geopolitical tensions, regulatory shifts, or new government policies may create uncertainties that are difficult to predict, which could impact its accuracy.