Micron – Huge Hit by the Market but the Growth Story is Still Here

Micron stock price crashed by 16% after the company announced the first quarter results for the new fiscal year. The market reacted badly mainly because the soft guidance itself reiterated the negative perception about memory chip stocks being notoriously cyclical. However, the investment thesis from the previous article remains largely intact. Firstly, the company is still in the very early stages of riding the High Bandwidth Memory (HBM) wave of sustainable growth and margin expansion. Secondly, the non-HBM revenue will still benefit from the positive supply-demand dynamics within the memory market. We reiterate the previously assigned price target of USD130.00-160.00.

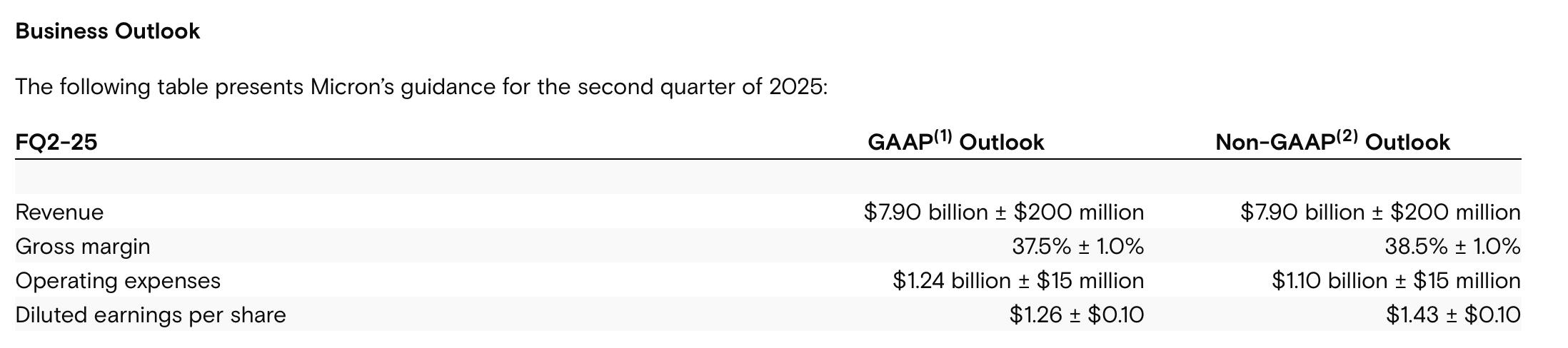

Barely meet the consensus but a huge correction in the Q2 outlook

The first quarter results of the new fiscal year were largely in line with the expectations both in terms of top line and bottom line:

· Earnings per share: $1.79, adjusted vs. $1.75 expected

· Revenue: $8.71 billion vs. $8.71 billion expected

The revenue grew solidly with 84% year-over-year. The gross margin inched up to 38.4% versus 35.3% the quarter before. The reported net income ended up at $1.87bn vs net loss of $1.2bn the year before and USD900mn from the previous quarter.

However, the main issue is the weak Q2 guidance. The mid-point revenue guidance of $7.9bn is far below the initial consensus of $8.9bn. The revenue will represent just 36% growth from Q2 last fiscal year, and that’s a huge deceleration from the growth rate posted most recently at 84%. We can say the same for the adjusted EPS guidance of $1.43 compared to the previously anticipated $1.92.

Source: Company Presentation

The weakness mainly comes from the NAND product line and non-HBM DRAM business to a lesser extent. NAND comprises 25% of the total revenue (DRAM and HBM represent the other 75%). The reason behind this is the fact that the demand is still tepid due to soft spending in the consumer electronics industry. And as per the current long-term strategy of Micron, this is a legacy business, and it will not be a priority in the future.

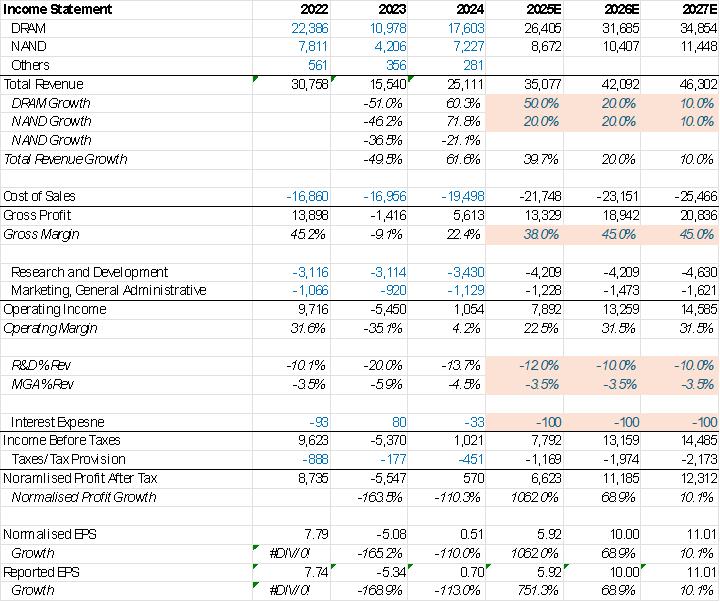

Source: TradingKey, Company Financials

It’s not all doom and gloom

On the positive note, HBM (high bandwidth memory), the recently developed AI-related product used for data centers, still holds very strong. MU doubled its HBM revenue on a quarter-to-quarter basis.

The management provided a more optimistic idea about the TAM of the product - $100bn by 2030, implying a CAGR of 36%. Expanded its HBM TAM to $30B in 2025, and considering the small number of market players, MU can easily get a solid piece of the pie.

How to look at MU from now on

In the previous report, we mentioned several factors that can help with the normalization of the supply-demand situation within the memory market: 1) higher portion of HBM revenue; 2) more capacity being allocated towards HBM chips and less capacity towards non-HBM; 3) high barriers of entry in the industry; 4) higher portion of long-term contracts to lock prices. We believe these dynamics still hold valid.

Initially, we estimated a revenue growth of 50% for 2025. At this point, this number appears to be on the more optimistic side. The reality is that it will take some time for the consumer electronics demand to take off and most probably we will see improvements in the latter half of the fiscal year. However, this is a question about “when” not “if”, as the AI-generated consumer electronic products (phones, personal computers, cars) will gradually get introduced in the market. Thus, 40% growth may seem more reasonable in this situation.

On the margins’ side, the situation is also quite certain that GPM and OPM will continue the upward trend, as the high-value HBM product will be a tailwind.

At this point, we will not revise our target price, as the stock appears to have a pretty good risk/reward profile. The current P/E ratio after the price drop still stands at mid-teens, implying 50% investment return upside.

Source: SEC Fillings, TradingKey