Visa: Unseen Strength in a Fragmented Fintech World

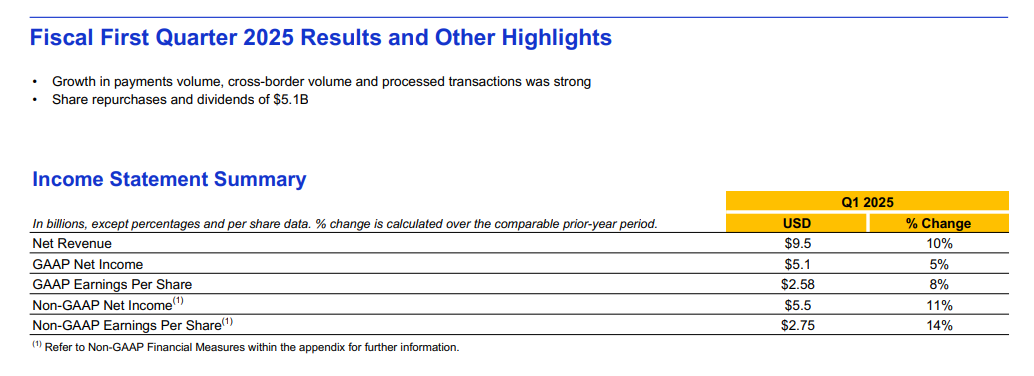

- Q1 FY25 revenue rose 10% YoY to $8.8B, led by strong growth in international transaction fees (+14%) and data processing revenue (+9%).

- Free cash flow hit $5.1B in the quarter, matching total shareholder returns via $3.8B in buybacks and $1.3B in dividends.

- Visa processed 63.8B transactions, up 11% YoY, with rising volumes across non-card payments via APIs and bank integrations driving network velocity.

- AI-driven fraud prevention is now sub-50ms latency, improving 99%+ transaction acceptance while enabling monetizable services for fintech partners.

TradingKey - With bottom-end disruption from fintechs and digital currencies under consideration from central banks, Visa (NYSE: V) still shows how size, trust, and network depth can beat speed alone. While investors increasingly favor payment enablers with new UX or crypto-nativistic architectures, Visa has staged a reacceleration under the radar. It posted 10% year-on-year growth in revenue and 14% EPS growth on a non-GAAP basis in Q1 FY25, defying margin compression and structural disintermediation fears.

This isn't a return to historic norms, however. Instead, Visa is taking its old assets, risk models, worldwide acquirer relationships, and dispute management rails, and reframing them as a next-gen orchestration layer for digital payments. With more than $5.1 billion in free cash flow this quarter and $5.1 billion paid out to shareholders in buybacks and dividends, the company has shown both defensive resiliency and capital discipline. Its strategic purchase of Featurespace, a real-time AI anti-fraud company, only enhances its competitive advantage in a more adversarial payments environment.

The broad-brush thesis: Visa's defensive moat has become an offensive flywheel. It's no longer about volumes on cards but about becoming ingrained in each and every node of the digital transaction journey, from alternative payment methods (APMs) to added-value fraud prevention. With secular tailwinds such as e-commerce globalization and API-based financial-technology integration gaining momentum, Visa finds itself more like a traffic cop than a toll collector on converging financial highways.

Source: Q1-FY25

From Plastic to Protocol: Visa's Embedded Empire

Visa's business remains fundamentally simple: it doesn't issue cards, lend credit, or take default risk. Rather, it enables secure digital transactions between consumers, merchants, and financial institutions in more than 200 countries. Its business model captures this enablement through four principal streams: service revenue linked to card payment volumes, data processing charges per transaction, cross-border activity charges in foreign currencies, and added services such as tokenization, analytics, and risk management.

This quarter demonstrated this model's resilience. Service revenue increased 8% year over year to $4.2 billion, while data processing increased 9% to $4.7 billion, reflecting increased engagement across the network. International transaction revenue was, however, where it truly excelled this quarter, increasing 14% to $3.4 billion, reflecting cross-border volumes up 16% on a constant-dollar basis. There's where Visa's embedded infrastructure excels. With increasing competition from bank-driven payments such as SEPA Instant and digital wallets such as Apple Pay, Visa's integration with banks and merchants provides it with unmatched distribution.

Processed transactions increased 11% to 63.8 billion this quarter, reflecting both network usage velocity and volume. Notably, Visa growth isn't coming solely from cards. With its so-called "network of networks" strategy, Visa is increasingly using APIs and partnerships to enable ACH, real-time payments, and A2A flows. The acquisition last quarter of Pismo, as well as its strategic layering of AI-powered fraud prevention tools such as those by Featurespace, are essential in broadening Visa’s position in adjacent flows beyond conventional consumption-based spending.

The company's moat isn't size, but optionality: its architecture can consume new modes of payment without cannibalizing its old ones. Thus, Visa is creating a horizontal payments operating system while charging for the verticals, whether it's card-present retail, CNP ecommerce, or embedded finance inside applications.

.png)

Source: Q1-FY25

Defending the Rails: A Dominator in a Time of Digital Disruption

Visa's toughest competitor isn't another payments network, it's disintermediation in the form of digital wallets, buy-now-pay-later (BNPL), and central bank digital currencies (CBDCs). Although MasterCard and American Express provide comparable infrastructure, their issuer coverage and overall penetration are less than Visa's. Visa's real challenge lies elsewhere, horizontal fintech ecosystems such as Apple, Google, and Shopify, which seek to own the layer of checkout.

However, Visa’s market position hasn’t been dented. On the pricing side, Visa has successfully defended its interchange economics, as regulators in Europe and India continue to pressure it. It raised client incentives by 13% annually to $3.8 billion, reflecting both volume growth as well as strategic rebate bargaining maintaining exclusivity with significant issuers. This incentive dynamic, a near-term margin suppressor, plays a vital role in cementing Visa’s pipes into worldwide financial flows.

From an artificial intelligence integration perspective, Visa is finally catching up with competitors such as Stripe in terms of fraud detection and risk scoring. The acquisition of Featurespace extends Visa's expertise in adaptive behavioural analytics, supporting real-time defense against synthetic identity fraud and deepfake transaction spoofing. Contrary to their fintech competitors with independent models, Visa can implement these tools across an enormous data lake of verified transactions, improving model accuracy.

Customer acquisition is where Visa excels. Although fintech apps may win wallets, Visa controls the rails. The very embeddedness in bank issuer technologies and POS terminal arrangements makes Visa more difficult to rip and replace. With more than 4.7 billion Visa-branded cards outstanding, switch costs are not technical, they are behavioral. While Apple Pay captures tap-to-pay market share, Visa earns on each Apple Pay payment run over its underlying network.

Where Visa falls short on consumer brand recognition against PayPal or Square, it makes up with near-imperceptible omnipresence and infrastructure superiority.

.png)

Source: Capital one

Under The Hood: Margin Mechanics and Growth Engines

Visa's growth drivers become more diverse. The consumer payments pillar is still robust, with payments volume growing 9% YoY in Q1 FY25, but it's the non-card pillars where there's promise in the future. Value-added services and new payment streams are Visa's growthiest segments. The firm's $912 million in "other revenue," a growth of 32% YoY, indicates tokenization, risk products, as well as B2B payments are being monetized.

AI plays a pivotal role. After its purchase of Featurespace, Visa has directly incorporated AI models into fraud decisioning processes. The models enable Visa to provide real-time notifications with less than 50ms latency, a vital advantage in sustaining over 99% transaction acceptance rates. With ownership of data as well as the scoring engine, Visa can sell fraud prevention as a separate service, especially to its fintech partners who are working on thinner margins.

Financially, Visa's cost efficiency remains class-leading. Non-GAAP operating expenses were higher by 11% YoY, reaching $2.9 billion, mainly as a result of increased staff and G&A expenses. However, free cash flow was also strong, coming in at $5.1 billion, reflecting high margin increments. CapEx of $345 million reflects low reinvestment needs, with AI, security, and cloud infrastructure as priority areas of spending.

Profitability remains solid. Non-GAAP net income was 11% higher, to $5.5 billion, as non-GAAP EPS was 14% higher, to $2.75, helped by buybacks. The effective tax rate was a disciplined 17.7%. With $16.1 billion in liquidity and very little net leverage, there remains space to explore opportunistic M&A or advance shareholder returns.

Visa's internal funding of innovation as well as repaying capital manifests its dual mandate, defense through efficiency, offense through reinvestment. The balance sheet is strong: $12.4 billion of cash, $1.9 billion of short-term investments, and $19.9 billion of repaid capital in the last 12 months.

.png)

Source: Q1-FY25

Valuation anchors in a premium multiple world

Visa costs about 30.65x forward P/E and 24.59x EV/EBITDA, putting it near the higher end of payment industry groups. But this kind of multiple more accurately reflects Visa’s lasting competitive advantage, international reach, and higher margins. To put this into greater perspective, MasterCard’s multiple sits at 28x on a forward basis, and PayPal remains in depressed territory at 13x, reflecting structural issues.

Using a discounted cash flow (DCF) model with a 9% discount rate and assuming 6% growth in long-term free cash flow, we arrive at an intrinsic value of $305 a share, representing a 12% move from where it trades currently in the area of $270. It aligns with the comp analysis as well, where EV/Revenue multiples in the payments infrastructure group (e.g., Adyen, FIS, Global Payments) are averaging roughly 8–10x, and Visa's multiple of ~11x is explained by greater FCF margins.

What remains underestimated by the market is Visa's optionality. Margin expansion and multiple re-rating may become material if embedded flows and value-added services increase from 10% to 20% of revenue over 3–5 years. Particularly when international flows recover and AI monetization scales, Visa's forward PEG ratio of ~1.8x may prove to be attractive in retrospect.

That notwithstanding, support from valuation relies on maintaining top-line growth and robust share in the cross-border space, albeit still under pressure from regional schemes as well as local real-time payment schemes.

.png)

Source: Ycharts

Structural Headwinds in a Decentralizing World

The biggest threat to Visa's business model remains macro, not micro. Widespread adoption of national real-time payments systems such as Indian UPI or Brazilian Pix threatens interchange economics in the longer term. Regulators increasingly distrust card-based hegemony, particularly in Europe and Latin America, where local schemes gain traction. Visa's business model globally may suffer from margin compression if cross-border routing needs to shift to government-owned pipes.

There's also litigation on the horizon. The $27 million provision this quarter pertains to its ongoing interchange multidistrict litigation (MDL), a lawsuit that could still put pressure on Visa’s pricing ability if settlement terms call for structural concessions.

Then there's also the tech threat. While Visa's investing in tokenization and AI, challenger platforms are innovating more rapidly. Stripe's developer-focused approach and blockchains’ ability to build decentralized payment layers can, over the long term, shrink Visa's fee capture. Yet none of these threats suddenly materialize overnight.

Visa's institutional relationships, compliance record, and enormous fraud infrastructure mean it still is, and will continue to be, the default choice for high-value and high-trust flows. But complacency may deliver slippage if the company doesn't pre-empt disruptive change in transaction initiation, identity checking, or settlement finality. Visa continues to be a cornerstone holding in institutional portfolios targeting stable, high-margin exposure to worldwide digital payments. Its resiliency, AI transformation, and cross-border flywheel provide asymmetric upside, if management remains ahead of protocol-native disruption.