TSMC’s AI Moat With 90% Market Share

- TSMC controls over 90% of global 3nm and 5nm chip production, making it an irreplaceable supplier in AI and high-performance computing.

- High-performance computing (HPC) now accounts for 44% of revenue, up from 38% in 2022, driven by hyperscaler demand for custom AI chips.

- Priced at a forward P/E of ~18x and EV/EBITDA of ~10.5x, TSMC trades at a steep discount to AI peers despite superior execution.

- Taiwan exposure creates investor hesitation, yet TSMC’s $40B fab expansion in Arizona, Japan, and Germany aims to diversify operations.

Silicon Sovereignty: The Asymmetric Role of TSMC

TradingKey - Amid the global dash to build next-generation AI infrastructure, Taiwan Semiconductor Manufacturing Company or TSMC (TSM) is a little-appreciated, if vital, pillar of technological sovereignty. As the conventional wisdom is taking shape around Nvidia, Microsoft, and Alphabet as the prime beneficiaries of AI's trillion-dollar tide, the position of TSMC as the go-to facilitator—making nearly all the world's high-end chips—goes at a discount. In a world in which compute is king, however, TSMC is not only a supplier but a geopolitical fulcrum, with control of well over 90% of global 3nm and 5nm chip production. With supply chain resilience now a boardroom imperative, this positioning vests power well beyond its market capitalization.

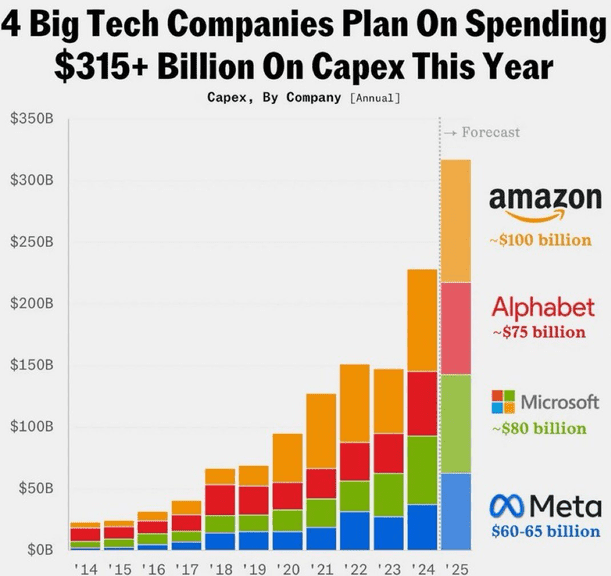

As the hyperscalers invest over $300 billion into AI data centers in 2025, the investment narrative increasingly tilts from software toward silicon. Custom chip designs such as Amazon’s Graviton, Meta’s MTIA, and Microsoft’s Maia all owe their embodiment to the fabs of TSMC. But the market still views TSMC with a cyclical lens—tied to smartphone and PC cycles—and can't see its structural mooring in AI, high-performance computing (HPC), and sovereign chip agendas. Here, we break the narrative down by analyzing the business model, the shifting client base, competitive dynamics, leverage, and asymmetry of valuation. In order to fully appreciate the depth of TSMC’s positioning in the AI industrial complex, these pillars must be fully understood.

Source: threads.net

Custom Chips and Foundry Wars:

The Crossroads of Competition The competitive dynamics bifurcate and speed up. Samsung Foundry and Intel’s Foundry Services (IFS) are positioning themselves to chip away at the market share of TSMC, particularly with the incentives of the EU Chips Act and the CHIPS Act. But the qualitative difference of execution persists. Samsung’s 3nm gate-all-around (GAA) process is still behind the performance-per-watt yields of TSMC, and the roadmap of Intel is still under the eye of execution, with IFS losing some high-profile customers recently. Even with subsidies, customers of the foundries prioritize technical reliability and supply chain reliability.

Custom chip momentum is a moat and a battleground. MTIA from Meta, Microsoft’s Azure Maia, and Google’s TPU v5 are all being made by TSMC. These chips are being designed internally by tech giants for the sole purpose of accelerating AI training and inference workloads, allowing hyperscalers to slash their reliance on the high-margin GPUs of Nvidia. But the production of these chips is still almost entirely with TSMC. In effect, as hyperscalers go vertical on their designs, they remain horizontal on the fab capabilities of TSMC. This paradox further entrenches the position of TSMC at the center of AI’s physical buildout.

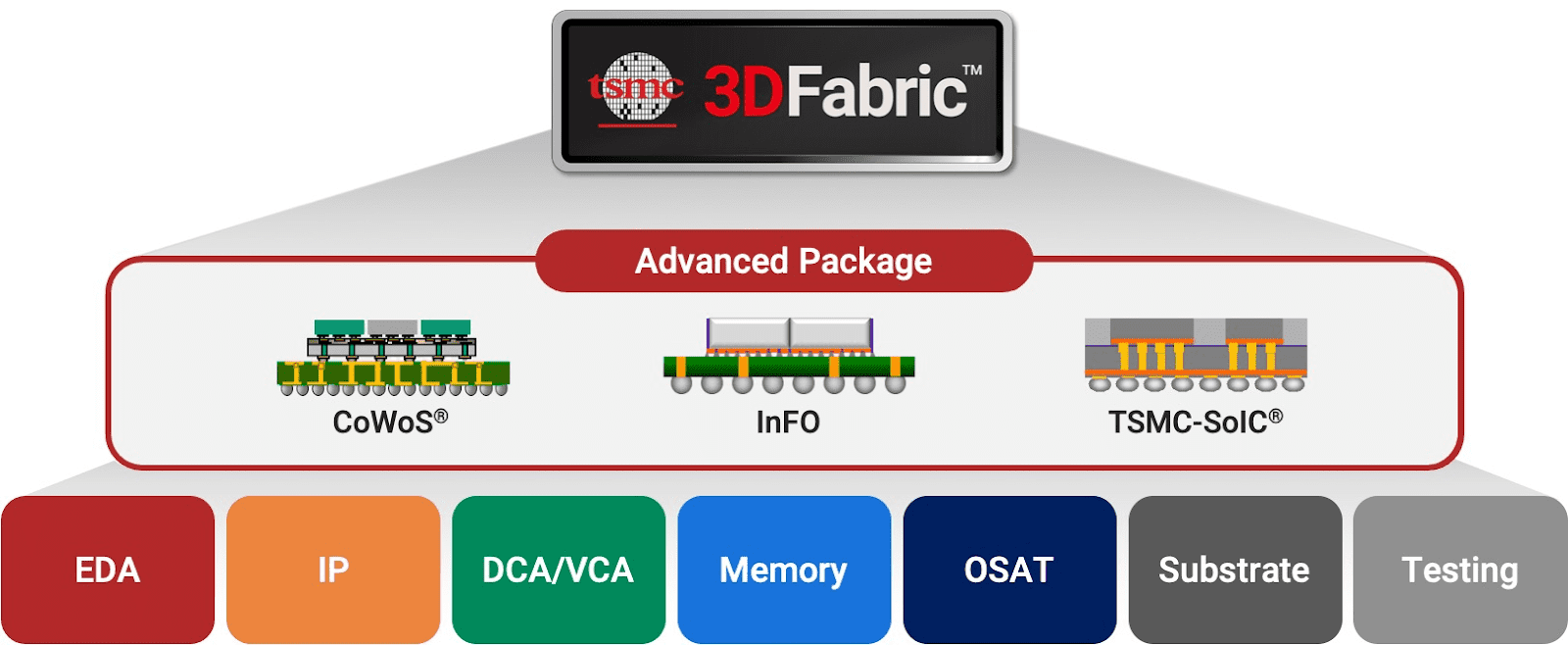

This creates a flywheel effect. As more and more firms design custom silicon, the function of TSMC shifts from volume manufacturing to value-added enablement. The manufacturing process expertise required for making low-power AI chips on 3nm nodes is non-trivial and years ahead of the competitors. Furthermore, the long-term relationships and ecosystem entrenchment—via its Open Innovation Platform (OIP)—of TSMC generate a developer network effect, which is hard for the competitors to replicate. The result is a flywheel effect of rising levels of innovation, customer lock-in, and scale economies.

Nonetheless, the potential for geopolitical disruption remains a wild card. With the fab concentration in Taiwan, the market is paying a geographic exposure risk premium on TSMC. Despite the fact that the firm is diversifying aggressively—$40B is being spent on new fabs in Arizona, Japan, and Germany—these will not be generating economic returns until 2027. Until then, the operational moat of TSMC is partially offset by the volatility of geopolitics. Investor attitudes remain tied up with the politics of Taiwan, no matter the strength of the execution.

Source: TSMC 3DFabric Alliance

TSMC's AI-based business model: Foundry Fortress

The revenue mix of TSMC is also strategically shifting. Smartphone chip demand remains a core pillar, but AI growth has brought strong growth from the high-performance computing (HPC) segment. HPC accounted for over 51% of the revenue for TSMC for 2024, up from 44% for 2023. The tailwind is underpinned by custom silicon partnerships with the likes of Apple, AMD, Nvidia, and Amazon, whose designs go hand-in-hand with the leading-edge process capabilities of TSMC. The shift toward purpose-built AI silicon is redefining chip economics for TSMC.

TSMC's strategy of manufacturing is positioned for success with the AI era. Unlike integrated device manufacturers such as Intel, TSMC only manufacturers, and this enables it to throw R&D and capital on the latest process nodes. In 2023, 5nm and 7nm nodes accounted for 59% of revenues of TSMC, with 3nm growing up to 6% by Q4 and is poised to grow beyond 20% by 2025. Scaling is being fueled by migration of customers for AI and HPC workloads, which demand power efficiency, high-transistor-density chips. The strength of the company lies with process repeatability and time-to-yield advantage, which enhances its market leadership.

The economic moat is also deepened by the fact that TSMC can produce at scale with unmatched yields. Q4 2024 operating margins were 49.0%, with gross margins of 59.0%-industry leading, but much better than the 40.4% of Intel and the 37.2% of Samsung for comparable quarters. The fabless customers of TSMC don't have switching costs due to the proprietary process design kits (PDKs) and the qualification tools the company works with their customers on. As such, TSMC is not only a supplier, but a co-architect of the AI chip design stack. The design enablement platforms of the company further create long-term ecosystem dependencies.

.png)

Source: Q4-Deck

Capex, Cost Curves, and Conviction Multiples

TSMC's fiscal engine still beats even with macro headwinds. In Q4 2024, net revenue grew 14.3% QoQ and 38.8% YoY, driven by a robust spike in 3nm shipments and AI-related orders. Net income grew 57% YoY, and return on equity (ROE) was a record 36.2%, demonstrating capital efficiency unmatched in the semiconductor sector. These results aren't one-off bounces—they're a structural step-up in demand for compute-dense nodes. Management commentary emphasizes order visibility and sustained utilization levels across advanced nodes.

CapEx remains a leading indicator of conviction. In 2023, TSMC invested NT$960 billion (~$30 billion USD), 70–80% of which was invested in advanced nodes (3nm/5nm/7nm). That percentage is a powerful indicator of customer commitment, as well as a calculated strategic pivot toward AI workloads. Compared with still-rationalizing cost structure at Intel, TSMC is ramping up with strong conviction of volume absorption from AI, automotive, and HPC markets. The company's internal estimates project AI-related demand growing at 50% CAGR up to 2027.

On a valuation basis, TSMC is priced at a forward P/E of ~18x and EV/EBITDA of ~10.5x—well below peers like Nvidia (>30x EV/EBITDA) with similar, if not superior, margins and return metrics. A DCF estimate with conservative assumptions (7.5% WACC, 5% long-term FCF growth, and 20% EBIT margin) calculates an intrinsic value of ~$160 per ADR, implying ~30% potential appreciation from here. Much of this discount is because of geopolitical, not operational execution or visibility of free cash flow. The risk-reward tradeoff here offers unusual asymmetric upside for large-cap tech.

Also, the low net debt and high free cash flow conversion of TSMC allow it the leeway to manage these geopolitical risks. With $38B of cash and equivalents and a 1.7% dividend yield, TSMC is not only a growth compounder but also a capital return vehicle—a rare combination for a high-CapEx industry. Financial strength makes it even more appealing as a core and satellite position for AI-focused portfolios.

.png)

Source: SEC-6K

Fragile Giants: Risks of Concentration in a Fragmenting World

While the size of TSMC is a strength, its customer and geographic concentration expose it to idiosyncrasies. In 2023, the top 10 customers accounted for 70% of total revenues, with Apple at 25%. The company is susceptible to procurement cycles, product delays, or strategic changes by a small group of hyperscalers. Export controls on Chinese AI firms can also dampen demand, particularly as TSMC stops shipping to U.S. Entity List entities. The balance of commercial opportunity and compliance is growing increasingly complex.

To this outlook, we can also add the geopolitical premium on Taiwan. Forced decoupling from Western consumers, or military provocation, is a non-zero tail event. Even with the encouraging plans for geographic diversification by TSMC, the strategic nature of advanced manufacturing—highly integrated with R&D centered on Taiwan—makes offshore replication difficult. Interdependencies of the supply chain add additional fragility to the best-planned contingencies.

From a supply chain perspective, the purchasing emphasis of TSMC on raw materials like silicon wafers and high-purity chemicals is also a source of danger. Natural disasters, trade barriers, or governmental instability in the source countries can disrupt manufacturing and increase the expense. As the complexity of extreme ultraviolet (EUV) lithography processes escalates, even minimal input disruptions can impact yields across a number of nodes. Supplier audits and contingency sourcing become mission-critical processes.

The final of the factors of fragility is human capital and knowledge systems. The tacit know-how of TSMC with regards to yield optimization, cycle time reduction, and defect control is embedded deeply in a team that is not easily replicable abroad. No matter how much TSMC spends on protocolized processes and automation, the organizational DNA is closely tied with Taiwan-based teams. Succession planning, skills transfer, and cultural coherence will determine long-term resilience. Conclusion TSMC is the behind-the-scenes backbone of the AI supercycle. Against near-term risks and geopolitical overhangs, its unmatched execution, capital discipline, and alignment with AI chip design ecosystems make it a linchpin of global compute infrastructure. As a play on the AI theme for investors beyond the headline AI names, it offers asymmetric potential with institutional-quality durability. Its contribution toward the future of intelligence is underestimated—until disruption proves otherwise.

Source: csis.org