Microsoft: The AI Power Move Wall Street Missed

- Microsoft’s AI revenue run rate exceeded $13B, growing 175% YoY, with Azure AI contributing 13 percentage points to Azure’s 31% YoY growth.

- GitHub Copilot saw over 1M signups within days of launch, reinforcing Microsoft's stronghold in AI-powered developer tools.

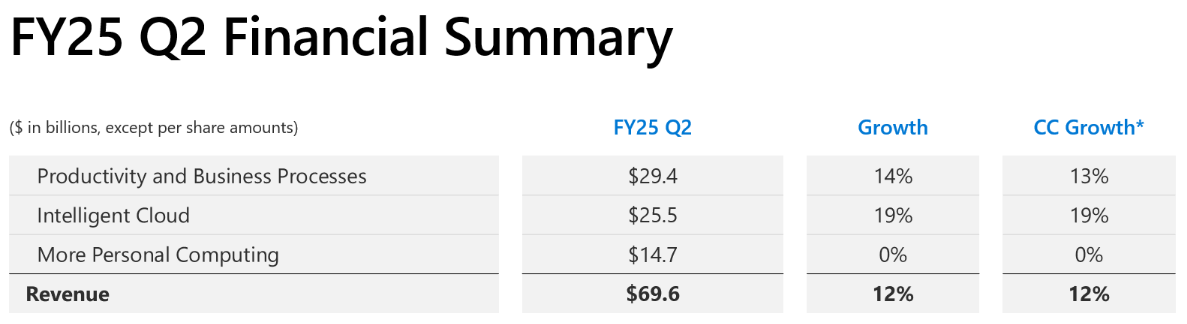

- Microsoft’s financials remain robust, with Q2 FY25 revenue at $69.6B (+12% YoY), operating income at $31.7B (+17%), and a 45% operating margin.

- Commercial bookings surged 67%, and Microsoft's $298B commercial RPO offers strong multi-year revenue visibility, with 40% expected to convert within a year.

AI in the Core: How Microsoft is Rewiring the Enterprise Stack

Microsoft's transition from software behemoth to AI-first worldwide platform is in full swing. Fiscal Q2 2025 results spoke volumes: AI is not an item in the experiment bucket anymore. It's the headliner. Azure, Microsoft's cloud infrastructure platform, saw 31% year-over-year revenue growth—a feat for a platform of its scale. What's even more insightful? Roughly 13 percentage points of that growth were directly credited to AI services.

At the forefront of this change is CEO Satya Nadella's strategic bet: pervading AI across every layer of Microsoft's stack—from infrastructure to productivity software to developer tools and vertical business applications. This isn't hype. This is monetization at scale. The AI revenue run rate exceeded $13 billion, growing 175% year over year. This isn't a tech revolution—it's a business model revolution.

Microsoft 365 Copilot, a generative AI assistant, is revolutionizing enterprise workflows. Novartis and Barclays are two early adopters that have licensed tens of thousands of seats, and usage intensity—how much users engage with the tool—grew over 60% quarter-over-quarter. On the developer front, GitHub Copilot is a game-changer. With over a million signups within days of availability in VS Code, the tool is rapidly becoming a vital part of modern software development pipelines.

What distinguishes Microsoft is not just the quality of its AI models, but its unmatched distribution. Azure AI Foundry, the company's platform for running and optimizing models, supports both proprietary (OpenAI) and open-source models like DeepSeek R1. The open-door approach allows developers and enterprises alike to tailor AI to their particular needs—all within the Azure ecosystem.

As this AI flywheel gathers speed, it creates self-reinforcing loops: more users generate more data, which feeds better models, which in turn speed more adoption. Microsoft isn't merely playing in the AI era—it's shaping it.

Source: Earnings Deck

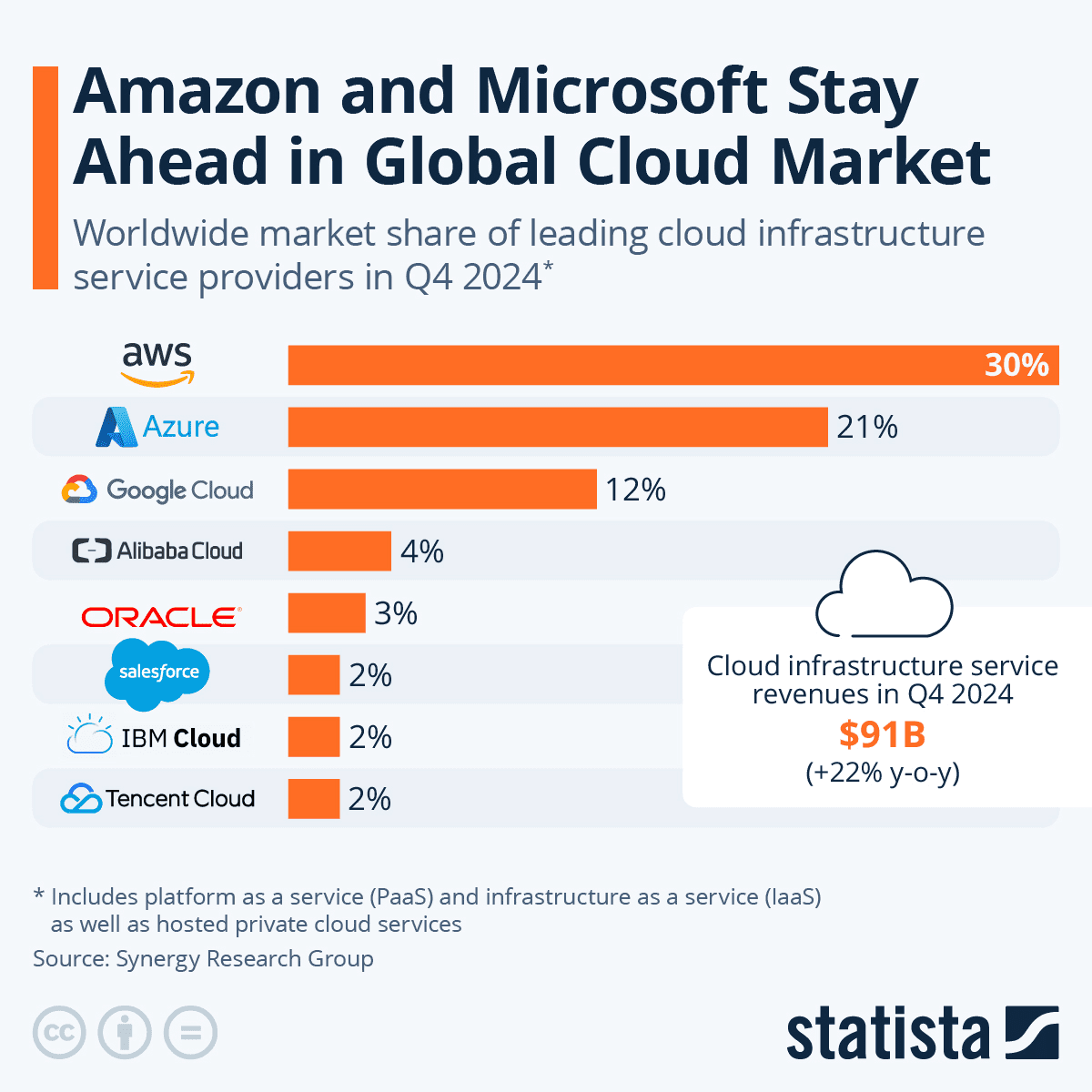

The Cloud Wars: Microsoft's Edge Over Amazon and Google

Microsoft isn't yet the largest cloud provider, but its strategic position is arguably the best. It is no longer a contest to determine who has the most data centers—it’s a contest to determine who can integrate cloud, AI, productivity, and developer tools into a single ecosystem. And that’s where Microsoft stands out.

Azure's 31% Q2 FY25 growth outpaced both AWS and Google Cloud Platform. But it is not just about numbers. Microsoft has created a flywheel effect by linking Azure in with the entire Microsoft suite—Microsoft 365, Dynamics, Power Platform, and LinkedIn. That bundling offers a compelling value proposition to enterprises: run your infrastructure, productivity, analytics, and AI tools all in one place, with common security, compliance, and support.

Google's Gemini models are gaining traction in the open-source world, and AWS is dominant in raw computing capacity. But Microsoft is the only one that has ownership of both the top layer (applications) and the bottom layer (infrastructure) of the cloud-AI stack. That end-to-end control enables it to build AI into workflows deeply, not as some add-on plug-in but as a native function.

Its exclusive hosting of OpenAI’s APIs further increases Microsoft’s moat. Anyone wishing to access GPT-4 or subsequent iterations must do so via Azure, which raises customer stickiness. Meanwhile, Microsoft's support for open-source models enables it to stay agile and future-proof. Irrespective of whether the future is closed models, open models, or hybrids, Microsoft will emerge victorious.

That same flexibility is reflected in its partnerships. Whether its SAP, Adobe, or Nvidia, Microsoft is not afraid to partner across ecosystems. That level of interoperability is perhaps increasingly valuable as enterprises attempt to avoid vendor lock-in and minimize concentration risk.

In short, Microsoft's cloud edge is not merely infrastructure. It is about orchestration—and right now, it is playing the long game better than anyone.

Source: Statista.com

Monetizing the AI Flywheel: Financial Firepower Behind the Vision

Underneath the flying AI story, Microsoft's financial discipline remains intact. The company posted $69.6 billion in Q2 FY25 revenue, a 12% year-over-year increase. Operating income rose 17% to $31.7 billion, and net income was $24.1 billion. Even more impressive is Microsoft's margin profile: 45% operating margin and 69% gross margin while investing in massive AI infrastructure build-outs.

Microsoft is growing in AI profitably—a feat not many can pull off. The company's quarterly operating free cash flow was $22.3 billion, and CapEx, while higher, remains productive. Microsoft’s CFO, Amy Hood, highlighted the company's emphasis on operational discipline, even amidst soaring demand.

Commercial bookings grew 67%, and commercial RPO was $298 billion, with 40% expected to convert to revenue in the next 12 months. This backlog level not only testifies to strong pipeline visibility but also to the reality that customers are committing to multi-year deals at scale—often with both cloud infrastructure and AI services.

Across Microsoft 365, Copilot, Dynamics 365, and LinkedIn Premium, we're seeing AI-driven growth in average revenue per user (ARPU). As an example, 40% of LinkedIn Premium subscribers are using AI-driven functionality to optimize profiles and job searches. GitHub has grown its developer base to over 150 million, 50% growth in the past two years, creating an enormous user base to upsell AI-native tools like Copilot.

And don't forget the leverage in gaming, with all-time high revenue Game Pass subscriptions. Microsoft is making more profitable digital content and platform revenue—again, AI is assisting in the form of personalization, game design, and cloud gaming optimization. In every segment, AI is not just an enabler, but a monetization lever. The company's balance sheet—with over $71 billion of cash and equivalents—provides it with the room to continue investing, acquiring, or defending its moat as and when necessary.

.png)

Source: Earnings Deck

The Valuation Premium: Justified Leadership or Irrational Exuberance?

Here's the catch: Microsoft's valuation is pricey—by just about any metric. MSFT trades at a forward P/E of 29.8x as of March 2025, almost 34% above the sector median. Its 10.6x EV/Sales multiple is over three times higher than most large-cap tech peers. Even on price-to-book and PEG basis, the company appears expensive. Dividend yield? A meager 0.8%—half the sector average.

And yet, investors just keep on buying. Why? Because Microsoft offers rare visibility. Unlike most high-growth tech plays, it combines rapid innovation with established profitability. Its AI revenue is not theoretical—it is already powering top-line growth, product breadth, and deal flow. That gives institutional buyers confidence to pay a premium, especially in a macro environment where quality, consistency, and cash flow are key.

.png)

Source: Nasdaq

Walking Through the Minefield: Key Risks Beneath the AI Halo

Microsoft's strategy is consistent, its execution all but flawless, and its position enviable. But no investment is without risk—and Microsoft's current trajectory has its share.

The most direct is geographic imbalance. U.S. business growth is booming, but international growth, particularly in Europe, remains uneven. With enterprise IT budgets tightening globally, especially in emerging markets, Microsoft might see slower growth overseas than in its U.S. home base.

There is also regulatory risk. Microsoft's exclusivity with OpenAI and its market-leading cloud presence have already attracted the attention of antitrust regulators. Europe has already spoken out against cloud concentration, and AI’s non-transparent model governance may invite further attention. Data privacy, algorithmic bias, and AI misuse—particularly in Copilot applications—are all potential flashpoints.

The AI arms race itself is becoming more competitive. Google, AWS, Meta, and open-source consortia are all accelerating. If Microsoft loses model leadership, or if OpenAI falters under the burden of controversy or competition, Azure could see customer churn, especially among developers for whom flexibility and performance are more important than brand alignment.

There's also concentration risk from a financial perspective. Microsoft's RPO levels today are encouraging—but also very dependent on mega-enterprise accounts. If economic uncertainty causes renewals to get pushed out or budgets to get reprioritized, forward visibility can evaporate quickly. And lastly, the present valuation does not allow for any mistakes. One weak quarter, and the market will aggressively reprice. However, none of these dangers negate the overall thesis. They simply introduce prudent caution to what is otherwise a very bullish narrative.

.png)

Source: Earnings Deck

Conclusion: Leading the AI Renaissance, but Priced Like It Already Won

Microsoft is firing on all cylinders—operational, financial, and strategic. It is attacking the multi-layered AI strategy with clarity and precision, inserting itself further into enterprise workflows by the quarter. But with expectations in the stratosphere and a valuation to match, investors now need to ask not only if Microsoft will win the AI race—but at what price? For long-term investors, the AI flywheel is just beginning. For valuation-conscious investors, it may be prudent to wait for a more attractive entry point. In either case, one thing is clear: Microsoft isn't merely keeping pace with the future—it's actively building it.