2025 S&P 500 Forecasts on Wall Street: Why Are Analysts Divided?

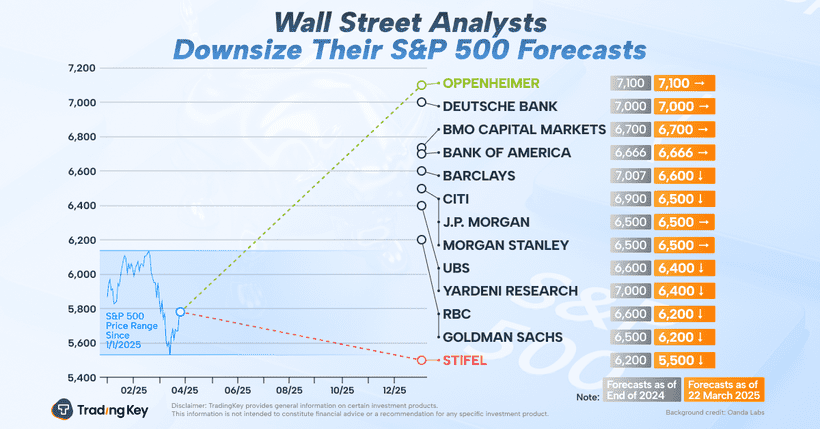

TradingKey - Wall Street's forecasts for the S&P 500 index in 2025 show a rare split: the lowest target from Stifel stands at 5,500 points, while Oppenheimer's highest target is 7,100 points, marking a significant 20% disparity. This is the biggest difference in annual outlooks among investment banks since 2015.

The divide reflects not only concerns about macroeconomic scenarios but also highlights three key tensions: the uneven impact of Trump-era policies across sectors, whether disruptors like OpenAI and DeepSeek can sustain the profit growth narrative of the "Magnificent Seven," and differing expectations regarding interest rate trends.

Bearish Arguments: Policy Risks and Earnings Concerns

Barclays and Stifel are part of the bearish camp.

Tariffs continue to be a focal point for analysts. According to a Bloomberg report from February 2025, about 50% of the factories for S&P 500 companies are located outside the U.S. The industrial, consumer goods, and tech sectors have the highest concentrations of overseas facilities. The report estimates that if the U.S. imposes a comprehensive tariff of 10% to 20% on imports, EPS for S&P 500 can be reduced by 1.6% to 9%, depending on the concentration of their overseas supply chains and the ability to pass on costs.

In the latest earnings season, mentions of tariffs during U.S. corporate earnings calls reached record levels. Over the past five years, similar discussions had never broken the 100-mention mark. The industrials and consumer discretionary sectors have discussed tariff impacts the most, as they face significant cost increases.

Venu Krishna from Barclays argues that with trade policy risks, alongside a weak manufacturing PMI, factories are trying to preemptively deal with tariff impacts. Moreover, uncertainties from canceled government contracts add to the volatility. With decreasing consumer confidence, slowing economic growth, rising inflation, and tariff effects, the market faces considerable headwinds.

Concerns over an "AI bubble" have also led to skepticism about the sustainability of investments by North American tech giants. Tech stocks have taken a hit recently, prompting doubts about the U.S.'s leading position in AI.

Notable bear and former Morgan Stanley strategist Marko Kolanovic stated that the unprecedented imbalance between the top ten stocks and the rest of the market cannot go on forever; a cyclical downturn might occur to correct inflated valuations.

Bullish Perspective: Liquidity and Earnings Resilience

On the flip side, the optimistic camp, led by DEUTSCHE BANK and Goldman Sachs, highlights several key factors.

Expectations surrounding Trump's tax cuts combined with potential Federal Reserve rate cuts could enhance corporate cash flow and fuel a wave of stock buybacks. The Trump administration plans to lower the federal corporate tax rate from 21% to 18% and broaden R&D tax credits, which could boost after-tax profits in sectors like technology and manufacturing (like Tesla and Boeing) by 5% to 8%.

Markets are currently anticipating two rate cuts this year. During the "tax cut + rate hike" period from 2016 to 2018, stock buybacks in the S&P 500 grew at an average rate of 20%. If the cycle shifts to "tax cut + rate cut," the growth rate of buybacks could exceed 25%.

The monetization of AI applications is also expected to support U.S. corporate earnings. Technologies like Microsoft's Copilot and improved advertising algorithms from Meta are accelerating revenue generation in the AI space.

The Middle Ground for Investors

Here are the five defensive stocks.

Procter & Gamble (PG): Resilient consumer brands with strong pricing power and low tariff exposure.

NextEra Energy (NEE): Largest U.S. renewable energy operator positioned to benefit from rising electricity demand and supportive subsidies.

Johnson & Johnson (JNJ): Diverse healthcare segments providing low cash flow volatility and a robust drug pipeline.

Lockheed Martin (LMT): Strong revenue visibility backed by rising defense spending and strategic lobbying efforts.

Newmont Corporation (NEM): Rising gold prices and effective cost management position it well as a preferred hedge.