[IN-DEPTH ANALYSIS] MicroStrategy (MSTR): The Core Strategy You Should Know about When Investing in Bitcoin

Source: TradingView

Key Points

- MicroStrategy, originally an enterprise data analysis software company, has now transformed to hold a large amount of Bitcoin, and its stock price is highly related to the Bitcoin price.

- MicroStrategy buys Bitcoin with borrowed money. If Bitcoin soars, stock profits multiply; if it crashes, debt risks explode.

- Currently, the premium of the stock price over the Bitcoin value is relatively low. If the Bitcoin price rises, the stock price may rebound by 30% and rise above $400 per share.

Overview

MicroStrategy (MSTR) is a globally recognized technology company with a dual focus on enterprise analytics and cryptocurrency investment. Originally established in 1989 as a business intelligence (BI) software provider, the company underwent a transformative shift in 2020, leveraging its financial acumen to become the world’s largest publicly traded corporate holder of Bitcoin. As of March 2025, its Bitcoin holdings have exceeded 490,000 coins, with an average cost of approximately $62,500 per coin. The total value is over $40 billion, accounting for more than 90% of the company's total assets. MicroStrategy has positioned itself as a key bridge between traditional financial markets and the digital asset economy. This strategy positions MSTR as the largest corporate holder of Bitcoin, driven by its "Digital Manhattan Strategy" to maximize shareholder value through long-term Bitcoin appreciation.

Business Model : A Tale of Two Worlds

1) Traditional BI Business

Once a dominant force in enterprise data analytics, MSTR’s on-premise BI solutions have struggled to adapt to the cloud-first era. According to Gartner, cloud-based BI tools accounted for 68% of global market share in 2024, yet MSTR’s legacy software revenue remains 40% of total sales, plagued by high maintenance costs and slower innovation compared to rivals like Tableau and Power BI. The company's income statement exhibits the dual characteristics of the contraction of its traditional BI business and the acceleration of its cloud transformation.

BI Product Support: The revenue decreased to $61 million in Q3 2024, a year-on-year decline of 8.7%, and there has been negative growth for seven consecutive quarters. This reflects that its on-premise software business is facing the issues of customer churn and price pressure. Mainly, cloud-native competitors such as Tableau and Power BI are seizing the market with lower costs, and its traditional licensing model finds it difficult to meet the needs of enterprise digital transformation.

Cloud Subscription Services: The revenue increased to $27.8 million in Q3 2024, a year-on-year growth of 32.5%. Although the growth rate has slightly slowed down compared with last year, it remains at a high level. This indicates that the company has attracted new customers through the "multi-cloud strategy" (supporting AWS, Azure, and GCP) and embedded analytics solutions (such as the cooperation with Snowflake). However, the net expansion rate in Q3 has dropped below the average level of the SaaS industry, and the company is facing the risk of fluctuations in customer renewal rates.

Revenue/Period | 30-Jun-23 | 30-Sep-23 | 31-Dec-23 | 31-Mar-24 | 30-Jun-24 | 30-Sep-24 |

Product Support | 66.08M | 66.86M | 65.47M | 62.69M | 61.74M | 61.02M |

Product Support Growth | -0.7% | 1.3% | -2.1% | -4.3% | -6.6% | -8.7% |

Subscription Services | 19.88M | 20.97M | 21.52M | 22.97M | 24.08M | 27.80M |

Subscription Services Growth | 41.8% | 27.8% | 23.2% | 22.1% | 21.1% | 32.6% |

Product Licenses | 13.65M | 17.58M | 19.13M | 16.66M | 16.34M | 16.17M |

Product Licenses Growth | -36.3% | -14.9% | -7.5% | -17.6% | 19.7% | -8.0% |

Source: TradingKey, SEC Filings

2) Bitcoin Investment Strategy

Since MicroStrategy launched its Bitcoin purchase program in August 2020, after its first purchase of 21,000 Bitcoins worth $250 million in 2020, by 2024, its cumulative Bitcoin holdings accounted for 2.3% of the global Bitcoin supply. Leveraging the high liquidity of the U.S. stock market, the company has raised funds by issuing premium stocks and bonds, hoarding Bitcoin as an "anti-inflation strategic asset," and forming a positive cycle of "financing - buying Bitcoin - rising stock price" through market value management. In the future, it plans to continue raising funds through the issuance of preferred stocks and additional share offerings via the At-the-Market (ATM) program. Its buying rhythm shows the characteristics of "accelerating purchases in bull markets and slowing down in bear markets." The company's goal is to purchase nearly 600,000 Bitcoins within the next three years to further solidify its position as a "Bitcoin bank."

.jpg)

Source:MicroStrategy

MicroStrategy's act of financing to buy Bitcoin assets has significantly changed the balance sheet. In terms of the accounting treatment of Bitcoin investments, the fluctuations of these assets are not directly reflected in the income statement but are instead manifested in the balance sheet. Bitcoin assets are classified as "other long-term assets," leading to a substantial increase. For example, by the end of 2024, the book value of the Bitcoins held by the company was approximately $23.9 billion, while calculated at the market price, it was about $41.79 billion, accounting for 92% of the company's total book assets.

After launching the low-interest convertible bond financing in 2020, the company's long-term debt increased from $0 in 2020 to $7.2 billion in Q4 2024. Most of these were low-cost debt instruments (convertible bonds with an interest rate of 0% - 0.75%), and the debt-to-Bitcoin market value ratio was maintained at 18.9%. However, while this strategy enables MicroStrategy to realize asset appreciation when the Bitcoin price rises, it also exposes the company to the risks brought about by high leverage. Especially when the Bitcoin price drops, it may trigger significant debt pressure and impairment losses.

Period(mn) | Q4 2022 | Q1 2023 | Q2 2023 | Q3 2023 | Q4 2023 | Q1 2024 | Q2 2024 | Q3 2024 | Q4 2024 |

Other Long-Term Assets | 1,847 | 2,023 | 2,345 | 2,474 | 3,634 | 5,103 | 5,726 | 6,897 | 23,930 |

Long-Term Debt | 2,379 | 2,176 | 2,178 | 2,180 | 2,182 | 3,559 | 3,703 | 4,212 | 7,191 |

Additional Paid-In Capital | 1,841 | 2,206 | 2,559 | 2,726 | 3,958 | 4,248 | 4,785 | 6,060 | 20,412 |

Shareholders' Equity | -383.1 | 443.21 | 819.12 | 840.4 | 2,165 | 2,400 | 2,835 | 3,774 | 18,230 |

Source: TradingKey, SEC Filings

MicroStrategy has raised funds by issuing new stocks and convertible bonds, which has significantly increased its share capital and additional paid-in capital while diluting the equity of existing shareholders. However, the rise in the Bitcoin price has increased the Bitcoin content per share, offsetting the dilution effect. At the same time, the accounting treatment rules for Bitcoin have led to the continuous negative retained earnings because impairment losses are recorded in the income statement, but the appreciation of fair value cannot be recognized,. These operations have not only magnified the leverage effect of Bitcoin holdings on shareholders' equity but also intensified equity dilution and financial risks.

2025 Bitcoin Outlook: Catalysts and Risks

The Bitcoin market in 2025 presents a promising but volatile outlook. On one hand, the massive influx of institutional investors and the widespread adoption of Bitcoin ETFs provide strong upward momentum for the price of Bitcoin. Additionally, macroeconomic factors such as rising inflation expectations and falling real yields have further solidified Bitcoin's position as a hedging tool.

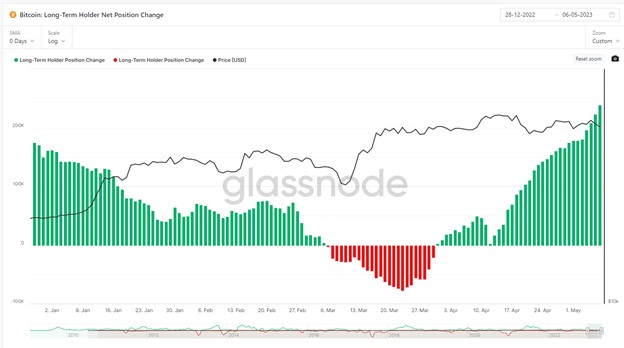

After the halving cycle, Bitcoin holdings and capital flows have shown a trend of concentration. Data from Glassnode reveals that addresses holding Bitcoin for more than one year account for 68%, and long-term holders make up 54%. This contraction in supply and the accumulation of tokens form the foundation for upward price movement. In terms of ETF holdings, three major products, BlackRock's IBIT, Fidelity's FBTC, and Grayscale's GBTC, together command 85% of the market share. As of March, the cumulative net inflow into Bitcoin ETFs has exceeded $50 billion. Sovereign funds (such as the Norwegian Government Pension Fund) and hedge funds, which hold Bitcoin indirectly through ETFs, have extended their holding periods to over six months, reflecting a long-term allocation preference.

Source:Glassnode

Against the backdrop of the dilution of fiat currency credibility and the intensification of geopolitical conflicts, the expected cryptocurrency-friendly policies of the Trump administration (such as the commitment to establish a strategic Bitcoin reserve and relax regulations on cryptocurrency companies) have boosted market sentiment. In 2025, with the halving effect resonating with the global central banks' interest rate cuts, the price of Bitcoin against the US dollar is still expected to rebound above $100,000.

Why Choose MSTR?

For investors who are bullish on Bitcoin, there are more than three investment options available, including directly purchasing Bitcoin spot, investing in Bitcoin Exchange-Traded Funds (ETFs), and buying the stocks of companies that hold Bitcoin. Each option corresponds to different investment costs, technical thresholds, and regulatory environments. For individual investors, the stock of MSTR remains an investment tool with low cost and high elasticity.

1) Choose Bitcoin Spot, ETF, or Stock?

Investors who directly hold Bitcoin through spot trading have the lowest cost. They can also transfer, trade, or make long-term investments, etc. Bitcoin transactions are recorded on the blockchain, which is completely transparent and immutable. However, investors need to manage private keys and wallets, and there is a risk of theft or loss. The long-term holding cost is the lowest, requiring only an initial transaction fee of about 0.1% - 0.2%.

Bitcoin spot ETFs are strictly regulated and protected, with high security and good trading liquidity, making it convenient for investors to trade quickly. However, long-term holding will be eroded by management fees (annualized rate of 0.2% - 0.8%), and the general income tax is usually relatively high for the dividends from the positions.

The advantage of holding Bitcoin through stocks lies in the leverage effect and the deferral of capital gains tax. When the price of Bitcoin rises, the stock price has higher elasticity, and the volatility is 1.5 - 2 times that of Bitcoin. When the price falls, there is also an additional risk of debt liquidation. Holding stocks incurs specific transaction and implicit financing costs, and the long-term holding cost is slightly higher than that of ETFs.

Investment | Spot | ETF | Stock |

Annualized Cost | 0% | 0.2% - 0.8% | 0.75% + volatility |

Technical Threshold | High (private key management) | Low (stock account) | Medium (fundamental analysis) |

Leverage Efficiency | None | None | 1.2x - 1.8x |

Tax Advantage | None | Partial deferral | Significant (tax deferral) |

Suitable Scenarios | Long - term holding | Medium - to - short - term allocation | Aggressive speculation |

Source: Tradingkey

2) Pick MicroStrategy, Coinbase or Marathon Digital?

If you directly participate in Bitcoin investment through stocks, the investment value and risks of related stocks still vary. MicroStrategy holds Bitcoin through debt financing and has the largest holding quantity. Its stock price is highly correlated with the Bitcoin price.

Coinbase and Robinhood are Bitcoin trading platforms, and their trading volumes are positively correlated with the Bitcoin price, but the quantity of Bitcoin held by the companies themselves is relatively small. Among them, Coinbase has a large-scale institutional customer custody business, while Robinhood has a higher participation rate of retail investors.

Marathon Digital is a Bitcoin mining producer, and its profitability depends on the difference between the Bitcoin price and the mining cost. When both the computing power expansion and the Bitcoin price increase occur simultaneously, it has an obvious leverage effect, but it is adversely affected by the fluctuations in energy costs and the intensified competition in computing power after the halving.

Indicator | MSTR | MARA | Coinbase | Robinhood |

Business Model | Bitcoin Holding (Corporate Strategic Reserve) | Bitcoin Mining | Trading Platform (Including Derivative Services Such as Custody and Staking) | Brokerage Service (Zero Commission Model for Attracting Traffic) |

Holding Quantity | 499,226 coins (accounting for 2.38% of the circulating quantity) | 46,374 coins | 9,363 coins (the company's own holding quantity, excluding the assets of custody users) | Not Disclosed |

Correlation Coefficient | Above 0.85 | Between 0.7 and 0.75 | Between 0.65 and 0.7 | 0.6 |

Leverage Attribute | 1.7 times (Market Value/BTC Net Value) | 1.2 times | None | None |

Financial Health | Low Debt (29%, but the debt cost is only 0.75%) | Low Debt (41%) | Medium Debt (55%, mainly from user deposits and transaction settlement funds) | High Debt (70%, zero commission leads to cash flow pressure) |

Risk Level | Bitcoin Pledge Liquidation Risk | Sensitivity to Energy and Halving Cycle | Regulatory Review and Trading Volume Fluctuation | Trading Volume Fluctuation |

Source: Tradingkey

Valuation in Terms of Bitcoin

If we conduct a valuation from the perspective of the traditional BI business and the income statement, we will find the value of this segment is negligible. When we look at the balance sheet of MicroStrategy in Terms of Bitcoin, the value fluctuations of Bitcoin holdings will directly determine the total asset scale. The amount of long-term debt (such as convertible bonds) is fixed, and when denominated in Bitcoin, its value fluctuates inversely with the BTC/USD exchange rate. In the fourth quarter of 2024, MicroStrategy's total debt ratio was 29.5%, but when converted based on the price of the Bitcoin it held, it was only 18.9%. If the price of BTC drops to $50,000, the quantity of BTC required to repay the debt will increase by 66%, and the company's liquidity risk will increase. Since MSTR's debt is not directly guaranteed by Bitcoin pledges, the company may handle the pressure of selling its Bitcoin holdings or diluting its equity under debt pressure.

Source: MSTR-tracker

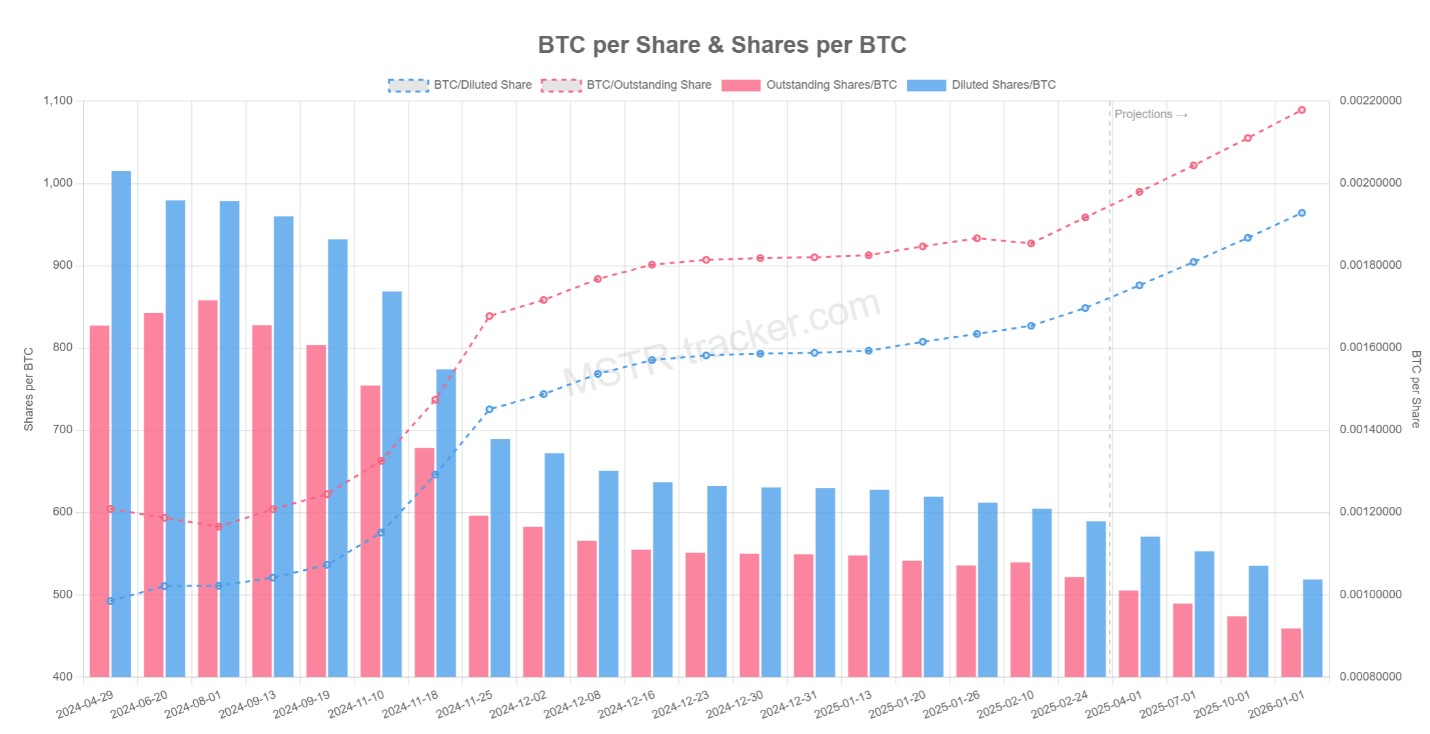

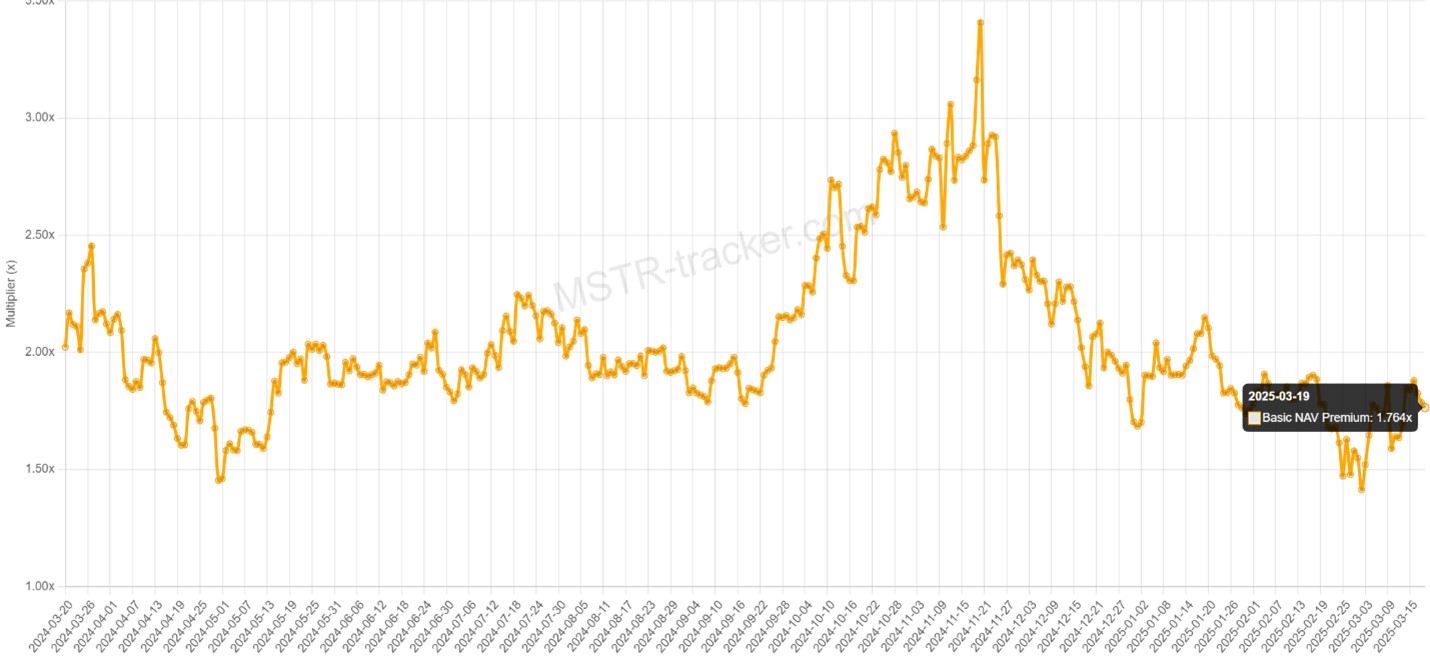

From the perspective of Bitcoin standard, shareholders' equity can directly reflect the net amount of Bitcoin held by the company. As of the fourth quarter of 2024, MSTR had approximately 0.0019 BTC per share. This means that at the current price of $83,000 per Bitcoin, the implied value per share is only $160. Moreover, previously, the premium rate of MSTR's market value over the net value of Bitcoin was as high as 70%. This indicates that the market still has a positive outlook on the company's development prospects and is willing to continuously pay a premium. However, as can be seen from the chart below, the premium rate of MSTR's market value relative to the net value of its Bitcoin holdings is at the 15% quantile of its historical lows. This may imply that if the Bitcoin price remains stable, MSTR's valuation will have strong support. If the Bitcoin price returns above $100,000 this year, then MSTR's stock price is expected to rebound by 30% and rise above $400 per share.

Source: MSTR-tracker