[IN-DEPTH ANALYSIS] Affirm: Will the End of Partnership with Walmart Impact Its Fundamentals?

Source: TradingView

Key Takeaways

- Walmart Partnership Impact: Walmart’s shift to Klarna in March 2025 ends its exclusive BNPL deal with Affirm. Though only 2% of operating revenue, it may dent Affirm’s reputation and GMV by ~5% short-term, but fundamentals remain largely intact due to diversified revenue streams.

- Revenue Diversification: Affirm’s income from interest ($1.204B, 76% growth in 2024), merchant fees ($675M, 33% growth), loan sales ($197M), virtual cards ($151M), and servicing fees ($95.48M) showcases resilience despite the Walmart loss.

- Industry Position: Affirm holds a 7% global BNPL share (possibly 33% in the U.S.), trailing Klarna (29%). BNPL’s market is growing (9% CAGR, $449.4B by 2027), yet remains <1% of global spending.

- Competitive Edge: Strengths in tech (AI-driven risk control, 2.4% delinquency rate) and partnerships (Amazon, Shopify) bolster Affirm’s position despite rising competition.

- Growth Concerns: GMV growth slowed to 30% in 2024, user growth to <20%, and AOV declined, signaling market saturation and competition pressures. Macro uncertainties add risk.

- Financial Outlook: With a 27% profit margin, $22.6B liquidity, and expected profitability by Q4 2025, Affirm is solid, though Walmart’s exit and competition impact its target price at $43/share.

1. Company Overview

Affirm is a trailblazing "Buy Now, Pay Later" (BNPL) fintech leader, empowering consumers to enjoy flexible installment payments on renowned retail platforms like Amazon, Shopify, and Target. Through partnerships with iconic brands such as Best Buy and Adidas, as well as payment giants like Stripe and Adyen, Affirm delivers transparent payment solutions to over 21 million users and 335,000 merchants, cement its position at the forefront of the BNPL industry.

2. Industry Positioning

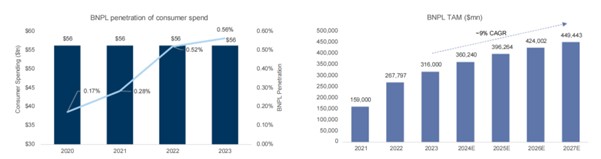

The Buy Now, Pay Later (BNPL) industry has grown rapidly, fueled by e-commerce expansion, digital wallet adoption, and demand for flexible payments among Millennials and Gen Z. According to Worldpay, the BNPL market is projected to grow at a CAGR of approximately 9% from 2021 to 2027, with its total market size expected to reach $449.4 billion by 2027. BNPL penetration rose from 0.17% of global consumer spending in 2020 to 0.56% in 2023, but it still accounts for less than 1% of global consumer expenditure, remaining a niche in the payments market despite significant growth potential.

Source: Affirm, Goldman Sachs, Worldpay

3. Competitive Analysis of Affirm in the BNPL Industry

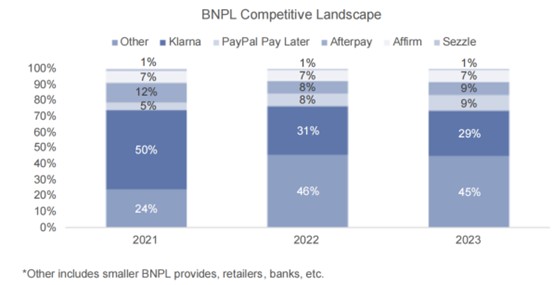

The Buy Now, Pay Later (BNPL) model allows consumers to pay in installments with little to no interest via e-commerce or POS systems. Affirm competes with traditional financial institutions and fintechs like Klarna, Afterpay, and PayPal, as well as Visa and Mastercard. In Q2 2025, Affirm’s GMV reached $10.1 billion (up 35% YoY), with 21 million active users (up 19% YoY). It holds a 7% global market share, potentially 33% in the U.S.

Klarna

Klarna's share of the global BNPL market dropped from 50% in 2021 to 29% in 2023, but it remains a leader with a $28.6 billion GMV and 36 million active users in its latest quarter. Its strength stems from robust expansion in Europe and the U.S., further solidified in March 2025 by replacing Affirm as Walmart’s exclusive BNPL provider, offering 3- to 36-month loans via OnePay. This partnership strengthens Klarna’s U.S. presence and boosts its IPO prospects.

Afterpay

Afterpay, acquired by Block in 2021, held a 9% share of global BNPL GMV in 2023, up from 8% in 2022. Since its acquisition by Block in 2021, Afterpay has faced integration challenges, and its profitability remains uncertain, limiting its short-term impact on the market landscape.

PayPal

PayPal’s “Pay in 4” holds a 9% global BNPL market share in 2023, leveraging its large user base and payment network. While offering four installments over six weeks with a six-month interest-free option, it trails behind Affirm and Klarna in focus, as BNPL isn’t its core business. Competition from specialized BNPL providers may limit its growth.

Other Competitors

In 2023, the "others" category, including smaller BNPL providers like Zip, retailers, and traditional financial institutions such as Visa and Mastercard, comprised 45% of the global BNPL market. Zip, operating in Australia and the U.S., lags behind Affirm and Klarna due to its late U.S. entry. Visa and Mastercard have introduced "Visa Installments" and "Mastercard Installments," using their established networks to compete with pure BNPL firms. The fragmented market offers opportunities for newcomers but intensifies competition.

Source: Goldman Sachs

4. How Affirm Makes Money

Affirm’s revenue streams are notably diversified, reflecting its robust business expansion capabilities within the fintech sector. Specifically, Affirm derives its income from several key areas: interest income, merchant fees, loan sales, virtual card services, and loan servicing fees.

Source: Affirm, TradingKey

Interest Income

Affirm’s primary revenue source is interest income from consumer installment loans offered through its Buy Now, Pay Later (BNPL) service, charging interest based on loan terms and amounts.

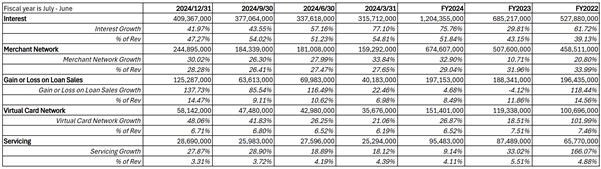

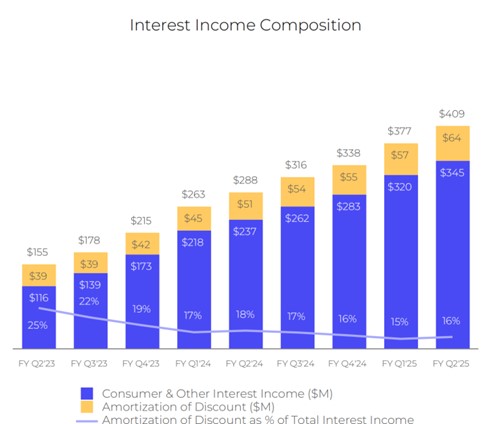

In fiscal year 2024, this segment generated $1.204 billion, up 76% from $685 million in 2023, reflecting robust growth. However, quarterly data reveals a slowdown, with interest income’s share of total revenue falling from 54.81% in Q1 to 47.27% in Q4, and growth rates dropping from 77.1% to 42%, possibly due to lower interest rates. Specifically, Affirm’s interest income consists of two main components:

- Consumer and other interest income: Interest directly from consumer installment loans.

- Loan discount amortization income: Accounting-related income tied to loans.

The slowdown in interest income growth is partly due to weak growth in loan discount amortization income. Analysis suggests Affirm may have strategically increased the proportion of interest-bearing loans, reducing reliance on loan discount amortization income. This adjustment may be linked to adapting to macroeconomic changes and optimizing revenue structure.

Source: Affirm

Merchant Fees

Affirm’s second-largest revenue source is fees charged to merchants. Merchants pay a percentage of transaction fees (merchant discount rate, MDR) to use Affirm’s BNPL service, attracting more consumers and boosting sales conversion rates.

In fiscal year 2024, the merchant network segment generated $675 million in revenue, up 33% from $508 million in fiscal year 2023. This growth was driven by:

- A 21% increase in active merchants.

- A 25% increase in high-value merchants, with their share rising from 39% to 40.36%.

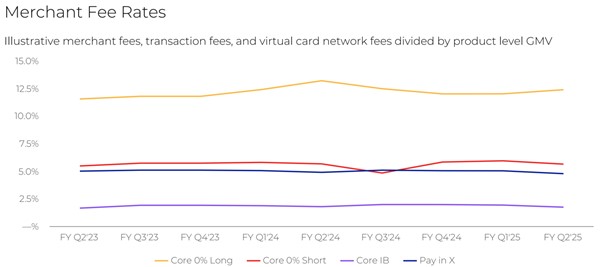

This trend highlights the significant success of Affirm’s partnerships with e-commerce giants like Amazon and Shopify. The merchant network segment’s revenue share remained stable between 26.41% and 28.28%, with minimal growth fluctuations, indicating its reliability. This stability stems from Affirm’s continuous adjustments to its merchant fee strategy. For example:

- Long-term zero-interest loans (Core 0% Long) have the highest MDR, around 12.5%-13%, due to higher risk.

- Interest-bearing loans (Core IB) have the lowest MDR, around 2.5%-2%, as they rely more on consumer interest income.

These dynamic adjustments show Affirm’s efforts to balance risk and merchant appeal. By optimizing the MDR structure, Affirm has enhanced its market competitiveness.

Source: Affirm

Source: Affirm

Loan Sales and Servicing Fees

Affirm earns revenue by selling loan portions to third-party investors, profiting from the difference between sale price and book value, and collecting servicing fees on managed loans post-sale. This model not only transfers loan risk to investors, freeing up capital for new loans, but also provides a steady cash flow source.

In fiscal 2024, loan sales revenue rose 4.68% to $197 million from $188 million in 2023, reversing a prior decline. Quarterly results varied, with Q4 hitting $125 million (up 137.73% YoY), comprising 14.47% of total revenue, compared to Q1’s 6.98%. This strong growth was driven by:

- Active capital markets in 2024, creating a favorable environment for loan sales.

- New market expansions, such as the UK.

- A significant increase in zero-interest installment loan users, expanding business scale.

The servicing segment generated $95.48 million in fiscal year 2024, up 9.14% from 2023. Although this segment’s revenue growth is stable, its share of total revenue ranges between 3.31% and 4.39%, making its overall contribution relatively limited.

Virtual Card Services

Affirm earns transaction processing and network fees through its virtual card product. The virtual card network segment generated $151 million in fiscal year 2024, a 27% increase from $119 million in 2023. Its share of total revenue remained stable between 6.19% and 6.80%, with Q4 growth rising to 48.06%.

5. Competitive Advaneage of Affirm

Technological Innovation, Enhanced Experience, Robust Risk Control

Affirm prioritizes transparency, displaying total costs and installment amounts upfront without hidden fees or high interest.

It uses AI and data analytics to assess creditworthiness quickly, bypassing traditional credit scores, which speeds up approvals and aids users with limited credit history.

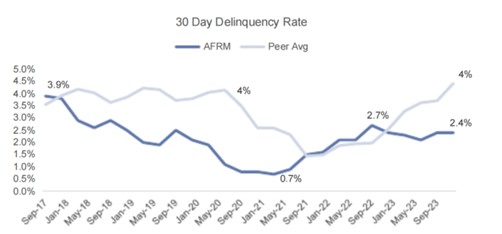

By analyzing purchasing behavior and financial data through data analytics and machine learning, Affirm tailors credit risk evaluations for short-term loans (3-12 months), reducing default risk compared to long-term mortgages (15-30 years) and enabling timely credit policy adjustments based on market changes. Its 30-day delinquency rate fell from 3.9% in 2017 to 2.4% in 2023, below industry averages, showcasing its tech-driven default management.

Source: Goldman Sachs

Strong Distribution Network and Diversified Asset Pool

Affirm has significantly optimized its market presence and consumer reach through strategic partnerships with major retailers and e-commerce platforms like Amazon, Peloton, and Shopify, integrating into high-traffic e-commerce platforms to drive adoption.

Moreover, Affirm’s loan portfolio is diversely distributed across industries like electronics, furniture, and apparel, reducing reliance on any single market and bolstering resilience against fluctuations.

Source: Affirm

6. Expectations and Concerns

Promising Highlights

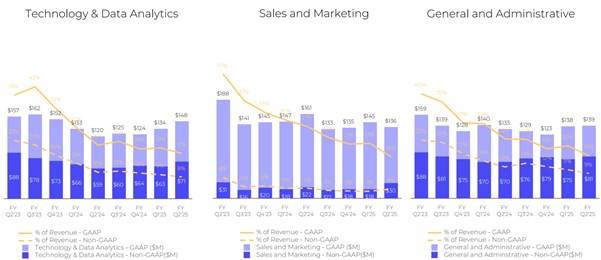

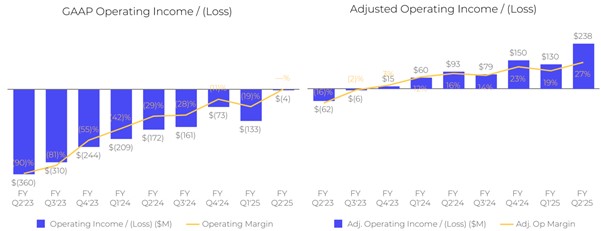

Profitability: Affirm’s operating expense-to-revenue ratio continues to decline, reflecting efficient cost control. Adjusted operating income has shifted from losses to profits, with a margin rising to 27%, signaling strong profitability and sustainable growth potential. GAAP operating income profitability is expected in Q4 2025, with promising future performance.

Source: Affirm

Source: Affirm

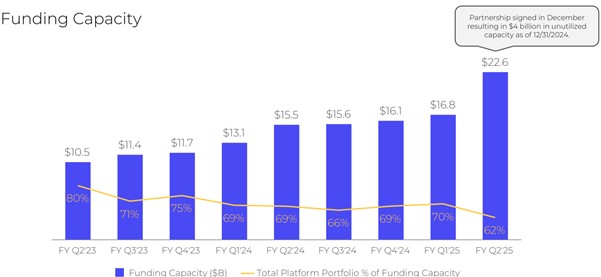

Abundant Liquidity: Affirm boasts strong financial resilience, with available liquidity reaching $22.6 billion, effectively addressing economic uncertainty. Notably, its capital utilization rate dropped from 80% to 62%, indicating expanded funding scale but a lower loan issuance proportion, possibly reserving funds for future expansion.

Source: Affirm

Leverage Fuels Growth: Affirm's ratio of total loans to total equity stands out in the BNPL industry, reaching 4.65 as of June 30, 2024—far below Klarna's 11 (1100%), yet above Afterpay's 0.96 (96%) and PayPal's 0.77 (77%)—demonstrating its strategy of using moderate leverage to drive growth while balancing expansion and risk in a competitive landscape.

Notable Concerns

Slowing Key Metrics: In fiscal year 2024, GMV growth slowed to around 30%, active user growth fell below 20%, transaction per active user growth stagnated, and average order value (AOV) continued to decline. These trends may stem from market saturation, reduced consumer purchasing power, and rising competition, making it hard to sustain high user and transaction growth. The AOV drop reflects a shift toward smaller transactions.

Source: Affirm, TradingKey

Intensifying Competition: In March 2025, Walmart ended its exclusive partnership with Affirm, partnering with Klarna instead. Though Walmart accounts for only 2% of Affirm’s operating revenue, its status as a retail giant makes its partnership critical to Affirm’s reputation and brand appeal. Losing this partner could weaken Affirm’s BNPL market competitiveness, further impacting business expansion and GMV growth, with an estimated short-term GMV drop of about 5%.

Macro Uncertainty: Macro uncertainties affecting Affirm include soft credit markets, economic downturns, regulatory changes, and interest rate volatility, potentially weakening revenue, compressing spreads, and increasing cost pressures. Affirm must adapt strategies flexibly to maintain competitiveness and financial stability.

7. Target Price Analysis

Despite challenges, Affirm demonstrates growth potential with a 27% adjusted operating margin, key partnerships like Shopify, and international expansion. However, Walmart’s partnership termination and 2025 macro uncertainties pose short-term hurdles, compounded by intensifying BNPL competition. A comprehensive assessment suggests a fair target price of $43 per share.

Valuation Methodology

- Revenue Forecast: Management projects fiscal year 2025 revenue between $3.13 billion and $3.19 billion. Adjusted for Walmart’s partnership end, the median revenue estimate is $3.002 billion.

- EV Calculation: Using a forward EV/Sales multiple of 7 (based on industry averages and growth prospects), the enterprise value (EV) is $21.01 billion.

- Equity Value: With projected fiscal year 2025 net debt of $6.256 billion, equity value is $21.01 - $6.256 = $14.754 billion.

- Share Price Calculation: Based on management data, the weighted average diluted shares outstanding in fiscal year 2025 is 342 million, yielding a target price of approximately $43 per share.