Broadcom’s AI Boom Reshapes the Industry

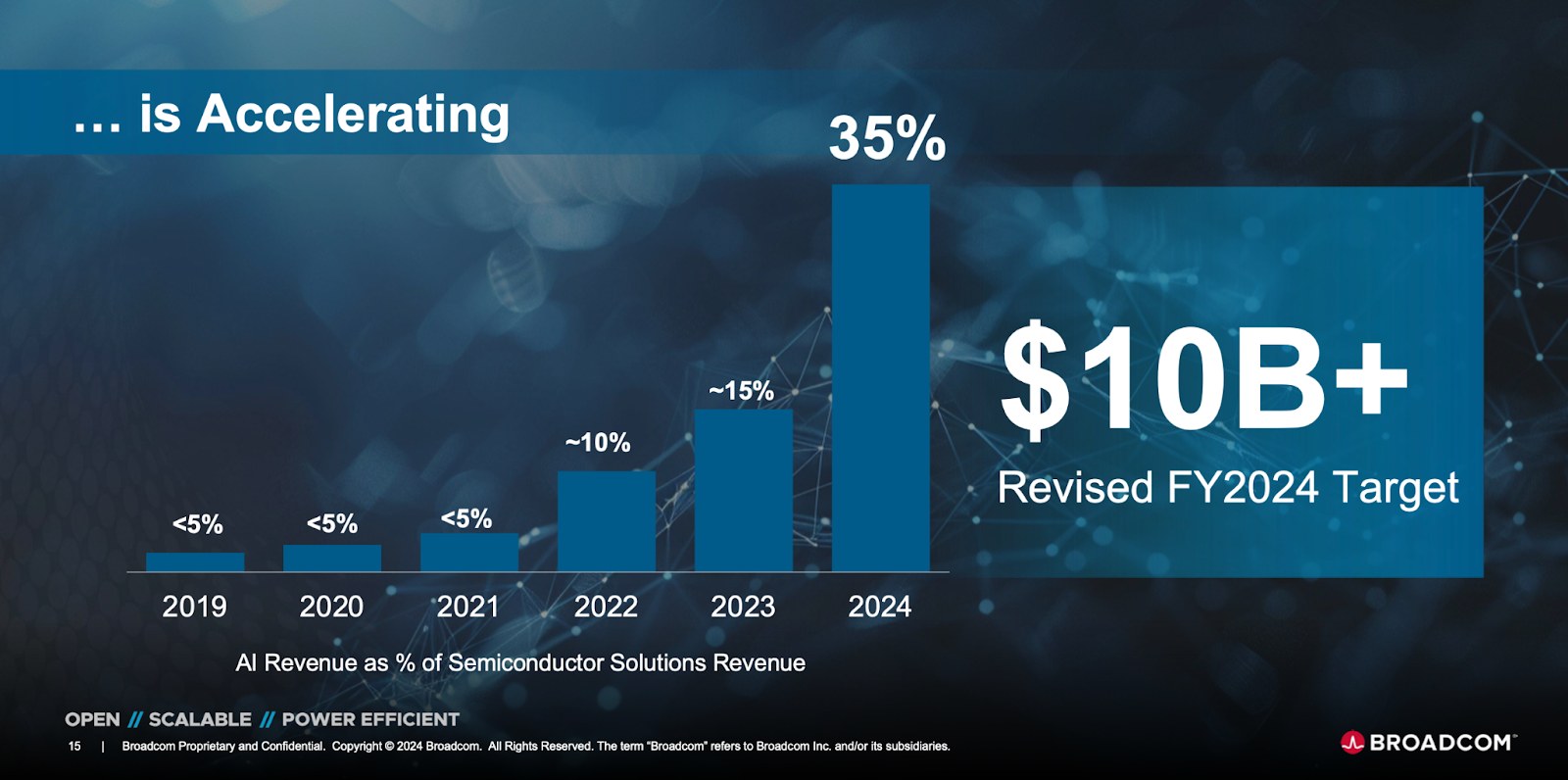

- AI Revenue Surge: Broadcom’s AI-related semiconductor revenue hit $10 billion in FY2024, now accounting for 35% of total semiconductor sales.

- Financial Strength: Q1 2025 revenue soared 25% YoY to $14.9 billion, with an EBITDA margin of 68% and $6 billion free cash flow.

- VMware Acquisition: The $61 billion deal accelerates Broadcom’s shift to software, boosting recurring revenue and strengthening enterprise cloud adoption.

- Premium Valuation: Broadcom trades at 22.8x EV/EBITDA, a 66% sector premium, requiring sustained AI-driven expansion to justify its high price tag.

TradingKey - Broadcom Inc. (AVGO) has become a leader in semiconductor and infrastructure software through AI-driven expansion and acquisitions.

On the basis of rising revenues tied to AI, healthy margins, and aggressive cash generation, Broadcom presents a compelling investment case to investors. Broadcom's long-term thesis is based on being positioned to capitalize on the AI wave, expansion of software offerings into enterprises, and competitive strength in networking solutions. The $61 billion VMware acquisition is a transition to a software-led model of expansion that will drive revenue predictability and profitability.

Broadcom's ability to capitalize on the wave of AI is a distinguishing factor that separates it from legacy semiconductor players. While other industry players have their eyes on developing direct AI chips, Broadcom provides connectivity solutions that make operations hassle-free through the help of AI. But even with positive fundamentals, valuation is a concern with it being at a premium. The investors will have to weigh Broadcom's competitive advantage against implementation risks to place their bet on the company's shares.

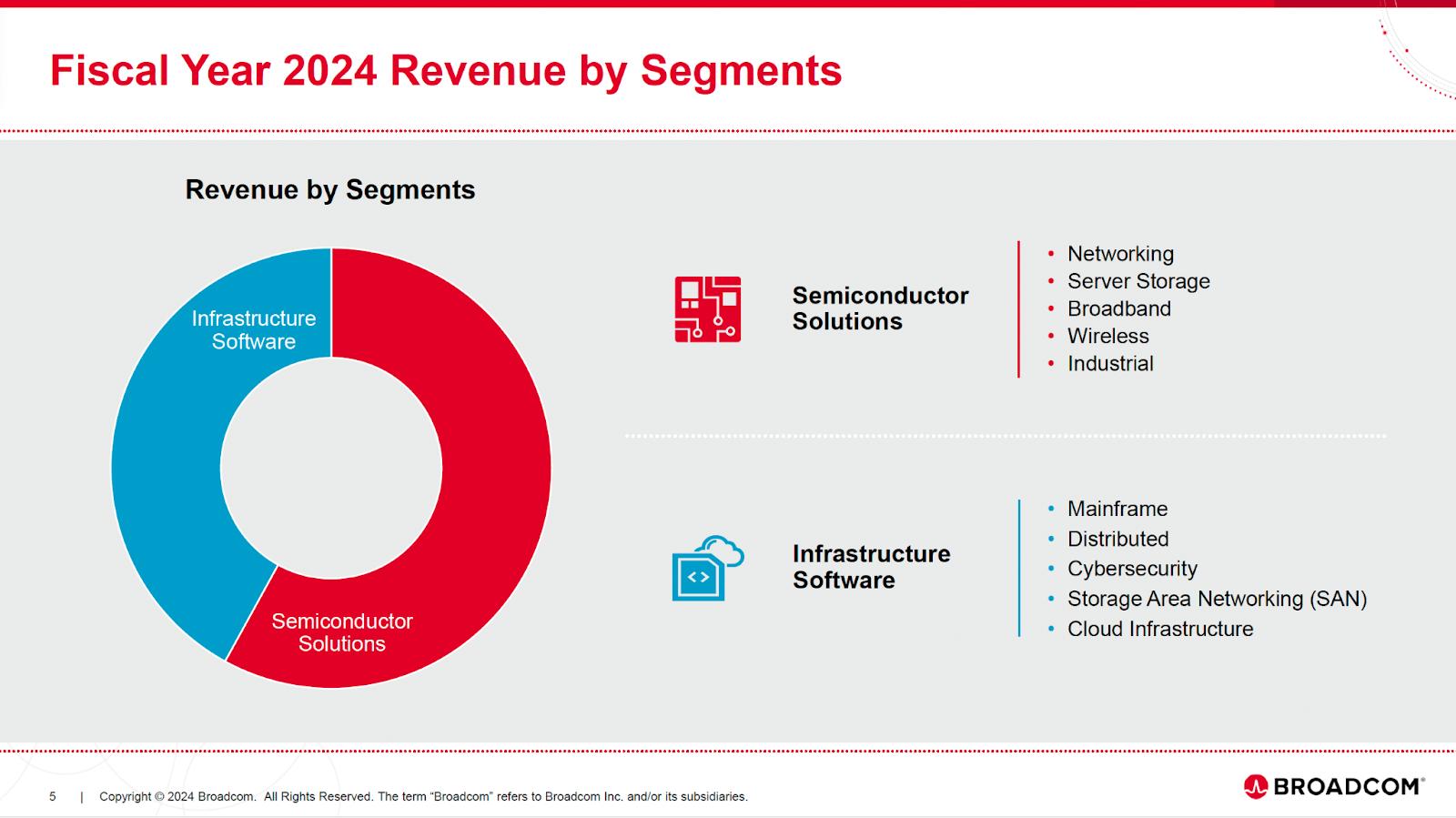

Business Summary: Semiconductors & Software Infrastructure Colossus

Broadcom's business is divided into two primary segments: semiconductor solutions and infrastructure software. The semiconductor business involves networking, broadband, wireless, and AI accelerators, while infrastructure software business involves mainframe, cybersecurity, and cloud solutions.

Revenues derived through AI increased 77% YoY to $4.1 billion in Q1 2025 due to hyperscalers ramping up spending on AI XPU and connectivity. The infrastructure software business achieved a still more impressive 47% YoY increase due to adoption by enterprises and VMware integration into Broadcom's ecosystem. Such aggressive revenue expansion in software offsets Broadcom's high-margin semiconductor business model and allows it to ride out industry cyclicality over time.

Broadcom's VMware acquisition secures its cloud and virtualization position while raising concern over risks of implementation. The acquisition will help Broadcom boost its base of recurring revenue by reducing dependency on cyclic semiconductor demand. Broadcom's strategy around AI is to provide connectivity solutions, AI interconnects, and merchant AI accelerators (XPUs) to hyperscale cloud providers.

As more complex data center infrastructure is needed to handle AI workloads, Broadcom is well-positioned to capitalize on secular trends driving demand for high-speed connectivity solutions and network AI based on Ethernet. The company's technology lead around AI interconnects will be key to driving long-term growth.

Broadcom is no longer merely a semiconductor company. Its expansion into software, particularly with VMware, offsets revenue volatility that follows chip demand cycles. However, software integration issues can mute synergistic hopes and slow revenue expansion.

Competitive Landscape: The War Heats Up

The competitive scenario in the semiconductor and software space is transforming at a very rapid rate with AI-powered infrastructure at their core. Broadcom is competing with semiconductor and software companies such as Nvidia (NVDA), AMD (AMD), Intel (INTC), and Cisco (CSCO).

Nvidia is way ahead in AI GPUs with their CUDA platform and deep learning. Broadcom's AI networking and connectivity products remain essential to hyperscalers constructing AI infrastructure. Unlike Nvidia and AMD's focus on compute-centric capabilities in AI, Broadcom's focus remains on high-speed interconnects and merchant AI accelerators that allow it to scale up AI workloads.

Even with such advantages, price pressure will still exist. As hardware margins narrow, Broadcom's pricing power on AI connectivity will be questioned. Furthermore, AMD and Intel continue to expand their AI-focused offerings with additional competition to the broader data center ecosystem. Another risk is that cloud providers design their own customized silicon internally, making Broadcom solutions increasingly dependent over time.

Broadcom's rich IP portfolio with ~21,000 patents and close customer relationship with hyperscalers do provide a competitive moat that cannot be easily replicated. The transition to Ethernet-based networking in AI provides a significant opportunity for Broadcom to gain more market share, particularly as Ethernet-based solutions scale cost-effectively in AI data centers.

Broadcom's role in network AI remains significant but can no longer be taken for granted with Nvidia's threat to move into this space. The battle to control AI infrastructure is heating up, and Broadcom will have to continue to innovate and build good customer relationships. If it can defend its market share while building up its presence in AI connectivity, it will remain a dominant player in the space. But if competitors erode its pricing power or cloud providers build stand-alone solutions, Broadcom's growth will be stifled.

Broadcom’s Triple-Threat Growth: How AI, Cloud, and VMware Are Powering Record-Breaking Financials

Broadcom's revenue expansion is driven by three key drivers: VMware integration, enterprise cloud adoption, and growth in AI infrastructure.

Financials continue to be record-breaking at Broadcom. Q1 2025 revenue was $14.9 billion, up 25% year over year. Adjusted EBITDA was $10.1 billion with a margin of 68%. Free cash flow was $6.0 billion at 40% of revenue and up 28% year over year. The numbers reflect Broadcom's ability to generate high operating leverage as it increases sales of products and software solutions related to AI.

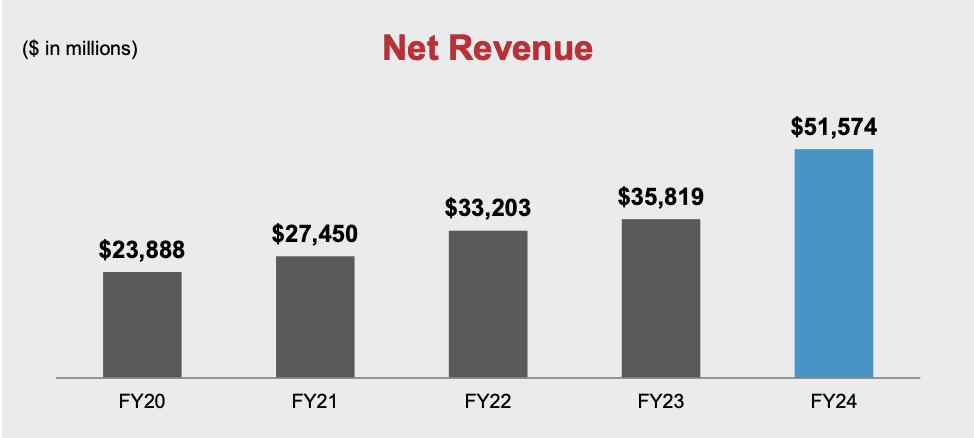

Broadcom has grown revenue every year over the past five fiscal years to $51.6 billion in FY2024 from $23.9 billion in FY2020. The rise is a compounded annual growth rate (CAGR) of approximately 21%, indicating that the company has successfully expanded into high-growth areas such as AI infrastructure and cloud software. FY2024 was especially notable with a boost coming through increased adoption of AI-related technologies and seamless integration of acquisitions such as VMware.

The consistent increase in revenues is a reflection of Broadcom's efficient market penetration and diversification in semiconductor and software sectors. Broadcom has effectively developed resilience against market volatility by diversifying its portfolio and reducing dependency on cyclic hardware markets. Plain and simple, Broadcom's steady and increasing revenue growth indicates a well-run company that can effectively capitalize on industry trends.

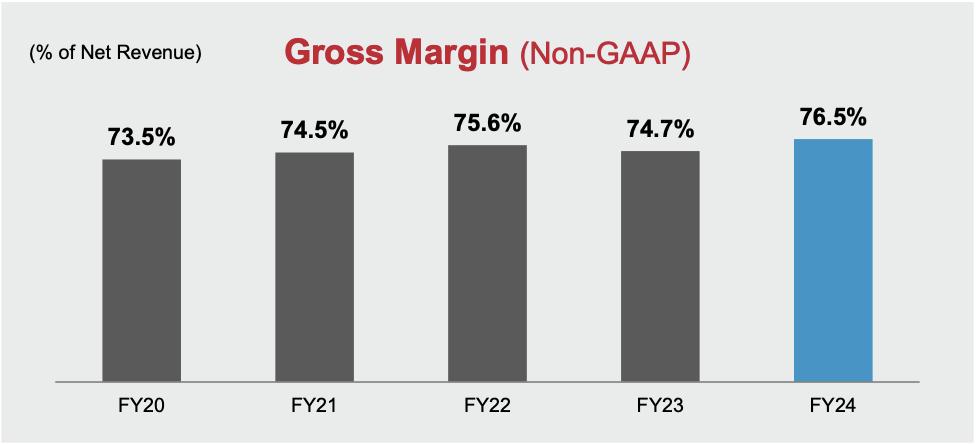

Broadcom's gross margin expansion over recent years demonstrates its cost management efficiency and pricing strength in markets. From a non-GAAP gross margin of 73.5% in FY2020 to 76.5% in FY2024, it increased this level. The expansion can be largely attributed to a shift to higher-margin software products and high-margin AI-driven solutions, reflecting a concern with profitability as well as revenue growth.

Adjusted EBITDA has also registered impressive growth to reach close to $31.9 billion in FY2024 from $13.6 billion in FY2020. Such a steep increase is a clear indication of Broadcom's high operational efficiency and scalability as it takes advantage of high-margin business segments and efficient cost management strategies.

Cost efficiency is a feature of Broadcom's business model. It incurred $9.3 billion in R&D spending in FY2024 to continue innovating while limiting capital spending to a paltry $100 million in Q1 to showcase asset-light operating efficiency. Broadcom's focus on software-driven and AI revenue streams enables it to maintain high adjusted EBITDA margins to justify business model scalability. The fact that it is able to sustain healthy profitability while accumulating a portfolio of AI infrastructure illustrates that it is positioned to be a high-growth, high-margin business.

Ultimately, Broadcom's financial well-being is based on its ability to generate plenty of free cash flow while still spending aggressively on R&D. As long as it continues to invest successfully in high-growth AI and software areas, profitability will continue to be healthy. Integration challenges with VMware and competition in AI networking remain top risks that can hinder continued margin expansion.

AI Boom: How Strategic Innovation Turned a Niche Bet into a Powerhouse

Broadcom's AI business has become a rapid growth driver generating $12.2 billion in FY2024. Starting at less than 5% of revenue in 2019, Broadcom has strategically built up its AI infrastructure capabilities through leading PCIe Retimer technologies. Broadcom offers differentiated advantages with proprietary 5nm silicon solutions such as 35% lower power consumption and 40% longer reach compared to competitors using third-party solutions. This technology advantage provides significant efficiency and cost-effectiveness in AI data centers.

Strategically, Broadcom's positioning within the space of AI is to prioritize high-performance networking and interconnectivity rather than competing head-to-head in Nvidia and AMD's dense compute space. Its revenue trajectory in AI emphasizes a well-executed strategy to capitalize on hyperscale expansion in the data center space, with scalability and efficiency being at the forefront. Its niche focus with heavy R&D investment and industry-leading technology positions Broadcom to continue healthy growth in the high-growth space of AI infrastructure.

AVGO’s Pricey AI Bet: Is Its Premium Valuation Justified?

Even with its strong growth, Broadcom's valuation continues to be a concern to investors. The company's current valuation at higher-than-peer multiples is evident in a forward EV/EBITDA of 22.8x against a sector median of 13.7x, a 66% premium. Similarly, its forward P/E multiple of 28.7x against a sector median of 21.5x suggests that investors are pricing in high levels of expansion in AI. However, looking at a PEG ratio of 1.31x against a sector median of 1.67x, it seems that expansion in AI is not yet fully priced into shares and that upside is present.

Broadcom is a fascinating AI-oriented investment with healthy financials, a lead position in AI networking, and rising software revenues. It is not risk-free, however. It is priced at a premium, so subsequent growth will have to be perfect to justify it. The investor will have to take a long-term position with Broadcom with short-term volatility in mind while understanding that it can dominate AI infrastructure markets. The company's size, diversified revenues, and high free cash flows make it a good institutional portfolio allocation.

Concluding Thoughts

Broadcom’s AI-driven growth, record-breaking revenues, and software expansion position it as a dominant force in AI infrastructure. With AI revenue surge and a strong cash flow engine, its future looks promising. However, its premium valuation requires flawless execution, making it a high-reward but carefully calculated investment.