[IN-DEPTH ANALYSIS] Constellation Energy (CEG): Deepseek Impact Meets Nuclear Power: Why CEG Is Still Underrated in the AI Era?

Source: TradingView

Key Points

- Surging electricity demand driven by AI data centers, electrification, and industrial growth exacerbates US power market tightness.

- DeepSeek’s efficiency gain may reduce per-unit power consumption, yet Jevons Paradox sustain long-term power demand resilience.

- Constellation’s Calpine acquisition creates the largest U.S. clean energy portfolio.

- CEG's reasonable value per share is around $250, indicating a potential increase of about 25% in 2025.

Overview

TradingKey - Constellation Energy (CEG) went public independently after being spun off from Exelon in 2022 and is currently a constituent of the S&P 500. Founded in 1999 and headquartered in Baltimore, Maryland, the United States, the company's core assets cover nuclear energy, wind energy, solar energy, and energy services. It is one of the largest carbon-free energy producers in the United States. The company has approximately 22GW of nuclear power generation capacity and about 11GW of non-nuclear baseload, intermittent, and peaking power generation capacity, with the nuclear power business accounting for over 70% of its total electricity generation.

CEG may focus more on technology development that is closely integrated with AI data centers and new energy businesses. For example, its technology may be more suitable for the special needs of AI data centers for stable and efficient power, being able to precisely regulate power supply to meet the peak and off - peak electricity demands of data centers. In contrast, the technical approaches of other SMR companies(such as NuScale Power、TerraPower) may be more inclined towards traditional energy application fields, or their exploration of technologies for integration with AI data centers and new energy businesses may be relatively lagging. This gives CEG a unique advantage in meeting the needs of AI data centers and new energy businesses, enabling it to better seize the development opportunities brought by these emerging fields.

Revenue Sources

1) Nuclear Energy Business

The company owns 14 nuclear power plants with a total of 23 reactors, boasting a large total installed capacity. Nuclear power generation is characterized by stability and low carbon emissions, providing the company with a continuous and reliable power output and occupying a dominant position in the company's energy supply structure.

The company has signed a ten-year power supply agreement worth $840 million with the federal government. In September 2024, CEG signed the largest-ever power purchase agreement with Microsoft. Microsoft will purchase all the electricity produced by the Three Mile Island Nuclear Generating Station over the next 20 years to support the demand of its AI data centers.

2) Renewables

The company is actively laying out wind and solar power generation projects. In 2024, the total electricity generation from wind and solar power accounted for about 10% of the company's total electricity generation. In 2025, CEG plans to acquire Calpine, a natural gas power generator, for $26.6 billion (including debt), adding 27GW of natural gas and geothermal assets and enhancing its peak regulation capacity.

3) Energy Solutions

CEG also provides related energy services. For example, it offers energy-saving renovation projects such as LED lighting and HVAC upgrades, provides electricity procurement and grid stability solutions, and is deeply tied to the demand of data centers and industrial users.

Date | 2024-09-30 | 2024-06-30 | ||||

Data Type | Indicator Value(mn) | Percentage | YoY % | Indicator Value(mn) | Percentage | YoY % |

Electricity sales | 5,351.00 | 81.69 | 3.08 | 4,527.00 | 82.68 | 2.01 |

Natural gas business | 533.00 | 8.14 | -11.90 | 580.00 | 10.59 | -11.59 |

Source: TradingKey, SEC Filings

From the perspective of the exposure of net asset value, the asset value of CEG is mainly concentrated in the nuclear power generation sector, accounting for 60% of the total assets. This indicates that the power business occupies a core position in CEG's asset portfolio. Other important assets include natural gas infrastructure (20%), renewable energy facilities (15%), and other services (5%).

Date | 2024-09-30 | 2024-06-30 | ||||

Data Type | Indicator Value(mn) | Percentage | YoY % | Indicator Value(mn) | Percentage | YoY % |

Mid-Atlantic | 1,603.00 | 24.47 | 13.61 | 1,304.00 | 23.82 | 8.85 |

Midwest | 1,275.00 | 19.47 | 14.14 | 1,168.00 | 21.33 | -12.18 |

Other international(regions) | 683.00 | 10.43 | -8.08 | 756.00 | 13.81 | -5.14 |

Taxes(ERCOT) | 523.00 | 7.98 | -6.44 | 357.00 | 6.52 | 8.84 |

Source: TradingKey, SEC Filings

Power Market Outlook: Demand, Technology and Industry Changes

1) Persistent Tightness in the U.S. Power Market

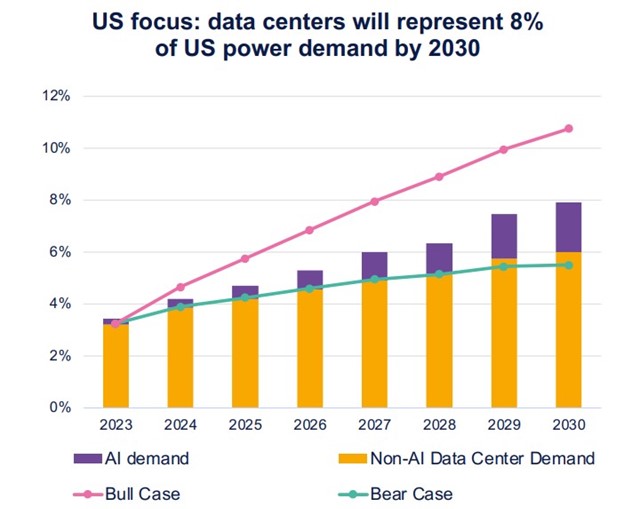

With the continuous increase in the demand for data centers in US, the load forecast has been continuously adjusted upward, and the backup power margin has been under pressure. In fact, in all the markets operated by Constellation, we have noticed that the load of data centers is not intermittent; instead, they are users that consume electricity around the clock, 24 hours a day and 7 days a week.

Source: CPRAM, IEA

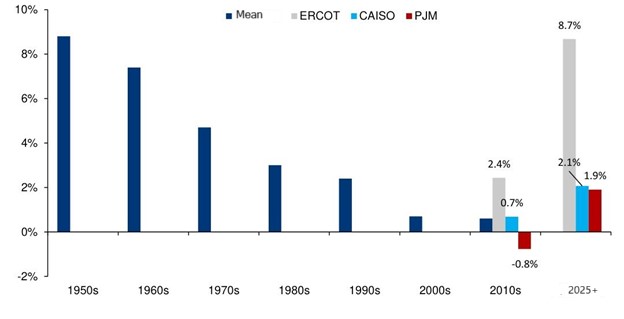

Approximately 60% of the electricity on the power generation side in the United States is traded through the wholesale electricity market. Seven major Regional Transmission Organizations (RTOs) and Independent System Operators (ISOs) operate seven electricity markets, including the California Independent System Operator (CAISO), the Electric Reliability Council of Texas (ERCOT), the New York Independent System Operator (NYISO), and the Pennsylvania - New Jersey - Maryland Interconnection (PJM). Over the past three years, the controllable installed capacity margin(the excess of controllable power generation capacity over the expected demand in a power region) in the ERCOT power region has been continuously decreasing to 1.02, far lower than the average level of 1.1 in the United States and 1.16 in the CAISO region of California. In the past few years, the U.S. power market has been in a continuous state of tightness. The main reasons are the accelerated retirement of fossil-fuel power plants and insufficient renewable energy installations, as well as the surge in power demand caused by industries such as data centers and cryptocurrency mining. Looking ahead, due to insufficient external interconnection on the supply side, the tight situation of power supply and demand may be further exacerbated.

Figure: Upward Revision of Long-Term Load Growth Forecasts

Source: EIA

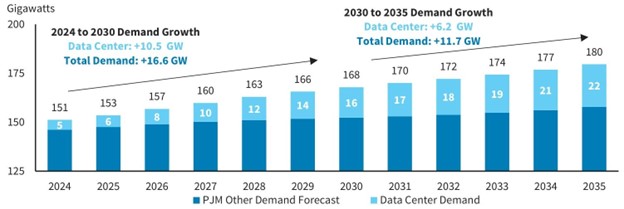

From a long-term demand perspective, the PJM forecasts that by 2035, compared to 2023, summer peak electricity demand will grow at an annual rate of 1.5%, nearly double last year's projected growth rate of 0.7%. Additionally, we note that the compound annual growth rate (CAGR) of annual net demand has been revised upward from the previous 1.5% to 3.6%.

Figure: PJM Region Summer Peak Demand Growth

Source: UBSe

2) DeepSeek's Energy-Efficiency Impact

DeepSeek's latest model R1 reduces training energy consumption by approximately 60% compared to U.S. counterparts. If this technical approach becomes widespread, data center power consumption per computing unit could drop 50% to 2-3kW, significantly altering EIA's projections for AI-related electricity demand.

While technology companies and power suppliers have secured long-term power purchase agreements (PPAs), the pace of technological iteration has outpaced expectations, creating reassessment pressures on the return on investment for new baseload power plants (nuclear, natural gas) post-2030. Meanwhile, market divergence intensifies: renewable energy operators and grid flexibility technology providers will continue to benefit from AI-driven dynamic load demands, while traditional baseload plant valuations would account for risks.

Source:Lawrence Berkley National Laboratory

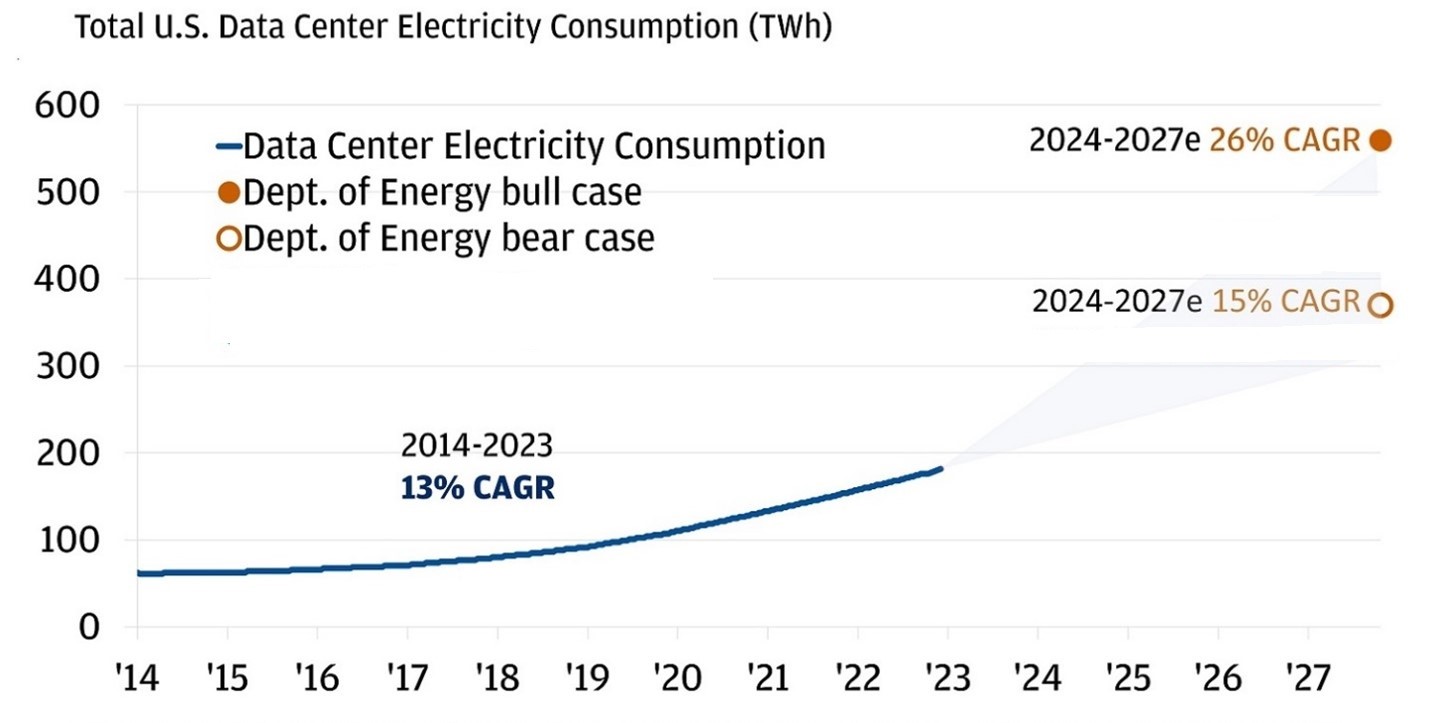

The latest forecast by the U.S. Department of Energy (DoE) shows that if AI workloads develop under the optimistic assumption scenario, the power demand of data centers will surge at a compound annual growth rate (CAGR) of 26% in the coming years, meaning the demand will double every 2.5 years. However, considering the slowdown in demand growth due to the energy - efficiency breakthrough of DeepSeek, the growth rate of power demand in data centers will fall back to around the historical level of 15%.

We still face the Jevons Paradox, while reducing energy consumption holds promise for efficiency gains, the open-source nature of Deepseek's strategy may incentivize exponential expansion of AI applications. Meanwhile, the Trump administration is accelerating its "Stargate Initiative," planning a $500 billion investment in next-generation AI computing infrastructure. Nuclear power, with its baseload stability and technological advancements, remains immune to fluctuations in renewable energy policies and could still be included in federal subsidy programs by 2026.

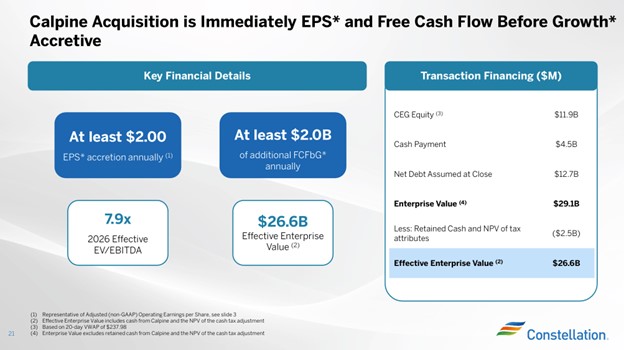

Acquisition of Calpine: Risks and Rewards

Constellation announced a cash-and-stock transaction to acquire Calpine Corporation. Prior to the acquisition, Constellation derived approximately 80% of its power generation from nuclear energy, demonstrating high business concentration. The integration of Calpine's 27.7 GW of installed capacity will expand CEG's clean energy portfolio (including natural gas, geothermal, etc.) to nearly 60 GW across 48 U.S. states, solidifying its position as the nation's largest clean energy provider. Calpine's presence in key regions such as Texas and California has helped Constellation capture the power markets with the fastest-growing demand. This acquisition has reduced its dependence on a single energy source and enhanced its ability to adapt to fluctuations in electricity demand.

Source:Constellation

The acquisition of Calpine is expected to be completed in the second half of 2025 to the first half of 2026. Constellation has calculated that the enterprise value of Calpine is $26.6 billion, based on the issuance of new shares, cash payments, and the assumption of Calpine's debt, minus the cash received from Calpine and the tax benefits obtained. The company will also assume a net debt of $12.7 billion, which may push up CEG's leverage ratio in the short term. However, Calpine's low-leverage assets (no coal-related liabilities) and stable cash flows are expected to deliver significant value creation: the acquisition is projected to boost CEG's 2026 earnings per share (EPS) by over 20% and generate more than $2 billion in annual free cash flow.

Financials and Valuation

The 2024 financial report of CEG outperformed its peer electric utilities and estimates. The revenue ($23.6 billion) was basically stable, while the adjusted earnings per share (EPS) ($8.67) surged (+52% YoY). However, 70% of the high-growth profit came from the Production Tax Credit (PTC) subsidy. According to the policy, utility projects started before 2025 can still enjoy the traditional PTC subsidy, which indicates that there will still be one of favorable supports this year.

The management is confident about 2025 and has confirmed that the full - year adjusted EPS guidance range is $8.90 - $9.60. CEO Joe Dominguez emphasized that "Nuclear plants are the only energy sources that can consistently deliver an abundance of energy that is carbon-free", and it is expected that the proportion of nuclear power revenue will increase to 85% by 2030. In 2024, the company increased its payout ratio to 28% and completed a $1 billion share repurchase (accounting for 2.1% of the outstanding shares). In 2025, it plans to continue repurchasing $1 billion worth of shares. If the integration of Calpine goes smoothly, the payout ratio is expected to increase to 45%, reaching the level of leading utility companies.

In the past two months, compared with the S&P Select Utility Sector Index (XLU), the company's stock price has relatively dropped by about 40% due to market concerns about AI-driven demand sustainability. We believe that after the adjustment, the company's stock is rather attractive, and the pace of share repurchase may accelerate. If the company can effectively utilize the demand from data centers, and with the support of the PTC, it may drive additional earnings growth.

Based on the previous analysis of a CAGR rate of 15% for data center demand and a 5% revenue growth rate for conventional power businesses, considering the average EV/EBITDA multiple of about 12.5 times, the reasonable value per share of CEG is around $250. The current trading price ($200) is close to the lower limit of the pessimistic DCF valuation. If the acquisition of Calpine proceeds smoothly and gets a premium from synergistic effects, CEG's share price may rebound to the range of $240 - $270. This implies a potential increase of about 25% in 2025.

Company Name | Constellation Energy Corporation | American Electric Power Company, Inc. | Exelon Corporation | Duke Energy Corporation | Eversource Energy | NextEra Energy, Inc. | Median |

Ticker | CEG | AEP | EXC | DUK | ES | NEE | — |

P/E (TTM) | 17.88 | 18.75 | 17.6 | 20.52 | 26.86 | 21.61 | 19.635 |

PEG (TTM) | 0.13 | 0.59 | 3.65 | 4.38 | — | — | 3.65 |

EV/EBITDA | 10.45 | 12.95 | 12.5 | 12.41 | 12.16 | 18.49 | 12.455 |

EBITDA Growth | 65.16% | 12.09% | 5.57% | 7.78% | 10.85% | -19.13% | 6.68% |

ROE | 30.11% | 11.39% | 9.34% | 9.08% | 5.55% | 9.51% | 10.37% |

ROA | 7.15% | 4.67% | 3.82% | 3.82% | 4.63% | 3.82% | 4.13% |

Source: Refinitiv