What Should Investors Watch With the Upcoming Federal Reserve FOMC From 18-19 March 2025?

TradingKey - It has been a rough three weeks for investors in US stock markets. The S&P 500 Index took just 16 trading sessions to fall 10%, what is officially termed a “correction”.

That unenviable data point also meant that the key US stock market index notched up its seventh-fastest correction going back to 1929, according to Bloomberg. Three of the seven fastest drawdowns have happened under current President Trump – in 2018, 2020 and just now.

But what’s just as important for investors this week will be the US Federal Reserve’s Federal Open Market Committee (FOMC) gathering that takes place from 18 to 19 March. Investors will be looking for commentary and guidance from the Fed on whether it’s likely to cut interest rates later this year.

Of course, the data haven’t been all that positive for the US economy in recent months but it’s far from a dire situation for the world’s largest economy. With that in mind, here’s what investors should be watching and what the Fed is likely to be discussing in its post-FOMC press conference.

Inflation numbers stay elevated

One of the key data points that Fed governors will have been poring over in the past few months – since the last FOMC meeting – is inflation. That’s because part of the Fed’s dual mandate is to ensure “stable prices” in the US economy.

Of course, inflation – as measured by core CPI – has been stubbornly stuck at around 3% in recent readings while the personal consumption expenditures (PCE) price index has been around 2.5%. While the latter is the Fed’s preferred measure of inflation, both are still well above the Fed’s target of 2% inflation for the US economy.

No doubt, there will be some comments from the Fed on what stubborn inflation means for long-term growth expectations as well as the outlook for the US economy. Of course, with tariffs, there have come worries around growth.

Inflation expectations and the dot plot

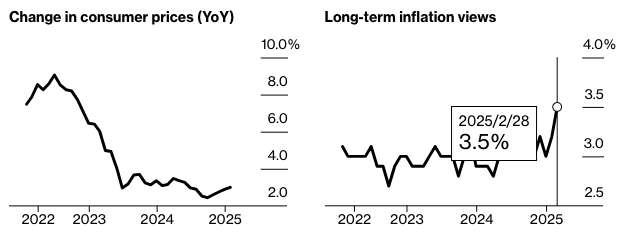

More worryingly for Fed officials is the fact that consumers are expecting higher inflation in the US economy – as per the University of Michigan consumer inflation expectations survey.

In that survey’s latest reading, US consumers expect long-term (over the next five years) inflation to average 3.9%, the highest reading since February 1993 and up from the 3.5% recorded at the end of February.

Unfortunately, higher expected inflation can end up leading to higher prices in reality – meaning inflation becomes entrenched.

US consumers expect inflation to keep rising

Sources: Bureau of Economic Analysis, University of Michigan

Expect the Fed to be on the lookout for that and comment on what that potentially means for the central bank’s interest rate policy for the rest of 2025. Indeed, the Fed will be releasing its updated “dot plot” of where the board of governors expects interest rates to be in the short and long term.

The last time the Fed released its dot plot was in its December 2024 FOMC gathering so investors will be keen to see whether the central bank agrees with the market’s expectations for two interest rate cuts for the rest of 2025.

Growth and recession fears on the agenda

Ultimately, a lot of what investors are focusing on is the massive fall in sentiment surrounding the health of the US economy. That has changed dramatically in the last few weeks as the stock market has taken a beating amid President Trump’s tariff announcements.

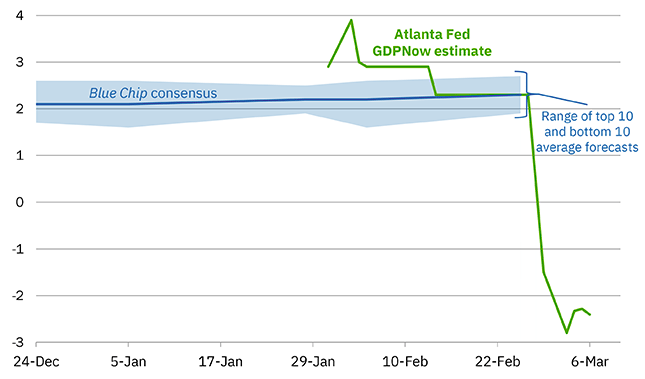

More importantly, growth expectations have also been cut massively for the US economy. The much-watched Atalata Fed’s GDPNow forecast – which looks at incoming data to track expected GDP growth in the current quarter – has plunged to -2.4% as of 6 March.

Atlanta Fed’s GDPNow real GDP estimate for Q1 2025

Sources: Atlanta Fed, Blue Chip Economic Indicators, Blue Chip Financial Forecasts

That has seen a slew of economists also cut their growth targets for the US economy this year. Weak consumer spending data as well as negative outlooks from some big US big box retailers have spooked investors. Add in President Trump’s tariffs and it’s a recipe for an expected recession.

The Fed will no doubt will be watching all this closely but the market’s fear is that the Fed will be constrained from cutting rates too much by still-elevated inflation, on the back of fears that inflation could shoot higher if rates get cut too quickly.

The central bank is likely to strike a conservative, hawkish tone as the plunge in sentiment isn’t actually matching up with the overall data. While the US economy is indeed slowing, the majority of growth metrics still look strong when juxtaposed against recent market declines.

Chairman Powell will likely agree with the market – on the caveat that inflation data can remain at its current level or fall further in coming months – that the Fed can start cutting rates in June.