Will the Federal Reserve Inject Liquidity Into the Market?

A Market at the Edge: The Fed's Most Stressful Liquidity Test Since 2020

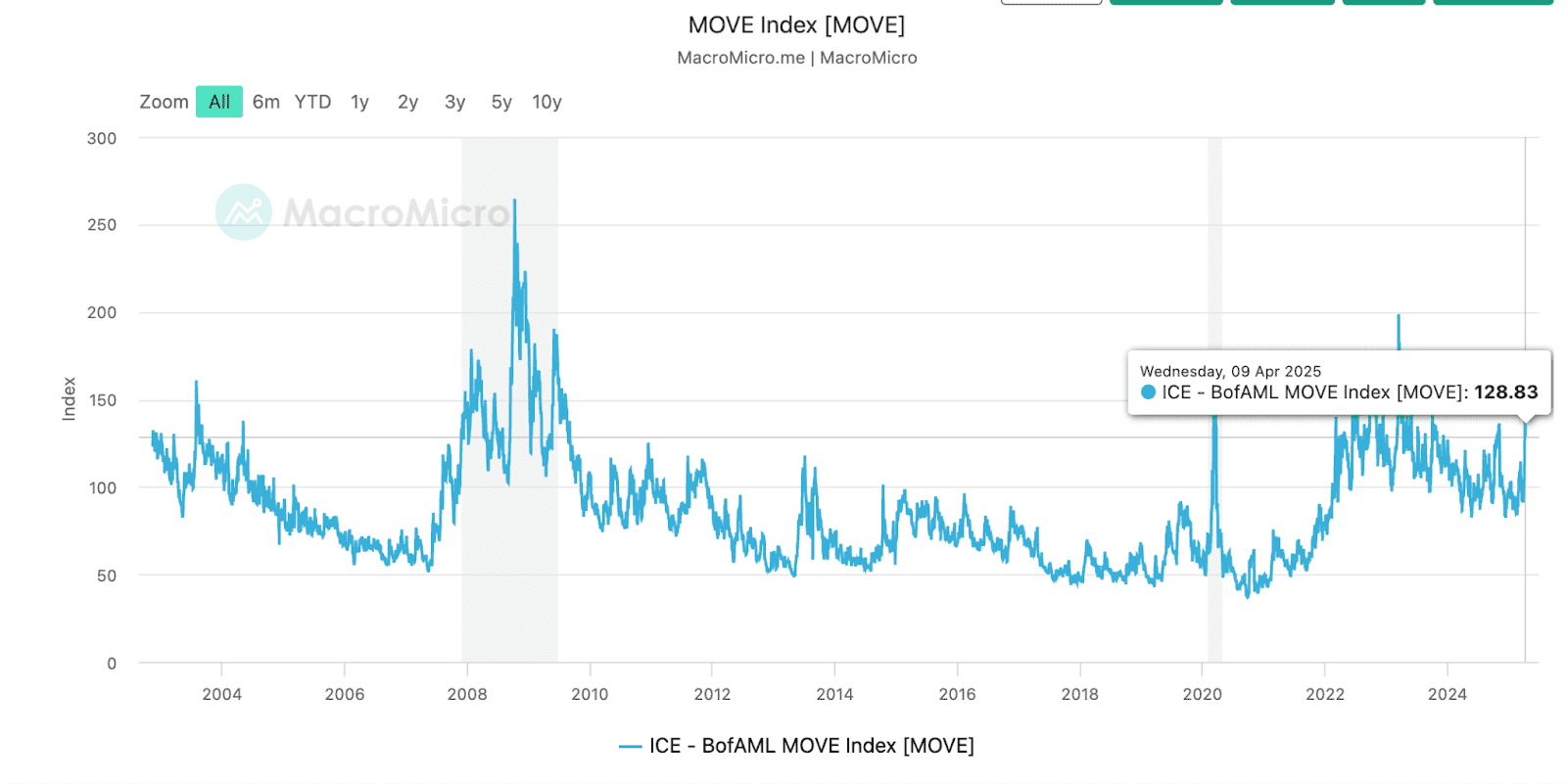

TradingKey - The American financial system is approaching its riskiest point since the COVID-19 collapse. In recent days, consecutive selloffs in stocks and Treasuries have sent one unmistakable message: investors are afraid. The S&P 500 experienced two of its worst back-to-back days of trading since the financial crisis. Wall Street's bond market volatility barometer, the MOVE index, has skyrocketed to historically high levels indicating systemic stress. Traders, fund managers, and institutionally allocated investors are quickly re-allocating portfolios, anticipating a monetary-policy regime change.

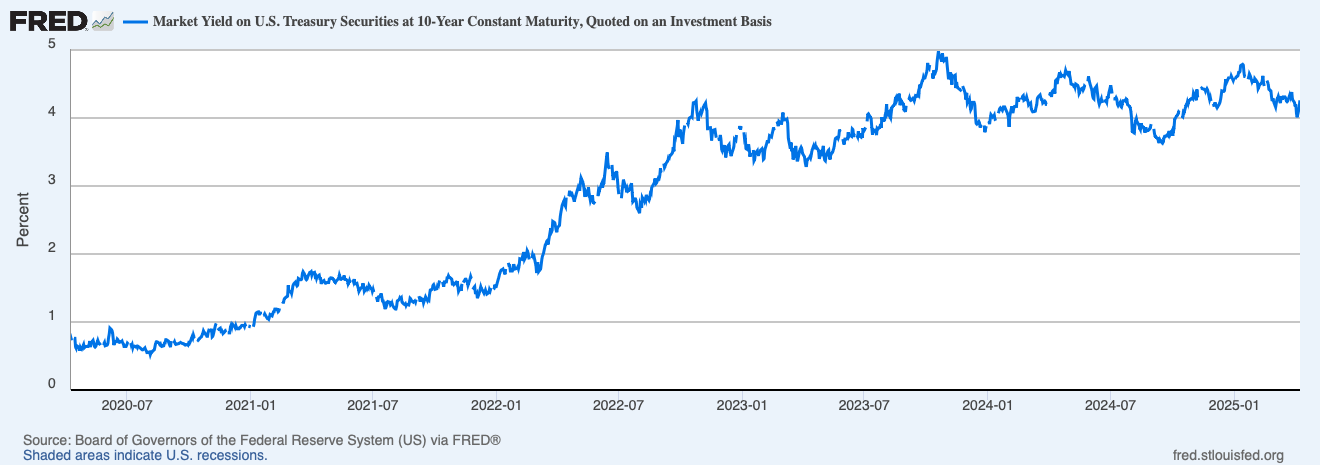

In normal circumstances, this would already have the Fed ready its liquidity firehose. But circumstances today are far from normal. The surge in long-term Treasury bond yields, specifically the 10- and 30-year, isn't driven by strength in the economy. Rather, it's driven by political risk, credit risk, and plummeting demand at a time when America needs to roll over trillions in coming due debt. And inflation is still sticky, constraining the Fed's flexibility. Jerome Powell's credibility rests upon tightrope-walking, act too late and risk market collapse, act too soon and risk fueling another inflationary spiral.

Source: FRED

The Trump Tariff Shock

At the center of this developing crisis is an immense geopolitical fuel: Donald Trump's re-launch of the U.S.-China trade war. President Trump initially imposed a broad wave of tariffs against Chinese products, as high as 125%. This prompted a new wave of retribution from Beijing, whose officials promised "a fight to the finish" and increased import tariffs against certain U.S. products.

Markets are not merely responding to the tariffs themselves, it's the broader implications. Trump's candid public remarks, such as suggesting cuts to the Fed while playing down inflation, have added gasoline to an already nervous atmosphere. His purpose seems to have two prongs to it: boost domestic growth in anticipation of an election and drive down long-term yields so that federal debt becomes less expensive to finance. Unintended side effect? Global capital fleeing Treasuries an the dollar.

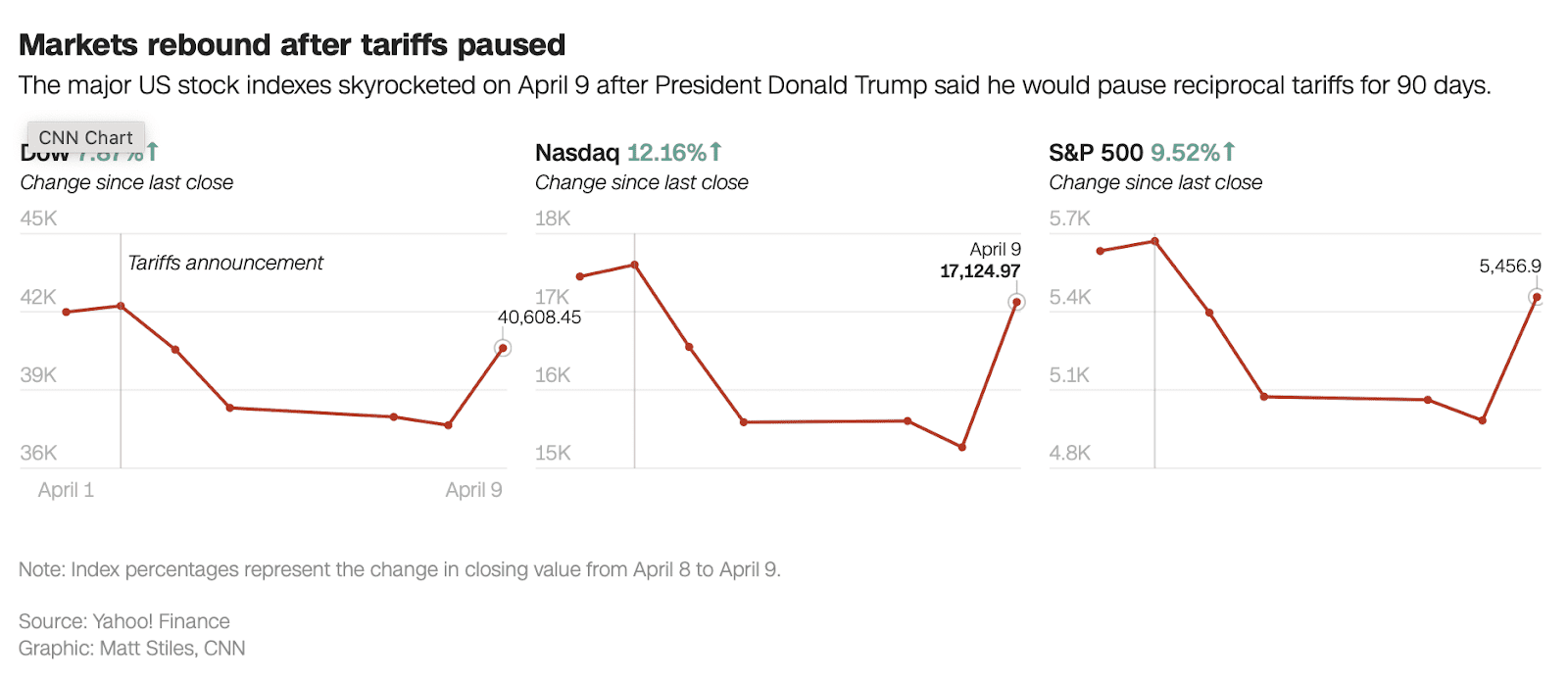

However, in a partial turnabout, Trump last week imposed a 90-day suspension of most new tariffs, while leaving a baseline level of 10%. Significantly, tariffs on imports from China were increased to 125%, fueling trade tensions. The unexpected move triggered an immediate market snapback, with the S&P 500 and Nasdaq bouncing hard.

For the Fed, this adds complexity. Although the timeout should ease near-term inflation pressure and volatility, China's specific increase can still fuel rising import costs, leaving inflation still in doubt. But perhaps more critically, temporary status implies underlying uncertainty, necessitating flexibility and vigilance from the Fed.

Source: CNN

Liquidity vs. Credibility: The Fed's Impossible Decision in an Election Year

The Federal Reserve is torn between two harsh realities: its obligation to maintain monetary credibility and its equally compelling obligation to stop financial contagion. In one corner, inflation, while easing, remains in excess of targets. The March CPI read of 2.4% YoY reaffirms that price stability is not yet back, particularly since supply chain pressures have returned as tariffs have re-activated. Reducing interest rates or reinstating QE has the potential to re-ignite inflation expectations, wiping out two-year hard-won disinflation.

.png)

Source: CNBC

On the other side, outright Treasury market turmoil would have substantially greater systemic consequences. If long-duration yields continue at current highs or spike even further, mortgage interest rates follow, consumer credit tightens, and the debt rollover cliff becomes an apparent trapdoor. The U.S. federal government simply can no longer roll over trillions of debt at 5%+ interest indefinitely. Banks, already laden with duration-imbalanced balance sheets, can't sustain another valuation blow.

During periods of acute uncertainty, the Fed has traditionally preferred to act forcefully. In 2008, following Lehman, it released liquidity without hesitation. And in 2020, it completed its fastest U-turn in monetary history. Whether Powell today is prepared to inject liquidity ahead of time, or wait for something to break, remains to be seen. His recent words about "long and variable lags" imply a preference for caution, but pressure from markets and even the White House can compel him to move earlier than one might think.

The probable course ahead, in an increasing clamor of opinion among analysts, is one of subtle rather than spectacular maneuver. This could take the form of halting balance sheet runoff (QT), offering stronger forward guidance on future rate cuts, or quietly ramping up repo operations to stabilize short-term funding and collateral markets.

Already, however, we can see evidence of the Fed stepping in quietly to fashion some sort of easing, liquidity is tentatively resurfacing in the system through the softening RRP and constrained issuance at the short end of the yield curve. The bond market is essentially compelling the Fed to act. Unless yields stabilize in the near future, and unless the MOVE index falls below 100, the pressure for action builds.

Source: Macromicro

Even when Powell resists easing formally in April, an acute credit shock or further equilibrium in equities can be the trigger for large-scale intervention. The risk-asset implications are binary: either liquidity pumps in and markets blow out, or the Fed dawdles and everything unravels. Plainly speaking, we have now entered the "window of intervention."

Announcements of QE by the Fed are not necessary in order to inject liquidity. However, it must do something, either through policy measures, communication, or both. The market has already shifted. Now, we wonder whether the central bank leads or forces reckoning. For institutional investors, this is an important turning point at which positioning for tail events, both good and bad, can shape next quarter's outcome.

Takeaway

The Fed is in a tight spot, markets are cracking, inflation is lingering, and trillions in debt needs refinancing. While Powell hasn’t officially acted, signs of quiet intervention are already emerging. With Trump’s tariff pause offering only brief relief, the pressure to inject liquidity is growing fast. Investors shouldn’t wait for a formal announcement, the Fed’s next move may be stealthy, but the market’s response could be anything but.