[IN-DEPTH ANALYSIS] GOOGL: The Most Attractively Valued Mag7 Stock

Source: TradingView

Key Points

- Alphabet, the parent company of Google, owns and operates the two most popular websites globally, making it one of the most prominent tech companies

- Google has solid positions in online advertising where they are the biggest player and Cloud where they are the third biggest player

- The strong balance sheet of Google allows them to be one of the largest investors in AI which is expected to cement their position as one of the most important companies in the world

- The outlook with regards to Google legal issues seems more optimistic after the change of power in the States

- With a target price of $230 (30% upside potential), Google is perhaps the most attractively valued investment among the Mag7 stocks

Business Description

Google is a technology company that owns and operates a set of products mainly revolving around Google Search – the most popular web-based search engine and the most visited website on earth. Google processes a hundred thousand searches per second, and the estimated daily searches are 8.5 billion. They have a 90% share in the search engine market, with the closest competitor being Bing with a 2.9% market share.

Source: Semrush

Part of Google is YouTube, the largest video-sharing platform and the second most visited website globally. Alphabet is the parent company of Google and several other related products and it is listed with the tickers GOOGL (with voting rights) and GOOG (with no voting rights). We will use Alphabet and Google interchangeably in this report.

Google was founded in 1998 and for these almost thirty years it has been one of the main engines of technological development becoming an integral part of our daily lives. “To google” has turned into the main verb to use when we want to say that we look for something on the internet.

.jpg)

Source: vestedfinance.com

Advertising as the Main Business Model

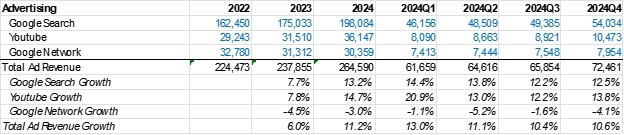

For its three decades of existence Google has been involved in numerous ventures across the tech industry, but advertising remains the backbone of the Google model. It currently represents over 75% of the total revenue generated in the last three years.

Source: SEC Filings, TradingKey

Source: SEC Filings, TradingKey

Google has many ways to advertise through its numerous websites and apps, including the Google Search Engine, Google Maps, YouTube, as well as partnering websites and apps.

With auction, advertisers can bid for specific search words and their products/services will appear on the top once users type that particular word in the google search engine.

The advertising business of Google can be classified in three main categories, called Google AdSense, Google Ads and Google AdMob:

Google Ads (formerly AdWords): Includes the ads that appear on Google Search, YouTube and other Google apps. This is where the majority of the revenue comes from

Google AdSense: Encompasses website owners and content creators. Here third parties display ads and share the ad revenue with Google. AdSense is part of Google Network revenue line.

Google AdMob: Helping mobile developers monetize their apps by displaying ads. This is also part of Google Network revenue line.

Google Subscriptions:

The revenue from subscriptions, platforms and devices represents 12% of the total revenue and it includes:

- Consumer subscriptions from YouTube Premium, YouTube TV, YouTube Music and Google One

- Sales of apps and in-app purchases from Google Play

- Devices, including sales from the Pixel family

Google vs Meta in Advertising

In terms of ad dollars in the field of online advertising, Google and Meta are taking the biggest and second biggest share respectively. Goole ad revenue is still significantly larger than that of Meta, however Meta has been growing faster. In 2024, the total revenue growth of Meta apps was 22% yoy vs 11% yoy for Google.

We believe there are two potential factors that contribute to this difference in performance. First, the nature of Meta websites and apps allows them to hold the attention of the user for longer and with a heavier emphasis on visual ad formats that we see in Meta, advertisers can achieve higher ROI.

Second, Meta has a heavier experience to the faster growing non-US market, while Google is geographically more inclined towards the more mature American market.

However, Google has its own unique strengths and areas that they can further monetize (e.g. YouTube) which means that Google will still dominate the online advertising industry for the years to come.

Cloud

Source: SEC Filings, TradingKey

Cloud is the fastest growing revenue segment of Google, currently representing 12% of the total revenues. Within this business segment, there is the Google Cloud Platform, the Google Workspace Package (Gmail, Google Drive, Google Docs and Google Meet), as well as all other services related to enterprise clients.

Source: Generating Value

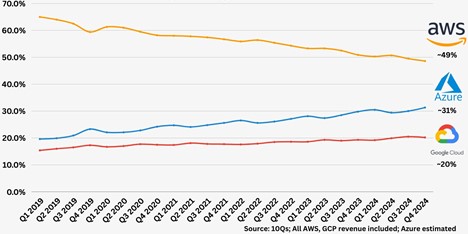

Makret Share of the Revenue Generatated Only by AWS, Azure and Google Cloud

Source: Generating Value

When it comes to cloud and enterprise businesses, Google is among the biggest names along with Amazon and Microsoft. However, Amazon and Microsoft, as incumbent players, have a bigger market share than Google. The outlook for Google Cloud is bright due to the following factors:

Industry tailwinds: All of Amazon, Azure and Google Cloud are increasing capital spending on the development of hardware/physical infrastructure that can solve the supply-side bottlenecks currently being experienced by the cloud players. This can fuel the revenue growth in the long term,

Clear value proposition: Google products are increasingly appealing for smaller and medium-sized businesses due to the more affordable pricing, more flexibility and tech savvy nature.

Early stage of monetization: As a segment, Google Cloud reached breakeven just two years ago. Just within the last financial year, the operating margin of the cloud segment expanded from a single digit percentage to nearly 18%. Further to this, the monetization for Google Cloud is still in a nascent stage, as the mature operating margins of the competitive products from Amazon and Microsoft are in the range of 30-40%.

Strong Balance Sheet Supporting Investments in AI

Source: SEC Filings, TradingKey

Similar to other Mag7 companies, GOOGL has been the center of attention for its significant capital spending, particularly on AI (GPUs, data centers, etc.).

The company expects $75 billion of capital expenditure in 2025, which is over 40% more than the previous financial year.

However, GOOGL's balance sheet looks very solid, with cash and short-term investments exceeding debt by $85 billion, implying a debt-to-asset ratio of just over 2%. Also, operating cash flow far exceeds the capital expenditures, keeping the free cash flows to the firm confidently in positive territory.

Competition from ChatGPT

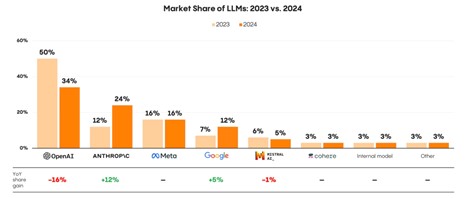

Google has been the world's main search engine since the beginning of the century, with a staggering 90% market share. However, with the growth of GPT, OpenAI's powerful language model, many believe that ChatGPT could dethrone Google as the primary tool for seeking knowledge on the internet. However, the argument that OpenAI poses an immediate threat to Google has some flaws:

First, OpenAI is not competing for ad space as the company currently derives revenue from subscriptions and API access. According to senior executives of OpenAI, there are no specific plans for developing an ad revenue stream at the moment. The main reason is that OpenAI does not want to compromise the user experience and the quality and truthfulness of the search results ChatGPT provides.

Second, with the enormous amount of expenses OpenAI is facing, it is highly unlikely it will further burden itself with spending more on infrastructure and tools related to advertising businesses.

Third, Google is developing its own AI product, Gemini LLM, and judging by the amount of resources they are willing to spend on it, it is unlikely to see Google trailing behind OpenAI with such significant margin.

Source: Menlo Ventures

Despite the fact that ChatGPT is not competing directly with Google in the advertising business, the rise of the OpenAI product still represents a certain treat to Google. If more users are switching to ChatGPT, less traffic towards the Google search engine would potentially mean less interest from advertisers to advertise on Google and that will lower the pricing for Google ads space. Currently, we do not see a clear trend towards this direction, but it will take a certain amount of time to see whether there is long-term trend for market share loss.

Google Monopoly Practices and 2024 Antitrust Ruling

The main factor that makes investors worried about Google is its recent legal troubles.

A U.S. federal judge recently ruled that Google has unlawfully maintained a monopoly in search and text advertising. The company is also under scrutiny from multiple states and territories in the U.S. for alleged antitrust violations. Google’s anti-competitive behavior can be seen from the following practices:

- Google has made deals with some of the largest device manufacturers like Apple and Samsung to ensure that Google is set as the default search engine on their devices.

- Google has also made deals with Android device manufacturers to ensure that the Google Play Store is the default app store on their devices.

- Google has been trying to oblige users to purchase from the Google Play Store only with Google Play Billing

- Google also pays developers to keep their apps on the Google Play Store and not distribute their apps through other platforms

Currently, it is hard to predict what the final ruling will be, but potential outcomes could involve breaking up parts of Google's business or eliminating exclusive contracts that reinforce its monopoly position. The decision is expected to be announced by August 2025.

Investors usually hate uncertainty, so any resolution, regardless of which form would bring more clarity to the market and potentially crystalize the real value of Alphabet. Additionally, with the recent change in the political landscape in the states, it is less likely to see big tech experiencing significant pressure from the authorities.

GOOGL as a Value Play

Among the Magnificent 7 stocks, GOOGL has the lowest multiple, with a trailing-twelve-months PE ratio of 25x. This valuation is particularly low for a tech giant with such a dominant business position.

The enterprise value (market capitalization minus cash) of Alphabet is $2.2 trillion. To put it in a comparative perspective, Meta, the direct advertising competitor, has $1.8 trillion enterprise value. This means, Alphabet is about 20% more valuable than Meta. However, the Alphabet advertising business is nearly 60% larger than that of Meta with $260 billion ad revenue for GOOGLE versus $160 billion ad revenue for META. Additionally, Alphabet has a top-performing cloud/enterprise software business, which Meta does not have.

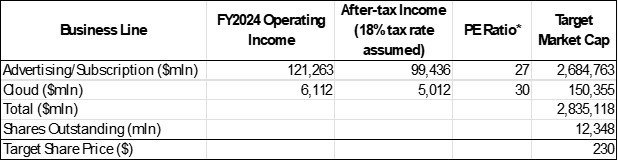

Alphabet can be viewed as having two main businesses – advertising and cloud. If we assign separate PE ratios to these segments, the target price will be around $230, roughly 30% upside potential from the current price.

*We use the current PE ratios of Meta for the advertising and subscription business and of Microsoft for the cloud business, respectively