What to Watch in Tesla’s Upcoming Q4 2024 Results

TradingKey - In the Artificial Intelligence (AI) space, the headlines have been grabbed by the big semiconductor names powering the AI revolution in markets.

However, one company that flew under the radar for most of 2024 was electric vehicle maker Tesla Inc (NASDAQ: TSLA). Of course, that changed in the run-up to the presidential election in November of last year, when Tesla CEO Elon Musk aligned himself with the eventual winner of the election – Donald Trump.

From the beginning of 2024 to the end of October 2024, Tesla shares were essentially flat. However, since the victory of Donald Trump, shares in the EV maker have soared 71% on optimism surrounding Musk’s relationship with Trump. But what about Tesla’s actual business?

Fortunately, investors will have an opportunity to see how it’s performing when Tesla reports its Q4 2024 and full-year earnings on Wednesday (29 January) after the market close. Here’s what investors should be watching.

With the profit upturn continue?

For Tesla, it’s been in turnaround mode for a few quarters given the intensely-competitive operating environment in China and a slowdown in overall EV sales in the US, with Tesla’s Q1 2024 revenue from EVs actually falling 13% year-on-year.

However, that situation seemed to be merely a blip for the company as Q3 2024 saw Tesla rock up with US$2.17 billion in net income, up 18% year-on-year while revenue from EVs ticked up for a third consecutive quarter with sales coming in at US$20 billion, up 2% year-on-year.

Total revenues for Q3 2024 came to US$25.1 billion, up 8% year-on-year, as Tesla’s energy generation and storage business posted an impressive 52% year-on-year revenue increase to US$2.4 billion.

So, what are analysts expecting for Tesla heading into this earnings print? Well, earnings per share (EPS) for Q4 2024 are expected to come in at US$0.65 on a diluted basis, implying a 14% year-on-year increase from the same period a year ago. In terms of actual 2025 full-year EPS, average estimates are for this to come in at US$2.85 – up a whopping 43.2% year-on-year from 2024’s expected EPS of US$2.60.

Vehicle deliveries hits record high

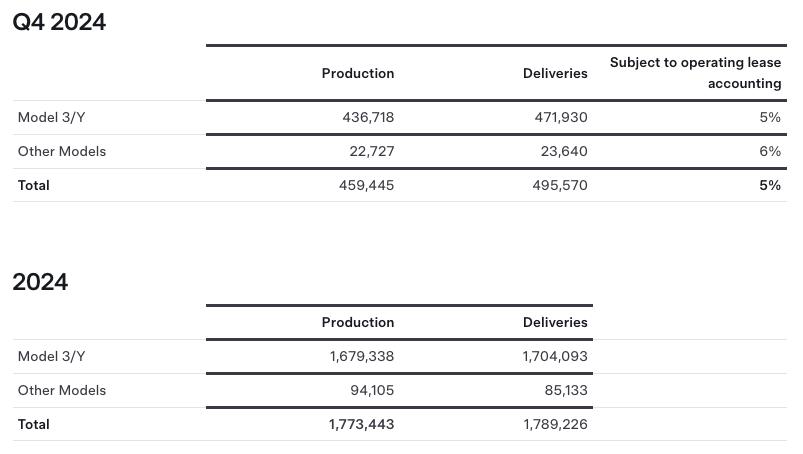

Tesla released its vehicle production and deliveries for Q4 2024 at the beginning of this month and the numbers looked promising. While production of EVs was slightly down sequentially – to 459,445 – vehicle deliveries was at a record high of 495,570.

Meanwhile, Tesla’s energy deployment hit a record high, too, of 11.0 gigawatt hours (GWh) of energy storage products.

Tesla’s Q4 2024 vehicle deliveries

Source: Tesla

Margins picture for gross and operating profits

There will also be more of a closer focus for investors on the margin profile – particularly that of Tesla’s pick-up EV (Cybertruck), which achieved a positive gross margin for the first time in Q3 2024.

In terms of overall gross margin, Tesla posted GAAP gross margin of 19.8% in Q3 2024 and that was up significantly from the 18.0% gross margin in Q2 2024. Whether that margin expansion can continue in Q4 2024 will be a key focus for investors.

Meanwhile, operating margin for Tesla hit double digits in Q3 2024, coming in at 10.8% and was up an impressive 323 basis points from the 7.6% in Q3 2023. An operating margin of 8.2% in Q4 2023 means the bar is relatively low for Tesla heading into the Q4 2024 earnings and if the company can surpass expectations on the operating margin front that could give investors confidence that 2025 will be a big year for Tesla.

How to think about Tesla earnings

Beyond just the numbers, though, investors will want to hear more concrete updates on other initiatives that Tesla has, such as the growth of its Full Self-Driving (FSD) system and “autopilot” autonomous feature for its EVS as well as the company’s much-touted Cybercabs.

With Tesla stock already up 12.5% so far in 2025, expectations could be said to be “elevated” as we head into the company’s Q4 2024 earnings.

However, with Tesla sitting on a cash pile of over US$33 billion and recording solid free cash flow of over US$2.7 billion in Q3 2024, investors could be forgiven for having confidence in the company’s upcoming results.