Nvidia: High Valuation But Will Maintain Robust Growth

Source: Yahoo Finance, Tradingkey.com

NVIDIA's stock price has soared by 2630% over the past five years, with a 206% increase year-to-date, and has been fluctuating within the $140-$150 range in the past month, reflecting the high level of market attention.

Business overview

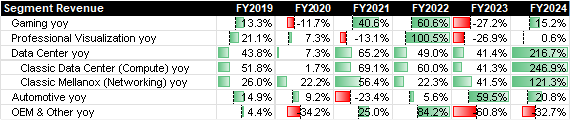

NVIDIA's business can be divided into five segments: Gaming, Professional Visualization, Data Center, Automotive, and OEM & Other. In FY2024, these segments accounted for 17.1%, 2.5%, 78%, 1.8%, and 0.5% of the company's total revenue, respectively. The Data Center segment's revenue has grown significantly, increasing from 34.3% in FY2019 to 78% in FY2024, with a growth rate of 216.7% in FY2024, making it the primary driver of NVIDIA's revenue growth.

Concurrently, NVIDIA has seen a steady improvement in gross margin and operating profit margin, while research and R&D expense ratio and SG&A expense ratio have declined.

Source: Company Data, Tradingkey.com

1.1 Gaming

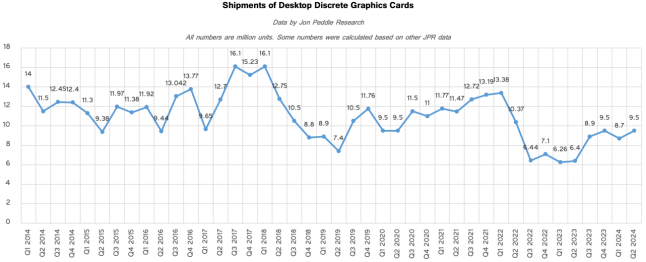

Jon Peddie Research data indicates that NVIDIA currently holds a strong number one market position in the discrete GPU (dGPU) market, with a market share of around 88%. AMD essentially accounts for the remaining share, with dGPU shipments in Q1 2024 reaching 8.7 million units, which is approximately 20% of the total GPU shipments.

1) The dGPU market has been recovering since Q2 2023, and with strong pricing power (ASP has significantly increased compared to 2017), which has led to increased revenue.

2) High premium capabilities also ensure a substantial gross margin for NVIDIA.

3) NVIDIA has stated that there may be a shortage of consumer-grade graphics cards in Q4 FY2025, and it is expected that the supply will improve by the beginning of next year with increased production. This could 1) ensure the demand for chips in data centers, and 2) lead to a price increase for RTX 40 series graphics cards, allowing the company to clear inventory at high prices before the release of the Blackwell products, which is beneficial for the company.

4) Competitor AMD is focusing more on expanding into the mid-to-low-end GPU market to gain more market share, which will strengthen NVIDIA's pricing power in high-end GPUs. Additionally, mainstream game developers are increasingly collaborating with NVIDIA, further reinforcing NVIDIA's competitive moat.

Therefore we project 21% yoy revenue growth for FY2025F.

Shipments and Market Share of dGPU

Source: Jon Peddie Research, Tradingkey.com

1.2 Data center

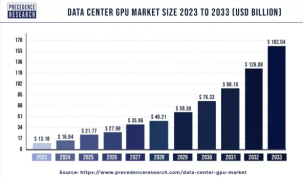

The industry space for data center GPUs is significant and growing rapidly. According to Precedence Research, the global data center GPU market size was estimated at USD 14.87 billion in 2023, and it is projected to be USD 17.92 billion in 2024. It is anticipated to expand to around USD 80.69 billion by 2030, registering a CAGR of 28.5% from 2024 to 2030. The increasing demand for artificial intelligence and the growth of the PC gaming and gaming console industries are key drivers propelling the expansion of the data center GPU market. However, a notable restraint is the high cost associated with data center GPUs, which can impact the market's growth.

Data Center Market Share Market Size

Source: Precedence Research, Tradingkey.com

2) As reported by HPCwire, Nvidia retained a 98% market share of the data center GPU market in FY2024, a figure that continued the dominance displayed by the company in FY2023.

3) Revenue of this segment grew 216.7% yoy, we’d love to discuss the following questions:

3.1) Does demand really exist?

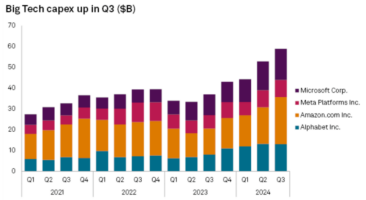

Big Tech companies have seen a sequential increase in their CAPEX since Q2 2023. Despite certain concerns regarding the implementation of AI applications, the market maintains an optimistic outlook due to the promising prospects in inference training, accelerated computing, and widespread applications. Meanwhile, NVIDIA, has been expanding its revenue streams by launching initiatives such as AI factories and AI enterprise, along with a broader range of products.

Source: S&P Global, Tradingkey.com

3.2) Could 1) high customer concentration, 2) major tech companies develop their own chip technology impact NVIDIA's revenue?

We thinks the impact is relatively small as NVIDIA's strengths lie in the following areas:

1) Mature CUDA Platform: With a vast software and application ecosystem, NVIDIA's CUDA platform has a large and growing developer community. This rich ecosystem enables cost-effective software innovation, driving demand and user growth.

2) High Switching Costs and Strong Customer Loyalty: CUDA's dominance makes it costly for customers to switch to other platforms, enhancing customer stickiness. Major tech companies still require large amount of time to accumulate technical expertise, amass training data, and ramp up production capacity.

3) Strong Technical Expertise and Customer Base: NVIDIA has accumulated significant technical prowess and a broad customer base over time.

4) Diverse Application Scenarios: NVIDIA's technology is adaptable across various scenarios, expanding its reach and application.

5) NVIDIA's continuous acquisitions, such as the acquisition of Mellanox, a leader in InfiniBand technology, are strategic moves to maintain technological advancement and high competitiveness. This acquisition has allowed NVIDIA to integrate accelerated computing with Mellanox's interconnect and storage capabilities, enhancing its position in high-performance computing and data center networking.

Development of NVIDIA’s Ecosystem Ecosystem

| 2021 | 2024 |

Developers | 2.5m | 5.1m |

CUDA Downloads | 26m | 53m |

AI Startups | 7k | 19k |

GPU-Accelerated Applications | 1700 | 3700 |

Source: Company Data, Tradingkey.com

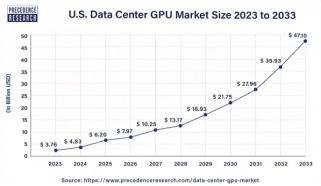

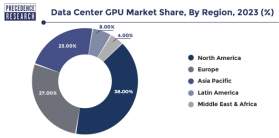

However, the Asia Pacific region accounts for 23% of the data center GPU market share in 2023. Geopolitical tensions between the U.S. and China, along with policy restrictions, may impact chip sales and shipments. Additionally, supply chain constraints, such as the switch from Monolithic Power Systems to Infineon Technologies as the primary PMIC vendor, could lead to temporary shortages of GB200 NVL server racks in Q4 FY2025.Above all, we project 134% yoy revenue growth for FY2025F.

Data Center GPU Market Sare by Region in 2023

Source: Precedence Research, Tradingkey.com

1.3 Physical AI

NVIDIA is at the forefront of the next AI revolution, focusing on Physical AI, which involves models that can interact with the physical world. This technology is set to transform robotic systems, from autonomous vehicles to industrial robots and humanoids. To build these Physical AI systems, NVIDIA relies on three key components: NVIDIA AI on DGX, NVIDIA Omniverse on OVX and NVIDIA AGX.

Enterprises are licensing NVIDIA Omniverse at a rate of $4,500 per GPU per year, indicating a significant investment in this technology. NVIDIA is also expanding its reach in robotics through partnerships with companies like BMW, which is using Isaac and Omniverse to train factory robots. Additionally, Boston Dynamics, BYD Electronics, Figure, Intrinsic, Siemens, and Teradyne Robotics are leveraging NVIDIA's technology stack to build various types of robots, including robotic arms and humanoids. These collaborations underscore NVIDIA's commitment to advancing the field of robotics and embedding AI capabilities into physical systems.

Valuation

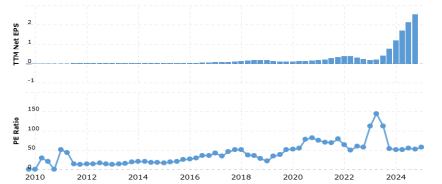

NVIDIA's current P/E ratio stands at 56x, which is considered mid-range over the past year. Despite its TTM P/E ratio being higher than industry peers, NVIDIA's EPS year-over-year growth is also significantly higher.

NVIDIA’s TTM EPS and P/E ratio

Source: Macrotrends, Tradingkey.com

We believe the current valuation of NVIDIA is not excessive, and we are confident that NVIDIA will maintain robust growth in the coming years, potentially becoming one of the most profitable companies in the market. NVIDIA allocated over $10 billion for share repurchase in Q3 FY2025, and this amount is likely to increase substantially in the next two years as profitability improves. We assign a P/E target range of 55x-65x for FY2026, corresponding to a target price of $162-$192.

Peer Comparison Consensus

Source: Seekingalpha, Tradingkey.com

Updated View of TESLA

Considering the intensifying competitive pressures, regulatory challenges, and significant overvaluation amidst deteriorating market conditions across key regions, we are transitioning our stance on Tesla from Hold to Sell.

Tesla's autonomous driving strategy shows fundamental flaws compared to competitors, particularly Waymo. While Tesla relies on a vision-only system, Waymo's multi-modal approach incorporating LiDAR, radar, and HD mapping has demonstrated superior safety metrics (one critical intervention per 17,000 miles vs. Tesla's intervention every few dozen miles). Tesla's hefty $1.1 trillion market cap is closely tied to the success of its autonomous driving technology. Amid skepticism and a lofty valuation, the company is exposed to considerable risk. In contrast, Waymo's robotaxi service, which has logged over 22 million autonomous miles, is on an expansion trajectory, with Miami set as the next destination for its fleet expansion next year. The company aims to offer paid rides to Miami residents by 2026.

The anticipated Trump administration is expected to eliminate the $7,500 EV tax credit, significantly impacting Tesla's pricing power. Notably, California's proposed state-level EV incentive program explicitly excludes Tesla, creating a competitive disadvantage in one of its largest markets. Meanwhile, competitors like Rivian are receiving substantial government support, including a $7 billion conditional loan from the Department of Energy.

Tesla faces competitive pressures in key markets: 1) China: Tesla faces declining year-over-year sales while domestic competitors are achieving higher revenues and maintaining rapid growth. 2) Europe: Lack of "home market" advantage and increasing restrictions on Chinese EVs create a challenging competitive environment. 3) United States: Rivian's expanding and potential production scale-up threaten Tesla's domestic market share.

Tesla’s TTM EPS and P/E ratio

Source: Macrotrends, Tradingkey.com

.jpg)