Asset Allocation in Developed Asia excluding Japan: Bullish on Australia and Taiwan Stocks

Executive summary

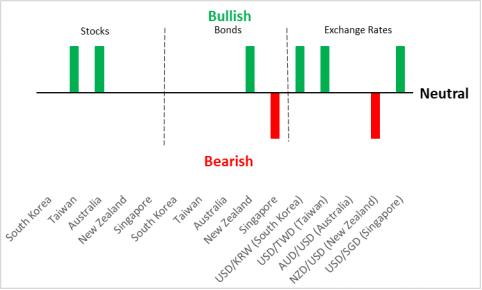

Short-term (<3 months) view

Source: Tradingkey.com

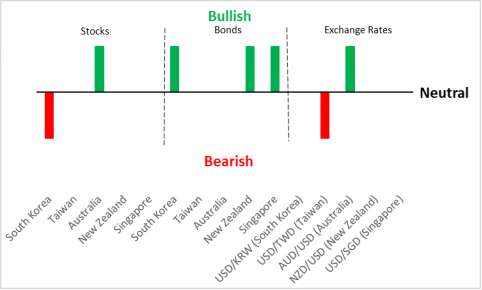

Medium-term (3-12 months) view

Source: Tradingkey.com

1. Macroeconomics

Due to the similarity of their economic structures and geographical proximity, economists consider South Korea and Taiwan as a pair, as well as Australia and New Zealand as another pair. In the past, the economic development of each pair was correlated. However, in recent years, the divergence has emerged. Currently, the economies of Taiwan and Australia are stronger than those of South Korea and New Zealand.

1.1 South Korea + Taiwan

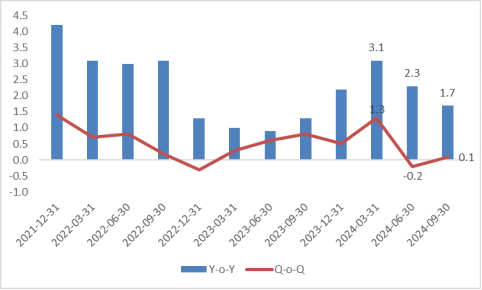

South Korea’s real GDP grew by -0.2% quarter-on-quarter in Q2 2024 and merely grew by 0.1% in Q3. In terms of year-on-year, the growth rate has continued to decline since the first quarter of this year (Figure 1.1.1). In the coming quarters, we believe that the Korean economy will continue to slow down. Domestically, the weakness of the labour market may limit household incomes, slowing the recovery of consumption. Due to the drag of the construction sector, investment is likely to be in a weak growth trend. In addition, Korea’s industrial production has also continued to cool down since the beginning of this year. In terms of external demand, as the Fed has begun an interest rate cut cycle and China has launched a series of policies to stabilize the economy, Korea’s exports have recovered slightly recently. However, it will take some time for these overseas policies to have a substantial effect on Korea’s exports. In the short term, Korea’s exports are expected to remain in a relatively weak position mainly driven by the depressed auto sector. As the economy is slowing down, the Korean government is expected to increase fiscal policy efforts. Meanwhile, following the recent unexpected 25bp interest rate cut by the Bank of Korea (BoK), we expect the central bank to further cut interest rates 2 or 3 times (25bp each) in 2025 to stimulate economic growth. On 3 December, South Korean President Yoon Suk Yeol suddenly declared martial law but lifted it a few hours later. As this incident was short-term and controllable, we do not expect it will have too much impact on the economy and the financial markets.

Figure 1.1.1: South Korea real GDP growth (%)

Source: Refinitiv, Tradingkey.com

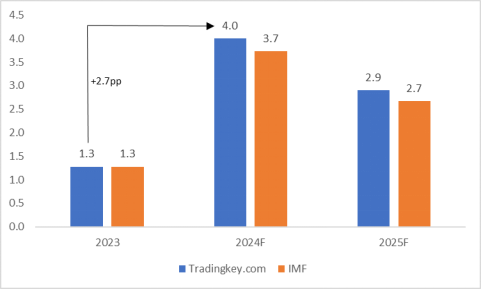

With favourable internal and external factors, we expect Taiwan's real GDP growth to reach 4% in 2024, higher than the IMF forecast of 3.7% and much higher than 1.3% in 2023 (Figure 1.1.2). In terms of internal factors, the weak consumption in the first three quarters of this year has shown a sign of recovery. Investment has begun to rebound since the second quarter. In addition, Taiwan's semiconductor sector has entered the stage of active inventory replenishment. The uptrend of the sector is expected to drive investment and economic growth. In terms of external factors, compared with last year, the volume of all products, especially tech products, has increased significantly since the beginning of this year. The export growth rate in October was 8.4%, in line with expectations. With the normalization of imports, net exports are expected to increase in the next few quarters. Against the backdrop of strong economic growth, we expect the Central Bank of the Republic of China (CBC) to be in no hurry to cut interest rates in H1 2025.

Figure 1.1.2: South Korea real GDP growth (%)

Source: IMF, Tradingkey.com

F: Forecasts

1.2 Australia + New Zealand

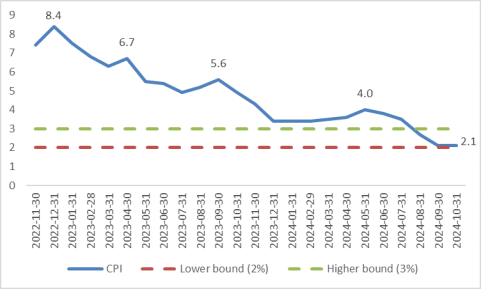

Despite no sign of recession, Australia's economic growth continues to slow, far below the past-year average. Compared with an average of 2.2% over the past five years, the IMF predicts that real GDP will grow by only 1.2% this year. The slowdown has also been reflected in weak productivity growth, with Australia's output per hour now back to the 2016 level. Looking ahead, Australia's economic growth may return to above 2% in 2025 due to the start of supportive fiscal policy. On the inflation front, although the headline CPI has fallen from a peak of 8.4% at the end of 2022 to 2.1% in October this year, close to the lower bound of the target, core inflation, measured by the trimmed mean CPI, increased to 3.5% (Figure 1.2.1). We expect the Reserve Bank of Australia (RBA) to delay cutting interest rates. Three reasons are as follows. First, the RBA’s monetary policy focuses more on the core CPI rather than the headline CPI; Second, the Australian economy is expected to pick up next year; Third, since most Australian mortgages are at variable rates and household debts are high, even a small scale of monetary easing will bring greater economic benefits. Therefore, the RBA may not cut interest rates before H1 2025.

Figure 1.2.1: Australia CPI (%)

Source: Refinitiv, Tradingkey.com

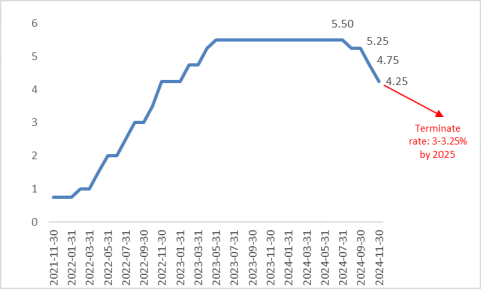

New Zealand's GDP has stopped growing for two years, and GDP per capita has continued to decline. Weakening consumption, suppressed investment, falling house prices and poor business sentiment are all driving forces for its slowing economy. In the labour market, the recent decline in both the employment rate and participation rate, together with slowing wage growth, has led to a rise in the unemployment rate from 4.6% in Q2 to 4.8% in Q3. In terms of inflation, the CPI decreased to 2.2% in Q3, falling into the Reserve Bank of New Zealand’s (RBNZ) target range of 1-3%. The decline in tradables inflation is the main driver of disinflation. On 27 November, the RBNZ announced a 50bp interest rate cut. Looking forward, due to weak growth and moderate inflation, we expect the central bank to further cut interest rates by 100bp or 125bp to 3.25% or 3% by the end of 2025 (Figure 1.2.2).

Figure 1.2.2: New Zealand policy rate (%)

Source: Refinitiv, Tradingkey.com

2. Stocks

2.1 South Korea + Taiwan

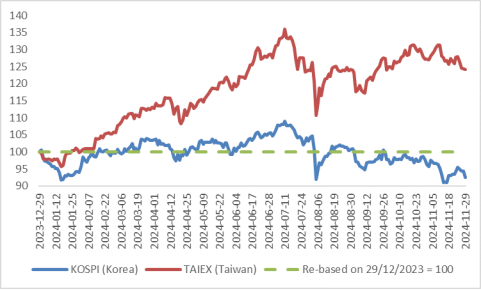

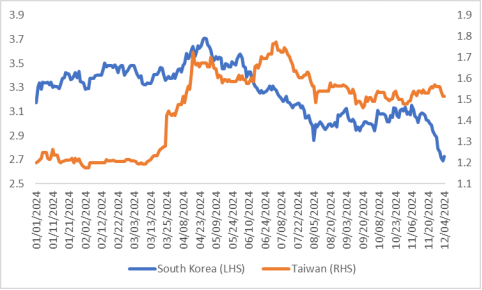

Calculating from the beginning of this year, South Korean stocks closed down while Taiwan stocks closed up (Figure 2.1). The main reason is the difference in economic strength between the two economies. Looking forward, the enthusiasm for AI in Asia is cooling down. This has started to harm the revenue and profits of Samsung, TSMC and other AI-related listed companies, putting pressure on these two stock markets. In the short term, South Korean stocks are unlikely to rise sharply due to the weak domestic economy and the decline in AI enthusiasm. On the other hand, due to the more BoK’s interest rate cuts, the stocks are unlikely to fall sharply either. Therefore, we are neutral on Korean stock prices. In the medium term, if interest rate cuts fail to substantially revive the economy, Korean stocks may re-start a downward trend.

Despite the cooling in AI enthusiasm, we are bullish on Taiwan stocks in the short term. Besides Taiwan's strong economy, which may push up the stock market, the recent continuous inflow of foreign capital is benefitting Taiwan stocks. As TSMC and other tech companies account for a large proportion of Taiwan's stock index, the performance of Taiwan stocks is similar to that of the US NASDAQ index. We are overweight US stocks, and so is Taiwan. In the medium term, we are neutral on Taiwan stocks. On the one hand, we expect the continued rise of US stocks to give Taiwan an upward push. On the other hand, the Taiwan stock valuation is above its 5-year average and ranks second in Asia, next to India. The high valuation, together with the possibility of the CBC's interest rate cuts being less than expected, will give Taiwan stocks a downward pull. The upward push and downward pull offset each other. Therefore, we expect Taiwan stocks to enter a choppy market after a short-term rise.

Figure 2.1: South Korea and Taiwan stocks

Source: Refinitiv, Tradingkey.com

2.2 Australia + New Zealand

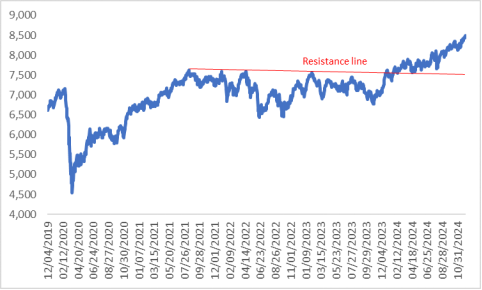

Since the beginning of 2024, after the S&P/ASX 200 broke through the resistance line, the stock index has been all the way up (Figure 2.2.1). So far this year, Australian stock prices have increased by 10.9%. Looking forward, we believe that the upward trend of the stocks may continue. Our reasons for being bullish are as follows. First, Australia's economic growth may accelerate. The GDP growth rate in 2025 is expected to be about 1 percentage point higher than that in 2024. Second, Australia’s fiscal policy is turning to be more supportive, boosting the domestic demand. Third, China has introduced a series of economic stabilization policies that will increase domestic demand in China. As the largest export destination, the recovery of the Chinese economy may benefit Australia's exports of commodities such as iron ore and coal, pushing up the revenue, profits and stock prices of Australia-listed mining companies.

Figure 2.2.1: S&P/ASX 200

Source: Refinitiv, Tradingkey.com

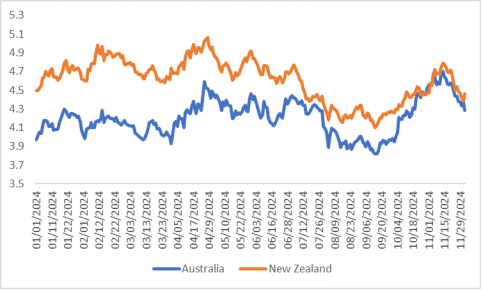

It seems that New Zealand stocks have denied the weakness of its economy, with the S&P/NZX 50 index following Australia’s S&P/ASX 200 breaking through the resistance line (Figure 2.2.2). However, the booming stock market is expected to come to an end. We believe that “the stock market is a barometer of the economy” is about to be priced in. With the offset of economic weakness and the RBNZ’s significant interest rate cuts, New Zealand stocks may enter choppy trading.

Figure 2.2.2: S&P/NZX 50

Source: Refinitiv, Tradingkey.com

3. Bonds

3.1 South Korea + Taiwan

Similar to the stock markets, a divergence in the yields of South Korean and Taiwan government bonds has arisen since October this year (Figure 3.1). Since April, the 10-year Korea Treasury Bond (KTB) yield has continued to fall, from the highest level of around 3.7% to the current level of around 2.7%. Looking forward, in the short term, we believe that KTB yields may stop one-way falling and fluctuate at a low-level range. On the one hand, the total issuance of Korean government bonds is planned to reach 201.3 trillion won next year, 27% more than this year. Based on this plan, the net issuance will increase by 68%. On the other hand, the expectation of KTB joining the FTSE World Government Bond Index (WGBI) may lead to investors rushing to buy the bonds, increasing the demand. As the Korean real estate market continues to cool down, loan growth may slow further, causing Korean banks to turn their attention to more cost-effective KTB. In short, the offset of supply and demand makes our view neural on KTB. In the medium term, the weak economy and moderate inflation may result in the BoK continuing to cut interest rates. This, together with the spillover effect of the medium-term decreasing of US Treasury yields, may drive KTB yields to re-start to fall.

By observing the last Fed's rate-cut cycles, we found that Taiwan's sovereign bond yield curve has a low correlation with the US yield curve. The expected short-term rise and medium-term decline of US yields are unlikely to have much impact on Taiwan's yields. Therefore, internal factors are the main driving force for Taiwan's yields. Although the CBC is expected to have ended the rate-hike cycle, due to the strong economic growth, the overheated real estate and the continued growth of private sector leverage, the central bank may increase the reserve requirement ratio (RRR) in the next few months. However, the recent rise in Taiwan's yields may have priced in the impact of the rise in RRR. Therefore, we do not expect Taiwan's yields to rise or fall significantly in the short and medium term.

Figure 3.1: South Korea and Taiwan 10Y government bond yields (%)

Source: Refinitiv, Tradingkey.com

3.2 Australia + New Zealand

The RBA is unlikely to cut interest rates before the first half of next year. Even if the central bank starts to cut interest rates in H2 2025, the extent of the cuts is expected to be limited. We believe that Australian government bond yields are not expected to fall sharply. With the backdrop of high commodity prices and the strong domestic labour market, the net issuance of Australian government bonds was low in the past two years. As Australia's fiscal policy has begun to turn to supportive, in theory, the government needs to issue more bonds to finance its spending. However, according to Australian budget forecasts, the total issuance of government bonds in FY2024/2025 will be AUD90 billion, with a net issuance of AUD7.2 billion, which is only about half of last year. The continued low bond supply may make the yields difficult to rise sharply. Due to being unlikely to increase or decrease much, we believe that the yields will enter a choppy market (Figure 3.2). On the other hand, New Zealand's government bond prices are likely to rise with the backdrop of the RBNZ's significant reduction in policy interest rates.

Figure 3.2: Australian and New Zealand 10Y government bond yield (%)

Source: Refinitiv, Tradingkey.com

4. Exchange rates

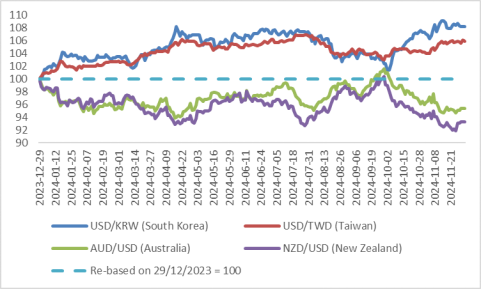

We expect the US dollar index to rise in the short term, affecting the exchange rates of all non-US currencies to various extents (Figure 4). The South Korean won (KRW) and the New Zealand dollar (NZD) are expected to be the most affected. This is because the central banks of these two countries may significantly cut interest rates, which may drive their exchange rates to fall further. Compared with the KRW and the NZD, the New Taiwan dollar (TWD) is not expected to depreciate much because the CBC does not expect to cut interest rates within the next six months. Among the four currencies, the only one that is not expected to fall is the Australian dollar (AUD). The 10-year real yield of Australian government bonds is similar to that of US government bonds, which is the highest among G10 countries. This has increased the attractiveness of the AUD. Compared to other central banks, the RBA's late and shallow interest rate cuts may cause the AUD to outperform the NZD, EUR, GBP and CAD.

Figure 4: Exchange rates

Source: Refinitiv, Tradingkey.com

5. Singapore

Under the impacts of external factors such as the Trump Trade, re-inflation, the US dollar and US Treasury yields going up, as well as internal factors such as the Singaporean economy growing at a rate close to its potential and the monetary policy stance remaining unchanged, we are neutral on Singapore's stocks, bearish on the government bonds, and bullish on the USD/SGD. For details, please read our report on Asset Allocation in India and ASEAN-6: Bullish on Indonesian Stocks published on 3 December 2024.