2025 Outlook: Robust Growth and Enhanced Stock Returns

By Jason Tang, Petar Petrov, Viga Liu

Executive Summary

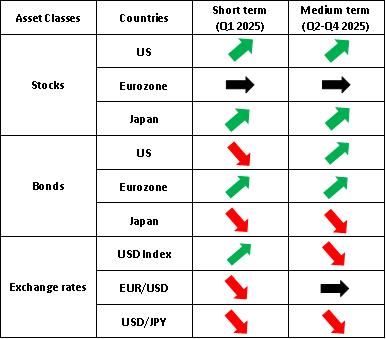

The main theme in 2024 was the decline in global inflation and the central banks' interest rate cut cycles. Looking ahead to 2025, the macroeconomic focus may shift towards ongoing interest rate cuts and stronger-than-expected global growth. In the context of robust economic growth, we are bullish on global stock markets, particularly US and Japanese equities. In the bond markets, driven by the combined effects of the Trump Trade and the Fed’s interest rate cut cycle, US Treasury yields are expected to rise initially and then fall. Due to the divergent monetary policies of the European Central Bank and the Bank of Japan, German yields are expected to decline, while Japanese yields will rise. In the foreign exchange markets, the USD Index may follow US Treasury yields, rising initially before experiencing a decline. Influenced by the US dollar's trend, the euro is expected to weaken initially and then stabilize, while the yen is anticipated to continue appreciating throughout 2025.

Throughout 2024, we witnessed stable growth in US equities across different industries, making passive index investing a straightforward path to achieve generous investment returns. However, with emerging and ongoing risks, related to politics, potential inflation and high valuations, we will probably observe a divergence in the performance across sectors and individual companies. Thus, we believe investors should look for sectors and companies with high quality that are well-positioned to face the potential challenges. We see solid foundations in banking, healthcare, semiconductor and energy stocks to outperform in 2025.

The 2025 commodities market is shaped by geopolitical shifts, evolving supply-demand dynamics and structural trends. The crude oil market faces a transition from tight balance to oversupply by mid-2025, driven by non-OPEC production growth. OPEC+ policies and geopolitical risks, including US-Russia relations and Middle East tensions, will influence prices, projected to range between $75-$85 per barrel. As a safe-haven asset, gold benefits from geopolitical risks, inflation concerns and strong central bank demand. While price growth may moderate, gold remains bullish, with the potential to reach $3,000 in 2025. Broader institutional adoption and more favourable regulations, fuelled by spot ETF inflows and potential pro-crypto policies, are expected to drive Bitcoin for strong growth in 2025.

Part 1: Macro and Multi-Asset Analysis

(by Jason Tang)

Macroeconomics

In 2024, global inflation gradually declined, prompting major central banks to enter a rate-cutting cycle, with the Bank of Japan (BoJ) being a notable exception. Supported by a robust labour market and a rebound in international trade, the global economy showed signs of recovery, though its growth rate remained below pre-pandemic levels.

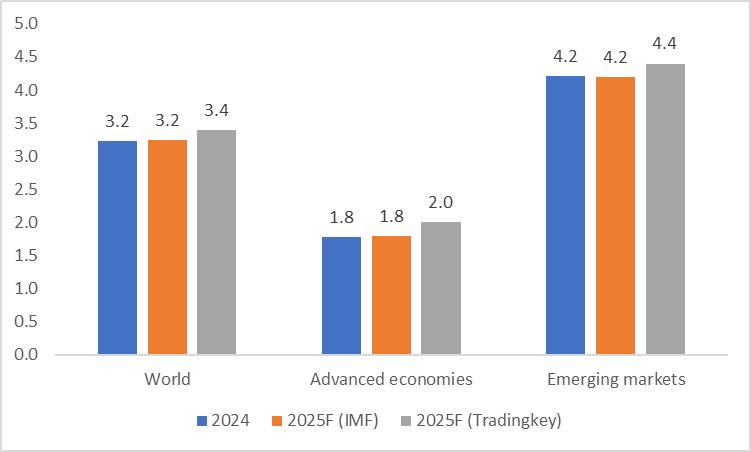

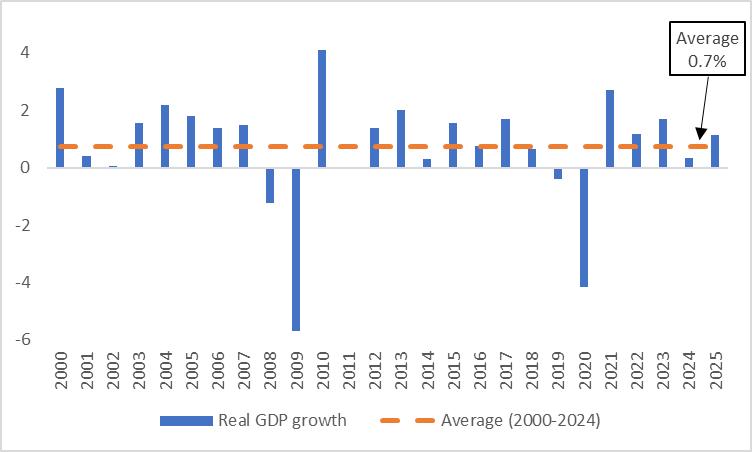

Looking ahead to 2025, the US economy is expected to maintain its resilience, while China's economic recovery is gaining momentum, spurred by a series of stabilization policies. Compared to the IMF's forecasts, we hold a more optimistic outlook for global GDP growth in 2025 (Figure 1). Sustained growth in consumption and investment, coupled with central banks' continued reduction of policy interest rates, suggests that developing economies may perform better than previously anticipated.

This article provides an in-depth analysis of the macroeconomic conditions and financial markets of developed economies, focusing on the US, the Eurozone and Japan.

Figure 1: 2025 GDP forecasts, IMF vs. Tradingkey (%)

Source: IMF, Tradingkey.com

US Macro

The US economy in 2024 oscillated between the possibilities of a hard landing and a soft landing but ultimately demonstrated resilience, with growth exceeding early-year expectations. Now that the election has concluded, the US economy in 2025 will primarily be shaped by two factors: Trump’s policies and the Fed’s interest rate cut cycle.

Trump’s tax cuts and policies encouraging the repatriation of manufacturing are likely to boost US economic growth. However, his stricter immigration policies and increased tariffs may raise concerns about re-inflation.

On the fiscal front, Trump advocates significant tax reductions. While he aims to offset fiscal deficits through higher tariffs, the trends of increasing deficits and rising public debt are expected to persist in 2025.

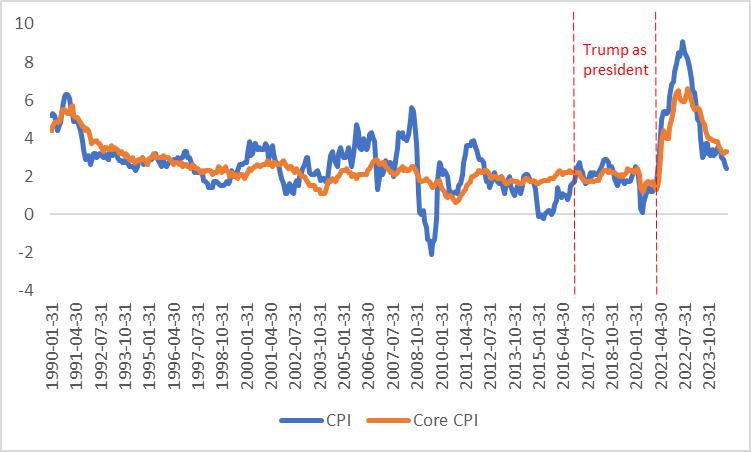

In terms of monetary policy, stronger economic growth and rising inflationary pressures have begun to slow the pace of the Fed’s rate cuts. However, a review of Trump’s first term suggests that his policies did not lead to high inflation (Figure 1.1). If inflation remains under control during this term, the Fed may have greater flexibility to reduce interest rates than projected in our baseline scenario.

Figure 1.1: US inflation (%)

Source: Refinitiv, Tradingkey.com

Eurozone Macro

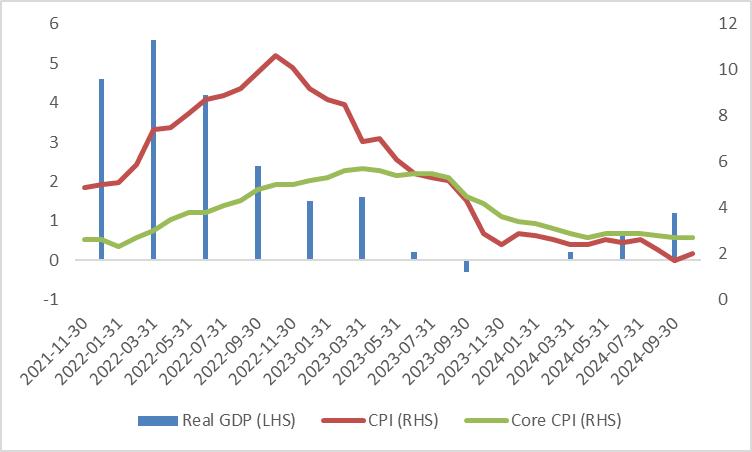

In the first three quarters of 2024, the eurozone economy grew at a faster pace than in the second half of 2023, signalling a recovery. However, the growth rate remains below the levels seen in 2021 and 2022, indicating that the recovery is still fragile.

On the inflation front, both the headline CPI and core CPI have fallen significantly from their peaks in 2022–2023. Core CPI is projected to decline further in 2025 (Figure 1.2).

The eurozone's economic outlook faces additional uncertainty from tariff measures implemented by the Trump administration. In June 2018, Trump imposed tariffs of 25% on EU steel imports and 10% on aluminium imports, citing national security concerns. He also proposed a 20% tariff on EU automobile and auto parts imports, although this was not enacted. In 2025, Trump is expected to escalate tariffs further and may pressure Europe to follow the US in decoupling from China. Additionally, his preference for bilateral trade agreements with individual EU member states could undermine EU unity and exacerbate political divisions within the eurozone.

Amidst weak recovery, low inflation and the impact of Trump’s tariff policies, the European Central Bank (ECB) is anticipated to cut interest rates 4–6 times in 2025, with each cut amounting to 25bp, to support economic stability.

However, if Trump succeeds in mediating the Russia-Ukraine conflict and achieving a ceasefire this year, the eurozone economy could perform better than our baseline scenario.

Figure 1.2: Eurozone real GDP and CPI (%)

Source: Refinitiv, Tradingkey.com

Japan Macro

The Japanese economy experienced low growth in 2024, primarily due to weak domestic consumption and insufficient external demand. Looking ahead to 2025, two key factors may contribute to economic improvement: rising wages and economic stimulus measures.

Wage growth during the 2025 Shuntō negotiations is expected to exceed 5%, significantly outpacing inflation. This suggests that real wage increases could stimulate consumer spending. Additionally, in November 2024, the Japanese government unveiled a 21.9 trillion yen economic stimulus plan. Supported by higher wages, increased consumption and fiscal stimulus, the IMF projects Japan's real GDP growth to reach 1.1% in 2025, a notable improvement from the 0.3% growth recorded in 2024 (Figure 1.3).

On the inflation front, Japan's headline CPI and core CPI (excluding fresh food) rose to 2.9% and 2.7%, respectively, in November 2024, up from 2.3% in October. Despite these increases, the Bank of Japan (BoJ) has maintained a cautious approach to normalizing monetary policy.

However, we anticipate the BoJ will implement three rate hikes in 2025—one in early 2025, another mid-year and a third in late 2025—each amounting to a 25bp increase.

Figure 1.3: IMF forecasts of Japanese real GDP growth (%)

Source: IMF, Tradingkey.com

Multi-Assets

Stocks

US Stocks

Although the US stock market has experienced a correction since December 2024, Trump's tax cuts and interest rate cuts remain supportive of the market. We are bullish on the US stock market in 2025.

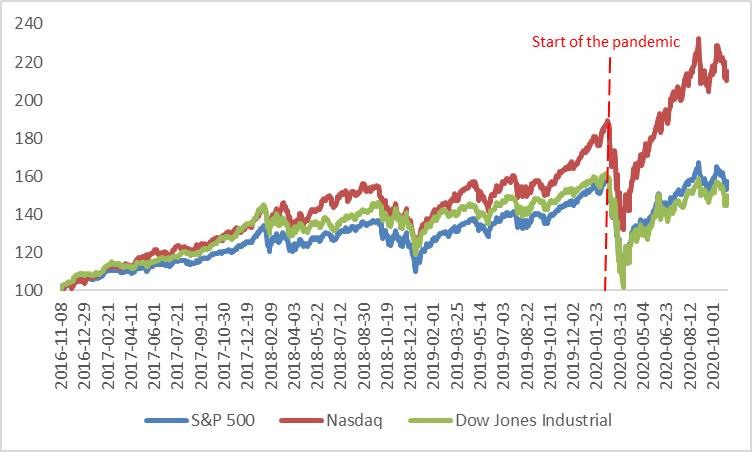

During his first term (from his election on 8 November 2016 to his defeat on 3 November 2020), despite being in a period of the Fed's interest rate hike cycle and the challenges posed by the pandemic, Trump's policies contributed to significant market gains. The S&P 500, Nasdaq and Dow Jones Industrial Average rose by 57.5%, 114.9% and 49.9%, respectively—outperforming the historical averages (Figure 3.1.1). In 2025, Trump's continued push for tax cuts is expected to further benefit the stock market.

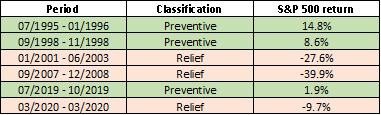

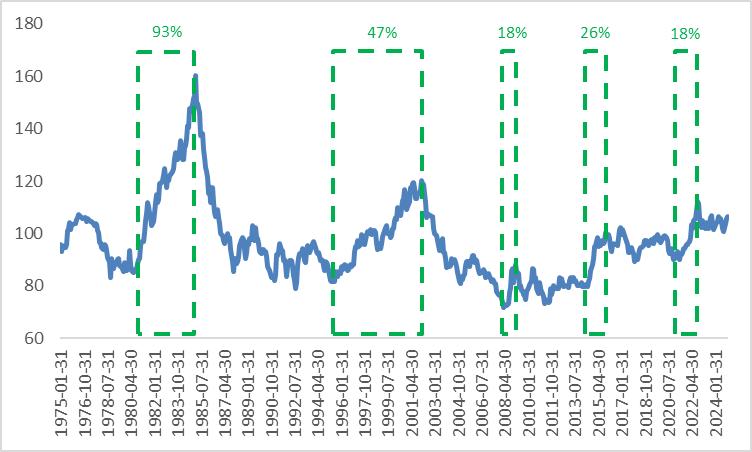

Interest rate cut cycles can be categorized into two types: Relief and Preventive. Of the six interest rate cut cycles in history, three were relief cuts, triggered by economic recessions. During these periods, the negative impacts of the recession outweighed the positive effects of rate cuts, resulting in a stock market decline. The remaining three were preventive rate cuts, implemented in response to economic slowdowns rather than recessions. In these cases, the positive effects of rate cuts were larger than the negative impacts of slower growth, leading to an upward market trend (Figure 3.1.2).

Looking ahead to 2025, the US economy is expected to remain resilient, with a soft landing being a high-probability scenario. As such, this interest rate cut cycle is likely to be preventive, with a net positive effect on the stock market.

However, risks to the US stock market remain. High valuations, the potential for re-inflation and growing public debt could trigger a periodic market decline.

Figure 3.1.1: US stock performance during Trump’s first term

Source: Refinitiv, Tradingkey.com

Note: Re-based 8 November 2016 = 100

Figure 3.1.2: S&P 500 return during rate cut cycles

Source: Refinitiv, Tradingkey.com

Eurozone Stocks

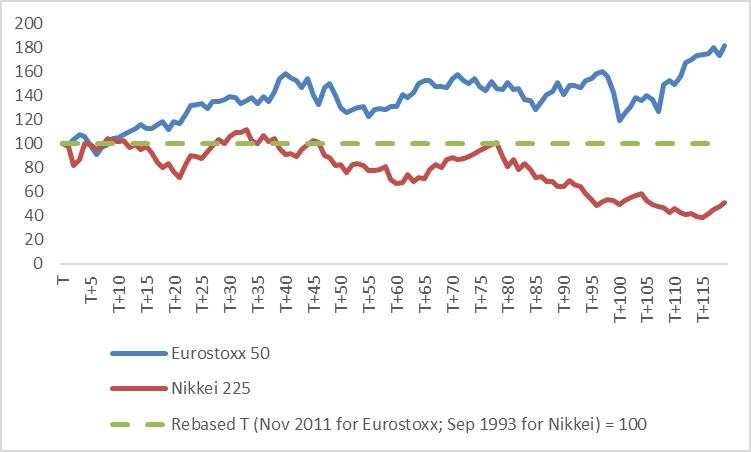

The eurozone is expected to enter a period of low interest rates in 2025. Looking at history, the eurozone began its low-interest rate era in November 2011, one year after the European debt crisis. In the following decade, the eurozone stock market performed relatively well. In contrast, Japan entered its low-interest rate period in September 1993, three years after its asset bubble burst. Over the next decade, Japan's stock market experienced a prolonged bear market (Figure 3.2).

As the eurozone enters this new low-interest rate era, the question arises: Will its stock market follow the path of prosperity seen in the past, or will it mirror the Japanese-style long bear market? To answer this, we need to analyse the underlying factors that influenced the stock markets in both regions during their respective low-interest rate periods.

One key similarity between the two markets is that both attracted foreign capital inflows during their low interest rate periods. However, the Japanese stock market benefited from strong government intervention, while the European stock market saw increased stock investment from the private sector, in contrast to the Japanese private sector, which reduced its stock investment.

That said, in developed markets, private sector investment has been the decisive factor in stock market performance. Therefore, the future performance of the eurozone stock market in 2025 will largely depend on the effectiveness of the eurozone's fiscal and monetary policies. If these policies successfully encourage the private sector to increase stock investments, the eurozone stock market could regain its former strength; otherwise, it may struggle.

Given the uncertainty surrounding the outlook, we assign a neutral rating to eurozone stocks. However, we do caution about potential downside risks, particularly due to Trump’s tariff policies.

Figure 3.2: Eurozone vs. Japanese stock performance during low-interest rate periods (monthly data)

Source: Refinitiv, Tradingkey.com

Japan Stocks

After the economic bubble burst in 1990, the Japanese stock market entered the "Lost Decades" (1990–2010). During this period, while the overall trend was downward, there were three periodic bull markets. Since May 2012, however, Japanese stocks have experienced a sustained and significant bull market (Figure 3.3). The driving forces behind these four bull markets—three short and one long—were shifts in domestic and international policies, as well as improvements in economic expectations both at home and abroad.

Looking ahead to 2025, domestic and international factors suggest a positive outlook for the Japanese stock market. Domestically, while the effects of expansionary fiscal policy may be tempered by contractionary monetary policy, Japan's economic growth in 2025 is projected to significantly surpass that of 2024.

Internationally, major central banks have entered a cycle of interest rate cuts, gradually improving the global financial environment. Meanwhile, the US economy continues to demonstrate resilience and China's economy is recovering, driven by a series of stabilization measures. These global dynamics, combined with domestic improvements, create a favourable environment for the Japanese stock market in 2025.

Figure 3.3: Nikkei 225

Source: Refinitiv, Tradingkey.com

Other stock markets

In addition to major economies, we are optimistic about the stock markets of Australia, Hungary, Indonesia and Taiwan in 2025 for the following reasons:

· Australia: Domestic demand is expected to increase and economic growth is projected to accelerate, driven by expansionary fiscal policies. Additionally, China's stimulus measures are likely to boost export demand for Australian products, further supporting economic and stock market performance.

· Hungary: After entering a technical recession in mid-2024, the Hungarian government implemented a series of measures to stabilize the economy, creating a favourable environment for the stock market. The Hungarian central bank (Magyar Nemzeti Bank, MNB) has recently adopted a more hawkish stance, which is beneficial to the financial sector—the largest component of the Hungarian stock index. Moreover, two-thirds of the revenue of Hungarian-listed companies comes from overseas markets. These firms are expected to benefit from the continued global economic recovery in 2025.

· Indonesia: The Indonesian government has shown greater tolerance for debt, making it more likely to stimulate economic growth through increased financing. A favourable economic outlook is expected to drive earnings growth for listed companies. Indonesian stock valuations are currently well below their 10-year average, making the market attractive for investors.

· Taiwan: Taiwan's previously weak consumption has shown signs of recovery and investment activity has rebounded. The semiconductor industry, a cornerstone of Taiwan’s economy, has entered a new inventory replenishment cycle, which is expected to drive investment growth. Technology stocks, including TSMC, have a significant weight in Taiwan's stock index. This high-tech focus makes its stock market trend closely aligned with that of the Nasdaq index. Given our bullish outlook on US stocks, we are similarly optimistic about the Taiwan stock market.

Bonds

US Bonds

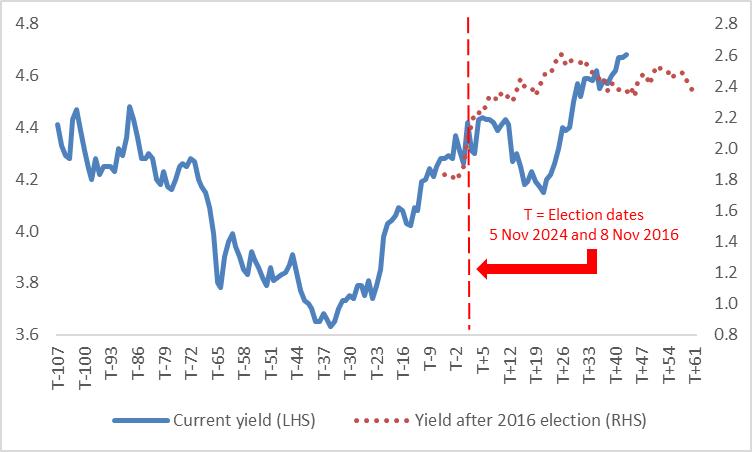

We anticipate that the 10-year US Treasury yield will rise initially and then decline in 2025. On the Trump Trade front, following Trump's previous election victory on 8 November 2016, concerns about re-inflation driven by his policies led to a one-month rise in the 10-year yield, which then gradually declined. After Trump’s re-election on 5 November 2024, US Treasury yields have exhibited fluctuations, but the overall trend remains upward (Figure 4.1.1).

On the interest rate cut front, historically, in five out of the past six interest rate cut cycles, the 10-year yield fell (Figure 4.1.2). However, in this current rate-cut cycle, the 10-year yield has risen instead of declining. Economists have attributed this anomaly to two key factors:

· Trump Trade: The expectation of higher inflation due to Trump's policies has pushed yields higher.

· Nature of Recent Rate Cuts: In prior cycles, interest rate cuts were typically deeper and longer, with the policy rate bottoming below the low point of the previous cycle. In contrast, the current rate-cut cycle has been less aggressive, leading to reduced market expectations for further declines.

In the short term, we agree with the prevailing view that yields will continue to rise, likely peaking by the end of the first quarter of 2025.

In the medium term, as the effects of the Trump Trade diminish and the market fully prices in the "slower-than-expected rate cuts", we expect US Treasury yields to begin a gradual decline from the second quarter onward. If Trump’s policies do not lead to a significant resurgence in inflation, the downward adjustment in yields could occur faster than currently anticipated.

Figure 4.1.1: 10Y US government bond yield (current vs. after 2016 election, %)

Source: Refinitiv, Tradingkey.com

Figure 4.1.2: US government bond yields during rate cut cycles (bp)

Source: Refinitiv, Tradingkey.com

Eurozone Bonds

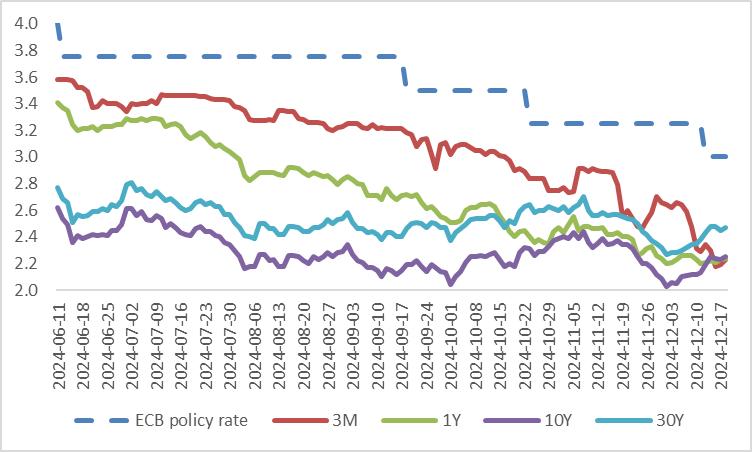

Since 12 June 2024, the European Central Bank (ECB) has embarked on a rate-cutting cycle, with cumulative reductions totalling 100bp to date. This policy shift has driven the entire German yield curve downward, with the most pronounced declines seen in short-term (front-end) yields. Short-term yields are primarily influenced by changes in policy rates, whereas long-term (back-end) yields reflect broader economic fundamentals.

Since the start of the rate-cutting cycle, the yields on German government bonds for 3-month, 1-year, 10-year and 30-year maturities have declined by 135bp, 117bp, 37bp and 30bp, respectively (Figure 4.2). This has resulted in a steeper yield curve as the downward shift has been more significant at the short end.

Looking ahead to 2025, the ECB is expected to continue its rate-cutting trajectory, further reinforcing the downward shift and steepening of the German yield curve. Additionally, the yields on French and Spanish government bonds are likely to decrease in tandem with German yields.

However, rising political uncertainty in France may lead to a widening spread between French and German government bond yields, reflecting increased risk premiums for French debt.

Figure 4.2: ECB policy rate vs. German government bond yields (%)

Source: Refinitiv, Tradingkey.com

Japan Bonds

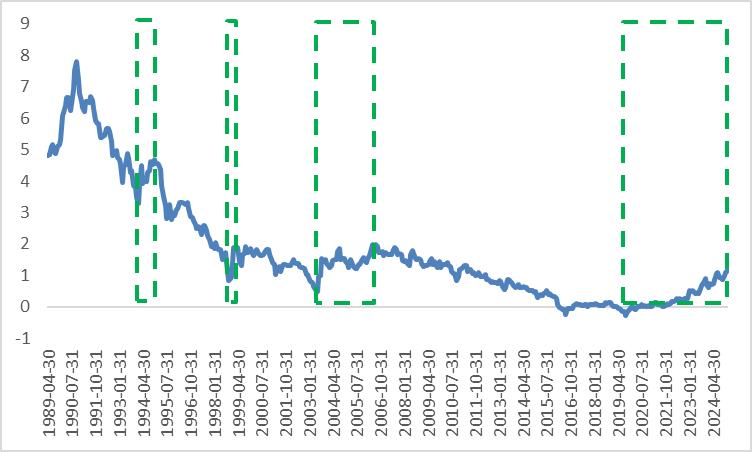

From 1990 to 2019, the Japanese bond market experienced a prolonged bull market. Amid the "Lost Decades" of economic stagnation, policy interest rates dropped to negative levels and bond yields followed a continuous downward trend. However, within this extended bull market, there were three notable periods of yield rebounds: 1) January to November 1994; 2) October 1998 to September 1999; 3) June 2003 to July 2006 (Figure 4.3).

These three episodes of yield increases shared several common factors:

· Temporary Economic Recovery: A brief improvement in the Japanese economy spurred market optimism.

· Increased Government Bond Issuance: Fiscal stimulus policies led to higher issuance of government bonds.

· Resonance with US Treasury Yields: Rising US Treasury yields created a spillover effect on Japanese bonds.

Looking at the current context, all three conditions are present again today. In addition, the Bank of Japan (BoJ) has initiated a rate hike cycle, further contributing to upward pressure on yields. Given these factors, we anticipate that the Japanese bond market will enter a bear market phase in 2025.

Figure 4.3: 10Y Japanese government bond yield (%)

Source: Refinitiv, Tradingkey.com

Exchange Rates

USD Index

Similar to US Treasury yields, we expect the USD Index to rise in the short term, driven by the dominance of Trump Trade in the market. This upward trend is likely to persist through the first quarter of 2025. In the medium term, however, the focus will shift to the Fed’s interest rate cut cycle, leading to a gradual decline in the USD Index. However, could the dollar remain stronger than expected in 2025?

To evaluate whether the USD Index could stay elevated throughout the year, we examine the historical patterns of dollar appreciation. Since the collapse of the Bretton Woods system and the creation of the USD Index, the dollar has experienced five major appreciation cycles—two long and three short (Figure 5.1).

By analysing these cycles, we identify five key conditions for the US dollar to sustain a medium- to long-term upward trend: 1) Rising inflation levels; 2) A Fed interest rate hike cycle; 3) Divergence in the US and European monetary policies; 4) Exceptional strength in the US economy; 5) A global economic crisis.

At present, none of these conditions are being met. Inflation remains under control, the Fed is in a rate-cutting phase and US monetary policy aligns with other major economies. Additionally, while the US economy shows resilience, it is not experiencing exceptional outperformance. The global economic environment also lacks the kind of crisis that typically drives a prolonged dollar rally.

Given these factors, the likelihood of the USD Index maintaining a sustained upward trend throughout 2025 is low.

Figure 5.1: US dollar upward cycles

Source: Refinitiv, Tradingkey.com

EUR/USD

After the US election, the euro has lagged behind other major currencies. Looking ahead to 2025, the euro’s performance against the US dollar is expected to be influenced by three main factors: 1) Divergence in economic growth between the US and the eurozone; 2) The different pace of inflation declines in the two economies; 3) Trump’s policies.

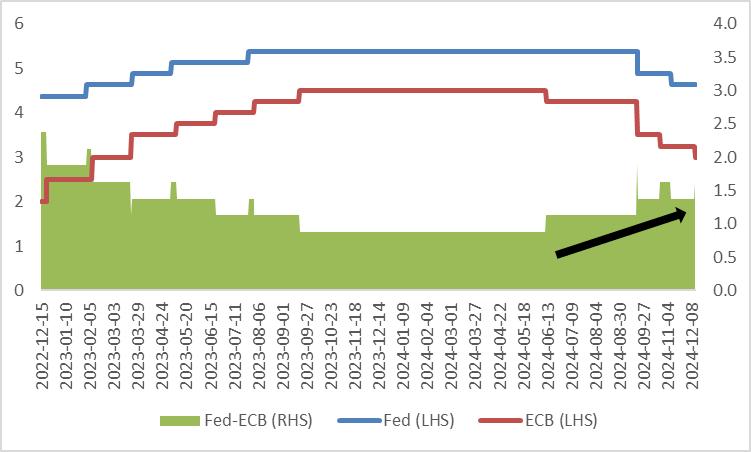

Regarding the first two factors, in 2025, the European Central Bank (ECB) will likely focus on addressing weak economic growth, while the Fed will concentrate on alleviating pressures from reflation. As a result, we expect the ECB to adopt a more aggressive rate-cutting strategy compared to the Fed, which could widen the policy interest rate gap between the US and Europe (Figure 5.2).

In addition to the monetary policy divergence, political unrest in Germany and France could further constrain fiscal spending, adding continued downward pressure on the euro against the dollar, particularly in the first quarter of 2025.

In terms of Trump’s impact on the euro, as discussed in the Macroeconomics section, Trump’s high tariffs and efforts to force the EU to decouple from China could negatively impact eurozone exports, which is generally bearish for the euro.

However, starting in the second quarter of 2025, we expect a decline in the USD Index. This could lead the euro to enter a period of choppy trading against the dollar as market dynamics evolve.

Figure 5.2: Fed vs. ECB policy rates (%)

Source: Refinitiv, Tradingkey.com

USD/JPY

As noted earlier, the Japanese bond market experienced a prolonged bull run from 1990 to 2019, with three notable periods of yield rebounds. Similar to other developed countries, Japanese bond yields and the yen tend to exhibit a degree of correlation. During these three periods of yield recovery, the yen also strengthened (Figure 5.3).

After 2021, however, Japanese bond yields and the yen began to diverge, largely due to the appreciation of the US dollar.

Looking ahead, we expect the dollar to enter a bear market starting in the second quarter of 2025. This, coupled with monetary policy divergence between the Fed and the Bank of Japan (BoJ), as well as the upward trajectory of Japanese bond yields, supports our view that the yen will enter a bull market in 2025.

Figure 5.3: 10Y Japanese government bond yield vs. USD/JPY

Source: Refinitiv, Tradingkey.com

Risks

If geopolitical tensions, escalating trade protectionism and intensifying reflationary pressures exceed expectations in 2025, the global macroeconomic environment and financial markets could face heightened risks. These challenges may lead to declines in global stock markets, rising bond yields and sustained strength in the USD Index.

Part 2: Investment Opportunities across US Stock Sectors

(by Petar Petrov)

No Recession, So Now What…?

Many would think 2025 will be smooth, as the recession is largely avoided. However, we believe the new year will be more challenging for equity investors.

After the post-Trump election rally, it is safe to say that the positive aspects of Trump’s future policies are reflected in the market prices but less so are the risks associated with tariffs and trade restrictions. The opposite direction is also valid, as Trump may backtrack on some of the policies he talked about during his presidential campaign, causing further market shifts.

Equity investors need to worry about the resurgence of inflation due to potential tariff policies and resilient consumer spending. This could mean less aggressive rate cuts from the Fed, which would translate into higher-than-expected discount rates and a headwind for equity valuations.

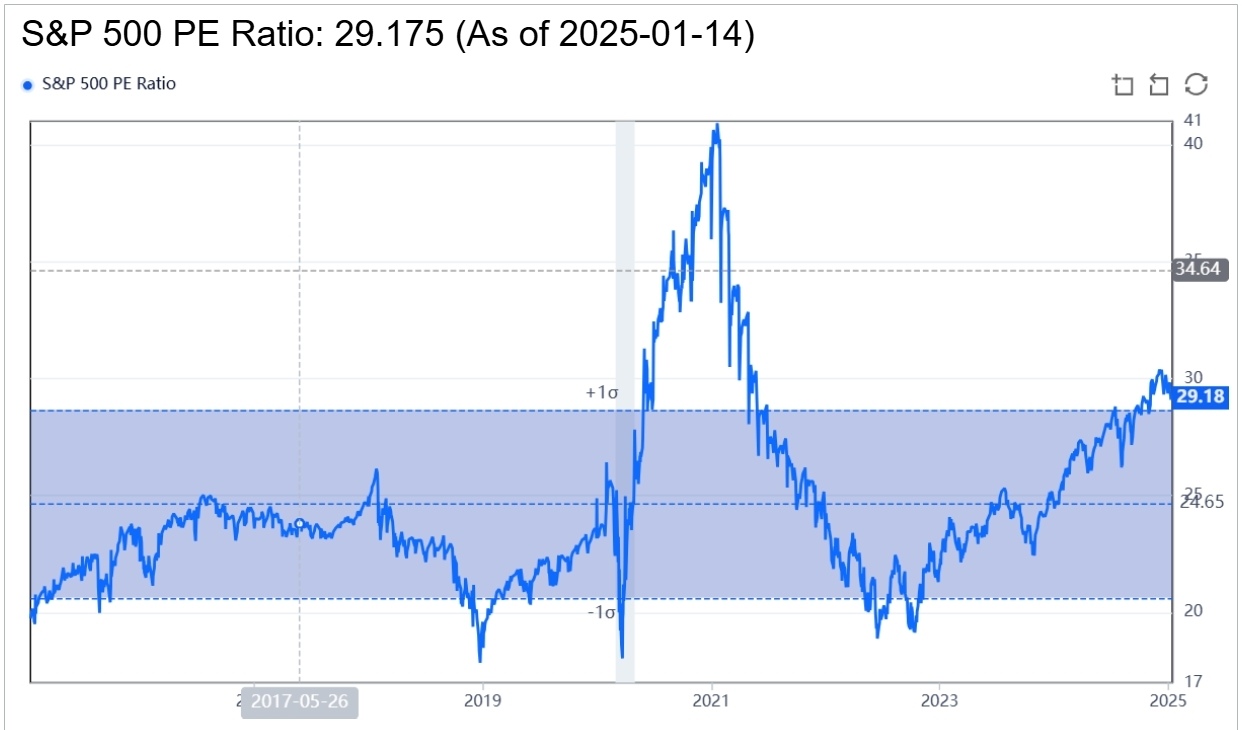

When we talk about valuations, the high multiples of US stocks have become an even greater concern than they were a year ago. The current PE ratio of S&P500 is above 29x, while the historical average is around 25x.

The big tech firms still post solid quarterly growth on top and bottom lines, but it is already difficult for them to satisfy investors’ high expectations. Even if they manage to beat the consensus, the market will scrutinize why the consensus beat is not as significant as it was previously.

Source: GuruFocus

Navigating the 2025 Equity Scene

Passive index investing was a great strategy over the last two years, as the major American indices were able to achieve annual returns of over 20%.

With all of the above-mentioned risks, we are still optimistic about US stocks but to a more modest degree. We believe there will be a disparity in the performance among sectors and companies, as some are better prepared to navigate through the uncertainties than others. Thus, we recommend looking at a more granular level to identify the winners of 2025. Four industries that are well-positioned to outperform in the next twelve months are Banking, Healthcare, Semiconductors and Energy.

Banking Stocks Look Solid

The prospects for banking stocks look quite bright due to several tailwinds coming from different directions. Large banks derive their revenues from various sources such as loans, investment banking, trading and wealth management and right now we can see positive signs for each of these businesses.

First, we already have a less dovish Fed which is good news for the Net Interest Income.

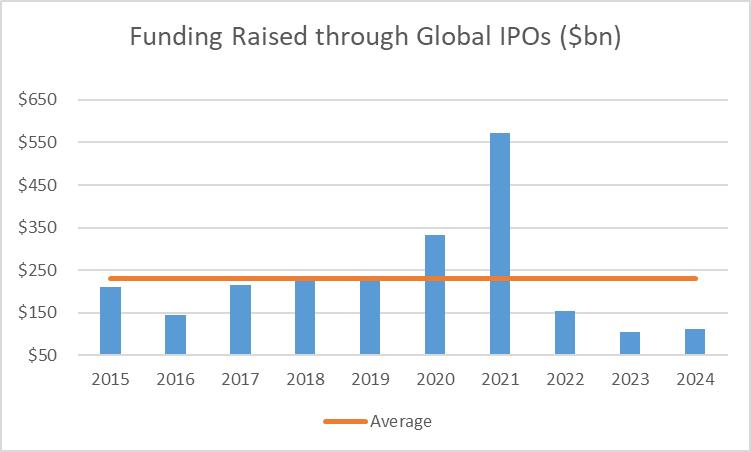

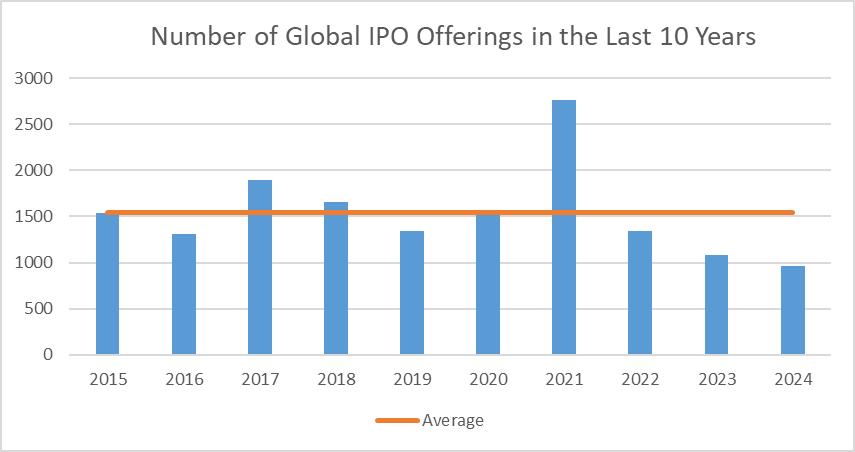

Second, on the investment banking front, the number of deals is picking up and it is still far below the ten-year average. In the last two years, IPOs and M&A deals have been very suppressed due to inflationary pressures and uncertainty over the general direction of the economy. Now the strong economy and the decent valuations can be seen as solid incentives for companies to raise funding through equity or debt or to engage in corporate combinations.

Source: TradingKey, Bloomberg

Source: TradingKey, Bloomberg

In terms of trading, we have strong trading activity across asset classes, which will be supported by the volatility of the markets. Investors will react to political events throughout the year, maintaining a higher level of trading volume.

On the wealth management side, the high asset valuations will keep the AUM high and with the high AUM, the dollar amount of fees that banks are collecting will remain robust.

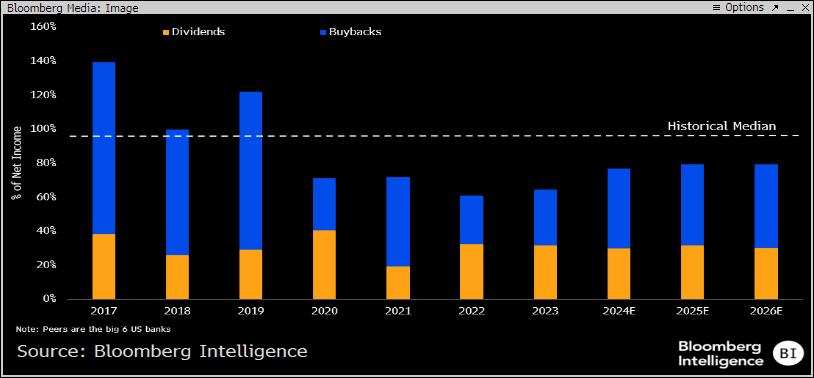

Another important aspect when investing in bank stocks is the shareholder return, either in the form of dividends or share buybacks. Historically, shareholder returns from banks have always been rather generous, but the payout ratio (as a percentage of net income) has been low in recent years despite good financial results.

Source: Bloomberg Intelligence

A potential explanation for the low payout ratio is the fact that banks had to accumulate more capital to prepare for the upcoming version of the Basel III regulatory framework. With the change of power in Washington, it appears that the framework will be either delayed indefinitely or changed to a more watered-down version, increasing the chance for capital returns to shareholders.

Among banking stocks, we favour the large systemically important banks due to their exposure towards higher-prospect non-interest income. Also, large systemically important banks face higher regulatory scrutiny compared with small regional banks, thus deregulation provides more upside for the former.

Healthcare May Be a Dark Horse

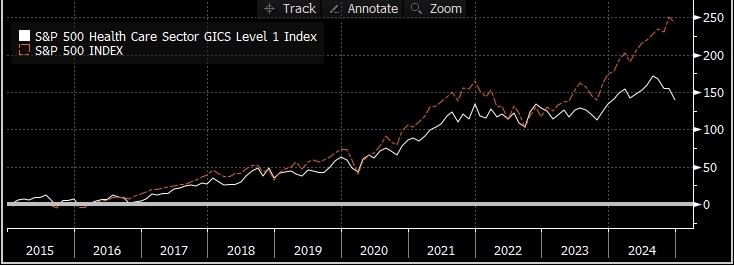

The healthcare sector is another field in which our team sees growth potential. The rationale for choosing this sector is different from that of choosing the banking sector. While, in banking, we see a perfect storm of positive developments, the thesis behind healthcare is more contrarian.

Historically, the Healthcare sector performance has been strongly correlated to the broad market, but in the last two years, we saw a divergence. The gap became even more pronounced in the second half of last year.

Source: Bloomberg Intelligence

With the election of Trump, a huge concern for healthcare investors is the new cabinet that may have a more unconventional attitude towards traditional medicine – against vaccines and weight-loss treatment. However, there are many reasons to think that the situation is not that bleak.

The market has probably only priced the risks of Trump’s mandate, but not the opportunities. The new cabinet deregulation wave can affect the industry with more liberalization of the prices of pharmaceutical products and shorter laboratory approval times from the FDA.

The robust economy and valuations provide a good environment for more fundraising and M&A deals – an important aspect of the healthcare industry. The increased M&A activity will be able to mitigate the risks associated with the patent cliff (the expiration of the patents of several blockbuster drugs).

Further, we see room for AI disruption as artificial intelligence will be gradually introduced in the industry with a lot of room for cutting personnel costs and optimizing the R&D process.

The megatrend of population ageing is also making an impact on the sector. According to the US Census Bureau, the amount of Americans aged 65 or above is expected to increase from 58 million in 2022 to 82 million by 2050 (47% increase), with an elderly share of the total American population going from 17% to 23%. The demand for healthcare-related products and services will be following this trend.

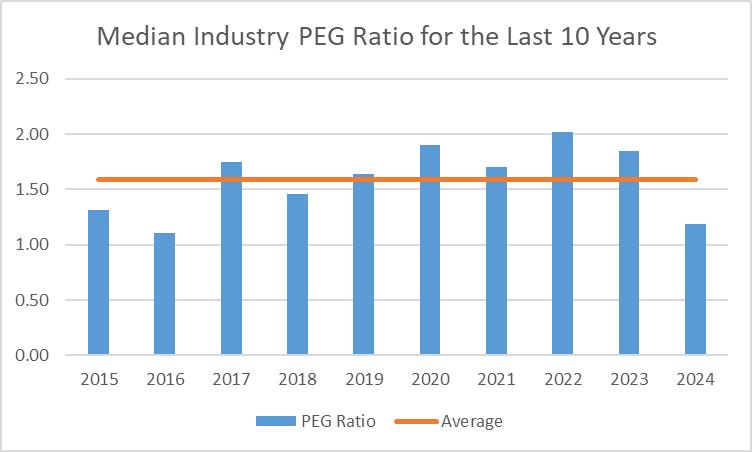

If we use the price/earnings to growth (PEG) ratio for the largest healthcare companies, we will see that the valuations are quite reasonable if we compare them with previous years. Overall, the uncertainties are still there, but it appears to be a limited downside-high upside situation.

Source: Bloomberg Intelligence, TradingKey

We believe the large pharmaceutical firms can benefit from all these trends as they can gain the most from potential deregulation in pricing and, as large institutions, they will have more capacity to invest in technological optimization or simply acquire smaller fast-growing companies.

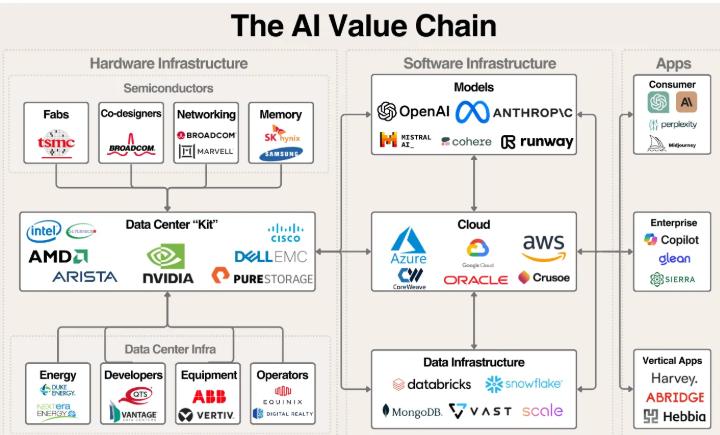

Time to Look for the Next Nvidia across the AI Value Chain

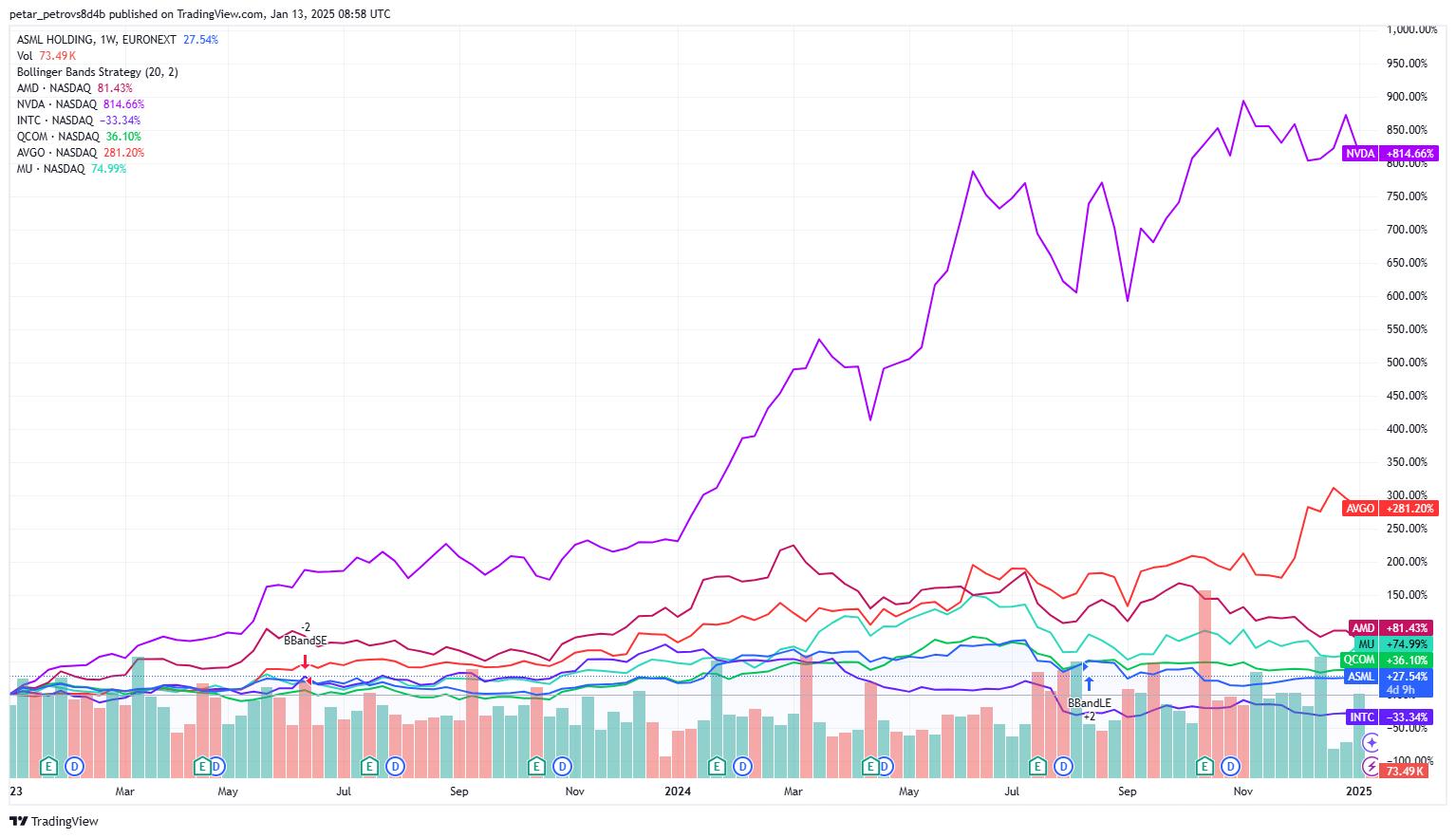

After the latest result releases of the large AI scalers (Meta, Microsoft, Amazon, Apple and Alphabet), we learned that AI spending has not slowed down and the investment opportunities are still there. However, after two years of an incredible bull run, it seems like Nvidia has already benefited disproportionally from the trend, unlike the majority of the semiconductor stocks.

Source: TradingView

Due to the rich valuation of Nvidia, investors may focus their attention on other companies along the vast AI supply chain to seek potential bargains.

The AI value chain encompasses not only GPU/CPU producers like Nvidia, AMD and Intel, but also companies with various other functions, each contributing to the final AI product:

· Fabs, or companies that focus entirely on producing semiconductors: TSMC

· Semiconductor companies focusing on non-GPU/CPU products: Qualcomm (specializing in network infrastructure) and Micron Technologies (specializing in memory chips)

· Operators of data centres: Equinix and Digital Realty

· Energy providers for data centres: NextEra Energy and Duke Energy

· Cloud companies: Amazon with AWS, Google Cloud and Microsoft with Azure

· Data companies: Snowflake, MongoDB and Databricks

· AI applications: Microsoft Copilot, Glean and Sierra

Source: Felicis Ventures

The list is far from complete and each of these markets has its own dynamics and specific features. What made Nvidia successful is the combination of exposure to a high growth trend, dominant market share, high barrier of entry and a superior product. Thus, when investors are looking within the AI value chain, they should look for the same formula.

Memory stocks focusing on High-Bandwidth Memory (HBM) have many of the above-mentioned elements. According to Bloomberg Intelligence, the HBM market is expected to grow 40% in the coming years due to the superior performance of the HBM memory chips and the insatiable AI demand. Currently, only three players dominate the market: SK Hynix, Micron and Samsung.

Energy Sector: Navigating the Dual Path of Traditional and Renewable Energy

Source: S&P Global, Tradingkey.com

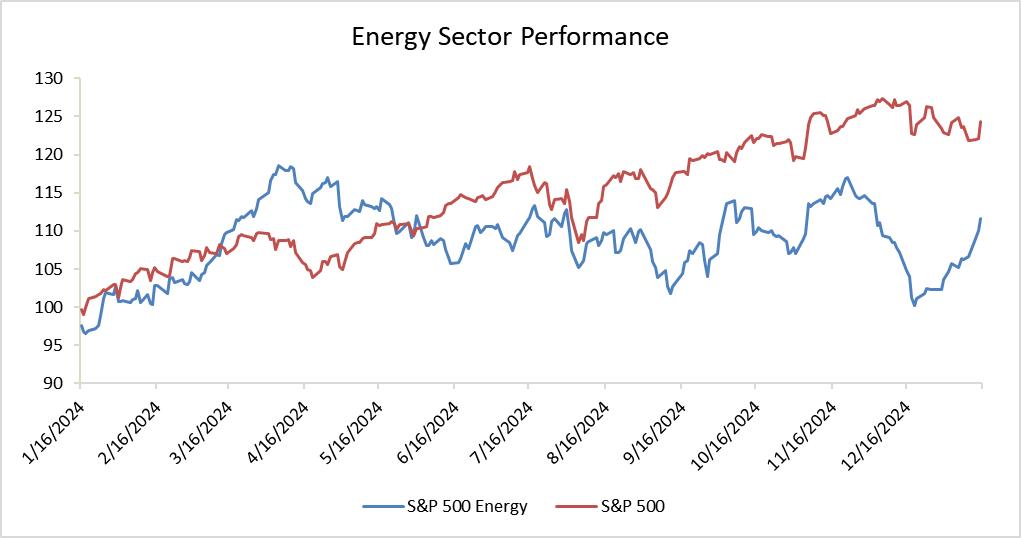

In 2024, the energy sector, as measured by the S&P 500 Energy Index, experienced a different pace of growth compared to the broader S&P 500 Index. However, this momentary pause in performance should not overshadow the sector's underlying strength and future potential. As we look towards 2025, several compelling trends are shaping a vibrant and dynamic future for the US energy landscape:

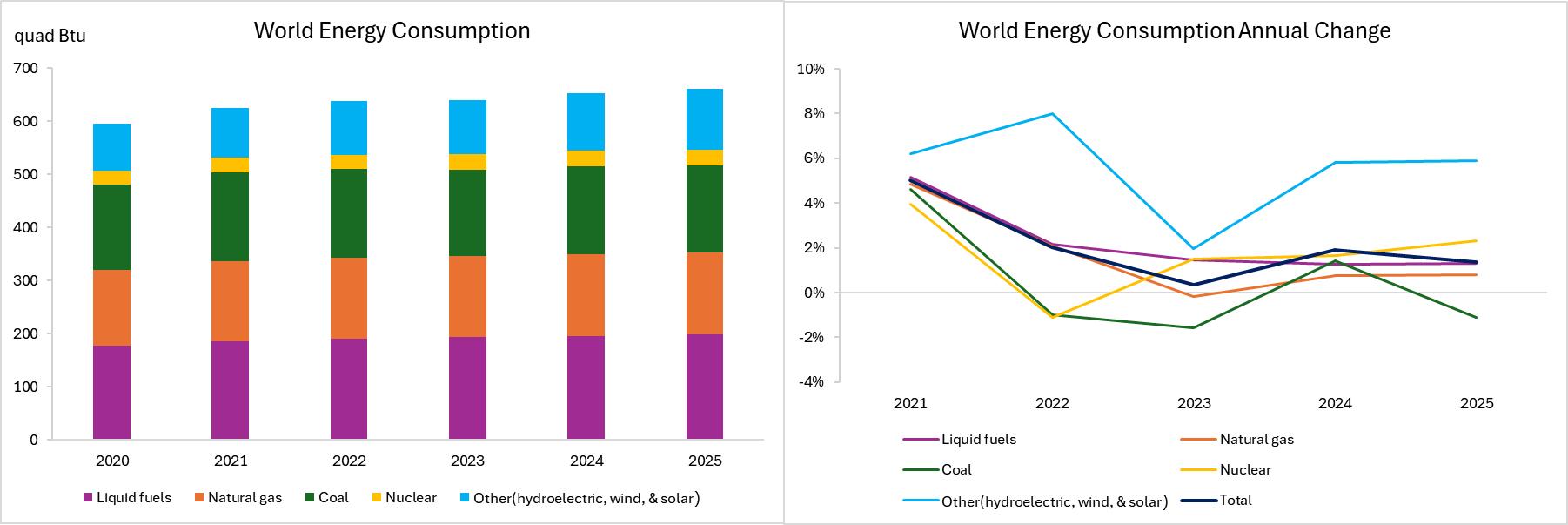

Energy demand: is rising across almost all sectors, driving increased investment in both traditional and renewable sources. According to EIA, global energy demand is expected to grow by about 1.37% in 2025 with higher growth in renewables, driven by economic recovery, increased industrial activity and AI's growing demand. This growth is supported by faster licensing processes and an enhanced focus on energy efficiency.

Source: EIA, Tradingkey.com

Smart Energy: A key trend shaping the sector is the push toward smarter energy management. This means using advanced technologies to make energy production, distribution and consumption more intelligent and efficient. Power grids are being upgraded to better integrate renewable energy sources like solar and wind, reducing energy loss during transmission.

Energy storage, like large batteries, is advancing quickly to store excess renewable energy for use when production is low, thus stabilizing the grid. These advancements are not just for utility companies, they reach consumers too, with smart home technologies and energy-efficient appliances helping to cut down on waste, optimize energy use and reduce costs. Essentially, this trend signifies a move towards a more efficient, sustainable and resilient energy system for all.

Policy Shifts: The political landscape plays a crucial role in shaping energy policy. Traditional fossil fuel production could see renewed support under the Trump administration, potentially boosting domestic production. After Trump takes office, there might be a shift towards faster approvals for fossil fuel projects, making it quicker to drill for oil or build gas plants. The process of renewable energy might not see the same level of support or could face more scrutiny. However, this push for conventional energy sources exists alongside the unstoppable momentum of renewable energy growth, driven by falling costs and strong corporate commitments to sustainability.

· Falling Costs: The cost of solar, wind and battery storage technologies continues to decline, making renewable energy increasingly competitive.

· Corporate Commitments: Major corporations are committing to sustainability, creating a steady demand for renewable energy solutions.

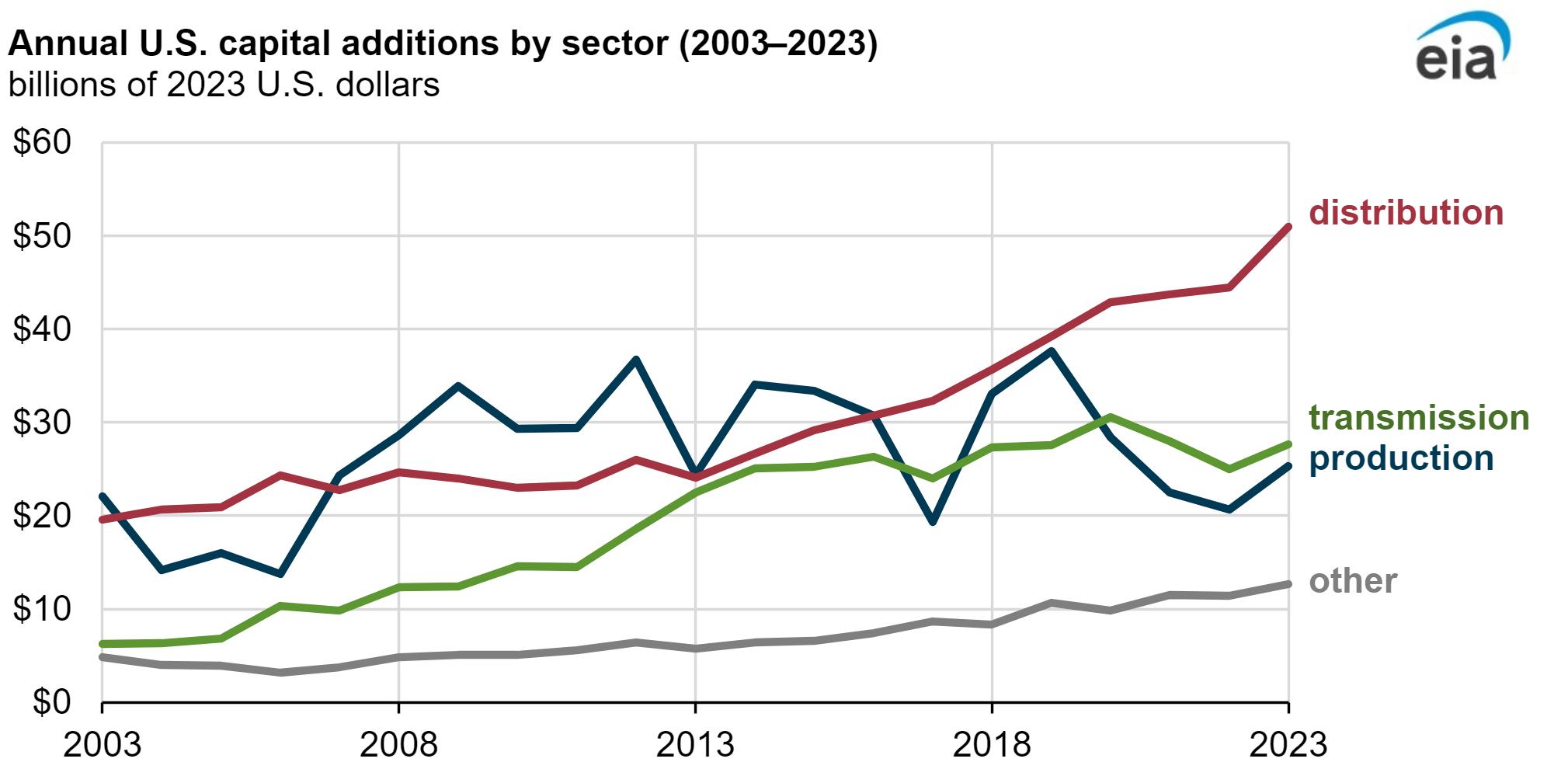

Energy investments: are increasing, with the US witnessing a surge in both renewable energy and fossil fuel sectors. From 2003 to 2023, the total annual investment by energy companies in the US saw a significant rise, increasing by 12%. The chart below illustrates the distribution of capital spending across different sectors of the energy industry.

Source: EIA

Renewable energy investments reached $280 billion in 2023 from $200 billion in 2020 according to IEA, surpassing fossil fuel investments. Legislative support, including the Bipartisan Infrastructure Investment and Jobs Act and the Inflation Reduction Act, has provided nearly $1 trillion for renewable energy initiatives.

Overall, energy investment in the US is on an upward trajectory, with both fossil fuels and renewable energy sectors seeing increased capital allocation. The US remains the world's largest oil and gas producer, while investments in low-emissions power and energy efficiency are projected to double and nearly triple by 2030.

Subsectors and Investment Direction

Traditional Energy Sector

• Integrated Oil Companies

Major integrated oil companies are successfully balancing traditional operations with energy transition initiatives. They operate across the value chain from exploration to refining, which can cushion against commodity price volatility. Many have learned from past cycles to manage capital more effectively, focusing on high-return projects and maintaining strong balance sheets. Both ExxonMobil and Chevron have significantly reduced their debt-to-equity ratios from around 0.30 in 2020 to 0.15 in 2024, reflecting their commitment to maintaining strong balance sheets and they also steadily improved their Return on Invested Capital (ROIC), for example ExxonMobil improved its ROIC from 6% to 12% over the past three years, driven by high-return projects such as Guyana, which boasts an internal rate of return (IRR) of 44%, showcasing disciplined capital allocation and a focus on profitability.

Their global operational footprint also provides stability, while their increasing investments in clean technology position them for long-term sustainability. For example, ExxonMobil has committed to investing up to 30 billion dollars in initiatives aimed at reducing carbon emissions from 2025 to 2030.

Stocks to Consider:

ExxonMobil (XOM): With investments in both traditional oil and emerging clean technologies, ExxonMobil aims for long-term sustainability.

Chevron Corporation (CVX): Strategic investments in shale and exploration in new markets could lead to stable growth.

• Oil and Gas Equipment and Services

This sector is critical for the extraction and processing of oil and gas, which is indispensable to the energy mix. The oil and gas equipment and services sector enters 2025 with renewed strength, benefiting from increased exploration and production activities. Drilling activity is growing, the total utilization rate for the US land and offshore fleet increased from 58% in 2023 to 64% in 2024. However, the supply of some equipment may face shortage concerns in the near term, modern super-spec rigs (which allow for longer laterals, higher pressure and faster drilling) are in high demand, but the number of new super-spec rigs entering the market has not kept pace with demand, leading to a shortage of these advanced drilling technologies in the market.

Stocks to Watch:

Schlumberger Limited (SLB): Known for its technological prowess in both traditional and emerging energy sectors, Schlumberger could benefit from any increase in drilling activities.

Baker Hughes Company (BKR): Its diversified operations, including LNG technology, position it well for growth in both oil and gas markets.

• Natural Gas Producers

Natural gas continues its role as a crucial transition fuel in 2025. The sector benefits from growing global LNG demand, particularly from Europe and Asia, driven by energy security concerns and coal-to-gas switching. Investments in LNG export facilities and pipelines will enhance market access, potentially increasing profitability.

Stocks of Interest:

EQT Corporation (EQT): As a major US shale gas producer, EQT stands to benefit from any policy shift favouring fossil fuels.

Cheniere Energy Inc. (LNG): Its focus on LNG could see significant growth with increased global demand.

Renewable Energy Sector

Renewable energy is experiencing significant growth. The costs for solar and wind energy have dropped, making these sources more affordable. Advancements in technology, especially in energy storage, have made renewable energy more reliable.

• Nuclear Energy

Nuclear energy offers a stable, reliable source of power, crucial for grid stability.

Support from Trump: While Trump has expressed reservations about wind and solar, he supports nuclear power, which could lead to more favourable policies and faster project approvals for nuclear development.

AI's Energy Demand: The growing demand for electricity from AI and data centres, which require a stable and reliable energy source, aligns well with nuclear's consistent power output.

Energy Security: Nuclear power provides energy independence, reducing reliance on imported fuels. Nuclear power plants use uranium as fuel, which can be sourced domestically as the US has significant uranium reserves.

Stocks to Consider:

NuScale Power Corp (SMR): With their reduced size, modular design and enhanced safety features, SMR could benefit from policy incentives and the growing demand for innovative, flexible nuclear energy solutions.

Uranium Energy Corp (UEC): With potential growth in nuclear power, uranium demand could increase, benefiting miners.

Energy Sector Conclusion

In 2025, a diversified approach to the US energy sector is most beneficial, balancing between traditional energy sources, which still play a crucial role and emerging renewable energy, which are gaining traction. Each subsector offers unique investment opportunities. By carefully selecting investments based on these factors, investors can navigate the complexities of the energy market in 2025, potentially reaping benefits from both the stability of established sectors and the growth potential of emerging ones.

Volatility Will Return to the Markets

With looming inflation and plenty of political factors, volatility will play a big role in the equity markets in the coming months. However, price fluctuations can be seen as an opportunity to identify mispriced assets. Investors can “defeat” the market volatility if they keep their holdings in high-quality companies, holding them with a long-term view.

Part 3: Commodities as an Alternative Asset Class

(by Viga Liu)

Crude Oil: Market Rebalancing Amid Geopolitical Shifts

The global oil market in 2025 stands at a critical juncture, marked by an emerging supply surplus against demand. Key factors shaping the market include evolving US-Russia relations following Trump's election victory, contrasting demand patterns between India and China and OPEC+'s strategic responses to price pressures. With Brent crude expected to trade within a $75-85 per barrel range, higher in the first half before facing downward pressure, these dynamics suggest a year of significant market realignment ahead.

A Pivotal Moment in Geopolitical Dynamics

As 2025 begins, the global oil market stands at a geopolitical crossroads. The Biden administration's exit is marked by unprecedented sanctions on Russian energy, targeting key producers and trade networks. However, Russia's adept evasion tactics, including alternative trade mechanisms, might mitigate the impact, with major buyers like China and India potentially continuing purchases in non-dollar settlements.

The US election outcome, with Trump's return, adds another layer of complexity. His commitment to ending the Russia-Ukraine conflict could reshape geopolitical dynamics, potentially reducing the risk premium in oil prices. Yet, the transition period might see increased market volatility as both sides manoeuvre for advantageous ceasefire terms.

Looking further ahead, de-escalation in the conflict could lower geopolitical risks, reshaping oil trade patterns. However, persistent tensions in the Middle East, coupled with Trump's possible hardline stance on Iran, suggest that geopolitical factors will continue to significantly influence oil prices in 2025.

Supply Side: From Tight Balance to Oversupply

Looking ahead to 2025, global oil supply is expected to increase by 1.7 million barrels per day, primarily from non-OPEC producers from EIA estimates. However, the US growth momentum is predicted to slow, building on the record-high production levels of 2024. This moderation is due to several factors:

· Delayed Effect: After reaching high production levels in 2024, maintaining growth requires drilling more new wells due to the depletion of existing ones. The reduction in new drilling rigs in late 2024 will gradually impact production in 2025.

· Technological Advances: The space for efficiency improvements narrows and the availability of prime drilling sites decreases, making it harder to increase per-well output.

Considering these elements, US oil production is expected to remain relatively stable at high levels in 2025, unless oil prices significantly rise, prompting increased capital investment.

Non-OPEC countries are projected to contribute an additional 610,000 barrels per day of production growth, with Brazil's deep-water projects, Guyana's Stabroek Block development and increased Canadian oil sands output following the TMX pipeline startup being key sources. Norway's North Sea projects, Argentina's shale oil and Mexico's shallow water projects will also add to the supply.

Source: EIA, Tradingkey.com

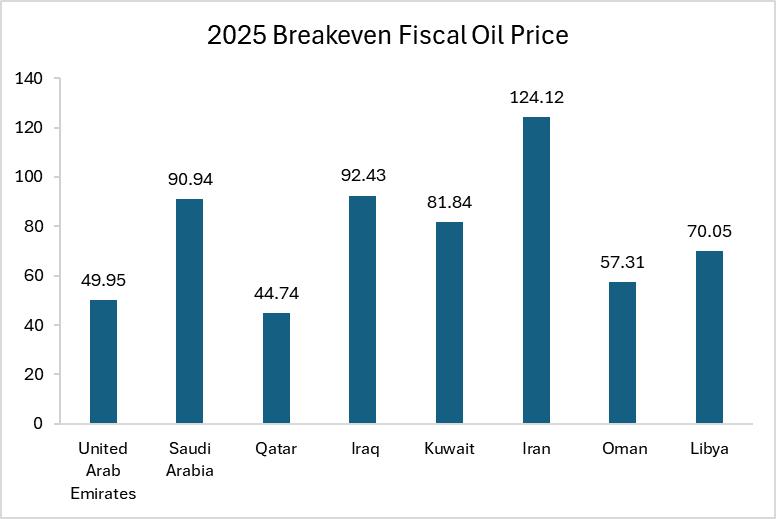

However, OPEC+ production policies remain the largest variable on the supply side. OPEC+ has extended its voluntary production cuts of 2.2 million barrels per day until the end of Q1 2025. Given that most OPEC countries require oil prices above $80 per barrel to balance their budgets, unless prices consistently remain above this level, the likelihood of continuing production cuts is high. Historical trends show OPEC+ tends to stabilize the market when Brent crude prices fall below $70 per barrel while increasing production becomes more likely when prices exceed $80 per barrel.

Source: IMF, Tradingkey.com

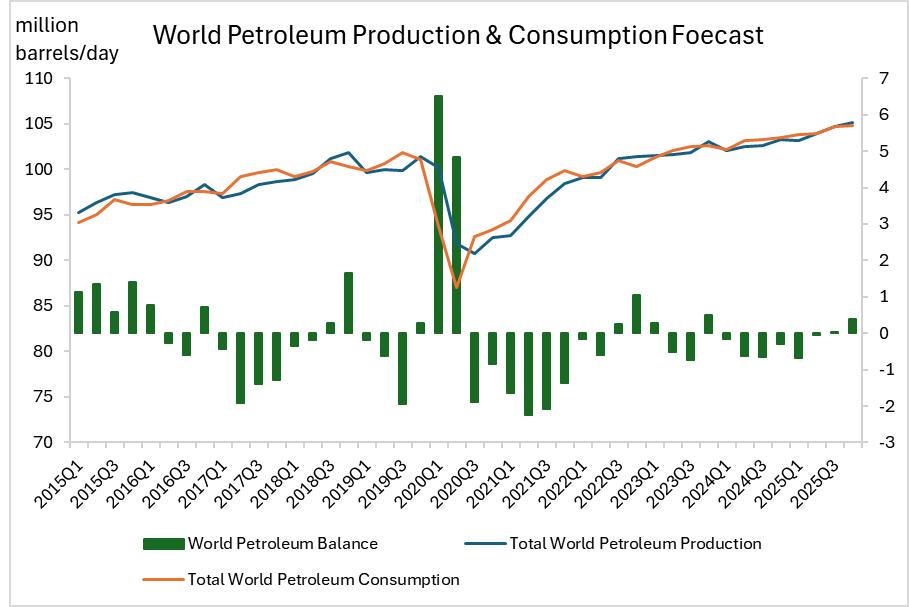

Based on supply-demand balance forecasts, global oil and other liquid fuels are expected to remain in a supply deficit in Q1 2025. However, from Q2, the supply-demand relationship is set to change significantly. With the release of new production capacity from non-OPEC countries, an oversupply is expected starting in Q2, with the surplus expanding further in Q3 and Q4.

Source: EIA, Tradingkey.com

This shift in supply-demand dynamics, coupled with OPEC+'s sensitivity to oil prices in adjusting production policies, means the oil market will face increased supply pressure in 2025. OPEC+ will need to strike a balance between maintaining market share and stabilizing prices.

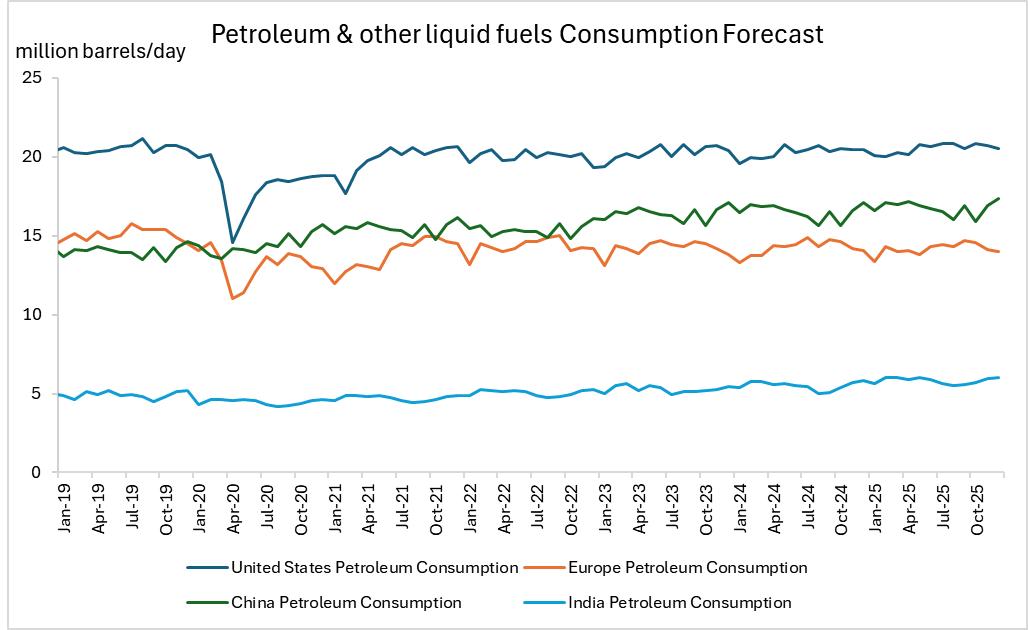

Demand Side: China's New Phase and India's Rapid Expansion

Global oil consumption patterns are undergoing significant changes. According to the latest EIA forecasts, global demand growth is expected to reach 1.3 million barrels per day in 2025. The performance of two major Asian economies stands out:

Source: EIA, Tradingkey.com

China's oil demand is entering a new phase. Despite government measures to boost the economy, demand growth in 2025 is projected to be only 280,000 barrels per day. This moderate growth reflects underlying structural changes - the rapid penetration of new energy vehicles (sales already exceeding 50% market share), population trends and moderate economic growth, which significantly limit traditional transportation fuel demand.

On the other hand, India's oil demand is set to surge. According to the latest EIA projections, India’s oil demand growth constitutes 25% of the global increase in oil demand, driven by the country's expanding middle class and increasing transportation needs.

However, China's consumption is still over three times larger, making it a pivotal factor in the global oil supply-demand balance. The contrast in growth trajectories between these two Asian giants will continue to shape the dynamics of the global oil market in 2025.

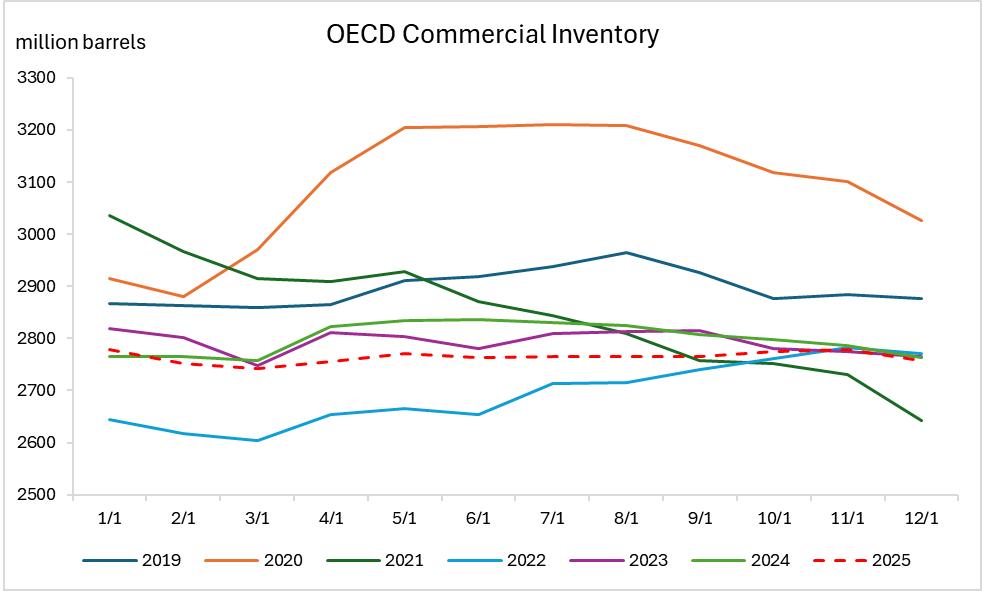

Inventory Status: Persistent Tightness

OECD commercial oil inventories in 2024 have remained near historical lows and this tight inventory situation is expected to persist into 2025. While this partly reflects a cooling of speculative market sentiment, low inventory levels also pose risks for price volatility. Particularly in the context of escalating geopolitical conflicts, low inventories could be leveraged by speculative capital to amplify upward price risks.

Source: EIA, Tradingkey.com

Crude Oil Conclusion

With supply gradually shifting towards oversupply but geopolitical risks remaining elevated, oil prices in 2025 are expected to follow a pattern of high in the first half, then lower. Geopolitical risk premiums and OPEC+ production cuts will drive prices in the first half and the second half, despite China's moderate demand recovery, global supply growth might outpace demand growth, putting downward pressure on prices.

Brent crude is projected to fluctuate within the $75-$85 per barrel range. An upward break would require further escalation in geopolitical risks or unexpectedly strong demand growth, while a downward break would need OPEC+ to abandon production cuts or a significant weakening in global demand.

Gold: Political Wildcards and Steady Central Bank Demand

As Donald Trump prepares to re-enter the White House in January 2025, the gold market is poised to experience an unprecedented level of policy uncertainty. Amidst ongoing geopolitical tensions and the potential resurgence of inflationary pressures, gold's role as a safe-haven asset remains in high demand. While the fundamentals still support a rise in gold prices, the extent of this increase might not match the gains seen in 2024, yet the market remains poised for a bullish trend, albeit with potentially more moderate returns.

Policy Uncertainty as a Key Driver

With Trump's inauguration, policy uncertainty is expected to surge significantly. His campaign promises, including imposing a 60% tariff on Chinese goods, mass deportation of undocumented immigrants and other aggressive policies, are likely to introduce notable market volatility. This uncertain environment favours gold and other safe-haven investments.

Persistent Geopolitical Risks

The ongoing conflict between Russia and Ukraine, instability in the Middle East and Trump's unpredictable foreign policy stance suggest that the global geopolitical risk index will remain elevated. In this context, institutional investors might increase their gold allocations to hedge against these risks.

Inflation Hedge

Looking ahead to 2025, the risk of inflation might resurface. Trump's proposed policies could increase production costs and wages, potentially igniting new inflationary pressures. Gold has historically served as a reliable hedge against inflation. As inflationary pressures mount, investors often turn to gold to preserve their purchasing power, which can bolster demand.

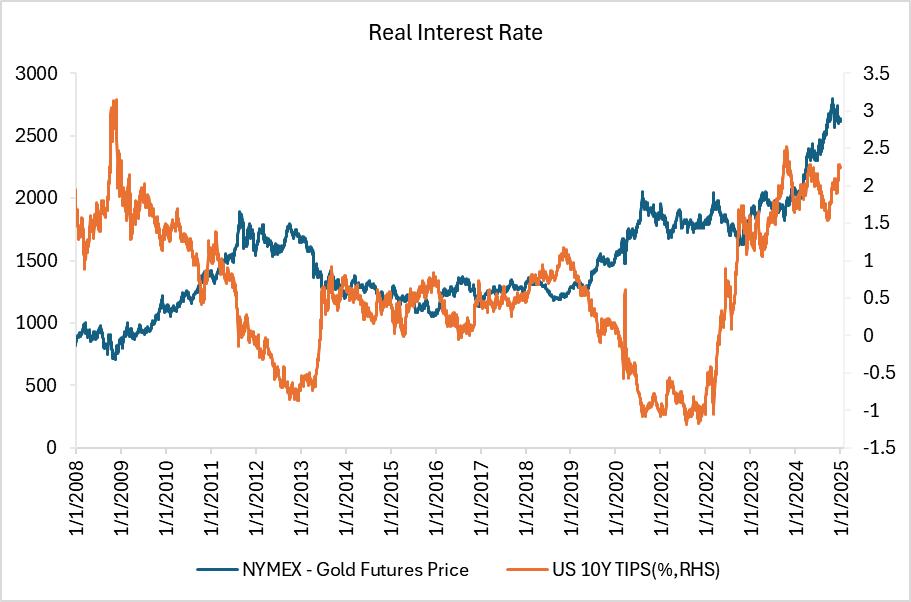

In this scenario, while the Federal Reserve might adopt a more cautious approach to rate cuts, keeping real interest rates relatively high, which might temper the immediate upward potential of gold prices, the underlying demand for gold as a hedge against inflation and policy uncertainty will continue to underpin its value. Gold's historical track record as a store of wealth during times of economic uncertainty and rising prices positions it well to benefit from the anticipated inflationary environment in 2025, even with potential headwinds from monetary policy.

Source: LSEG, Tradingkey.com

Central Bank Demand: A Pillar of Support

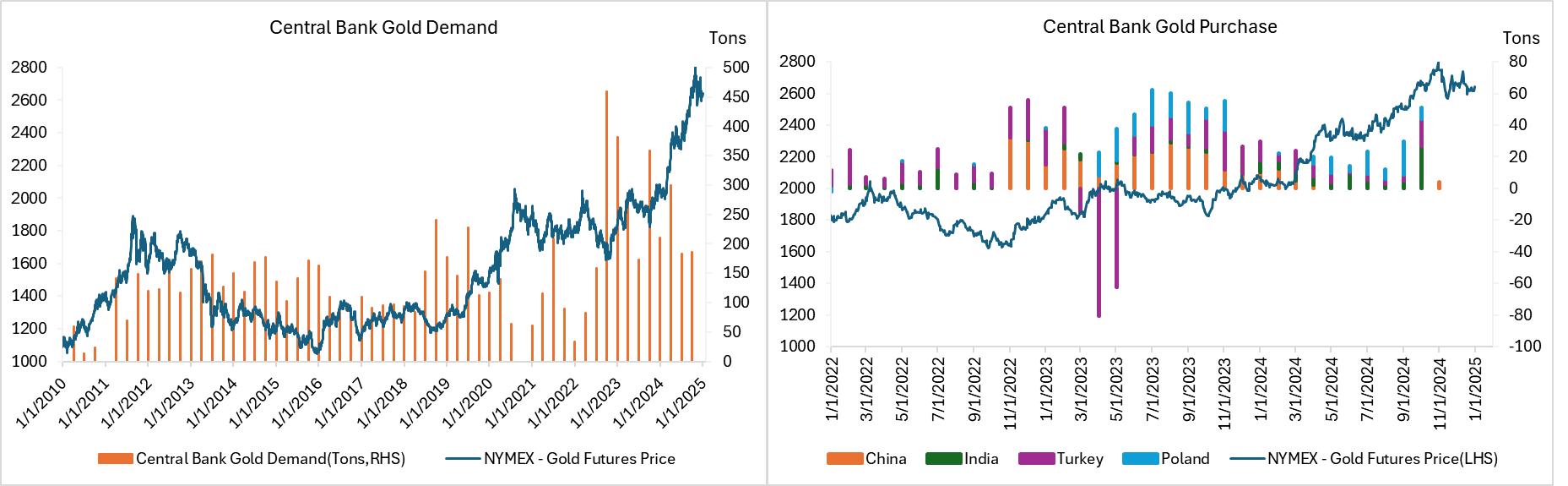

Global central banks, having purchased over 1,000 tons of gold in both 2022 and 2023, setting new records, reflect an accelerated trend towards de-dollarization and strategic diversification of foreign exchange reserves. While the pace of buying might slow in 2025, demand is expected to remain robust.

China's continued accumulation of gold is particularly noteworthy. According to the World Gold Council, China's gold reserves as a percentage of its total foreign exchange reserves remain below 5%, significantly lower than the 15-20% typical of developed economies, indicating room for further increases.

Emerging market central banks like those in India, Turkey and Poland also maintain steady gold purchases. These countries face currency depreciation pressures and geopolitical risks, making gold an essential hedge and a strategic choice to bolster currency credibility, especially as the dominance of the dollar is challenged.

However, current gold prices might deter some central banks from buying. Historical data suggests central banks prefer to accumulate gold when prices are relatively low. Also, some central banks might have already met their reserve adjustment targets, possibly leading to a slowdown in purchases. It's projected that global central bank gold buying will remain within the 800-1,000 tons range in 2025, lower than the previous two years but still well above historical averages.

Overall, central bank demand will continue to be a significant factor supporting gold prices in 2025, though its marginal impact might be less pronounced than in previous years.

Source: World Gold Council, Tradingkey.com

Gold Conclusion

Gold prices in 2025 are anticipated to maintain a bullish trajectory, supported by robust fundamentals, policy uncertainty and inflation expectations. Although the Federal Reserve's cautious approach to rate cuts might initially moderate the upward momentum due to higher real interest rates, the enduring demand for gold as a safe-haven asset and inflation hedge is expected to drive prices higher. Central banks' continued accumulation of gold, coupled with investors' need to protect against geopolitical risks and economic volatility, will support gold's value. Prices are projected to consolidate in the near term around $2,600 to $2,800 per ounce, with potential highs reaching $3,000 to $3,200 by the end of the year, reflecting the interplay between inflation hedging, policy uncertainty, reflecting its appeal as a reliable store of value in a world of economic and political changes.

Bitcoin: Institutional Transformation and Policy Shifts Fuel Bull Market

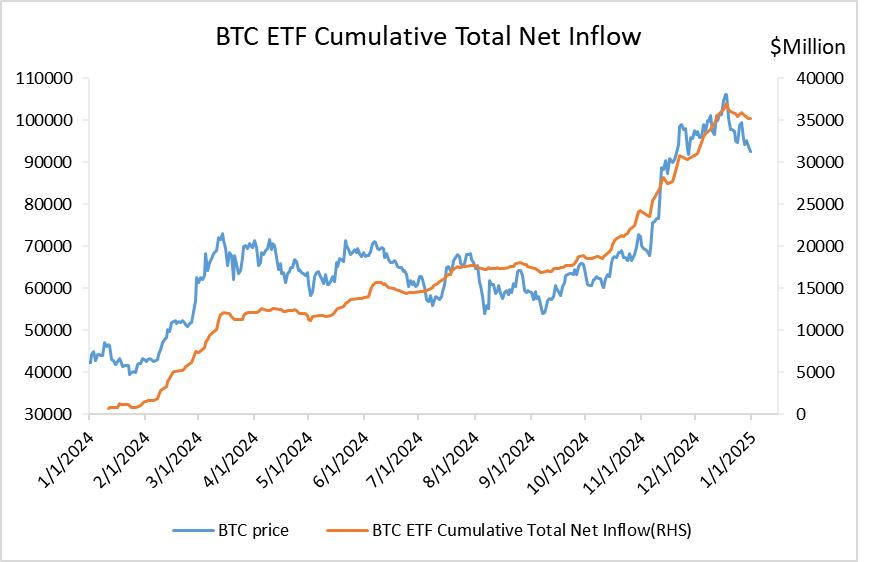

As the Bitcoin market continues to mature, its 2025 outlook appears highly favourable, driven by institutional adoption and regulatory developments. The approval of Bitcoin spot ETFs in early 2024 marked a pivotal milestone, attracting significant institutional fund inflows and establishing Bitcoin as a mainstream asset. In 2025, these trends are expected to accelerate. Optimism around potential pro-crypto policies under a Trump administration adds another bullish layer.

Bitcoin Spot ETFs: A Milestone in Institutional Adoption

The approval of Bitcoin spot ETFs has paved the way for more institutional participation and ETF fund inflows have shown a positive correlation with Bitcoin’s price, meaning increased institutional involvement could further drive price growth. Traditional financial institutions are expected to increase their Bitcoin allocations in 2025. For example, insurance companies may begin small investments, while pension funds could test the waters with pilot programs. Family offices, known for their flexibility, are likely to expand their exposure to digital assets.

Source: SoSoValue, Tradingkey.com

Potential Pro-Crypto Policies Under Trump: Impact and Feasibility

Several pro-crypto policies were proposed by Trump during and after his campaign and they could significantly influence the cryptocurrency market if implemented. Below, we analyze some key proposals, their potential impact, possible timeline and feasibility.

1. Regulatory Overhaul

• Possible Timeline: January 20, 2025 – March 2025

• Difficulty: Moderate (Requires Senate confirmation, but Republican control of the Senate reduces resistance)

January 20, 2025, could mark a turning point for US cryptocurrency regulation. With the current chairs of the SEC (Gary Gensler) and the CFTC expected to step down upon Trump taking office, leadership changes at these key regulatory bodies will reshape the regulatory landscape. Under Gensler, the SEC’s strict enforcement has slowed industry innovation.

Trump’s administration nominated figures like pro-crypto former SEC Commissioner Paul Atkins as the new SEC chair and venture capitalist David Sacks as a potential “AI and Crypto Czar.” These candidates favour reforming securities laws to better accommodate the unique characteristics of digital assets. While Senate approval is needed, Republican control could speed up the process. These leadership changes could lower compliance costs and foster a more crypto-friendly environment.

2. Improving Banking Access for Crypto Businesses

• Possible Timeline: February 2025 – August 2025

• Difficulty: Moderately High (Requires coordination with multiple banking regulators, may face resistance from traditional financial institutions)

Under Trump, executive orders are expected to address the banking challenges faced by cryptocurrency businesses. From 2023 to 2024, Operation Choke Point 2.0 led to widespread "de-banking" of compliant crypto firms, stripping them of essential banking services such as account access and payment processing. This restricted industry growth and heightened systemic risks.

New policies are likely to legally prohibit financial institutions from denying services solely based on a company’s involvement in cryptocurrency. These measures, expected to be implemented through executive orders, will involve multiple regulatory bodies. Such reforms could significantly improve banking access for crypto businesses, fostering industry growth.

3. Opposition to Central Bank Digital Currencies (CBDCs)

• Possible Timeline: January 2025 – March 2025

• Difficulty: Low (Primarily relies on executive authority, easily implemented)

Trump has explicitly opposed the issuance of a US CBDC. Unlike decentralized cryptocurrencies like Bitcoin, CBDCs are centralized and fully controlled by central banks. Trump views CBDCs as tools for increased government financial surveillance, posing risks to individual privacy.

Trump’s stance is a positive signal for Bitcoin and other cryptocurrencies. A US CBDC could directly compete with cryptocurrencies in the digital payments space. By opposing CBDCs, Trump could reduce competitive pressures in this area.

4. National Bitcoin Reserve

• Possible Timeline: Proposed in Q2 2025 – Execution in 2026

• Difficulty: Extremely High (Requires Treasury and Federal Reserve coordination, likely to face strong political opposition)

One of Trump’s most ambitious and controversial proposals is the Bitcoin Reserve, aimed at incorporating Bitcoin into the US National Reserve system. With the dollar’s dominance as a global reserve currency increasingly challenged, adding Bitcoin to national reserves is seen to modernize monetary policy while reinforcing US financial leadership.

However, the policy faces major challenges. Political opposition—especially from Democrats—could prevent the use of public funds for what many view as a speculative and risky asset. Additionally, large-scale Bitcoin purchases risk triggering extreme price volatility, demanding careful strategies to minimize market disruptions.

Despite these challenges, the policy’s potential significance cannot be overstated. Since the collapse of the Bretton Woods system in 1971, this would represent one of the most transformative shifts in US monetary policy. If successful, it could elevate Bitcoin’s legal and institutional status, and encourage other nations to follow and reshape the global financial order.

5. Innovation Funding Initiative

• Possible Timeline: Launch in Q2 2025 – Full implementation by 2026

• Difficulty: Moderate (Primarily involves budget allocation and inter-agency coordination)

Trump proposed to establish a dedicated fund to support cryptocurrency innovation. This initiative would focus on critical areas such as expanding blockchain infrastructure, enhancing security measures to prevent cyberattacks and advancing cross-border payment solutions. Initial funding is expected to reach several billion dollars and will be managed through existing or newly created departments under the Treasury and Commerce Departments. While the funding scale is significant, the initiative falls largely within executive authority, making it relatively straightforward to implement.

6. Cross-Border Payment Reform

• Possible Timeline: Begins in Q3 2025 – Completion by 2027

• Difficulty: High (Requires international coordination and collaboration with multiple regulatory bodies)

To enhance US competitiveness in global payments, Trump has proposed promoting the use of cryptocurrencies like Bitcoin in cross-border transactions. This includes ideas such as establishing mutual regulatory recognition agreements with other nations, simplifying payment processes and reducing compliance costs. While promising, this proposal would require extensive international coordination and careful balancing of anti-money laundering and other regulatory concerns, making it a long-term objective.

7. Comprehensive Tax Reform

• Possible Timeline: Proposed in late 2025 – Implementation by the end of 2026

• Difficulty: Extremely High (Requires Congressional approval, involves federal tax code changes)

Trump’s tax reform proposals include crypto-friendly measures such as exempting small crypto transactions from capital gains taxes and offering tax incentives for US-issued cryptocurrencies. These changes could significantly boost the adoption of cryptocurrencies for everyday use and institutional investment. However, since tax reforms require legislative approval, implementation will depend on both parties’ support, making it one of the more challenging proposals.

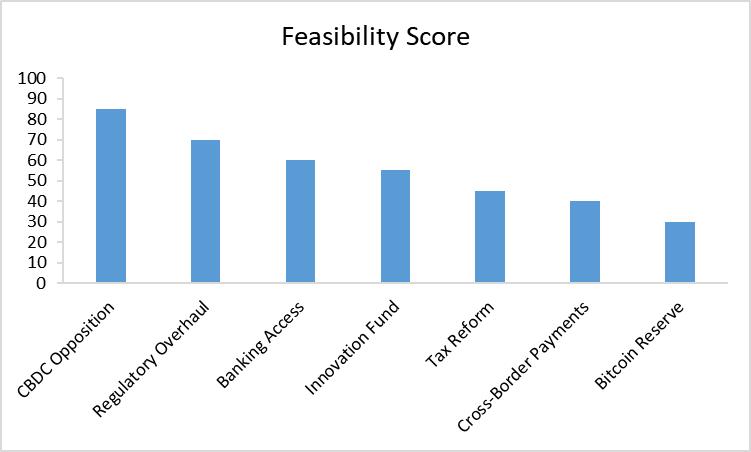

Based on 5 key criteria (0-20 points each): Executive Authority, Congressional Approval, Regulatory Complexity, Technical Requirements, and Stakeholder Resistance, the feasibility scores can be calculated based on our assumptions, with higher scores indicating more favourable conditions for implementation.

Source: Tradingkey.com

The most likely policies to be implemented by the Trump administration in 2025 are regulatory overhaul, opposition to CBDCs and improving banking access for crypto businesses. These policies would create a more crypto-friendly regulatory environment. Long-term, more ambitious policies like the National Bitcoin Reserve or Comprehensive Tax Reform face significant political and technical challenges, making their implementation uncertain, though not entirely impossible if political conditions align in later years.

Bitcoin Conclusion

Bitcoin’s 2025 outlook points to strong price growth, driven by institutional adoption, regulatory clarity, enhanced infrastructure and the effects of Bitcoin's 2024 halving. The Federal Reserve's pace of rate cuts and overall liquidity conditions in the market will play a crucial role in shaping Bitcoin's price. As the number of expected rate cuts decreases in 2025, shifts in liquidity could also influence Bitcoin's price movement. Long-term, while challenging, the possibility of more ambitious policies could further bolster Bitcoin’s role in reshaping the financial landscape.