Emerging Europe Economics: Will the Region Experience a Stronger Growth in 2025?

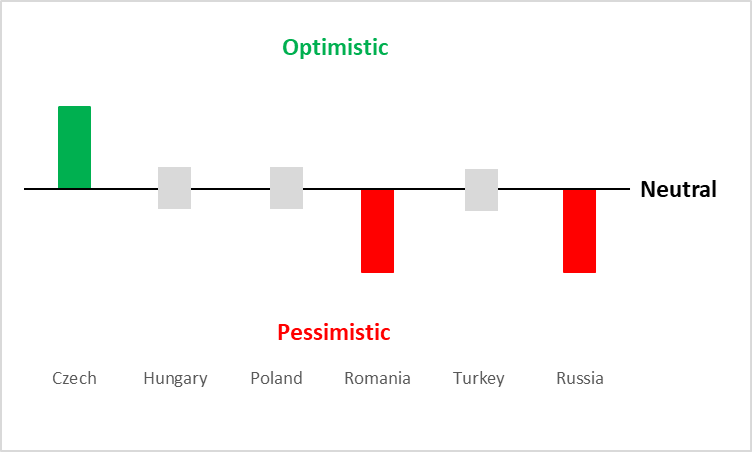

Executive summary: Short- and medium-term (0-12 months) view

Source: Tradingkey.com

1. Central and Eastern Europe (CEE)

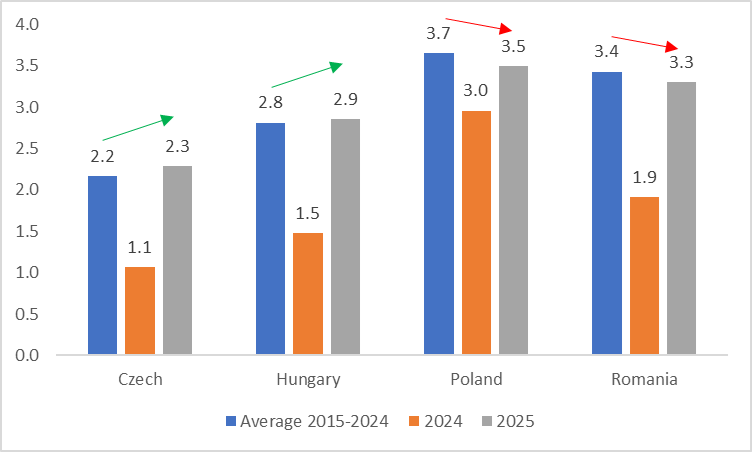

Looking ahead to next year, the economic performance of the four major Central and Eastern European (CEE) economies is expected to show a mixed picture compared to this year. According to the IMF, GDP growth in the Czech Republic and Hungary is projected to exceed their 10-year averages in 2025, while Poland and Romania are likely to experience a slight decline in growth (Figure 1). This section examines the current economic conditions of these four countries and provides an outlook for 2025.

Figure 1: CEE countries' real GDP growth (%)

Source: IMF, Tradingkey.com

1.1 Czech Republic

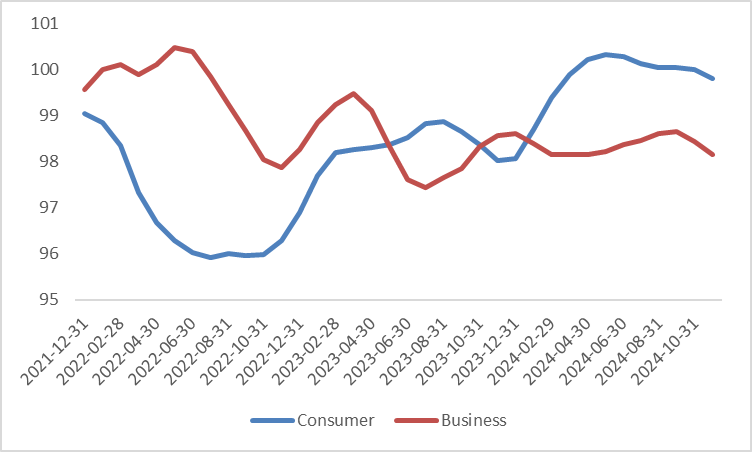

The Czech economy has shown significant improvement, driven by increased domestic demand and net exports. In the third quarter, GDP grew by 0.4% quarter-on-quarter and 1.3% year-on-year. Stronger economic growth was partly attributed to the Czech National Bank’s (Česká národní banka, CNB) easing monetary policy. Since the central bank initiated a rate-cutting cycle at the end of 2023, the policy rate has been reduced by a cumulative 300bp. High-frequency data indicate that consumer and business confidence indices have declined in recent months (Figure 1.1). However, looking ahead, as the CNB is expected to continue lowering interest rates, we anticipate these indices will recover further in the coming quarters, suggesting a more optimistic outlook for private consumption and fixed investment.

Figure 1.1: Czech consumer and business confidence indices

Source: Refinitiv, Tradingkey.com

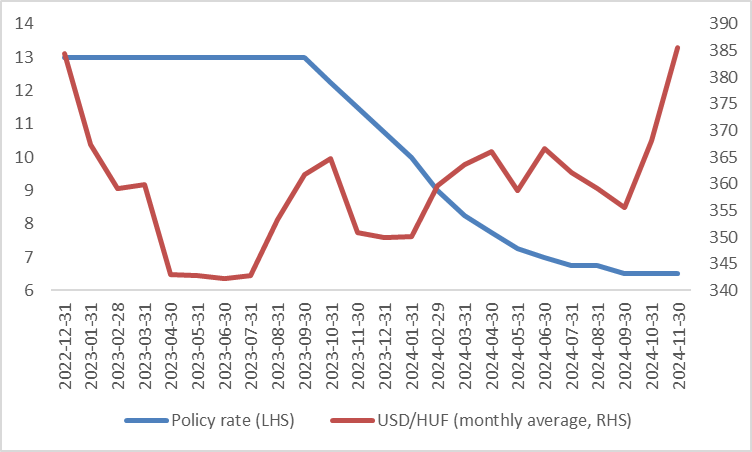

1.2 Hungary

Hungary's economic growth contracted quarter-on-quarter in both the second and third quarters of this year, placing the economy in a technical recession. This downturn was primarily driven by weak external demand, reductions in EU funding, and domestic fiscal tightening. Since the third quarter, consumption has shown signs of recovery; however, the ongoing decline in fixed investment has continued to weigh on the overall economic rebound. In response to the weak economy, the Hungarian government has implemented a range of supportive fiscal measures, including raising the minimum wage, lowering the cap on mortgage interest rates, and increasing corporate lending. On the monetary front, the depreciation of the Hungarian forint and the resurgence of inflation could prompt the Hungarian National Bank (Magyar Nemzeti Bank, MNB) to adopt a more hawkish stance. Considering these economic and policy developments, the IMF forecasts Hungary's real GDP growth at 1.5% in 2024 and 2.9% in 2025, both at the lower end of the government's target growth ranges.

Figure 1.2: Hungary policy rate vs. USD/HUF

Source: Refinitiv, Tradingkey.com

1.3 Poland

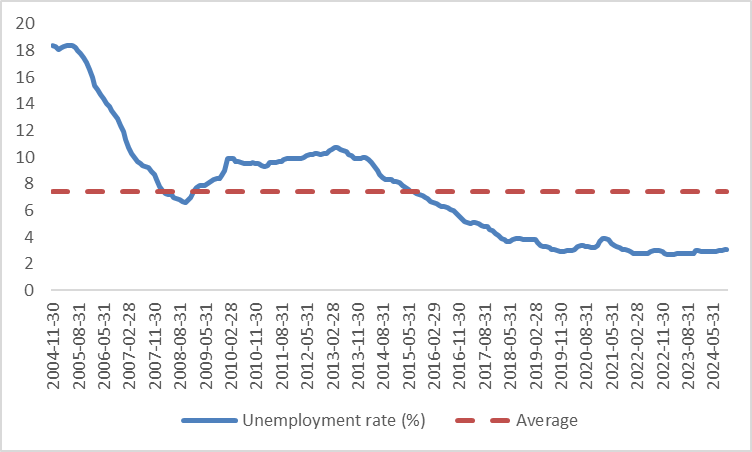

The Polish economy has experienced mixed performance since the beginning of this year. While economic activity in the first half of the year exceeded expectations, a sharp increase in non-core CPI during the third quarter eroded real incomes, reducing private consumption. This resulted in negative real GDP growth in Q3 2024. Looking ahead, the Polish economy is expected to exhibit both strengths and challenges. On the positive side, wage growth remains above historical averages, and unemployment remains low (Figure 1.3). Additionally, the impact of severe floods in southwestern Poland in September is expected to gradually dissipate.

However, significant fiscal challenges lie ahead. To comply with the European Commission’s deficit reduction plan, Poland’s fiscal budget is expected to contract substantially, which will dampen economic growth. Furthermore, the rise of global trade protectionism poses risks to Polish exports. Against the backdrop of fiscal tightening and heightened uncertainty in external demand, we anticipate that the National Bank of Poland (Narodowy Bank Polski, NBP) will begin a rate-cutting cycle in mid-2025 to support the economy.

Figure 1.3: Poland's unemployment rate (%)

Source: Refinitiv, Tradingkey.com

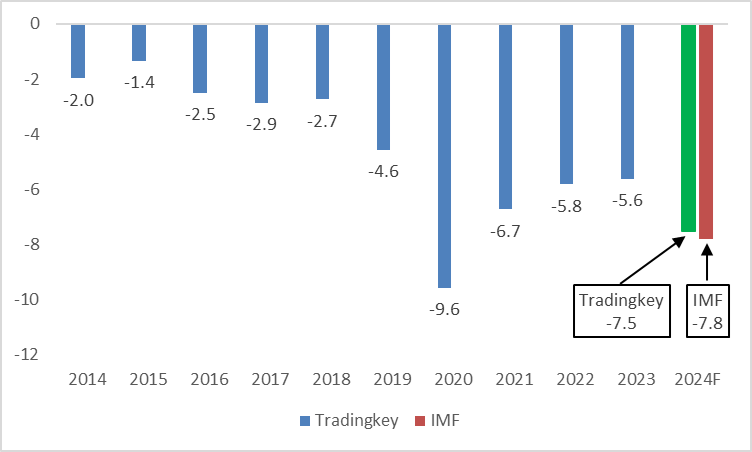

1.4 Romania

In recent years, Romania's fiscal position and external balance have both shown signs of deterioration. On the fiscal front, we expect the deficit to reach 7.5% of GDP in 2024. Although this figure is lower than the IMF's forecast, it significantly exceeds the government’s target of 5% (Figure 1.4). Public debt has also surged, now exceeding 50% of GDP.

Externally, the Balance of Payments has also worsened, with the current account deficit rising to 7.6% of GDP in the third quarter, compared to 7% in 2023. These internal and external deficits are the highest among the four major Central and Eastern European (CEE) economies. The elevated deficits have begun to weigh on economic growth, with real GDP contracting by 0.1% in the third quarter.

Faced with high deficits, persistent inflation, and sluggish growth, the Romanian government introduced a seven-year fiscal consolidation plan in October. The plan includes measures to cut fiscal spending and raise tax revenues, but its implementation is expected to be challenging. Looking ahead, Romania's economic outlook remains uncertain and will heavily depend on the successful execution of this consolidation plan.

Figure 1.4: Romania fiscal deficit (% of GDP)

Source: Refinitiv, Tradingkey.com

2. Turkey

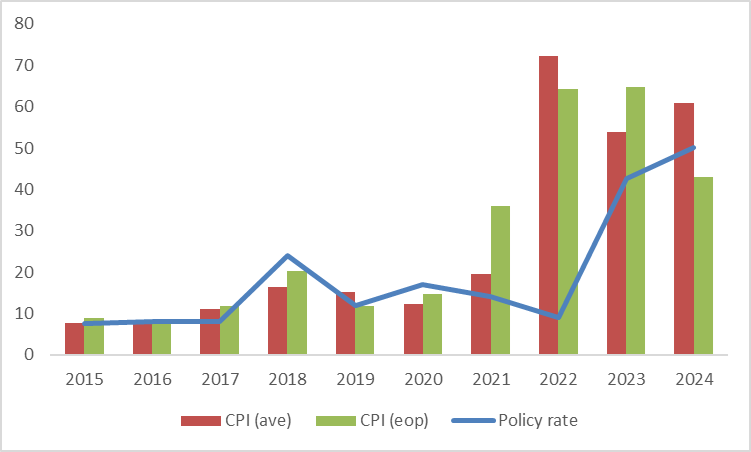

Following negative growth in the second and third quarters of this year, the Turkish economy has shown signs of recovery. Recent improvements in credit growth, the PMI, housing sales, and the current account deficit suggest a positive trend. Economic growth is expected to return to positive territory in the fourth quarter of this year, with full-year growth projected to reach approximately 2.7% next year.

However, Turkey’s biggest challenge remains persistently high inflation. In response to soaring consumer prices, the Central Bank of the Republic of Türkiye (CBRT) has implemented substantial interest rate hikes since mid-2023. While CPI has declined significantly from its peak in 2022, it is still projected to remain as high as 43% by the end of this year (Figure 2). Given this outlook, we expect the central bank to maintain its tight monetary policy stance through 2025.

Figure 2: Turkey policy rate and CPI (%)

Source: Refinitiv, Tradingkey.com

3. Russia

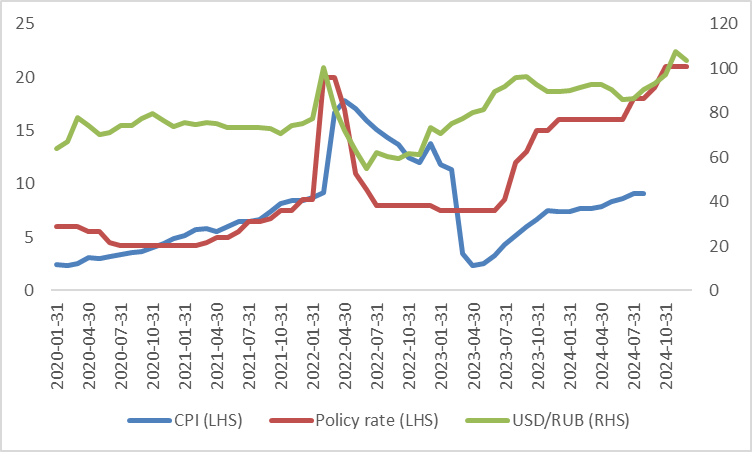

Since the outbreak of the Russo-Ukrainian war in 2022, Russia’s economy has demonstrated resilience, growing by 3.6% in 2023 and projected to expand at a similar rate in 2024, supported by capital and resource reallocation. However, as the war continues, the destruction of national wealth, persistently high inflation, and the ongoing depreciation of the Russian ruble are expected to weigh on economic performance. Real GDP growth is forecast to slow to below 1.5% in 2025.

Meanwhile, heightened inflation expectations and a growing fiscal deficit driven by sharply increased defence spending prompted the Central Bank of Russia (CBR) to raise interest rates by 200bp in October (Figure 3). Looking ahead, the CBR is likely to maintain a tight monetary policy stance, further constraining economic growth.

That said, a potential easing of tensions in the Russo-Ukrainian conflict, such as through diplomatic efforts by a future US administration, could improve the outlook. In such a scenario, Russian inflation could decline, the ruble might stabilize, and economic growth could exceed our baseline forecasts.

Figure 3: Russia CPI, policy rate and USD/RUB (%)

Source: Refinitiv, Tradingkey.com