[IN-DEPTH ANALYSIS] Salesforce: Will Salesforce Be Replaced by AI or Leverage It to Lead?

Key Takeaways

- AI Opportunity and Risk: Salesforce’s decade-long AI investment and Agentforce leverage its clients, but AI could reduce seat demand and commoditize offerings.

- Moat vs. Agility: High switching costs secure its enterprise base, yet its size may slow adaptation to AI-native competitors.

- Growth Dependency: With 8.7% revenue growth and 77.8% margins, success hinges on accelerating growth, signaled by Agentforce adoption in the following quarters.

What Does Salesforce Do?

TradingKey - Salesforce is a leading provider of cloud-based Customer Relationship Management (CRM) software designed to help businesses optimize their interactions with customers, prospects, and partners. Serving as a digital hub, Salesforce unifies critical functions like sales, marketing, customer service, and analytics into one cohesive platform. For example, sales teams can track a lead’s journey from the first outreach to closing the deal, while marketing teams use data to create tailored campaigns.

Advantages:

- Unified Platform: Salesforce’s unified cloud-based ecosystem integrates sales, service, marketing, and analytics, eliminating the inefficiencies of juggling disparate tools. For instance, Walmart uses Salesforce to centralize customer data from over many stores, enabling real-time inventory tracking, personalized offers, and faster issue resolution, all managed through a single dashboard. According to a 2023 study by IDC, companies using Salesforce achieved a 25% reduction in operational silos, improving efficiency by consolidating workflows.

- Customization: Salesforce’s adaptability allows businesses of all sizes, from startups to major corporations, to tailor the platform to their unique needs. Through its AppExchange marketplace, which offers over 7,000 pre-built applications, companies can add features ranging from payment processing to custom forecasting tools. 87% of its users implement some level of customization, underscoring its ability to meet diverse industry demands.

- Migration Difficulty: Once businesses adopt Salesforce, moving to an alternative platform becomes a formidable challenge, with an over 90% customer retention rate. Switching to another solution would involve migrating terabytes of data, retraining employees, and incurring significant costs, efforts that Gartner estimates could cost up to three times the annual licensing fees. This high switching cost ensures Salesforce’s ongoing relevance for its clients.

Disadvantages:

- High Cost: Salesforce’s pricing can deter smaller businesses. As of FY25, a Sales Cloud Enterprise license costs $150 per user per month, with AI-powered add-ons like Einstein priced at $50 or more per user per month. For a 100-person team, this translates to $240,000 annually, before factoring in implementation fees, which range from $50,000 to $500,000 depending on complexity. HubSpot’s 2024 SaaS survey found that 62% of SMBs cited cost as a major obstacle, often choosing more affordable tools like Zoho CRM ($20/user/month).

- Complexity: Salesforce’s vast array of features, spanning over 20 clouds (Sales, Marketing, Service), can overwhelm users. Report found that 34% of Salesforce users leverage less than half of the platform’s capabilities, leading to underutilization. For example, a mid-sized insurance company might use Salesforce for basic sales tracking but ignore its analytics features, paying for tools they don’t use. This complexity frustrates users who prefer simpler, more intuitive solutions.

- Customer Dissatisfaction: Once businesses adopt Salesforce, they often find themselves locked into its ecosystem. For example, Delta Airlines reportedly spent 18 months and $100 million transitioning from legacy systems to Salesforce in 2022. Such migrations are costly and time-consuming. Around 70% of CRM migrations either fail or encounter significant delays due to data transfer and employee resistance.

Why Customers Stay:

Customers remain loyal to Salesforce because of its reliability, scalability, and extensive ecosystem, which includes integration with tools like Slack and Tableau. For large enterprises, years of accumulated customer data stored in Salesforce make switching to a competitor or building an in-house solution a daunting and costly task. High switching costs, both financial and operational, ensure companies remain committed to the platform.

The Competitive Landscape: Traditional SaaS Meets the AI Agent Era

AI Hype vs. Reality in SaaS

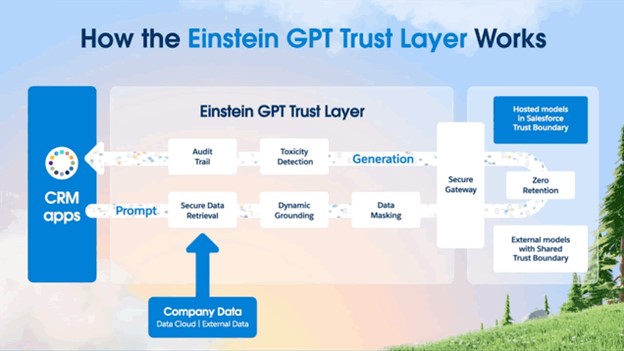

AI is becoming the defining trend in SaaS, with many companies rushing to integrate generative AI and position themselves as “AI-powered.” However, the depth of AI adoption varies significantly. Many providers simply embed ChatGPT-like models into their platforms and market them as transformative innovations. Salesforce, on the other hand, is taking a distinct approach with its Einstein GPT offering—a generative AI layer embedded directly into its CRM platform.

Einstein GPT combines both public and private AI models with Salesforce’s locally stored CRM data to generate personalized and adaptive content. This includes features like auto-drafting emails, predicting customer needs, and curating recommendations, all within Salesforce’s ecosystem. Users don’t need to leave the platform to harness these capabilities, which enhances efficiency and workflow continuity.

Despite these advancements, questions remain about how groundbreaking this approach truly is. Einstein GPT leverages underlying capabilities from ChatGPT and other third-party AI technologies, meaning Salesforce isn’t developing AI models entirely from scratch. Instead, it’s integrating these technologies into its ecosystem. While this enhances productivity and saves sales teams hours of manual work, it raises concerns about how much of Salesforce's AI offering is proprietary versus borrowed from external tech providers.

Salesforce’s AI Focus: The Front Office

Salesforce’s AI strategy focuses on the “front office,” where customer interactions take place. Einstein GPT powers applications across sales (lead scoring), service (automated chatbot responses), marketing (personalized campaigns), and Slack (summarizing conversations). With over 150,000 clients and extensive CRM datasets, Salesforce has a strong foundation for AI commercialization. However, the adoption of these features remains uncertain— how many clients actually use these AI features versus sticking to basic CRM? Existing users are already very proficient with the old tools and may only dabble in AI features, reinforcing inertia.

Source: Salesforce

The SaaS Moat: Established Position vs. Agility Risks

Salesforce’s strength lies in its deeply rooted position among large enterprises. Long-term contracts and the high costs of migrating to alternative platforms make switching difficult and risky. Executives, driven by short-term priorities, rarely push for such upheavals, ensuring Salesforce’s continued dominance.

However, this reliance also creates opportunities for disruption. AI-native startups, free from legacy constraints, could challenge Salesforce with simpler, more affordable solutions. While Salesforce’s AI initiatives, such as Einstein GPT, aim to fend off these threats, its size and complexity may limit its ability to adapt as quickly as smaller, more agile competitors.

AI: Salesforce’s Opportunity or Existential Threat?

The Threat: AI Could Replace CRM Entirely

If AI becomes powerful enough to replace workers, it might also replace tools like Salesforce. Imagine an AI that listens to sales calls, logs data, and builds custom apps—all without a CRM middleman. Companies could bypass Salesforce by integrating AI directly with their product data, a cheaper and more flexible alternative. Klarna’s move to replace Salesforce with AI-built solutions is an early warning shot. Companies are lying off more workers with AI implementation. Fewer employees mean less SaaS demand. Salesforce’s seat-based revenue model, billing based on the number of people using its platform, faces real risk if AI eliminates the humans using those seats. SaaS thrives on upselling: convince clients to buy more seats or add-ons (like AI agents) to save labor costs. However, as AI makes coding more accessible and affordable, companies may begin to question Salesforce’s value. Why pay $150 per user/month when an in-house AI-powered app could deliver similar results at a lower cost? Even if Salesforce nails AI integration, competition could erode pricing power, turning its premium offering into a commodity.

The Layers of Disruption

AI has the potential to disrupt the traditional CRM model at multiple levels:

- Interface Layer: In an AI-driven landscape, humans may no longer need Salesforce’s user interface. AI could process calls, emails, or other interactions and directly feed the data into systems, rendering Salesforce’s UI less relevant.

- Logic Layer: AI is increasingly encroaching on the business logic traditionally built into SaaS platforms. In the future, AI could memorize Salesforce’s entire rulebook, requiring only access to data rather than relying on pre-coded workflows.

- Data Layer: Legacy data platforms like Salesforce face growing challenges from AI-focused startups, such as Vast Data, which excel at handling unstructured data more efficiently. If Salesforce’s Data Cloud doesn’t evolve, it risks losing relevance in an AI-first market.

The Opportunity: Agentforce

Salesforce is responding to these threats with its Agentforce initiative, which embeds AI agents across its platform. CEO Marc Benioff has described Agentforce as a groundbreaking step that leverages a decade of AI investment to provide proactive solutions like automated customer support and predictive sales recommendations. These agents could proactively resolve customer issues or upsell products, boosting client ROI and justifying higher fees. If successful, Agentforce could strengthen Salesforce’s competitive moat, making the platform indispensable in an AI-driven world.

Financial Perspective: Salesforce’s Challenges Amid Slowing Growth

Key Metrics:

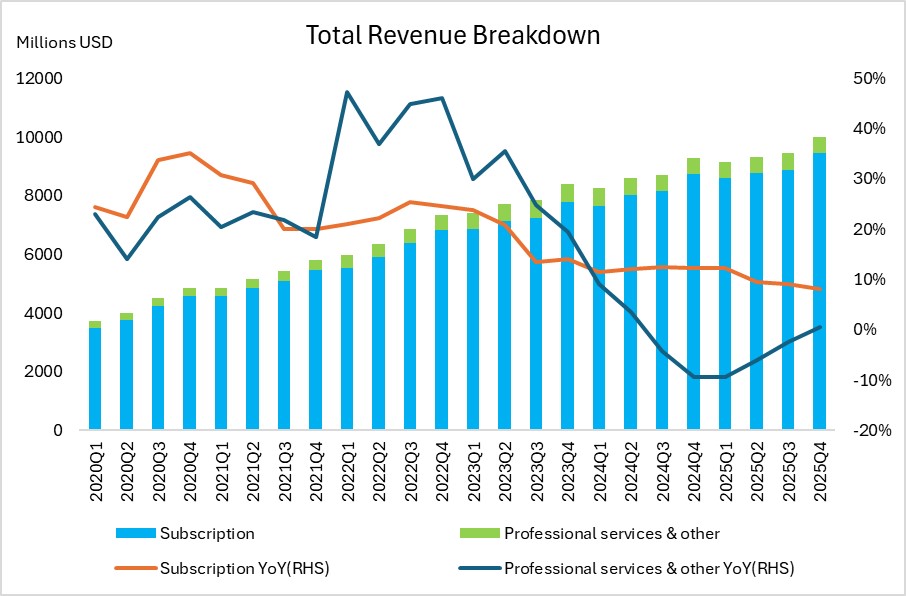

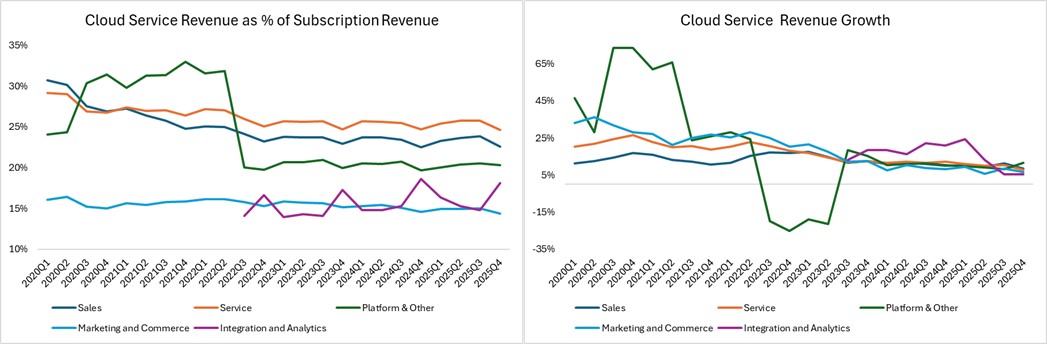

- Revenue Growth: Subscription revenue, a core component of Salesforce’s business, experienced a slight decline. The growth rate is low compared to other SaaS companies. Among cloud service offerings, only the "Platform and Other" category showed growth, while other segments stagnated. This uneven performance raises questions about the strength of Salesforce’s diversified cloud portfolio.

Source: Company Financials, Tradingkey.com

Source: Company Financials, Tradingkey.com

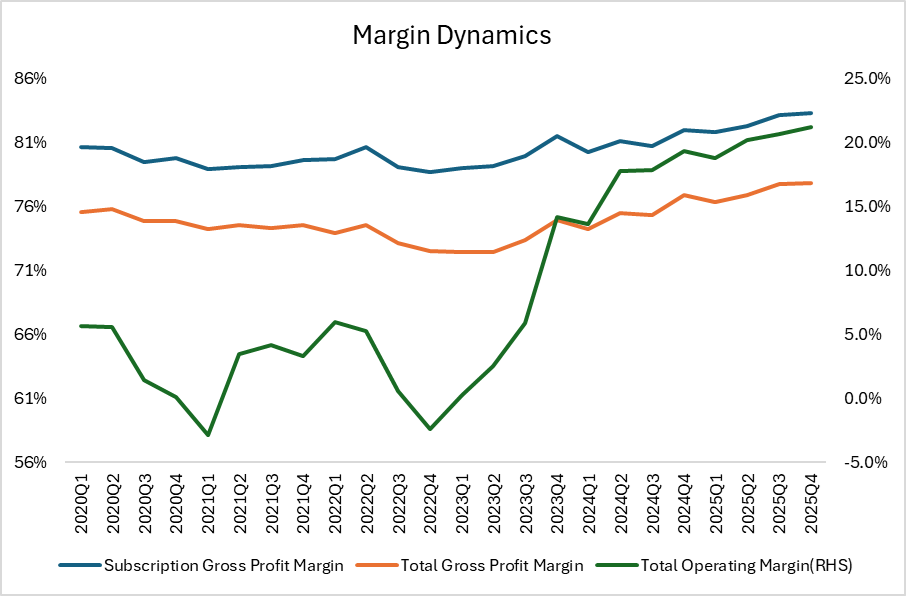

- Profit Margin: Since FY2023, gross profit margins have steadily improved. Subscription margins reached an impressive 83%, with total gross margin at 77.8%—both notably high for the industry. Operating margin has also seen significant gains, reflecting improved cost efficiency or pricing power. Despite these strengths, commoditization looms as a threat. If clients push for cheaper AI-driven alternatives, margins could face pressure, challenging Salesforce’s profitability.

Source: Company Financials, Tradingkey.com

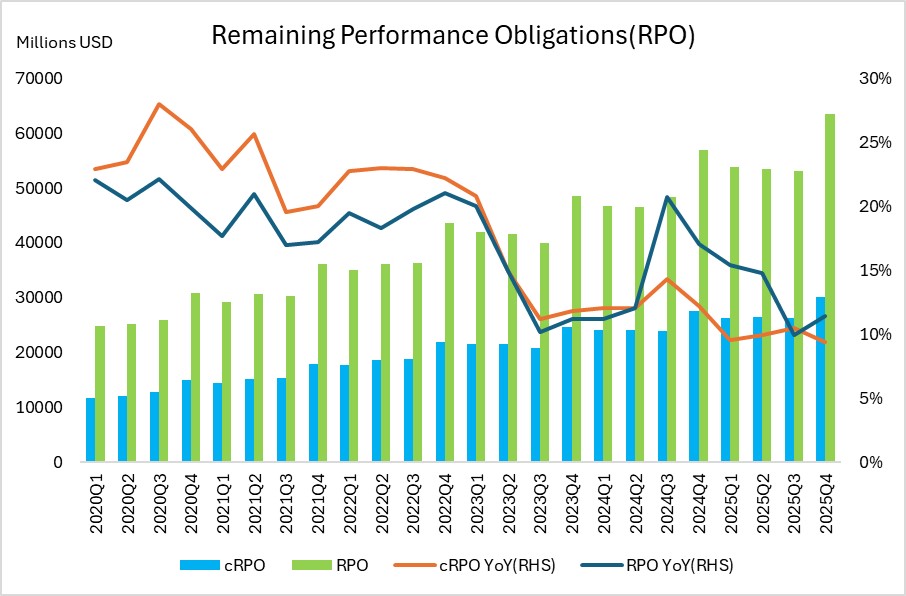

- cRPO (Current Remaining Performance Obligations): cRPO represents the backlog of contracted revenue yet to be recognized, serving as a key indicator of future revenue potential. cRPO grew 9.4% YoY in Q4 FY25, but this growth rate continues to decline, signaling a slowdown in momentum. However, total RPO (Remaining Performance Obligations) YoY growth rate rebounded, offering a more optimistic view of the backlog. The role of AI in driving cRPO growth remains unclear, complicating forecasts about its long-term revenue impact.

Source: Company Financials, Tradingkey.com

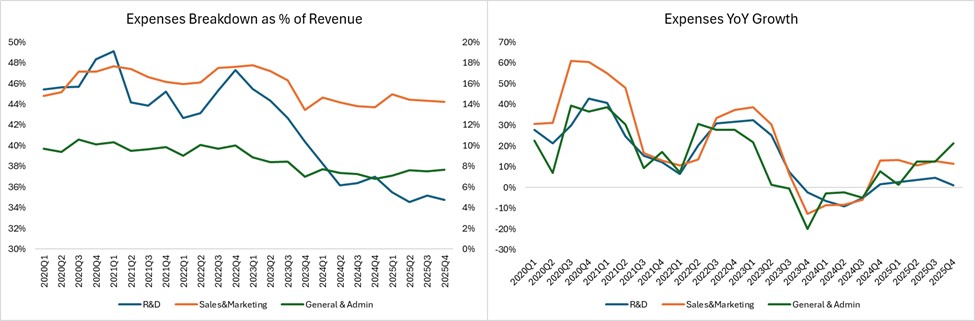

- Operating Expenses: Sales & Marketing have decreased as a percentage of revenue, suggesting improved operational efficiency or a strategic shift in resource allocation. In contrast, G&A expenses are rising relative to revenue. This divergence warrants scrutiny—possible causes could include increased overhead, compliance costs, or investments in non-revenue-generating areas.

Source: Company Financials, Tradingkey.com

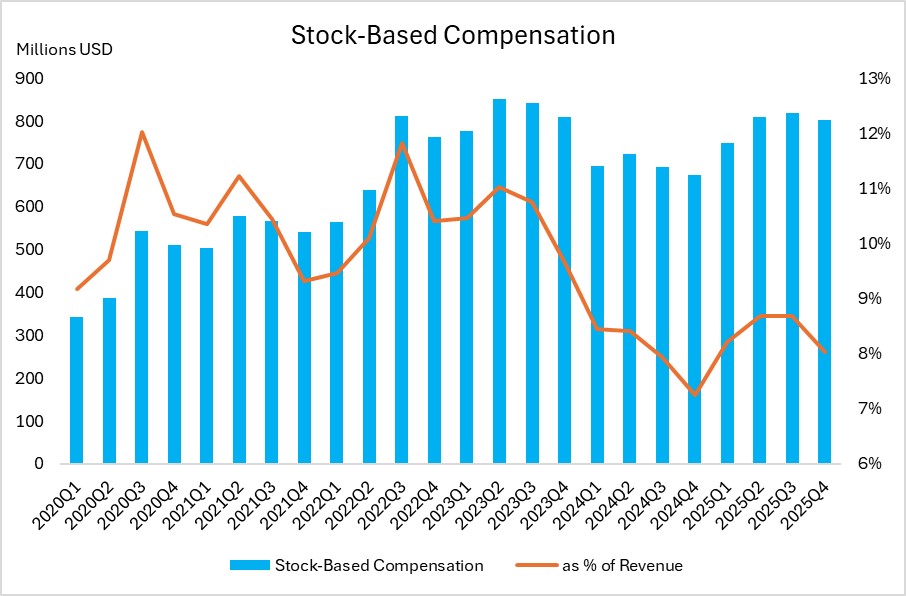

- Stock-Based Compensation (SBC): In FY2025, SBC fell to 8% of revenue. These lifts reported earnings, a plus for GAAP-focused investors, since SBC is a non-cash hit to net income. For Salesforce, a mature SaaS leader, this could signal a shift to tighter equity use to curb dilution. Yet, if it reflects weaker talent incentives, it might strain the Salesforce’s ability to innovate and grow ARR.

Source: Company Financials, Tradingkey.com

Valuation

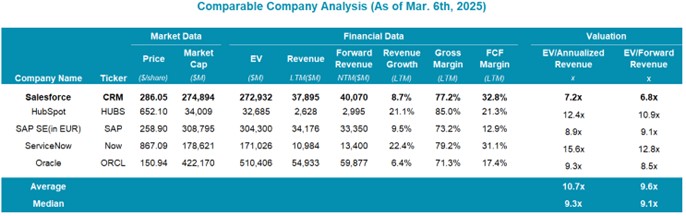

We evaluate Salesforce using the EV/Forward Revenue multiple. With forward revenue at $40,070M and an enterprise value of $272,932M, its current multiple is 6.8x, compared to a peer median of 9.1x. Given Salesforce’s 8.7% growth, which lags ServiceNow (22.4%) and slightly exceeds Oracle (6.4%), its low growth rate suggests a more conservative valuation. We adjust to a 6.5x-7.5x target range, reflecting the modest growth and slowing cRPO.

Applying this to $40,070M yields a target EV of $260,455M-300,525M. Using forecasted FY2026 net cash of $2,354M, equity value ranges from $262,809M to $302,879M, translating to a target price of $273-$315 per share.

Source: Company Financials, Tradingkey.com

Conclusion

Salesforce faces a pivotal moment as the SaaS industry transitions to an AI world. The company’s strengths,150,000 clients, a deeply entrenched platform, and a decade of AI investment, position it well to capitalize on AI opportunities. However, risks loom: AI could reduce seat demand, commoditize offerings, or allow agile competitors to outflank Salesforce.

Investors should monitor the next few quarters’ results for early signs of Agentforce adoption and AI-driven growth. If Salesforce can demonstrate double-digit growth and maintain margins, it will reinforce its market leadership. Otherwise, the risks of commoditization may begin to overshadow its strengths.