Trump Tariffs or Not: Is a Trumpcession Coming?

TradingKey - On Sunday, when asked if he was expecting a recession this year, US President Donald Trump responded: “I hate to predict things like that. There is a period of transition, because what we’re doing is very big. We’re bringing wealth back to America. That’s a big thing. And there are always periods; it takes a little time. It takes a little time, but I think it should be great for us.”

Since Trump's inauguration on January 20, the S&P 500 has dropped 3.8%, falling 6% from its record high on February 19.

Source: TradingView; SPX YTDperformance

Since mid-February, bond yields have begun to decline amid significant uncertainty regarding the new administration’s policies (Treasury yields typically fall during economic recessions). This decline has been primarily led by short-term securities, resulting in a steepening yield curve.

“Prior to this tariff war, the market thought tariffs were inflationary, and now people think they are recessionary,” said Brandywine Global Investment Management’s portfolio manager, Tracy Chen. “So this is a significant shift.”

A Range of Signals Indicating Potential Recession

Recent economic data also paint a bleak picture. Last Wednesday’s ADP payroll report significantly missed expectations, and Friday’s nonfarm payrolls, while not surprising, still fell short of forecasts, indicating a contraction in the labor market.

The Consumer Confidence Index released last Tuesday by the Conference Board for February experienced its largest monthly decline since August 2021, aligning with trends reflected in the University of Michigan’s consumer survey for the same month.

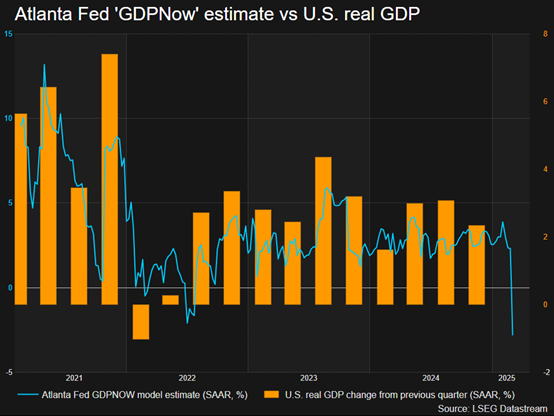

The Atlanta Federal Reserve's GDPNow model, which aims to provide real-time estimates, projected a contraction of 1.5% for the current quarter following new data on trade and consumer spending released last Monday. This figure sharply contrasts with the expected growth rate of 2.3%. A month ago, the model indicated growth in the range of 4.0% for the January-March period.

Source: Reuters

Uncertainty as a Key Factor

Alex Jacquez, who previously worked at the National Economic Council under the Biden administration, pointed out that it is normal for certain sectors to decline during a government's tenure and for economic errors to occur; however, a true recession indicator is when these declines become widespread across various sectors.

He highlighted specific indicators of economic recession, such as whether consumers expect future inflation to rise, which can affect their spending habits and subsequently “spill over” into the real economy. Approximately two-thirds of economic activity in the U.S. is driven by consumer spending, thus, if people start saving rather than spending, it could lead the U.S. and the world into a recession.

Jacquez noted that the decline in Consumer Confidence indicates a 'softening consumer' who is changing their spending habits and is no longer spending at the previous pace. Inflation expectations among consumers surged significantly in February. It is evident that Trump’s tariffs are a pivotal factor.

Can Trump's Tariff Policies Achieve His Goals?

Trump and his advisors believe that his policies will ultimately lead to lower prices for domestically manufactured goods and higher prices for foreign-made goods. Once their policies have time to take effect, they anticipate improvements in the overall economic landscape, including reductions in deficits and interest rates, although many economists disagree with their assessment.

He has asserted that manufacturers have a straightforward way to avoid his tariff storm: by relocating production back to the U.S. If successful, Trump's "tariff-first" strategy could end the long stagnation of U.S. manufacturing output and create jobs that his blue-collar supporters crave.

Meanwhile, Trump has long criticized the global economy as fundamentally unfair and seeks to rebalance America's trade deficits through tariffs.

“Tariffs by themselves can’t be a solution,” said Robert Lawrence, a professor of international trade and investment at Harvard University’s Kennedy School of Government.

Manufacturing industry has changed drastically from last century. Machines in modern factories far outnumber workers. The remaining jobs require higher skills, and wages are no longer superior to those available to workers without a college degree. His sweeping immigration policies could make it more difficult to find new factory workers. Over the past quarter-century, businesses have increasingly relied on factories outside the U.S. and their low-wage labor. Returning manufacturing to the U.S. could significantly increase labor costs, which may be hard for CEOs to absorb.

Last week, Trump agreed to exempt automakers from the 25% tariffs on Canadian and Mexican goods until April 2, at which point he plans to announce reciprocal tariffs. However, supply chain experts indicate that he has also demanded U.S. automakers to begin shifting production back to the U.S. within the next 30 days.

Stephen Blitz, chief U.S. economist at TS Lombard, provided a lively example: “You can’t just tell GM, ‘It’s too expensive to buy headlights from China.’ Nobody makes headlights in the United States. So then all you’re doing is adding cost without really giving time for an adjustment.”

Manufacturers that Trump claimed to want to help have been left scrambling, unsure of where to invest. According to a recent survey by the National Association of Manufacturers, more than three-quarters of respondents indicated that “trade uncertainty” is their biggest challenge, a proportion more than double what it was before the election.

Unpredictable Policies are a Puzzle for Everyone

The Ministry of Finance finds it almost impossible to reduce expenditures—on one hand, the statutory expenditures for social insurance are difficult to decrease; on the other hand, discretionary spending on national defense continues to rise year after year. Also, Trump's strategy of using tariffs to boost revenue, improve employment, and balance trade relations is an ongoing attempt.

However, Trump has consistently failed to provide a clear policy direction. One day he announces a 25% tariff on goods from Canada and Mexico, and the next day he suggests that he may not implement it. Tariffs on imports of metals, lumber, semiconductors, and pharmaceuticals are subject to change, with potential exceptions that may or may not be applied. In an environment where regulations are consistently shifting, businesses are left uncertain about their investment strategies.