[IN-DEPTH ANALYSIS] Nike (NKE): Will This be the Greatest Turnaround Story of this Decade?

Source: TradingView

Key Points

· Nike is the largest and most well-known athletic and footwear apparel brand globally, but it is currently facing declining revenue and shrinking margins.

· Nike management made two strategic mistakes – 1) Excessively focusing on directly-owned stores and e-commerce, souring relationships with wholesalers and 2) Trailing behind with innovation.

· As a result, the company struggles with declining market share, slower growth than peers, excessive inventory and eroded brand value.

· After the change of the CEO, Nike seems to have figured out the problems and is taking action to fix them.

· Collaboration with Kim Kardashian’s Skims will bring certain tailwinds, however, it will take at least a year to see positive revenue growth and margin expansion.

Company Overview

TradingKey - Nike Inc (NYSE: NKE) designs, develops, markets, and sells athletic footwear, apparel, equipment, accessories, and services worldwide. It is the largest seller of athletic footwear and apparel in the world. Nike sells products from its namesake brand and Converse.

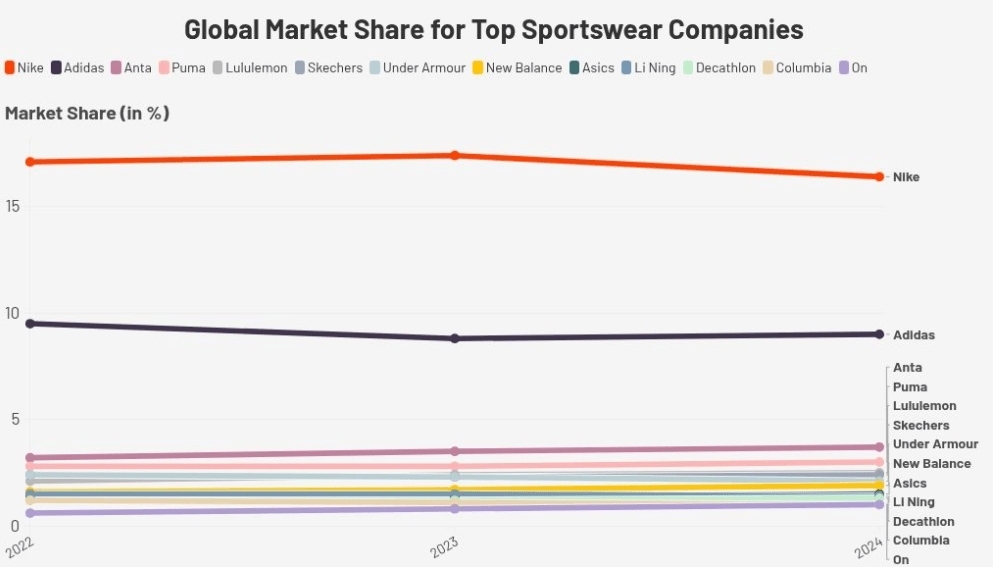

Source: Euromonitor

Nike has a strong presence in the following markets: running (athletics), apparel, sports equipment, basketball, and football.

Nike is one of the most iconic and recognizable brands in the world in the last forty years. What kept them on the top all these years is their very strong brand image and their marketing strategy of collaborating with the top athletes in every big sport globally. Without a doubt, the most successful athlete collaboration of Nike is with Michael Jordan - Air Jordan brand, which represents roughly 15% of the total company revenue in the last fiscal year. Nike has the most recognizable logo for a clothing brand, and it is known for the slogan “Just Do It”.

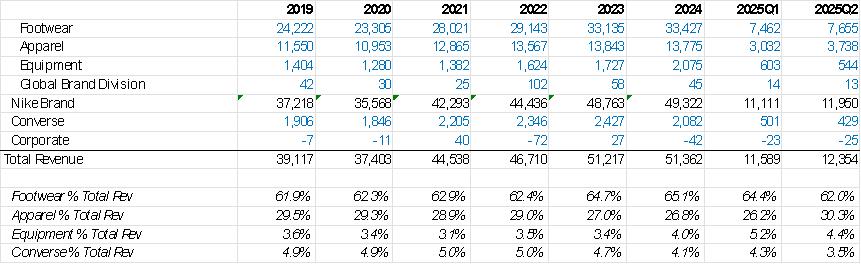

Source: SEC Filings, TradingKey

In terms of products, two-thirds of the revenue normally comes from footwear (that includes the Converse brand also), while the rest is from apparel and equipment.

Source: SEC Filings, TradingKey

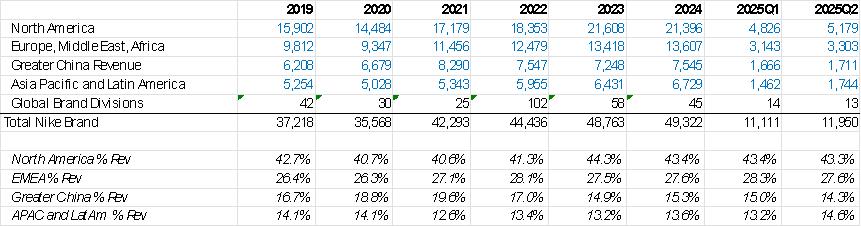

In terms of geography, as an American brand, Nike has strong roots in North America with nearly half of the revenue coming from there. In contrast, their major competitor Adidas (German brand) is more exposed to EMEA.

Source: SEC Filings, TradingKey

Nike's distribution network is categorized into two main sales channels:

Nike Direct (Direct-to-Consumer): The company sells directly to consumers through company-owned physical stores and its online portal. Nike's physical stores represent 70% of the DTC revenue, while the remaining 30% comes from e-commerce.

Wholesale: Nike uses a mix of independent distributors, retailers, licensees, and sales representatives in many countries worldwide. Some of the biggest retailers of Nike products are Foot Locker, Champs Sports, Finish Line, and Dick’s.

The dynamic between DTC and wholesale has been the centerpiece of what has been happening to the company in the past five years.

What Happened to Nike?

Currently, the sports giant is going through one of its toughest times in decades with declining growth, shrinking margins and eroding brand image. The crisis seems even more painful once we see it in the context of a strong consumer sentiment in the past two years as other sports brands have been doing significantly better.

Source: SEC Filings, TradingKey

Source: SEC Filings, TradingKey

Source: SEC Filings

Source: SEC Filings, TradingKey

DTC Missteps

With the boom of e-commerce in the 2010s, Nike decided in 2019 to make a major change in their strategy by focusing more on the DTC channel, developing its own store network, and cutting off third-party retailers. At that time, this decision seemed perfectly reasonable due to the numerous benefits of a DTC approach.

Higher Margins: Selling directly to consumers allows Nike to capture higher profit margins by cutting out the wholesalers and retailers that charge a percentage of the end price.

Better Customer Relationships: Nike could build a stronger relationship with its customers and gather valuable first-party customer data.

More Control: Nike could better control how its brand is perceived by the public. Also, DTC allows quicker product launches and more efficient inventory management.

Nike exited several large wholesale accounts and pulled their best products from others. Initially, the plan worked quite well, especially in the context of the Covid lockdowns where people avoided visiting physical stores but opted to shop online.

Source: Euromonitor

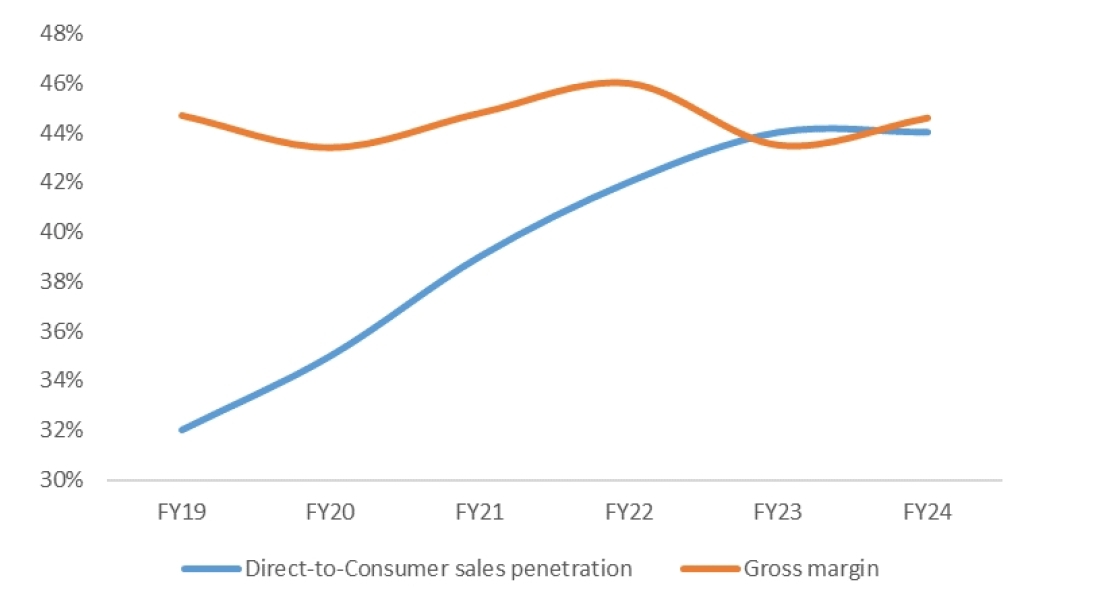

However, soon things went wrong. To remain competitive, retailers decided to slash prices. At the same time, Nike accumulated an enormous amount of inventory in 2022. This forced Nike to cut the prices of its products, pulling gross margins down.

The gross margin should have been significantly higher due to the higher portion of the DTC channel, but there was no margin increase because they had to apply discounts and promotions. Another reason for the lack of margin expansion is that Nike had to take on the role of a distributor and ramp up investments in physical stores and online infrastructure. Instead of eliminating the middleman, they became the middleman themselves.

Eroded Brand Value

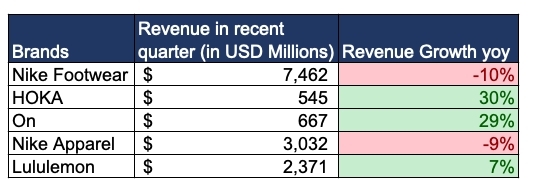

When Nike exited third-party retailers' spaces, competitors took advantage of the void left and pushed their products to the retailers. Once the lockdown was over and customers returned to physical stores, they found other brands on the shelves – Adidas, New Balance, On, and Hoka.

Moreover, with the excessive focus on developing the DTC channel, Nike trailed behind in product innovation. On top of all this, with inventory clearance and major discounts, Nike has lost some of its premium brand status, diluting the premium perception of its products among customers.

Source: Euromonitor

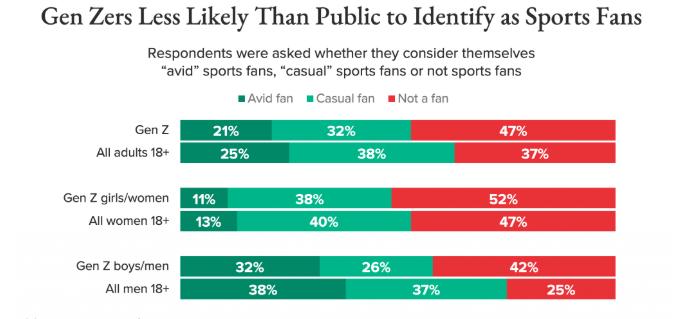

Another reason, more macro in nature, is the general trend of Gen Z consumers to be less interested in sports than previous generations. As a company that relies on athletes as brand representatives, Nike can find less appeal among young people.

Source: Morning Consult

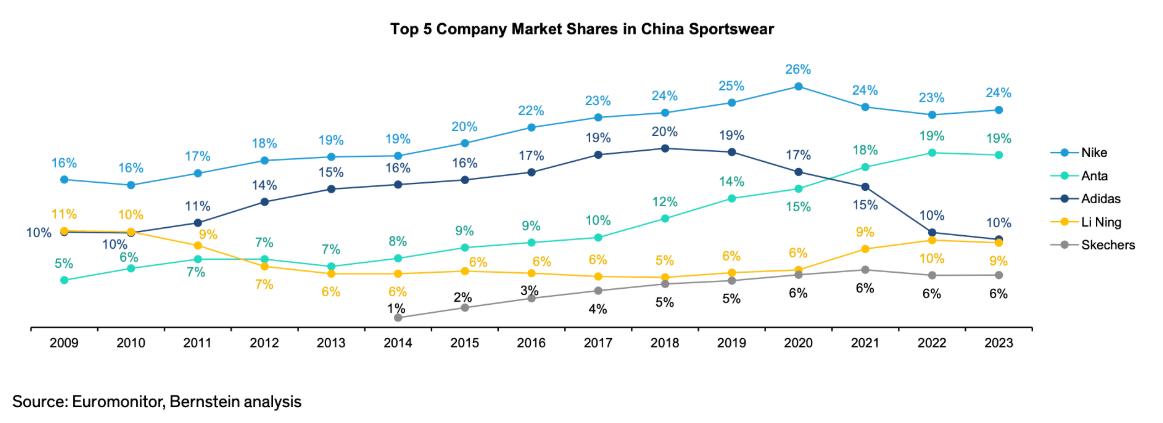

China Market

The company has significant exposure to China, accounting for 15% of its revenues. Although it is not as important a market as North America, it still holds considerable weight. However, the market has become increasingly challenging to navigate due to fiercer competition from local players like Anta and Li Ning, and a shift in consumer sentiment favoring local brands.

Source: SEC Filings, TradingKey

What is the Plan for Nike?

CEO transition from John Donohoe to Elliot Hill

Nike appointed Elliot Hill as CEO in October 2024 to replace John Donohoe. Donohoe's stint with Nike was clearly not successful. He has a strong technology background, having worked for eBay and ServiceNow, and his focus was on growing Nike’s e-commerce channel. However, he lacked an understanding of sales, marketing, and branding, and the consequences are now obvious.

Hill, on the other hand, is a Nike veteran who started at the company as an intern back in the 1980s. His area of expertise is sales. He retired in 2020 after a 30+ year tenure with Nike but decided to return to help bring the sports giant back to its feet.

Re-focusing on Wholesale

Nike is back to doing in-person key account meetings, bringing partners back to HQ, re-engaging those relationships, and discussing products for future seasons. They are now more comfortable with the teams in place, their focus, and speed-to-market capabilities.

Collaboration with SKIMS

A big positive development for Nike is the recently-announced collaboration with Kim Kardashian’s clothing brand SKIMS. Nike has always collaborated with the biggest names in sports, and now they will work with one of the biggest influencers (the eighth most followed account on Instagram).

The collaboration can increase Nike’s presence in two fast-growing market segments: 1) the athleisure market - a style of clothing designed to be worn both for athletic activities and for general, everyday use; and 2) the women's sports business. Both these markets are growing at around 10% annually – higher than the general clothing market.

Outlook and Valuation

Identifying the problem is already half the solution. We believe the current management has the awareness of the situation and the capabilities to turn the company back on track. The turnaround will probably take a while.

2025 will be a transitional year, and we expect revenue to shrink by high-single digits, especially in the context of deteriorating consumer sentiment. In 2026 and 2027, Nike is projected to return to single-digit percentage positive growth as the current policies begin to reflect in the financial results.

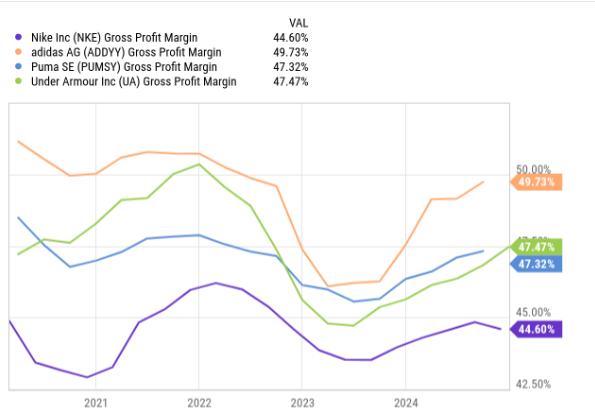

In terms of gross margin, the current number is 44.5%, but we expect it to reach 47% by 2027, in line with peers. With these assumptions, NKE is currently trading at 16 times the expected 2027 earnings. This is lower than the normal historical valuation of 20x, implying an upside potential of 25% for the current price. However, the re-rating towards the target price will happen over the span of 1-2 years, making it a less attractive investment.