January CPI Preview: Severe Divergence in the Inflation Outlook—Time to Adjust Allocations?

TradingKey - Ahead of the release of the US January CPI report, inflation expectation surveys from the University of Michigan and the New York Fed have shown a rare divergence. With the escalation of Trump's tariffs, the trajectory of US inflation has garnered significant attention.

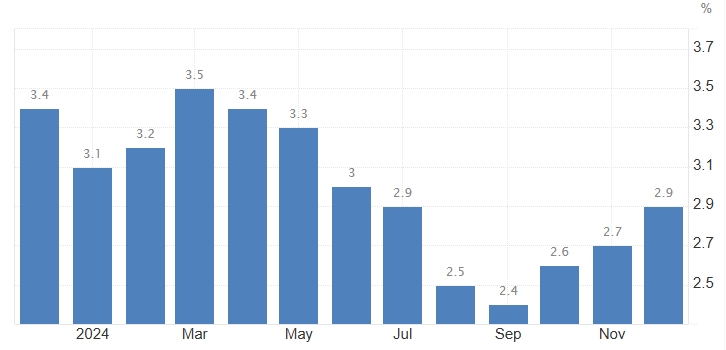

On Wednesday, February 12, the US Bureau of Labor Statistics will release the January Consumer Price Index (CPI) report. Market expectations suggest that the year-over-year growth rate of the overall CPI will reach 2.9%, unchanged from December 2024. Meanwhile, the core CPI, which excludes volatile food and energy components, is expected to rise 3.1%, slightly lower than the previous reading of 3.2%.

[Trend of the US CPI, Source: Trading Economics]

Since hitting a low in October last year, overall US inflation has been on an upward trend, rebounding for three consecutive months. Wall Street analysts anticipate that January's CPI will remain stable or decline slightly, yet inflation remains persistent, making it likely that the Federal Reserve will hold rates steady in March.

Will Inflation Exceed Market Expectations?

TradingKey analyst Jason Tang believes January's inflation data could surpass market expectations, citing the following reasons:

1、 Although nonfarm payrolls in January declined compared to December of last year, the growth rate of average hourly earnings, labour force participation rate, and unemployment rate all performed strongly, surpassing expectations and prior values. This indicates that the US labour market remains resilient, and a tight labour market typically exerts upward inflation pressure.

2、Looking at the CPI subcomponents, recent high-frequency data shows that several key indicators have rebounded. For example, the S&P CoreLogic Case-Shiller Home Price Index and Zillow Rent Index (corresponding to the housing component of CPI, accounting for 37% of the CPI basket), the CRB Food Index (corresponding to the food component, 13%), the Manheim Index (corresponding to the transportation component, 6%), and US retail gasoline prices (corresponding to the energy component, 3%) have all shown an upward trend. The recovery in these subcomponents suggests that both the CPI and core CPI for January could be higher than the previous readings.

In summary, based on the strong performance of the labour market and the rebound in multiple CPI subcomponents, there is a possibility that January's US inflation data will exceed expectations.

Growing Divergence in Inflation Expectations

Two key inflation surveys—widely followed by economists—have revealed a stark divergence in expectations.

- University of Michigan Survey (February):

-> One-year inflation expectations surged from 3.3% in January to 4.3%, the highest level since November 2023.

-> This increase was largely driven by differing political views on Trump's tariffs: Democrats expect inflation to rise to 5.1% in the next year; Republicans anticipate it dropping to 0.0%.

- New York Fed Survey (January):

-> Five-year inflation expectations rose to 3%.

-> One-year and three-year expectations remained at 3%, showing stability.

This divergence in expectations complicates the Federal Reserve's interest rate path, making it crucial to watch Fed Chair Jerome Powell’s remarks during his "Capitol Hill Visit" this week.

How Will the Market React?

Trump's policies are emerging as a key variable in US inflation trends.

- Deutsche Bank warns that tariff escalations could fuel trade tensions, potentially triggering a stock market correction.

- Barclays suggests that given rising risks in US equities, including economic concerns and profit concentration in a few companies, diversifying into other stock markets may be prudent.

- Amid stubborn inflation and rising risk aversion from tariffs, gold prices have hit new all-time highs in recent days. UBS recommends a balanced allocation between US stocks, high-grade bonds, and gold to hedge against tariff-related risks.