PCE Inflation: What’s the Market Expecting Ahead of Key Data Release?

TradingKey - Inflation has been grabbing the headlines given markets are watching the every move of the US Federal Reserve (Fed) when it comes to interest rates.

Lower, cooler inflation should technically lead to lower long-term rates. However, the headline consumer price inflation (CPI) index isn’t actually what the Fed uses to determine how hot prices are.

Instead, the Fed’s preferred measure of inflation is the personal consumption expenditures (PCE) index and it usually comes out at the end of the following month. So, December 2024’s PCE figure is being released by the Bureau of Economic Analysis (BEA) next Friday (31 January) before the market opens.

It will be a key data point for the Fed as it looks to the next Federal Open Market Committee (FOMC) gathering in March, after the 28-29 January one taking place next week, where it will make a decision on interest rates.

Here’s what you need to know about the index, why the Fed prefers it as a measure of inflation and what investors can expect for next week’s number.

PCE Price Index: What is it?

The PCE Price Index is actually a useful indicator of the level of prices that consumers spend on goods and services in the US. According to the BEA, the PCE accounts for around two-thirds of domestic spending, giving economists a useful window into the broader price levels within the US economy.

Crucially, the so-called core PCE Price Index excludes things like food and energy items – given these can be highly volatile in nature. As a result, it gives the Fed a clearer picture of the true rate of inflation in the US economy.

Unlike the headline CPI data – which only tracks out-of-pocket spending by urban households – the PCE Price Index tracks spending by all households in the US, including rural areas, as well as spending on behalf of households.

One other key difference is that the CPI tracks a set basket of goods and services whereas the PCE Price Index look at a more comprehensive series of data points related to goods and services, including medical care paid for by employers or the government.

Why the Fed uses it and the outlook for PCE

Generally, the Fed prefers PCE because it gives a more accurate picture of spending patterns “on the ground” in the US as it relates to the consumer and prices. Furthermore, the PCE index is more dynamic in nature as it’s weighted more frequently (monthly) versus CPI (which is annually-weighted).

The crucial measure of inflation has been moderating in recent months – providing succour to market participants out there that are hoping for more rate cuts from the Fed this year.

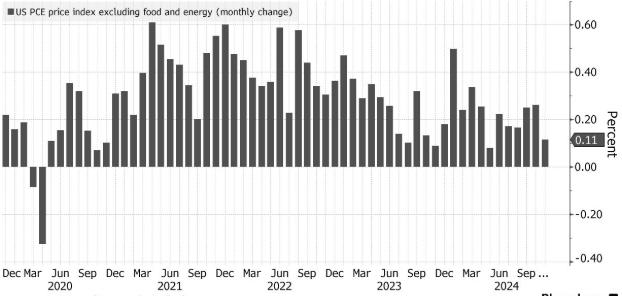

However, one of the key data points came last month during November’s PCE Price Index release. That showed that core PCE increased just 0.1% month-on-month, marking a noticeable drop after monthly PCE figures had stalled out in prior months.

Breaking the December PCE data down further, core services prices rose 0.2% month-on-month, recording its slowest advance since August. Meanwhile, core goods prices – excluding goods and energy – fell for the first time in three months.

US core inflation moderates in December

Sources: Bloomberg, BEA

As a result of that data – out on 20 December – Treasury yields and the US dollar remained lower, insinuating that the Fed could cut more in 2025. Of course, that thought was nipped in the bud by a much stronger-than-expected payrolls report for December, which was released early this month.

What is the market expecting for PCE?

The outlook for PCE heading into next week’s print is relatively optimistic given recent data points that have been released. For example, on 14 January, it was revealed that US wholesale inflation had unexpectedly cooled off in December.

The so-called producer price index (PPI) for final demand rose 0.2% month-on-month and was well below a median forecast of economists that forecast a 0.4% monthly gain. Then came December’s CPI data just a day later (15 January) which, while higher than expected, actually saw core CPI expand just 0.2% month-on-month – after having been stuck at 0.3% since August.

Heading into next week, the market is relatively sanguine that the core PCE data will be relatively benign. If it does come in as expected, or lower, then a market rally could certainly be on the cards.

However, if it’s hotter than expected, and the underlying data suggests that some of these drivers of elevated prices aren’t temporary, then the market could see a sell-off on the back of pessimism as it relates to potential rate cuts from the Fed.

Investors should remember that the Fed remains “data-dependent” and that no single data point is going to determine their policy on interest rates. Rather, it’s an amalgamation of data points that could end up pointing towards a trend – as many Fed board governors have said.

Given this, it’s important to put the PCE data into context but also be prepared to be flexible to position accordingly within your portfolio when the PCE data is released before the market opens on Friday 31 January.