1 Super Stock Down 80% You'll Regret Not Buying on the Dip

Upstart (NASDAQ: UPST) went public in December 2020 priced at $20 per share. In less than 12 months, its stock rocketed 20-fold to $401 on the back of historically low interest rates, which were a tailwind for its artificial intelligence (AI)-powered loan origination platform.

That tailwind turned into a headwind in 2022 when the U.S. Federal Reserve aggressively hiked interest rates, which plummeted consumer demand for loans. Upstart stock proceeded to sink 97% from its all-time high to a low of around $12.

However, Upstart's AI-originated loans performed well under challenging economic conditions, and its business is now on the upswing. Its stock price has roared back to around $78 as of this writing, but that's still 80% below its all-time high. I think a further recovery is in the cards, so here's why investors might regret not buying the dip.

Transforming the lending industry with AI

Banks have used Fair Isaac's FICO scoring system to determine the creditworthiness of borrowers since 1989. FICO uses five core metrics to determine someone's ability to repay a loan, including the size of their existing debt and their payment history.

Upstart thinks that approach is outdated. It designed an AI algorithm that analyzes 1,600 different metrics for a potential borrower to gain a better understanding of their ability to repay a loan and help determine the interest rate they should be charged. AI can perform that analysis instantly, whereas it might take a human assessor days or even weeks. That also allows Upstart to automate a staggering 91% of loan decisions, with no human intervention.

When it comes to risk, Upstart's latest AI model, called Model 18 (M18), makes 1 million predictions for every applicant to arrive at the appropriate interest rate, which is 6 times the number of predictions its previous model could make. The end result is a fairer and more accurate outcome for the borrower.

Overall, Upstart says its AI-based approach allows it to approve double the number of loans compared to traditional assessment methods, at an interest rate that is around 38% cheaper, on average. In other words, by analyzing so much data, it's likely that Upstart is capturing thousands of high-quality deals that traditional assessment methods are overlooking.

Unsecured personal loans are Upstart's bread and butter, but it also has a growing presence in the secured car lending and home equity line of credit (HELOC) segments. Demand is picking up across all three at the moment because interest rates are coming down.

Image source: Getty Images.

Upstart's revenue just hit a high point for 2024

Upstart operates an origination platform that approves loans for customers but then offloads the loans to lending partners. If things are working as they should, it doesn't keep those loans on its books. However, it did use its own money to fulfill a portion of the loans it initiated during a difficult period in 2022 and 2023 when partner funding dried up because of soaring interest rates, and that's one of the reasons its stock plummeted. Investors weren't comfortable with the company taking on that credit risk.

In normal circumstances, Upstart simply earns a fee every time its algorithm approves an application on behalf of its bank and credit union partners. Those partners can also pay to license Upstart's software, so they can embed it into their own online loan application processes.

During the third quarter of 2024 (ended Sept. 30), Upstart originated 186,786 unsecured personal loans, which was a whopping 65% increase from the year-ago period. It also originated 1,080 car loans, which was down year over year, but up 53% from just three months earlier. The company announced a new funding deal with Blue Owl (an asset management firm), which will buy $2 billion worth of loans over the next 18 months to help absorb that growing demand.

That follows billions of dollars' worth of deals with other third-party funding partners over the past year, as their appetite for risk gradually returns. That is key, because Upstart has to fulfill loans in order to get paid and generate revenue growth.

On that note, the company delivered $162 million in total revenue during Q3, which was up 20% from the year-ago period. It was the largest amount of revenue the company delivered in a quarter this year, and that 20% growth rate was a positive turnaround from the 6% drop it delivered in the second quarter.

Why Upstart stock could move higher from here

Upstart stock is up by around 500% from its 2022 low point, so a recovery is certainly underway. However, it could continue for at least the next couple of years.

The company is on track to deliver $587.5 million in total revenue in 2024, which would be a 14% increase from 2023. But looking further ahead, Wall Street's consensus forecast (provided by Yahoo! Finance) suggests the company will deliver $812.7 million in revenue during 2025, which would mark an accelerated growth rate of 35%.

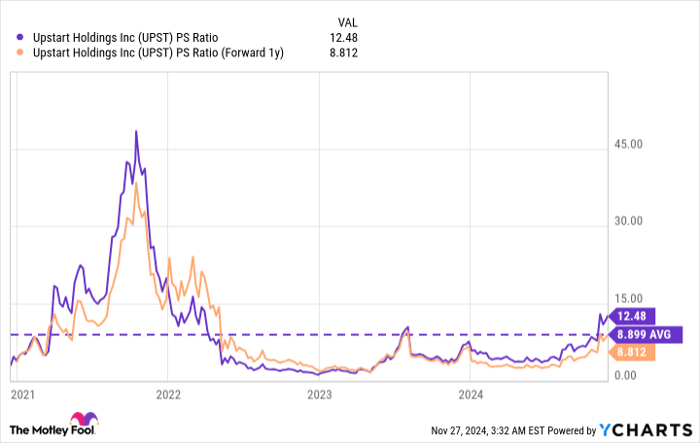

Upstart stock currently trades at a price-to-sales (P/S) ratio of 12.4, which is a premium to its long-term average of 8.9 going back to when the company came public in 2020. However, based on Wall Street's 2025 revenue forecast, Upstart's forward P/S ratio is just 8.8, which is slightly below its average:

UPST PS Ratio data by YCharts

In other words, investors who are willing to hold Upstart stock for at least the next year could be getting a good price right now. However, the real opportunity will likely be realized over the longer term, because the company has identified a whopping $3 trillion worth of annual loan originations in its addressable market across unsecured personal loans, car loans, home loans, and small business loans.

Considering Upstart has only originated around $40 billion worth of loans so far in its history, it hasn't even scratched the surface of its opportunity. If the company continues to execute its strategy, long-term investors could reap substantial rewards.

Don’t miss this second chance at a potentially lucrative opportunity

Ever feel like you missed the boat in buying the most successful stocks? Then you’ll want to hear this.

On rare occasions, our expert team of analysts issues a “Double Down” stock recommendation for companies that they think are about to pop. If you’re worried you’ve already missed your chance to invest, now is the best time to buy before it’s too late. And the numbers speak for themselves:

- Nvidia: if you invested $1,000 when we doubled down in 2009, you’d have $350,915!*

- Apple: if you invested $1,000 when we doubled down in 2008, you’d have $44,492!*

- Netflix: if you invested $1,000 when we doubled down in 2004, you’d have $473,142!*

Right now, we’re issuing “Double Down” alerts for three incredible companies, and there may not be another chance like this anytime soon.

*Stock Advisor returns as of November 25, 2024

Anthony Di Pizio has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Upstart. The Motley Fool recommends Fair Isaac. The Motley Fool has a disclosure policy.

Related Articles

Amazon Stock Predictions for 2026 to 2030: Will They Exceed Expectations and Achieve Major Long-Term Goals?

TradingKey - As we head into 2026, many investors are questioning where Amazon (AMZN) fits into the technology world.

A Crash After a Surge: Why Silver Lost 40% in a Week?

TradingKey - Spot silver (XAGUSD) prices continue to decline. Silver plunged 20% on Thursday, breaking below $71 per ounce, with the sell-off intensifying on Friday as prices fell further below $64. Compared to the all-time high set on January 29, silver prices have retraced more than 40%, wiping out nearly all gains accumulated over the previous month.

Is Bitcoin’s Four-Year Cycle Dead in 2026?

Is the Bitcoin 4-year cycle dead? After 2025 broke historical records with a red post-halving year, institutional analysts explore if the Bitcoin price has decoupled from the halving countdown. Analyze the impact of spot ETFs, global liquidity, and the roadmap to the 2028 halving in this 2026 market

USD Dollar Trend Forecast: Dollar Index Falls Below 97.0 to 4-Year Low, Will the Dollar Continue To Fall or Bottom Out in 2026?

TradingKey - In January 2026, the US Dollar Index continued its downward trend from 2025, officially breaking below the key 97.0 level and reaching a low of 95.5, marking a nearly four-year low since February 2022.