Why Did SanDisk (SNDK) Stock Crash? AI Chip Selloff, Valuation, and What's Next

AI Podcast

SanDisk Corporation experienced a sharp decline in early July due to a broader semiconductor sector rotation and concerns over stretched AI-related valuations, rather than company-specific headwinds. Despite a 640% year-to-date gain, the stock remains supported by strong long-term demand for AI-driven flash memory and a strategic partnership with Kioxia. While analysts remain divided on valuation, risks include insider selling, reliance on spot market pricing, and competitive pressures. Technical indicators suggest potential exhaustion of the sell-off, though volatility is expected until management provides further clarity on enterprise SSD demand and contract growth through 2028.

TradingKey - SanDisk Corporation (NASDAQ: SNDK) had one of its worst trading sessions of the year in the two days before the July 4 holiday, losing about 10% on one day and 14% the next. The stock has been confused with its former parent, Western Digital (NASDAQ: WDC), and the two have been trading separately since SanDisk's spinoff was completed in February 2026. It is SanDisk's flash-memory business, not Western Digital's hard-drive operations, that has become one of the most talked-about AI trades of 2026 — and the one that just hit a wall.

What Actually Caused SanDisk's Stock to Drop?

The sell-off wasn't triggered by bad news from SanDisk itself. On July 1, the Philadelphia Semiconductor Index plunged more than 6% in one day, while SanDisk sold in sympathy, declining by more than 10% as a wider rotation out of AI and chip stocks. The sentiment worsened further following remarks by Federal Reserve Chair Kevin Warsh that valuations of assets were becoming stretched.

SanDisk lost 14.13% on the next day, closing at $1,745 before making a modest recovery after hours. Rival Micron also plummeted, as did Kioxia, the NAND manufacturing partner of SanDisk listed in Japan, which fell as much as 12% in Tokyo. This was not a move by SanDisk, but rather a repricing across the entire industry, following months of record profits.

How Sharp Was the Sell-Off, and Where Does the Stock Stand Now?

The magnitude of the move can be better understood in context. Data compiled by The Motley Fool via Robinhood shows that SanDisk has been one of the best stocks in the S&P 500 in 2026, having jumped nearly 640% year to date and more than 6,000% since it spun off from Western Digital.

The stock is trading at around $1,810, which has the company's market cap nearing $272 billion and its price-to-earnings ratio exceeding 60, down from the 52-week high of $2,354.39 but still well over the 52-week low of $40.10. The drop broke SanDisk below its 20-day moving average for the first time in months, a signal that often invites further short-term selling before buyers step back in.

Has the AI Memory Boom Ended or Is It Taking a Break?

The long-term demand narrative is still intact. Earlier this month, SanDisk and Kioxia announced that they had just begun volume production of 10th-gen 3D flash at their Fab2 plant in Iwate, Japan, using their CBA (chip bonding architecture) design to combine memory and logic directly in order to achieve even higher densities and lower power consumption. The two companies have also agreed to extend the term of their NAND venture partnership until December 2034, and the partnership has been key in advancing flash technology for more than two decades.

Demand for large volumes of data storage in the data center continues to build as hyperscalers continue to pour money into AI, but supply has remained tight relative to prior cycles since there have been years of sluggish price growth leading to sluggish capacity growth. That's what is keeping most analysts from trimming their forecasts on the stock given the recent pullback.

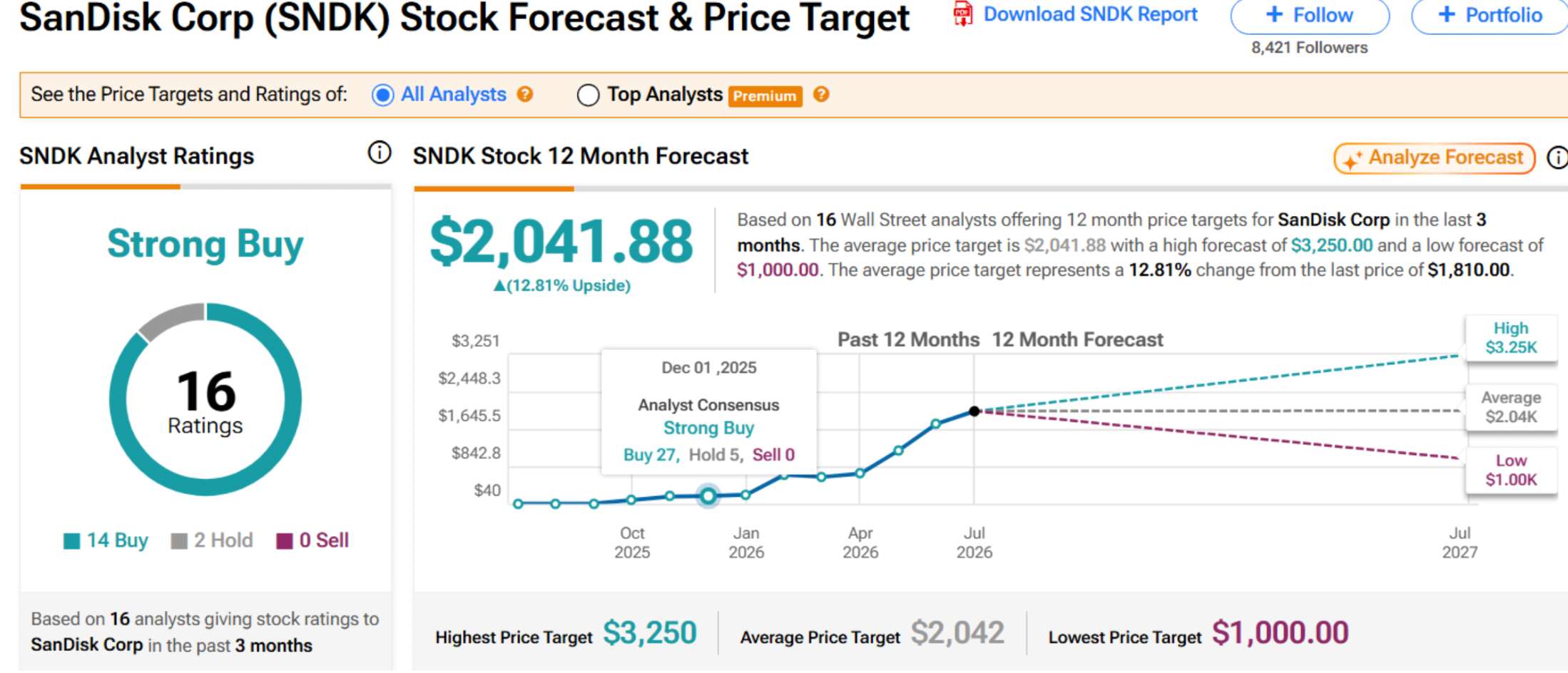

Analysts' Opinions on SanDisk's Valuation

Wall Street still has a split on how high the stock can go. Bernstein has set a $3,000 price target, while Citigroup and Bank of America are both looking for $2,500. In a wider sample, data from TipRanks shows that 16 analysts have price targets ranging from $1,000 to $3,250, with an average of $2,041, just a bit higher than the current share price, suggesting some real differences in the degree to which analysts think SanDisk's growth is already being valued.

Souce: TipRanks

Skeptics highlight details: data reveals that insiders have been selling off shares over the last three months, while SanDisk has a GF Score of only 46 out of 100, and analysis suggests that only one-third of its anticipated fiscal 2027 revenue is guaranteed under contract, with about 60% of NAND output subject to spot market pricing if supply conditions improve.

What Investors Need to Pay Attention To Next?

From a technical chart perspective, the $1,987 to $2,084 zone is where the stock needs to move higher on a daily basis, having recently fallen below a number of technical moving averages. Beyond that, it will ultimately be up to management commentary to provide visibility into enterprise SSD demand, contract price renewals, and hyperscale growth commitments through 2027 and 2028.

Competition will remain an issue, and SanDisk will be fighting back against the likes of Samsung Electronics, SK Hynix, and Micron Technology which are rolling out similar AI-memory technology, as well as China's lower-cost NAND players, which will continue to put pressure on pricing power over the longer term.

What Does This Mean for Investors Weighing SNDK Right Now?

Wall Street is mixed on the share price upside. Bernstein set a price target of $3,000 per share, while Citigroup and Bank of America set price targets of $2,500 per share. In a broader data set, analysis shows that 16 analysts have price targets between $1,000 and $3,250 with an average target of $2,041 per share, which is only slightly above the current trading price and would indicate analysts have very different opinions regarding whether they believe SanDisk's growth has already been priced in or not.

Critics point to specific issues: data shows that insiders have been selling shares over the past 3 months; SanDisk's GF Score (overall health) is a mere 46 out of 100; data reveals that only one-third of expected fiscal 2027 revenue is covered by contract, and approximately 60% of NAND production will likely be sold at spot market prices if supply is adequate.

Sandisk Corporation 2H Chart: Rebound from Ascending Trendline Support

SNDK has bounced off its uptrend line and found support just above $1,548. The RSI at 33.74 now shows oversold readings, signaling that the sell-off could be exhausting. A breakout above $1,892 could resume the rally towards $1,978. Alternatively, a break below $1,548 could open the road for a test of $1,414.

Sandisk Corporation Price Chart - Source: Tradingview

- Entry: Long above $1,892

- Target: $1,978

- Stop Loss: Close below $1,548

Bottom Line

The selloff on SAN disk was a broad sector rotation in AI and semis. Fundamentally, SAN disk has a solid long-term case based on strong AI demand for flash memory storage, its multidecade agreement with Kioxia, and robust capital spending from the hyperscalers. The upcoming key drivers will be the management guidance on enterprise SSD demand and NAND pricing, as well as the outlook on customers signing up longer 2027-28 agreements.

The strong rally over the past year may have pushed valuation to a point where market sentiment swings could lead to volatile moves until next earnings report, where better execution and guidance could be needed to push the stock higher.

Recommended Articles

Comments (0)

Click the $ button, enter the symbol, and select to link a stock, ETF, or other ticker.