[IN-DEPTH ANALYSIS] From Alarm Clocks to EVs: Why Texas Instruments’ Chips Are Your Next Big Bet

Key Takeaways

- Defensive Investment: Texas Instruments offers stable dividends and strong cash flow, supported by its defensive market position.

- Recovery Signs: Q1 2025 revenue grew 11% YoY, showing signs that the analog chip market may have bottomed out.

- Valuation: Target range of $155–$180, potentially 10% upside, reflecting modest growth expectations amid challenging industry conditions.

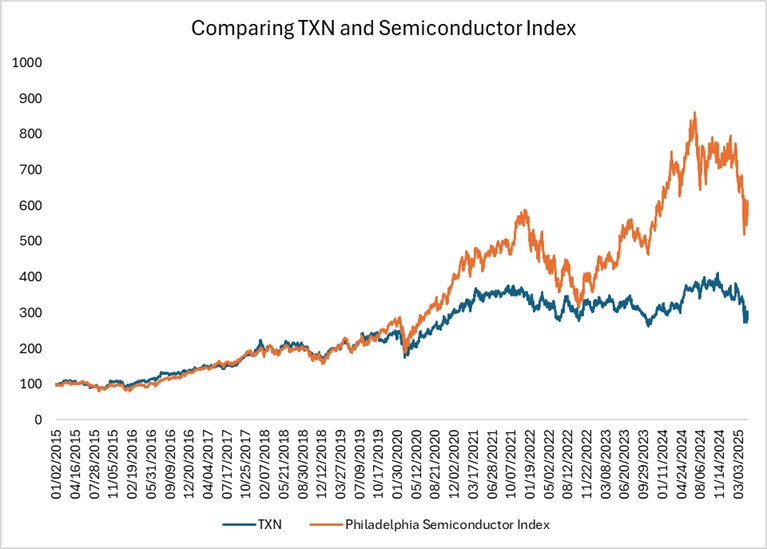

TradingKey - From the moment you wake up, Texas Instruments (TI) is there. Whether it’s the buzzing of your bedside alarm, the humming of your electric car in your garage, or the factory automation that brews your morning coffee, TI’s chips are the silent force behind it all. As a global leader in analog and embedded processors, TI powers everything from industrial machinery to cutting-edge medical wearables, and is embedded in every aspect of modern life. Yet despite TI’s pervasive influence, its stock price has lagged behind the semiconductor industry’s AI-driven boom. Can this defensive giant with a steady dividend and strong cash flow capitalize on the market recovery to regain its former glory?

Source: Set Jan 2nd 2015 as 100, Investing.com, TradingKey

Company Overview and Strategic Positioning

Headquartered in Dallas, Texas, TI is a global leader in the semiconductor industry. TI was founded in 1930 as Geophysical Services Incorporated (GSI) to perform seismic exploration for the oil industry. In the 1950s, TI transitioned into the electronics industry with the introduction of the silicon transistor (1954), the first integrated circuit for military use (1961), and the handheld calculator at Caltech (1967). Today, TI focuses on analog chips and embedded processors, serving the industrial, automotive, personal electronics, enterprise systems, and communications markets with more than 80,000 products and more than 100,000 customers, ensuring diversified revenues.

Faced with competition from Asia in the 1990s, TI focused on semiconductors and educational technology and divested non-core businesses (e.g., the defense business was sold to Raytheon and the memory chips were sold to Micron in 1997). Since the 2010s, TI has strengthened its analog and embedded processing portfolio. In 2020, TI received $1.61 billion in funding from the CHIPS Act to expand U.S. manufacturing, with the goal of achieving 95% wafer self-production by 2030 and building three new 300mm fabs in Texas and Utah.

TI's competitive advantage stems from its technological moat, with more than 50,000 patents and continued R&D investment (accounting for more than 15% of revenue), especially in the field of analog chips. Its global manufacturing network of 15 manufacturing bases (including 12 wafer fabs and 7 packaging plants) improves cost efficiency, and its 300mm fab strategy further enhances this advantage. TI's focus on long-life products and high customer stickiness makes it a strong defensive investment.

Product Competitiveness

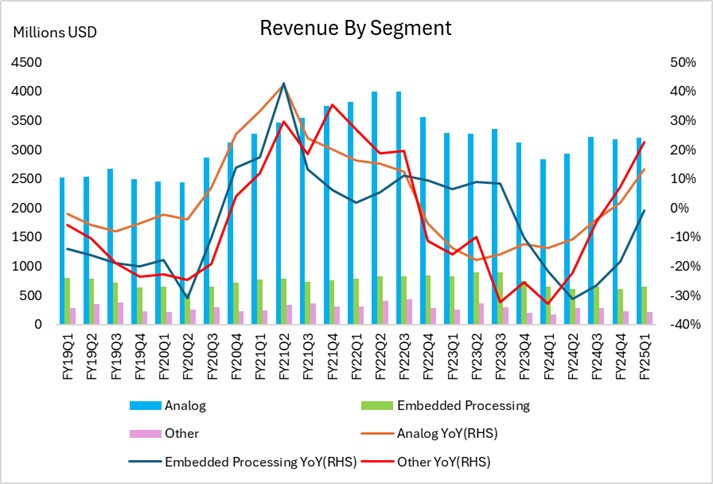

Texas Instruments produces two main types of chips: analog chips and embedded processors. These two categories account for most of the company's total revenue, about 94%. Other businesses such as DLP display technology and educational products (such as calculators) account for the remaining 6%.

Source: Company Financials, TradingKey

Analog

Analog chips help devices manage power and process various sensor signals. TI's analog chips mainly include two categories:

- Power management chips: used for battery management and power conversion, widely used in electric vehicles and industrial equipment to ensure efficient and stable power.

- Signal chain chips: including amplifiers, data converters and sensors, responsible for collecting and processing various signals such as sound, temperature, pressure, etc.

In 2024, TI launched a high-efficiency power chip using the new material "gallium nitride" (GaN). This chip is smaller in size and consumes less energy, which is particularly suitable for the high-efficiency needs of electric vehicles and industrial equipment.

Embedded Processors

Embedded processors are small computer chips that control the operation of machines and equipment, mainly including:

- Microcontroller (MCU): responsible for basic control and operation of equipment.

- Digital signal processor (DSP): used to process complex signals and data.

In 2024, TI released the world's smallest microcontroller, which is only 1.38 square millimeters in area and low cost, specifically for medical wearable devices. At the same time, TI also launched a new microcontroller with integrated artificial intelligence functions to help industrial and automotive equipment achieve accurate fault detection with an accuracy rate of up to 99%.

Other businesses

TI's DLP display technology and educational products (such as the TI-30 calculator) are still competitive in certain market segments and meet specific user needs.

Market Competition

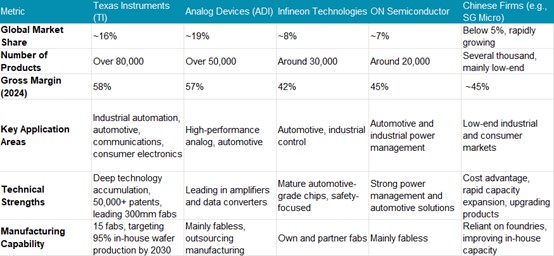

In the market competition, TI is the leader in the field of analog chips, with a market share of 16.1% in 2023, but the company faces multiple challenges. Analog Devices leads with a market share of 19.4%, especially in the high-performance analog chips and automotive markets; it has an advantage in the field of automotive-grade microcontrollers and power chips, especially in the rapid expansion of the Chinese market. ON Semiconductor directly competes with TI in the field of automotive and industrial power management. In addition, Chinese manufacturers such as Shengbang Microelectronics are accelerating substitution in the low-end analog chip market. In 2024, China's mature process production capacity will account for 28% of the world, intensifying price competition.

Source: TradingKey

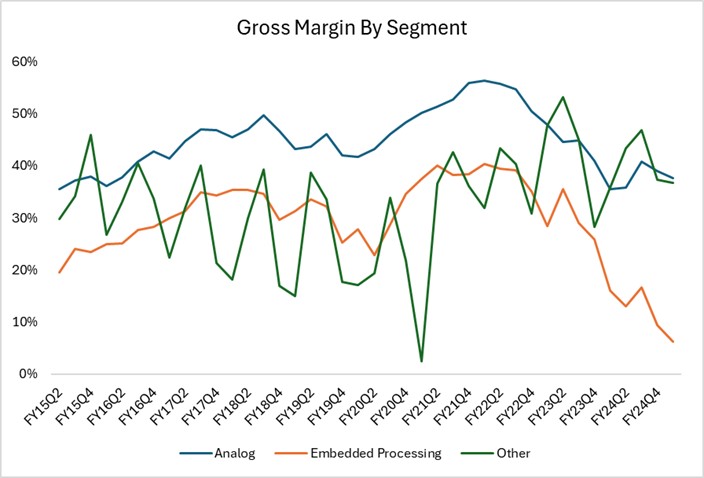

TI's advantages lie in its technological barriers, manufacturing scale and customer dispersion, but its embedded processor business is squeezed by competition from Infineon and Renesas, with revenue from this business falling 18% year-on-year in 2024.

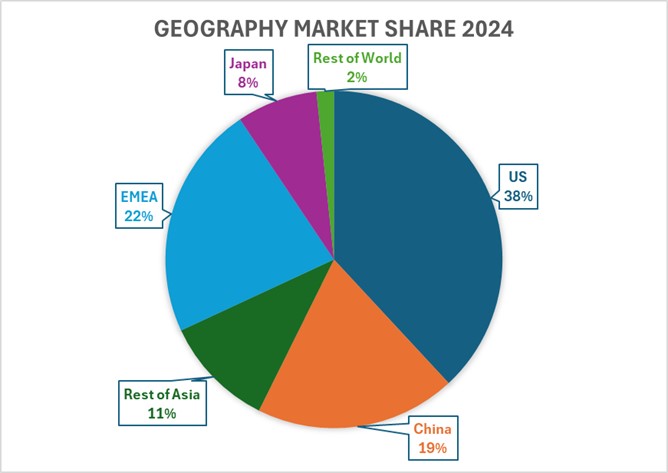

Customer and Terminal Market

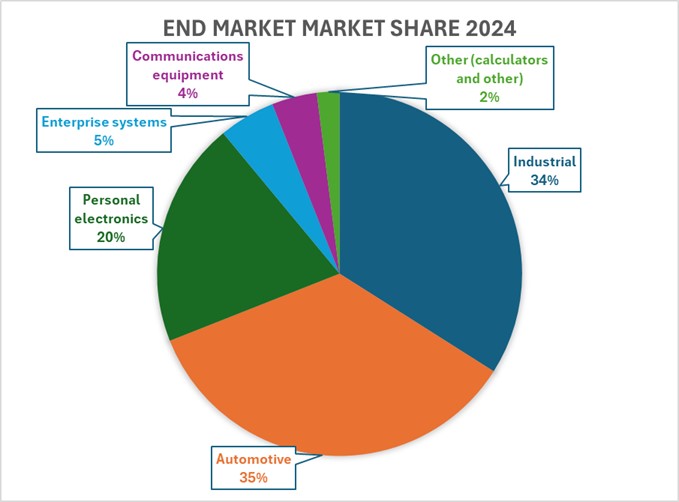

TI's customer base is highly dispersed, covering the industrial, automotive, personal electronics, enterprise systems and communications equipment markets, with more than 100,000 customers, and no single customer accounts for more than 10%, effectively reducing the risk of a single customer. The company's revenue is highly dependent on the industrial and automotive markets, which together account for 70% in 2024, which may amplify the impact of cyclical fluctuations.

Source: Company Financials, TradingKey

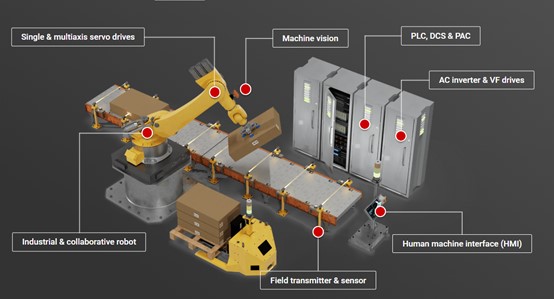

Industrials

Source: Texas Instruments

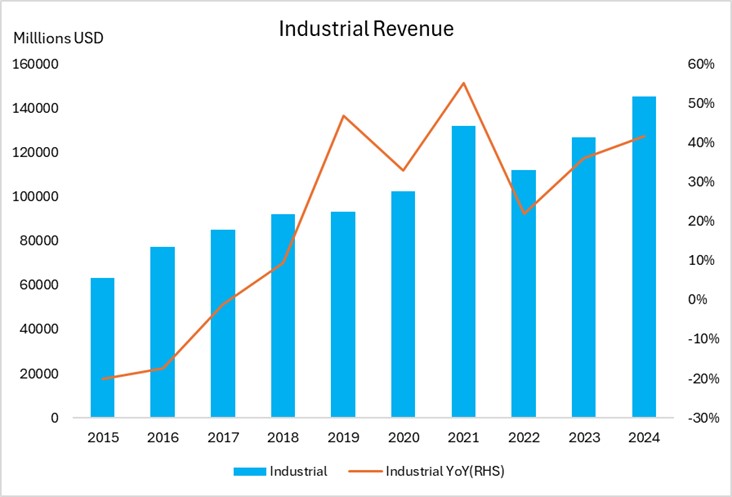

As TI's core growth engine, the industrial market will account for approximately 34% of the company's revenue in 2024. In the first quarter of 2025, the industrial market revenue reached $1.38 billion, an increase of 8-9% year-on-year, successfully ending the downward trend for seven consecutive quarters, showing strong recovery momentum. TI's sensors and MCUs are widely used in factory automation and energy infrastructure. The Chinese market is the main driving force. In 2025, the scale of China's industrial automation market is expected to exceed 300 billion RMB, investment continues to grow, and manufacturing PMI remains at 50.8, indicating that the manufacturing industry as a whole is in an expansionary trend. In contrast, the US manufacturing PMI reached 50.9 at the beginning of the year, entering the expansion range, but fell back to 49.8 in March, close to the edge of contraction, indicating that the recovery of the manufacturing industry is volatile. The European manufacturing PMI is about 48.2. Although it has rebounded continuously, it is still in the contraction range, and the economic recovery is limited.

Source: Company Financials, TradingKey

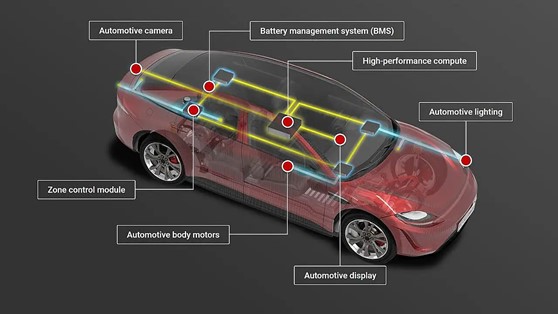

Automotive

Source: Texas Instruments

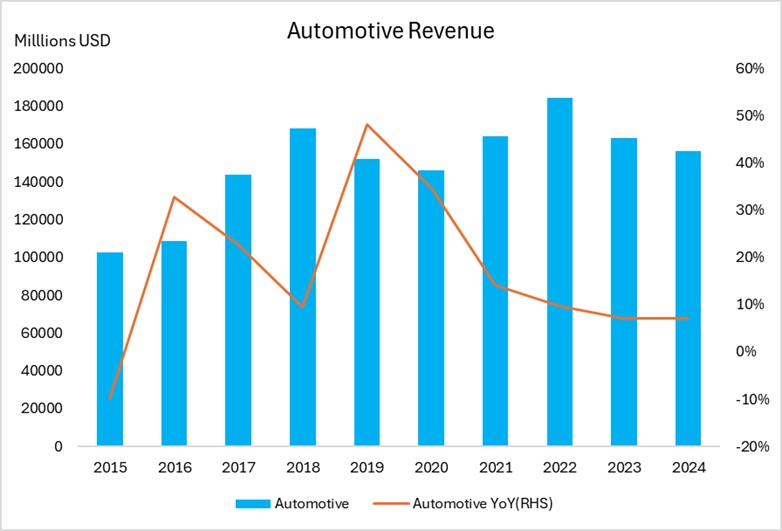

The automotive market is also an important pillar of TI, contributing about 35% of revenue in 2024. In Q1 2025, the automotive market revenue was about $1.4 billion, a year-on-year increase of 3-4%, but a month-on-month decrease of 5%, mainly due to seasonal factors.

Source: Company Financials, TradingKey

TI's customers in tthe automotive field include Chinese electric car manufacturers BYD and NIO, and traditional American car companies GM, Ford, and Tesla. China's new energy vehicle market is an important growth driver for TI. In Q1 2025, China's new energy vehicle sales reached approximately 3.075 million units, a year-on-year increase of 47.1%, accounting for 41.2% of total new car sales. This growth was mainly driven by mainstream car companies such as BYD, Geely, Xiaopeng, and Ideal. TI's battery management system chips and 77GHz millimeter wave radar sensors are in high demand. These chips help improve the safety and intelligence of electric vehicles and support advanced driver assistance systems (ADAS) and battery management functions.

Recent reports indicate that some imported semiconductor products from the United States have been exempted from additional tariffs by China. The adjustment covers eight tariff lines related to semiconductors and integrated circuits, excluding memory chips, and the import tariff has been reduced from 125% to 0%, with only a 13% value-added tax. This may be a positive for TI because its analog and embedded processing chips are essential to key areas such as automotive and industrial applications, where domestic alternatives may not yet fully meet demand. While the tariff reduction may ease the cost pressure on TI's US production, the company's global manufacturing operations in Malaysia, the Philippines and China, etc., further reduce tariff-related risks.

Source: Company Financials, TradingKey

The U.S. market accounts for about 30% to 35% of TI's automotive business revenue. Although the penetration rate of electric vehicles in the United States is still at a low level, about 7%-10% in 2024, the sales of electric vehicles in the United States in the first quarter of 2025 increased by about 11% year-on-year, part of the growth benefited from the early purchase of cars caused by the adjustment of tariff policies. Overall, although the electric vehicle market is developing rapidly, factors such as price and supply chain still pose certain restrictions on growth. The European market faces supply chain bottlenecks and high inflation pressure, and demand performance is relatively weak. The main customers include traditional automakers such as Volkswagen and BMW. The market challenges are relatively large, and the sales growth of new energy vehicles has slowed down.

Financial Performance

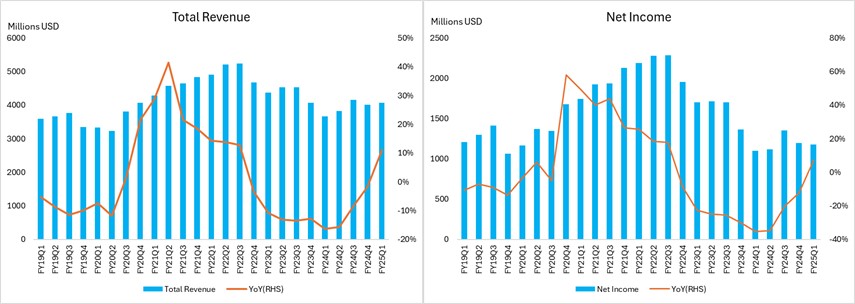

TI's financial performance is affected by both industry cycle fluctuations and internal operating strategies. From 2023 to 2024, the company's revenue and profits continued to decline due to weak demand and inventory backlogs. Total revenue in 2024 was $15.64 billion, a year-on-year decrease of 10.7%. Revenue in Q1 2025 rebounded to $4.07 billion, an increase of 11% year-on-year, ending two consecutive years of decline and exceeding market expectations.

Source: Company Financials, TradingKey

In terms of net profit, it will be $4.8 billion in 2024, a year-on-year decrease of 26%; in Q1 2025, the net profit will be $1.18 billion, a year-on-year decrease of 10%, but the earnings per share of $1.28 exceeded expectations, indicating that profitability has improved. TI's gross profit margin will drop from 63% in 2023 to 58% in 2024, and further to about 57% in the first quarter of 2025, mainly due to the cyclical downturn in the semiconductor industry. Weak demand has led to a decline in capacity utilization, and the company has to cut prices to maintain its market share, resulting in lower product prices and a weakened cost dilution effect, which has compressed gross profit margins.

Source: Company Financials, TradingKey

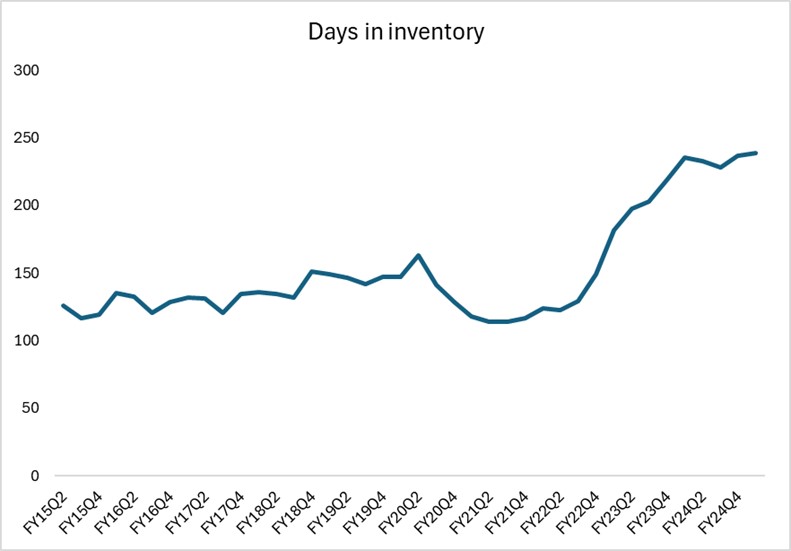

In terms of cash flow, operating cash flow in 2024 is $6.3 billion, and free cash flow is $1.5 billion, accounting for about 9.6% of revenue; operating cash flow in Q1 2025 is about $1.6 billion, and cash flow performance is stable. Inventory turnover days rose to 240 days in the fourth quarter of 2024, which was far higher than the industry's healthy level, reflecting inventory digestion pressure.

Source: Company Financials, TradingKey

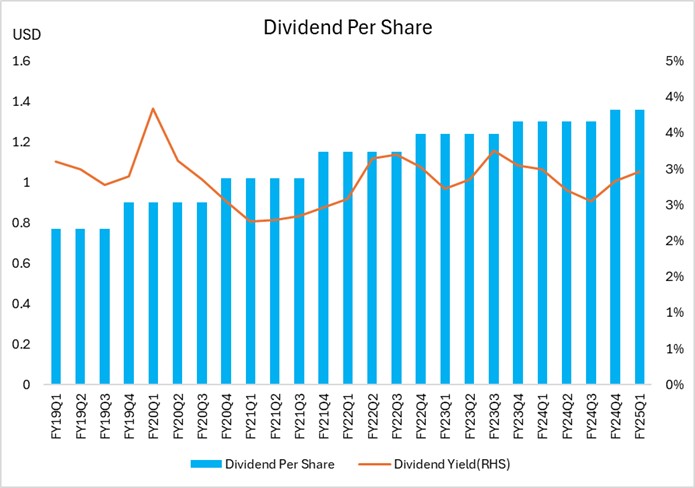

Capital expenditures are expected to be approximately $5 billion in 2025, mainly used to expand 300mm wafer fabs in the United States and strengthen high-end manufacturing capabilities. The company's full-year dividend in 2024 is approximately $5.20 per share, and it is expected to increase to $5.41 per share in 2025 at a growth rate of approximately 4%, with a dividend yield of approximately 3.6%, continuing to maintain its high-dividend stock characteristics. In 2024, TI repurchased approximately $1 billion in shares, and the repurchase plan will continue in the first quarter of 2025. Management is committed to using strong cash flow to support shareholder returns and increase earnings per share.

Source: Company Financials, TradingKey

Industry Background and Cycle Analysis

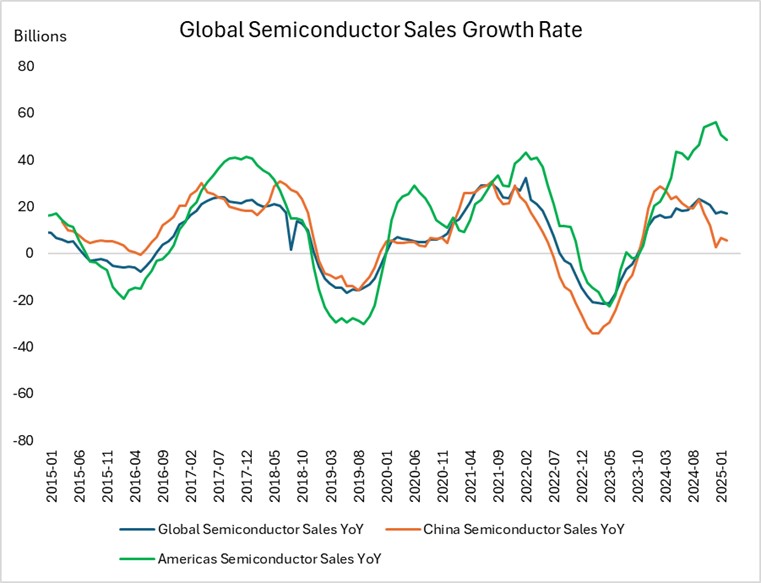

The global semiconductor industry has experienced dramatic cyclical fluctuations. In 2021, driven by chip shortages and the explosive demand for emerging technologies (AI, 5G, EV), the year-on-year growth rate of global semiconductor sales once reached a high of 25%-30%. Subsequently, in 2023, due to excess inventory and weak terminal demand, industry sales fell by about 15% year-on-year, reaching the trough of the cycle.

Source: Refinitive, TradingKey

Entering 2024, the industry began to gradually recover, and the global semiconductor market size reached US$627.6 billion, a year-on-year increase of 19.1%. It is expected to continue to grow by about 11.2% in 2025 (WSTS data), mainly driven by AI chips and memory chips (DRAM growth exceeded 80%), but the recovery of the analog chip market is relatively lagging, and it will still show a downward trend in 2024.

TI's industrial and automotive markets recovered by 8-9% and 3-4% in Q1 2025, ending two consecutive years of decline in 2023-2024. The growth and order improvement in the first quarter of 2025 are positive signs that the bottom may be approaching, but high inventory and conservative performance guidance indicate that the bottom has not yet been fully confirmed. About 30%-50% of the growth in the first quarter may be affected by tariff expectations, and the actual demand growth is estimated to be only 5%-7%, lower than the industry's overall growth rate of 19.1%. The recovery of the analog chip market lags behind that of AI and memory chips. TI needs to further digest inventory and stabilize orders in mid-2025 to truly confirm the turning point of the cycle and usher in sustained growth.

Valuation

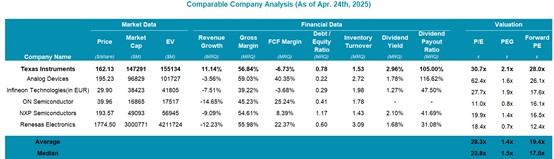

As a leading company in the field of analog chips, TI shows typical defensive investment value. Currently, TI's PE is about 30 times, slightly higher than the average level of the semiconductor industry, reflecting the market's recognition of its stable profitability, but also showing a certain valuation premium. TI is also a mature high-dividend stock, with a dividend of approximately $5.20 per share in 2024. Based on the current share price of $162, the dividend yield is about 3.2%, which is much higher than the S&P 500 average of 1.5%.

Based on the PE ratio and the dividend discount method for valuation, TI's reasonable target price range is $155 to $180. The lower limit of $155 is based on a more conservative earnings growth expectation and valuation level. It assumes that the EPS in the next 12 months will be about $6.0, and adopts a PE of about 26 times, reflecting the cautious expectation of TI's earnings recovery in the current industry environment. The upper limit of $180 is mainly derived from the dividend discount model (DDM). Assuming that the expected dividend in 2025 is $5.4 and the dividend growth rate is 4%, we calculate the discount rate to be 7% considering the market risk premium. The calculated reasonable share price is about $180, which reflects TI's stable cash flow and continuously growing dividend returns.

Overall, TI's valuation reflects its characteristics as a defensive asset at the bottom of the cycle. Although its growth potential is limited, its stable profitability, strong cash flow and generous dividend returns make it very attractive in the current market environment.

Source: Company Financials, TradingKey