[IN-DEPTH ANALYSIS] Chipotle: How to Maintain Dominance under Tariff Storm

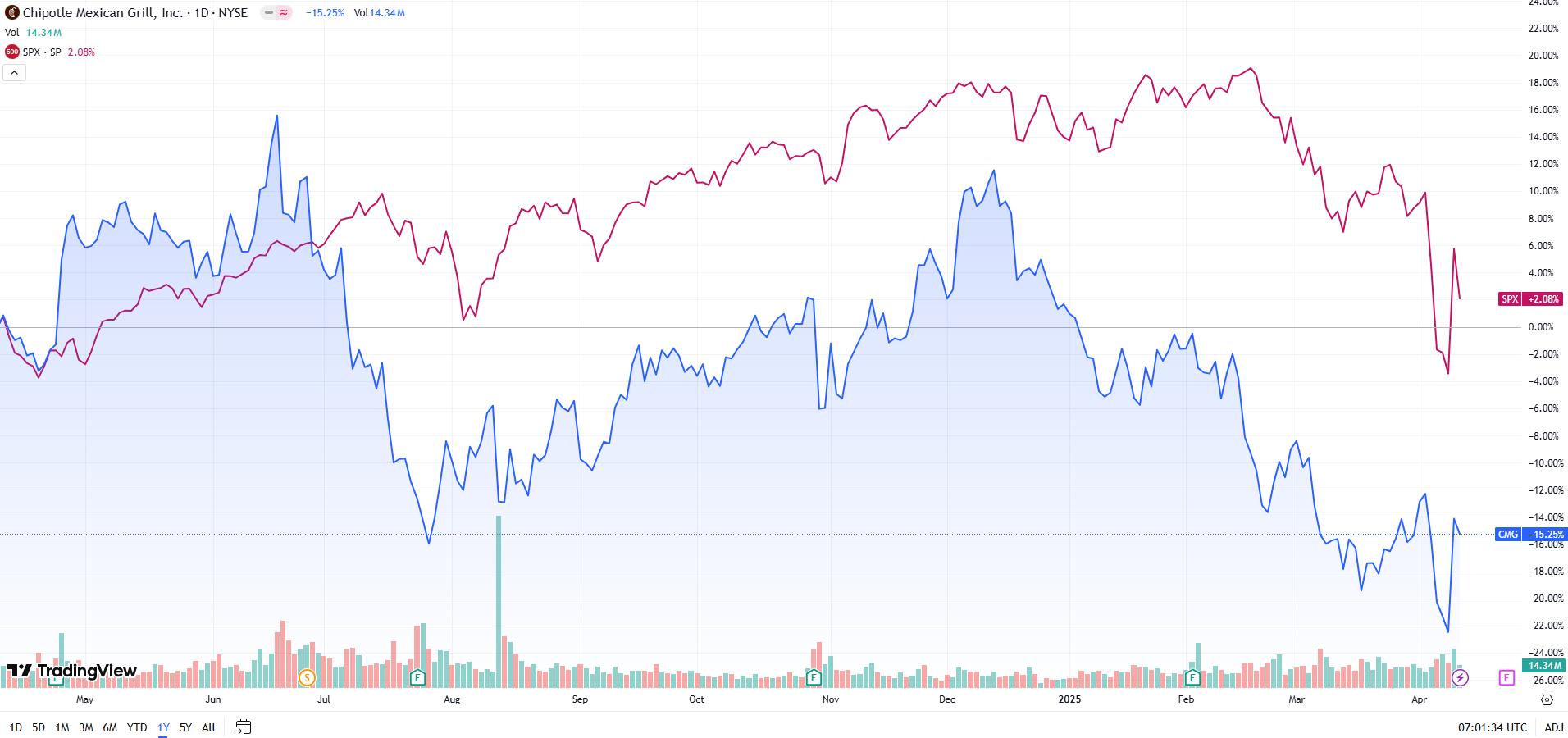

Source: TradingView

1. Key Takeaways

Cost Pressure Mitigation: Facing an around 0.6% cost increase due to tariffs and immigration policies, Chipotle absorbs costs through automation (e.g., Autocado), supply chain diversification, and cautious pricing (2% increase), avoiding significant price hikes in the short term.

Robust Financial Resilience: A strong balance sheet supports expansion and stock buybacks, offering greater risk resistance and lower stock volatility compared to leveraged competitors.

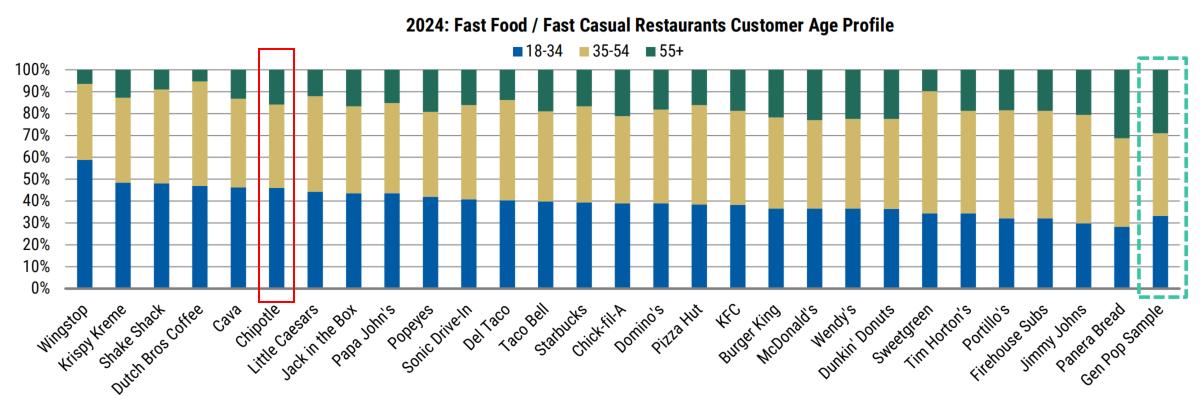

Healthy Brand Advantage: Anchored by the “Food with Integrity” philosophy, 100% fresh, non-GMO ingredients attract 18-34-year-old consumers, with highly customizable menus enhancing brand loyalty.

Digital Transformation Empowerment: Mobile ordering, Chipotlane, and AI optimization drive same-store sales growth, increase digital sales share, and reduce food waste by 10%.

Intensifying Market Competition: Threats from CAVA, Sweetgreen, and Taco Bell’s premium offerings grow, requiring Chipotle to innovate to maintain its 25% fast-casual market share.

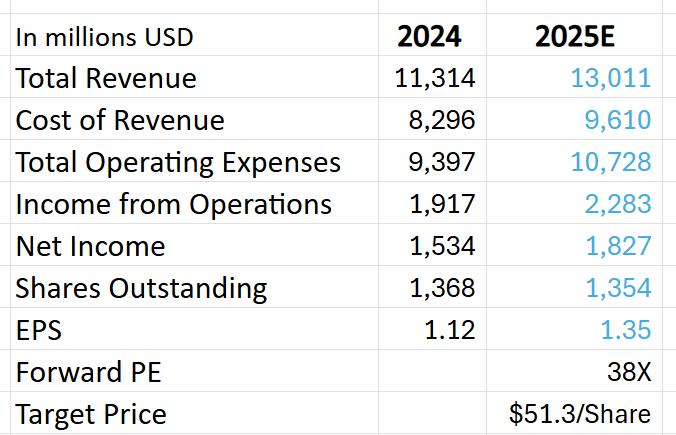

Conservative Valuation Outlook: A 2025 P/E ratio of 38x, with a target stock price of $51.3, reflects steady growth expectations under macroeconomic pressures.

2. Company Overview

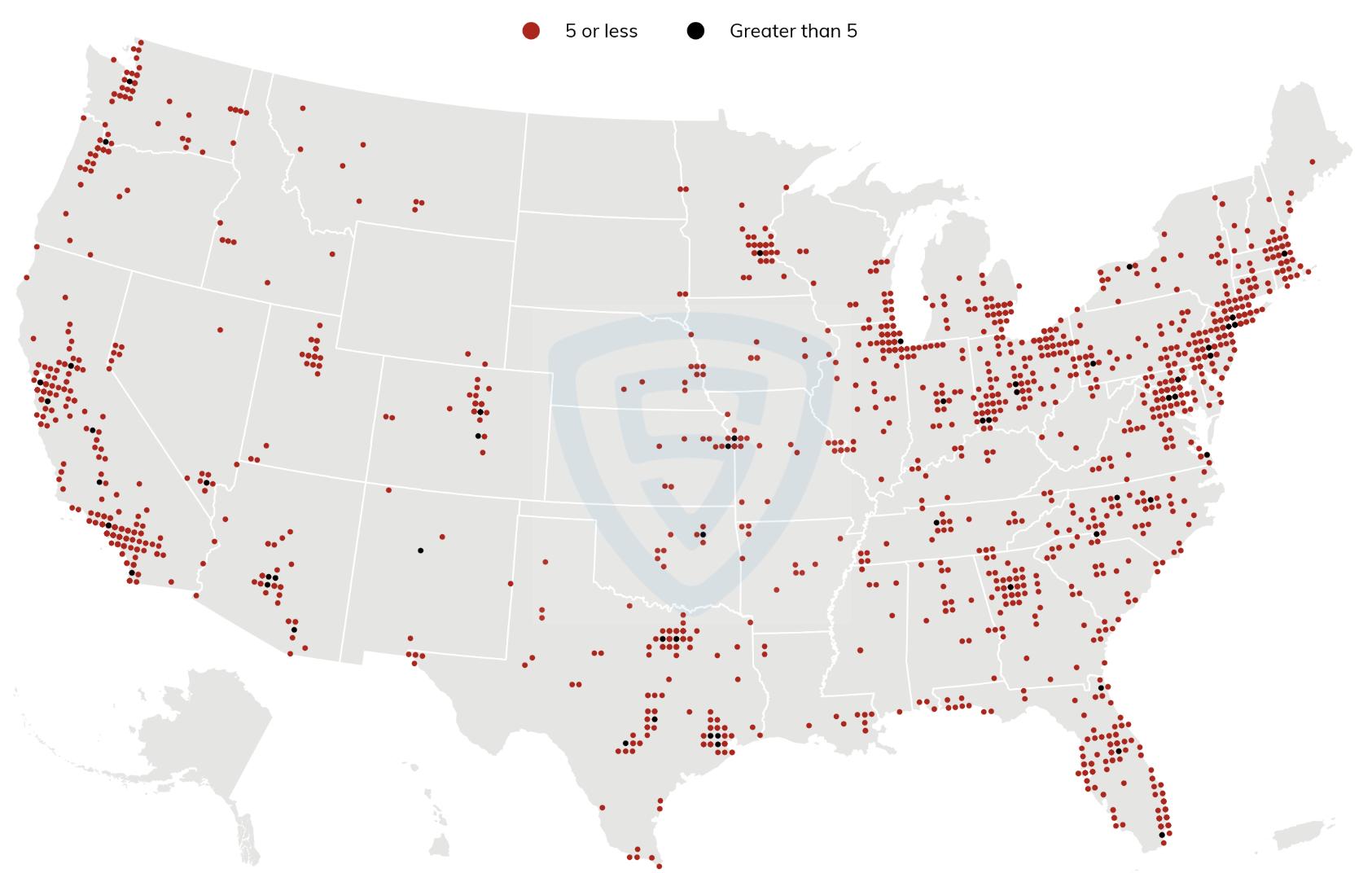

TradingKey - Chipotle Mexican Grill, Inc., an American fast-food chain founded in 1993, has grown from a single store to a global restaurant giant with over 3,700 restaurants, driven by its “Food with Integrity” philosophy. Nearly 98% of Chipotle's stores are in the U.S., primarily in densely populated and high-consumption areas, with only 2% in Europe and Canada. Chipotle offers customizable Mexican-style burritos, bowls, and salads, catering to consumer demand for health and convenience.

Source: Scrapehero

3. What Makes Chipotle Stand Out?

Source: TradingKey, Chipotle

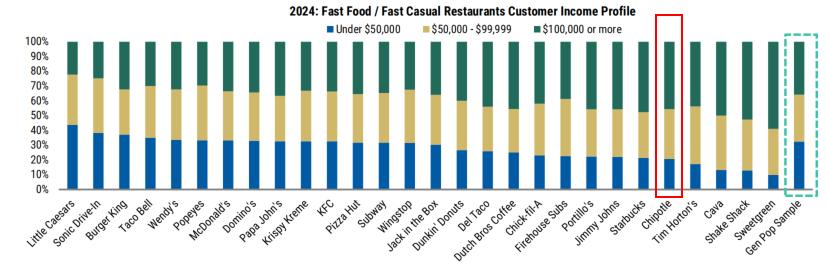

Unique Market Positioning: Through precise market positioning, Chipotle blends the convenience of fast food with the quality and health of casual dining, defining the “fast-casual” category. By the end of 2024, Chipotle holds around 25% of the U.S. fast-casual dining market, leading the industry. It provides efficient service while attracting consumers, especially higher-income ones, with premium ingredients and a comfortable dining environment, securing a foothold in the competitive restaurant market.

Source: AlphaWise, Morgan Stanley Research

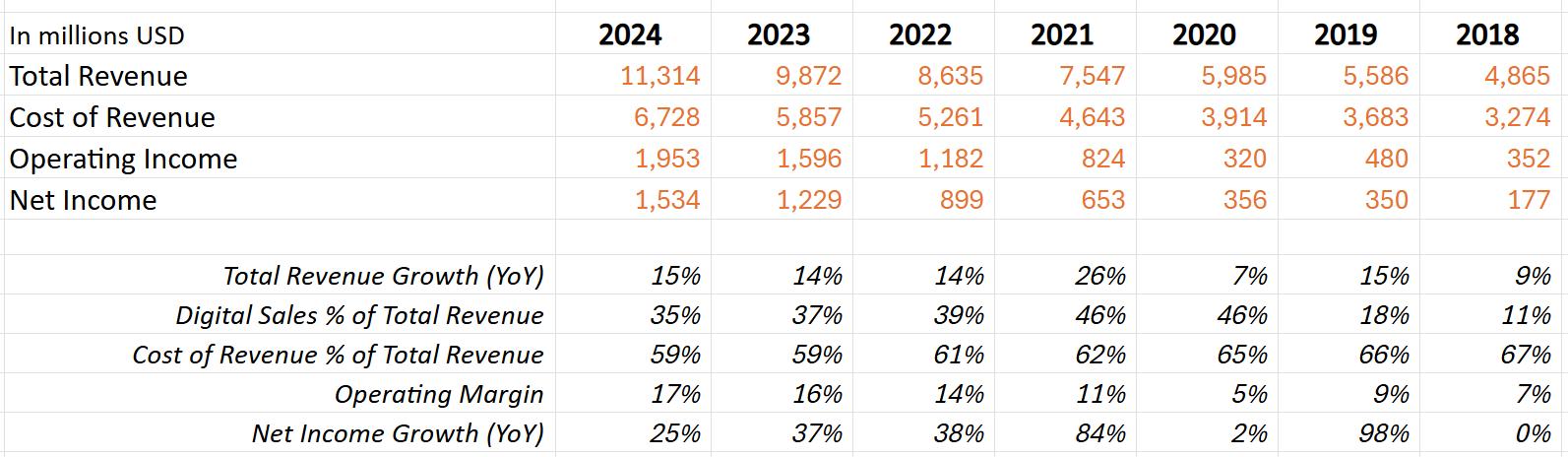

Food with Integrity: Chipotle’s brand cornerstone is its commitment to 100% fresh, non-GMO, hormone-free ingredients. This focus on high-quality ingredients results in a higher cost-to-revenue ratio but serves as a competitive advantage, attracting loyal customers and driving double-digit revenue growth. In an era of heightened food safety concerns, this “fresh and healthy” philosophy resonates strongly with 18-34-year-old consumers, a group with strong spending power and high brand loyalty, forming Chipotle’s most solid competitive moat.

Source:AlphaWise, Morgan Stanley Research

Highly Customizable Menu: Chipotle’s menu is simple yet versatile, offering over 65,000 combinations, allowing customers to freely customize burritos, bowls, or salads to match personal tastes and dietary preferences. This highly personalized experience boosts customer satisfaction, aligns with modern consumers’ demand for diverse, tailored dining options, and strengthens brand stickiness.

Digital Transformation: Since 2018, former CEO Brian Niccol made digital transformation a strategic priority. Optimized mobile apps and online ordering have driven steady same-store sales growth. Chipotlane drive-thru services reduce customer wait times and boost operational efficiency, with Chipotlane locations achieving 10-15% higher sales and 5-6% higher margins than traditional stores. AI and automation optimize ingredient preparation and inventory management, cutting food waste by 10% and improving order accuracy. As digital sales continue to grow, they not only solidify market share but also significantly enhance profitability.

Source: TradingKey, Chipotle

Robust Supply Chain Management: Chipotle’s supply chain system tracks ingredients from farm to restaurant, significantly reducing recall response times. It supports sustainable and local sourcing, prioritizing farms within 350 miles of restaurants to shorten transport distances and ensure freshness. Additionally, increasing supplier numbers and expanding geographic sourcing reduces single-supplier risks.

4. What Issues Does Chipotle’s Current Stock Price Reflect?

Source: TradingKey, Chipotle

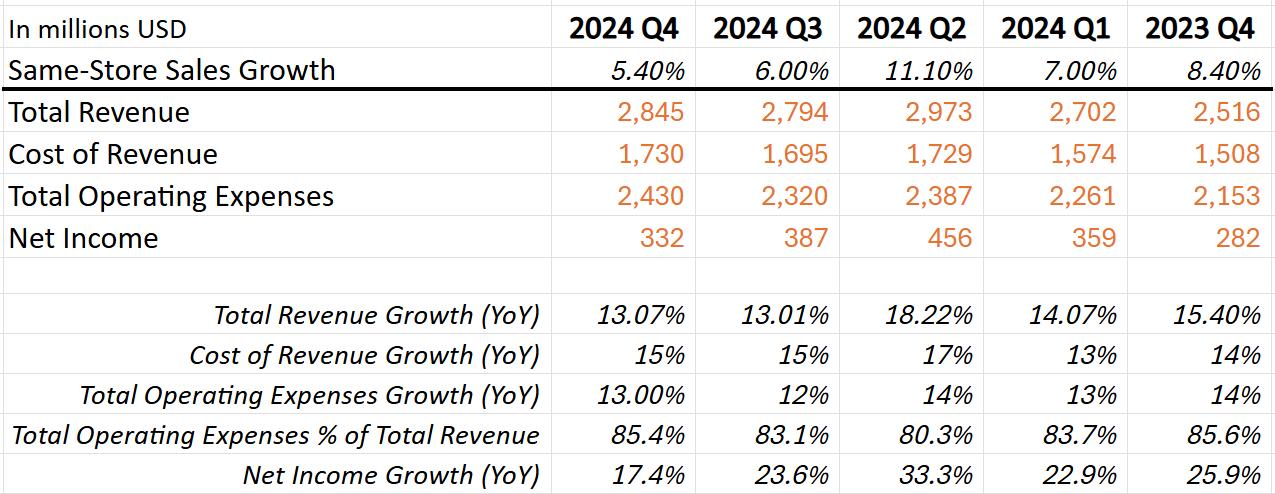

As a consumer growth stock, Chipotle’s performance over the past year contrasts sharply with the strong S&P 500 trend. Its stock price weakness stems from: sluggish same-store sales growth, uncertainty from executive changes, rising food, labor, and administrative costs, weather-related sales impacts, and adverse macroeconomic conditions. These factors, particularly in a high-inflation environment with weakened consumer spending, have constrained Chipotle’s pricing power, slowing net income growth.

5. How Significant Is the Impact of Tariffs on Chipotle?

Source: TradingKey, Chipotle

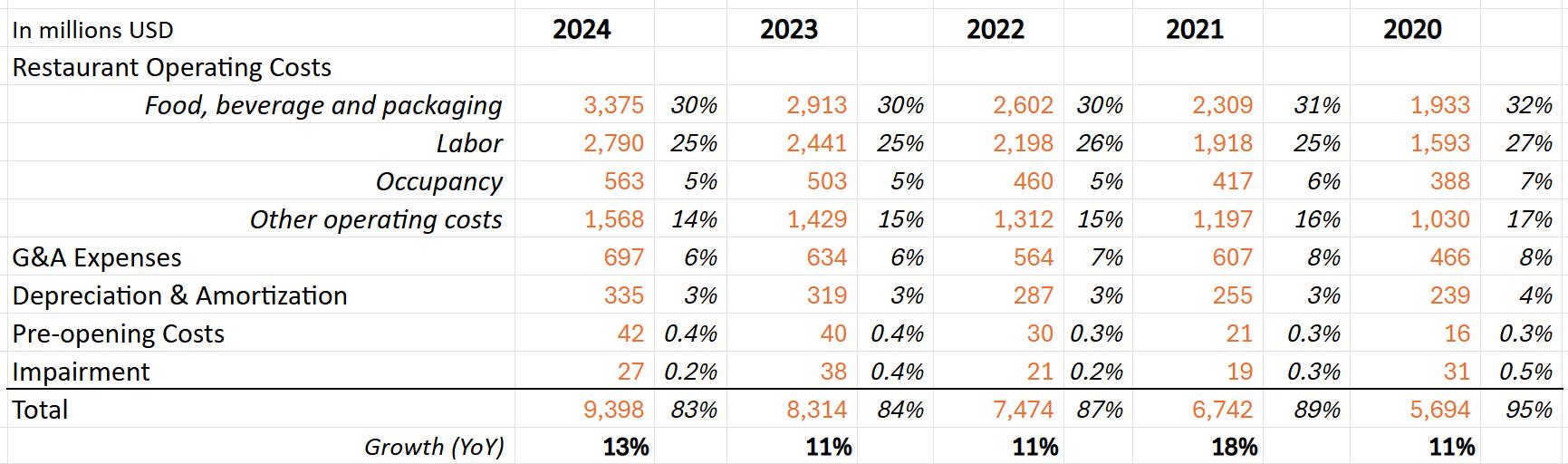

Chipotle’s operating costs primarily include ingredient procurement, labor, rent, marketing, and equipment maintenance. Labor and ingredient costs are particularly sensitive to tariffs and immigration policies. Stricter immigration policies may lead to labor shortages, especially in the restaurant industry, which relies heavily on immigrant labor, driving up wages and cost pressures. Meanwhile, tariffs may increase prices for some imported raw materials, challenging ingredient costs.

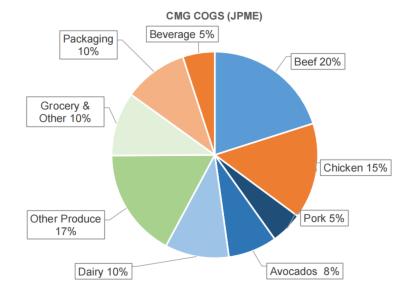

Chipotle’s top-selling products, such as Chicken Burrito, Lifestyle Bowls, and Guacamole, rely on beef, chicken, cheese, avocados, and beans as core procurement items. Mexico is Chipotle’s largest avocado supplier, accounting for around 50% of its avocado purchases. While Chipotle does not disclose specific beef sources, Mexico, a key U.S. beef supplier, likely contributes. In contrast, chicken and beans are primarily sourced domestically, with low import reliance and minimal tariff impact. As the world’s largest cheese producer, the U.S. supplies nearly all of Chipotle’s cheese, with negligible tariff effects. Other ingredients like tomatoes and peppers also face limited tariff-related cost impacts.

Source: Company reports and J.P. Morgan estimates

6. Chipotle’s Cost Hedging Strategies

Facing potential risks from rising tariffs and labor costs, Chipotle’s management states that the company can mitigate performance impacts through multiple strategies, including technological upgrades, supply chain optimization, and cost absorption.

Automation and Technology Investments: To address cost pressures, Chipotle is accelerating automation adoption, introducing tools like production slicers, Autocado (automated avocado processing), and Hyphen (automated bowl and burrito lines). These technologies aim to reduce labor time and boost efficiency. Estimates suggest that from mid-2025, these optimizations could improve margins by 25-30 basis points, significantly shortening food preparation times and further lowering labor costs.

Supply Chain Optimization: To reduce reliance on single markets, Chipotle is diversifying raw material sourcing. For avocados, it has increased procurement from Colombia, Peru, and the Dominican Republic. In its February 2025 earnings call, CEO Scott Boatwright noted that this diversification strategy is expected to effectively offset some cost pressures from tariff increases.

Cautious Pricing Strategy: Chipotle opts for below-industry-average price adjustments (around 2% vs. industry 3%+), absorbing some costs to maintain consumer value. This approach is critical in an inflationary environment, as price-sensitive young consumers may switch to alternatives if prices rise. By balancing cost absorption with competitiveness, Chipotle aims to protect market share while sustaining brand appeal.

7. Investment Outlook and Valuation

Chipotle plans to open 315-345 new stores in 2025, with over 80% featuring Chipotlane drive-thru lanes to boost efficiency and margins. Facing cost pressures from tariffs and tighter immigration policies, the company will absorb these costs through internal optimization, avoiding price hikes in the short term to preserve consumer value. Management expects tariffs to have limited revenue impact initially, but immigration policies and tariff adjustments may raise costs by around 0.6%.

Chipotle’s no debt and ample cash financial position supports ongoing expansion and innovation. Its net income conversion rate remains robust and continues to improve. Recently, the company has used excess cash for stock buybacks, a trend expected to persist. Unlike peers facing debt refinancing pressures in a high-interest-rate environment, Chipotle’s no-debt structure shields it from such risks. Chipotle's financial resilience is highly favored by investors like Bill Ackman, whose Pershing Square Capital Management has long held a $1.486 billion stake in Chipotle, accounting for 11.74% of its portfolio, enabling stronger risk resistance in environments with potentially weak consumer spending and lower stock volatility compared to highly leveraged peers.

However, Chipotle faces multiple challenges in 2025. First, U.S. consumer confidence may decline due to tariff changes, dragging down overall market performance. Despite Chipotle’s strong balance sheet and pricing advantages, it may still be affected by industry downturns. Second, intensifying competition from CAVA, Sweetgreen, Qdoba, and Taco Bell’s premium lines requires continuous innovation to maintain its leading position. While the fast-casual market retains growth potential, Chipotle must innovate to solidify its dominance.

Source: Macrotrends

Considering these factors, we assign Chipotle a conservative 2025 P/E ratio of 38x. Accounting for macroeconomic cost pressures, the estimated fair target stock price for 2025 is $51.3.

Source: TradingKey